- Automotive Components & Materials

- Automotive Drive Shaft Market

Automotive Drive Shaft Market Size, Share, and Growth Forecast, 2025 - 2032

Automotive Drive Shaft Market by Product Type (Hollow, Solid), Position (Front, Rear), Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs)), and Regional Analysis for 2025 - 2032

Automotive Drive Shaft Market Share and Trends Analysis

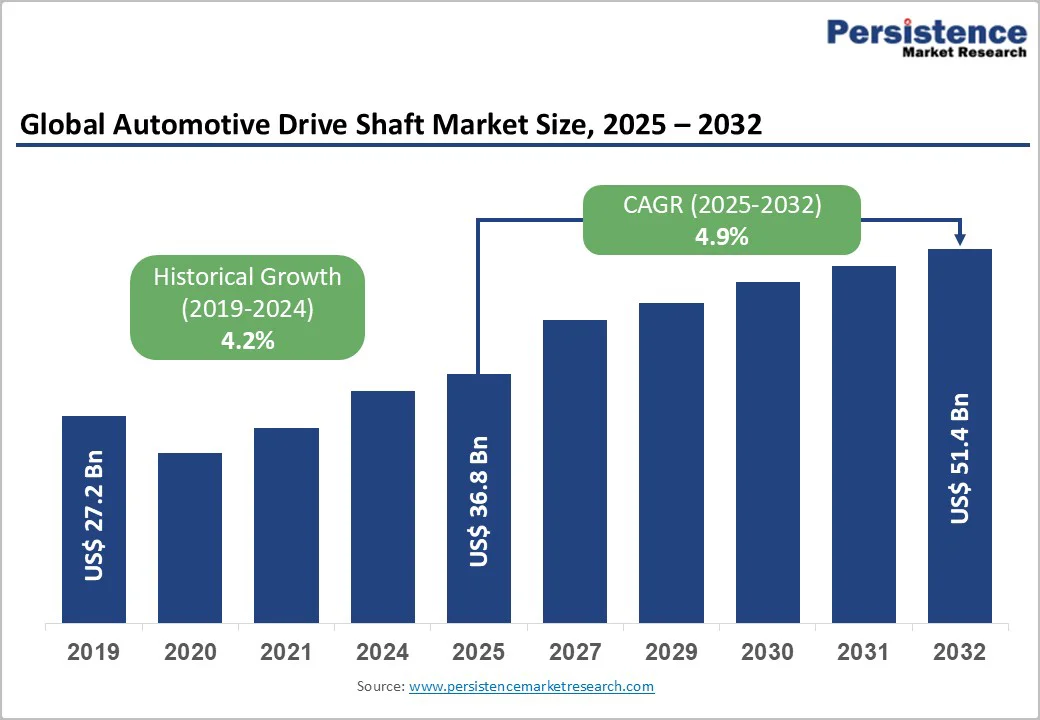

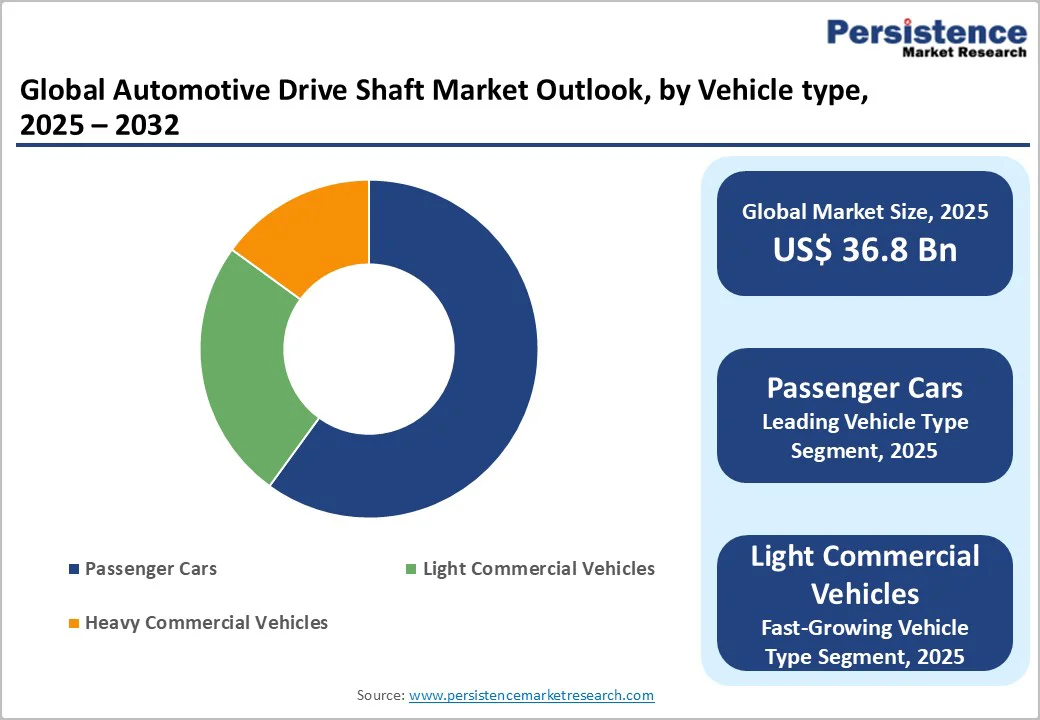

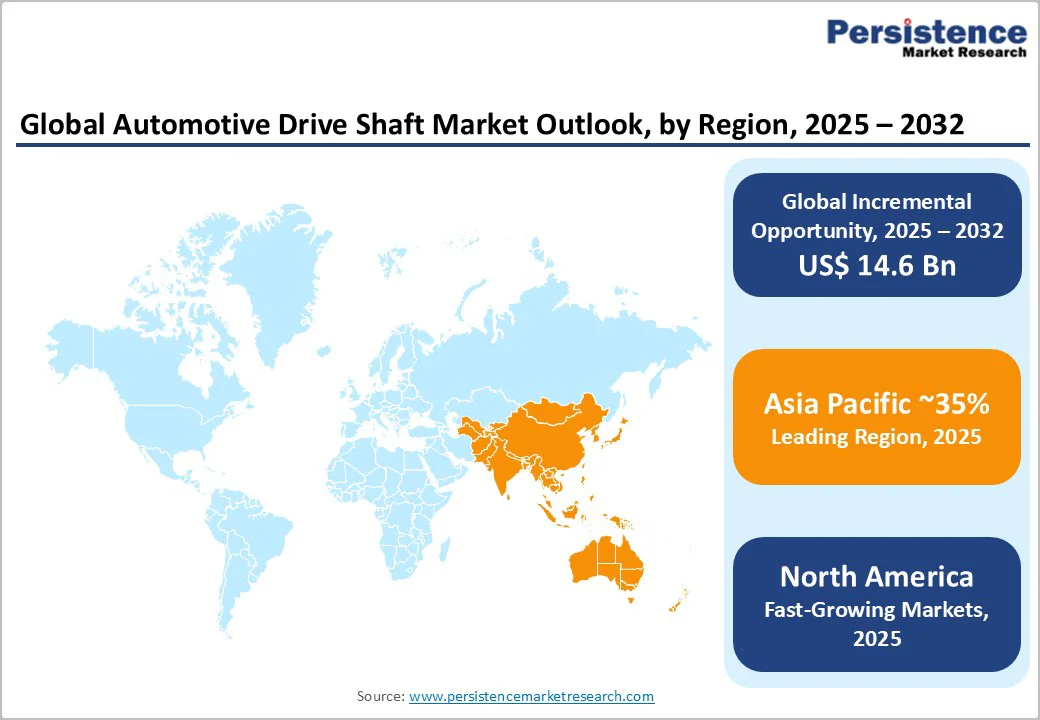

The global automotive drive shaft market size is likely to be valued at US$ 36.8 billion in 2025, and is projected to reach US$ 51.4 billion by 2032, growing at a CAGR of 4.9% during the forecast period 2025-2032. Stringent government fuel economy and emissions mandates worldwide are accelerating the adoption of lightweight hollow drive shafts engineered from advanced materials including carbon fiber and aluminum alloys, which reduce vehicle mass while maintaining structural integrity and high-torque transmission capabilities.

Rapid electrification of vehicle powertrains is fundamentally reshaping drive shaft design requirements, compelling manufacturers to develop specialized, low-vibration, torque-optimized systems tailored to unique EV architectures and battery layouts. The commercial heavy-duty vehicle segment and thriving aftermarket demand driven by expanding global vehicle production continue bolstering market expansion.

Key Industry Highlights

- Dominant Product Type: Hollow drive shafts dominate with a commanding 57.2% revenue share in 2025, driven by their ability to reduce vehicle weight and enhance fuel efficiency.

- Fastest-growing Product Type: Solid drive shafts are expected to grow the fastest from 2025 to 2032, owing to their widening adoption in high-torque and performance applications.

- Leading Position: Rear drive shafts lead with approximately 63.1% share, supported by their widespread use in rear-wheel-drive (RWD) and all-wheel-drive (AWD) systems.

- Fastest-growing Position Segment: Front drive shafts are the fastest-growing segment, driven by the proliferation of AWD platforms requiring multiple shafts per vehicle to enhance traction and handling.

- Leading Vehicle Type: Passenger cars dominate with 68.5% market share, powered by their massive production volumes and consistent single rear-shaft configurations.

- Fastest-growing Vehicle Type: Light commercial vehicles are likely to post the highest 2025-2032 CAGR due to the surge in e-commerce logistics and last-mile delivery demand.

- Regional Leadership: Asia Pacific commands 35% of the global market share, and the regional is also predicted to grow the fastest at about 7.2% CAGR, led by the strong automotive production capacities of China and India.

- Competitive Scenario: GKN Driveline leads with an estimated 19% market share, with Dana, Schaeffler, and American Axle & Manufacturing maintaining strong global positions through investments in advanced composite materials and multi-motor architecture drive shafts.

| Key Insights | Details |

|---|---|

|

Automotive Drive Shaft Market Size (2025E) |

US$ 3.98 Bn |

|

Market Value Forecast (2032F) |

US$ 22.7 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

30.4% |

|

Historical Market Growth (CAGR 2019 to 2024) |

27.5 % |

Market Factors - Growth, Barriers, and Opportunity Analysis

Electric Vehicle (EV) Proliferation and Drivetrain Architecture Evolution

According to the International Energy Agency (IEA), global electric car sales surpassed 17 million units in 2024, representing nearly 20% of the total vehicle sales. This has the potential to result in an exponential demand growth for specialized drive shafts accommodating unique EV powertrain configurations requiring different torque characteristics and positioning compared to internal combustion engine (ICE) vehicles. Surging EV market growth across developed and emerging markets drives proportional increase in drive shaft production through dual-motor AWD configurations, increased all-wheel-drive adoption, and emerging mid-motor designs requiring specialized shaft architectures.

Tesla's Giga Berlin and Shanghai expansion, established EV plants, and new Chinese manufacturer emergence including BYD and NIO accelerate regional production capacity requiring localized drive shaft supply chains. The inherent low center of gravity and torque vectoring capabilities of EVs enable innovative drivetrain designs including central drive shafts and multi-motor systems requiring premium lightweight shafts, with aluminum and carbon fiber implementations raising average shaft content value per vehicle by more than a quarter versus traditional vehicles.

Supply Chain Disruptions and Raw Material Cost Volatility

Being heavily dependent on steel, aluminum, and composite material sourcing, drive shaft manufacturing can get disturbed quickly by commodity price fluctuations and supply chain disruptions. These challenges are strongly correlated with global economic conditions and geopolitical tensions affecting manufacturing costs and pricing stability. Steel tube sourcing from traditional suppliers including Mexico, China, and India faces tariff barriers and supply chain constraints, with severe cost impacts during trade tension periods affecting final drive shaft pricing and manufacturer margins. Aluminum and carbon fiber material supply chain volatilities directly impact hollow and composite drive shaft profitability, with small-to-medium manufacturers lacking hedging capabilities exposed to significant margin compression.

Drive shaft manufacturing needs precision bearing tolerances, balanced component assembly, and vibration control, creating high technical barriers and quality requirements and elevating production costs. Hollow drive shaft design optimization involving finite element analysis, simulation, and iterative development requires significant R&D investment limiting manufacturer participation to well-capitalized enterprises. Moreover, specialized equipment including balancing machines, universal joint installation equipment, and vibration testing infrastructure entails substantial capital investment, constraining market entry for new competitors. Supply relationship requirements of original equipment manufacturers (OEMs) including IATF 16949 certification, component traceability documentation, and rigorous quality assurance processes has erected structural barriers protecting established suppliers.

Vehicle Production Expansion and Supply Chain Localization in Emerging Markets

Rapidly developing economies across Asia Pacific, Latin America, and India are creating unprecedented opportunities for drive shaft manufacturers through explosive vehicle production growth. India's expanding automotive sector is driving proportional demand for locally manufactured drive shafts that reduce import dependency and enhance cost competitiveness. China's strategic pivot from ICE dominance toward EV manufacturing is simultaneously opening specialized market segments for electrically-optimized drive shaft architectures designed specifically for emerging EV manufacturers. Southeast Asian nations, including Indonesia, Thailand, and Vietnam, are rapidly establishing automotive manufacturing hubs through government incentives and international OEM investments, collectively representing a supply opportunity of over US$ 2 billion that requires localized infrastructure development and supply chain partnerships.

Three-dimensional (3D) printing and advanced composite manufacturing technologies are fundamentally reshaping drive shaft production economics, enabling customized designs optimized for specific vehicle architectures while simultaneously reducing production costs by 20–35% compared to traditional forging and machining methodologies. Carbon nanotube-reinforced composite drive shafts represent the frontier of materials innovation, achieving over 50% weight reductions relative to aluminum while maintaining structural strength, creating premium vehicle applications with pricing power. The advanced manufacturing drive shaft segment is projected to establish a strong market presence by 2032 as production costs decline and technical capabilities mature, positioning early-stage adopters to capture significant market share within high-performance and luxury automotive segments.

Category-wise Analysis

Product Type Insights

Hollow drive shafts dominate the market with about 57.2% revenue share in 2025, driven by their ability to deliver 25% weight reduction compared to solid shafts while maintaining high torque transmission efficiency. Their lightweight design enhances fuel efficiency, supports emission compliance, and improves drivetrain smoothness through lower rotational inertia and reduced vibration sensitivity, enhancing overall noise, vibration, & harshness (NVH) performance. Aluminum hollow shafts enable additional weight savings at moderate cost, supporting adoption across sedans, crossovers, and light trucks, while steel hollow shafts remain the volume leader due to cost-effectiveness and established production infrastructure.

Meanwhile, solid drive shafts are the fastest-growing segment, forecasted to register an estimated 5% CAGR between 2025 and 2032, aided by the widespread demand for high-torque commercial vehicles, performance cars, and EVs, where maximum strength and rigidity are prioritized overweight optimization.

Position Insights

Rear drive shafts dominate with approximately 63.1% of the automotive drive shaft market revenue share in 2025, on account of their essential role in RWD and AWD vehicles, transmitting power from the transmission to the rear axle. With RWD vehicles accounting for over 45% of global production, rear shafts ensure a stable and recurring demand base. The growing adoption of AWD systems further amplifies rear shaft needs, as these architectures require additional components for balanced power distribution. The critical safety and durability requirements of rear shafts also command premium pricing.

On the other hand, front drive shafts are poised to grow the fastest at around 6% CAGR through 2032, fueled by the rising adoption of AWD and front-motor EV, especially in SUVs and crossovers, enhancing vehicle traction and performance across key global markets.

Vehicle Type Insights

Passenger cars lead the market with an estimated 68.5% revenue share in 2025, supported by high production volumes exceeding 50 million units annually and universal adoption across economy to luxury segments. The standard single rear-shaft configuration of passenger cars ensures a stable, recurring demand for conventional drive shafts. Premium and luxury models from German, Japanese, and Chinese brands are increasingly adopting all-wheel-drive systems, doubling shaft requirements and enhancing per-vehicle value.

Meanwhile, light commercial vehicles (LCVs) represent the fastest-growing segment at 7% CAGR, driven by rapid e-commerce expansion, urban logistics, and rising demand for delivery vans and pickup trucks. Higher torque needs and increasing AWD adoption have elevated component content per vehicle, while major OEMs such as Ford, GM, and Chinese manufacturers are expanding production to meet last-mile delivery growth.

Regional Insights

North America Automotive Drive Shaft Market Trends

North America commands a central position in the global market for automotive drive shafts, powered by a strong regional OEM presence and established supply chain infrastructure. The United States dominates this regional landscape with 36.6% of the market share, supported by vehicle production exceeding 10 million units annually, substantial pickup truck and SUV market penetration, and a deeply entrenched automotive supply base developed over decades of industry consolidation and specialization. The U.S. light truck market, capturing over 80% of domestic production preferences, generates exceptional demand for multiple drive shafts per vehicle, driving 20–25% higher per-vehicle shaft content compared to global averages and enhancing market penetration depth.

Stringent regulatory frameworks, including the Corporate Average Fuel Economy (CAFE) standards and state-level emissions regulations, are accelerating the adoption of hollow drive shafts and lightweight advanced materials, creating competitive differentiation and sustained demand for next-generation technologies. The Canadian automotive sector also contributes around 10–12% of regional market share through tightly integrated North American supply chains that facilitate cross-border component flows and coordinated vehicle production strategies, further consolidating the region's position as a mature, high-value market segment.

Europe Automotive Drive Shaft Market Trends

The Europe market is predicted to expand at a 5.2% CAGR through 2032, characterized by premium vehicle concentration, exceptionally stringent emissions regulations, and strategic prioritization of advanced drivetrain technologies. Germany dominates the European automotive drive shaft market share through automotive manufacturing leadership, since the country is the birthplace of luxury and performance brands such as BMW, Mercedes-Benz, and Volkswagen. These auto giants actively prioritize lightweight drive shaft technologies and advanced material integration to optimize vehicle performance and efficiency. The European Union (EU)'s ambitious vehicular emissions reduction mandate for 2030 is catalyzing comprehensive lightweighting strategies across both mainstream and premium vehicle segments, driving universal adoption of hollow drive shafts and carbon-intensive material reduction initiatives throughout the region.

The United Kingdom, France, and Italy also contribute substantially to the regional growth momentum through established automotive manufacturing capabilities and rapidly expanding EV production capacity requiring specialized, architecture-optimized drive shaft designs tailored to emerging battery electric platforms. European component manufacturers, including Schaeffler, GKN Driveline, and Dana, lead global innovation in advanced composite and carbon fiber drive shaft technologies, positioning Europe as a premium market with a strategic focus on high-margin, technology-differentiated products.

Asia Pacific Automotive Drive Shaft Market Trends

Asia Pacific leads with approximately 35% of the automotive drive shaft market share, and is also projected to expanding the fastest at about 7.2% CAGR through 2032. This exceptional growth trajectory reflects the region's unparalleled manufacturing leadership and vehicle production expansion across multiple high-growth markets. China anchors regional dominance with around 50% market share, supported by annual vehicle production volumes exceeding 25 million, burgeoning EV manufacturers, and strategic government initiatives prioritizing automotive supply chain localization and domestic component development. India represents a particularly compelling high-growth opportunity, with vehicle production projected to surge from 4 million to over 7 million units over the next 8 to 10 years. Government-backed manufacturing initiatives and domestic production incentives are also systematically creating localized supply chain development opportunities and reducing import dependency.

Japan maintains stable market presence and technological leadership through established manufacturing capabilities anchored by Toyota, Honda, and Nissan, complemented by advanced supply chain expertise and widespread implementation of AWD architectures. Thailand, Vietnam, and Indonesia are rapidly emerging as significant growth contributors, collectively driving 12–15% regional growth through expanding vehicle production capacity, substantial foreign direct investment (FDI) from multinational OEMs, and the systematic emergence of competitive local manufacturers building indigenous component supply capabilities. This multi-country diversification strategy across Asia Pacific substantially mitigates concentration risk while positioning the region as the primary engine of the drive shaft market expansion through 2032.

Competitive Landscape

The global automotive drive shaft market landscape is experiencing moderate consolidation as tier-1 suppliers pursue strategic scale advantages through targeted acquisitions and vertical integration initiatives designed to enhance technological capabilities and operational efficiency. For example, the 2025 acquisition of Dowlais Group by American Axle & Manufacturing (AAM) produced a combined entity with projected annual revenues of US$ 12 billion and targeted cost synergies of US$ 300 million. This transaction strategically combines AAM's established forging capabilities with GKN Automotive's comprehensive driveline expertise, positioning the merged entity as a global powertrain-agnostic driveline technology leader equipped to serve diverse vehicle architectures.

Market participants are strategically differentiating through dual-focused approaches combining affordability with uncompromised vehicle performance, while systematically developing products that comply with current and prospective emission regulations across diverse global markets. Supply-side consolidation is complemented by intensive collaborative partnerships between manufacturers, regional component suppliers, and OEMs, enabling shared development costs and accelerated technology advancement in specialized drive shaft architectures tailored to evolving powertrain requirements. This collaborative ecosystem approach is establishing new competitive barriers while empowering leading suppliers to capture disproportionate market share.

Key Industry Developments

- In August 2025, Isuzu’s first all-electric D-Max pickup entered production using a compact, efficient e-Axle supplied by the BluE Nexus consortium of Toyota, Aisin, and Denso. The same e-Axle will be manufactured in India by BluE Nexus Automotive India for Suzuki Motor Gujarat and deployed in the upcoming Maruti e-Vitara, highlighting shared EV drivetrain technology across global and Indian OEM programs.

- In July 2025, Volkswagen Commercial Vehicles launched the eHybrid 4MOTION plug-in hybrid AWD system for Multivan and California vans, combining a 130kW 1.5 TSI engine with 85kW front and 100kW rear electric motors for up to 95km electric range and maximum traction. The innovative dual-motor setup enables electric AWD up to 130km/h, stationary air conditioning, and optimal efficiency for commercial and camper applications.

- In March 2025, Meyer Distributing partnered with Adams Driveshaft to expand its powertrain component offerings across 109 nationwide locations. The partnership leverages Adams' expertise in precision driveshaft engineering using American components from Spicer and Neapco, combined with Meyer's extensive distribution network and next-day delivery capabilities to enhance market reach within the specialty automotive aftermarket.

Companies Covered in Automotive Drive Shaft Market

- GKN Automotive Limited

- NTN Corporation

- Nexteer Automotive

- Hyundai WIA Corporation

- American Axle Manufacturing Inc.

- Dana Incorporated

- Xuchang Yuangdong Driveshaft Co., Ltd

- Neapco Holdings

- Wanxiang Qianchao

- Trelleborg AB

Frequently Asked Questions

The global automotive drive shaft market is projected to reach US$ 36.8 billion in 2025.

Rising production of passenger cars integrated with advanced powertrain and lightweight technologies to enhance fuel efficiency and performance is driving the market.

The market is poised to witness a CAGR of 4.9% from 2025 to 2032.

Stringent government fuel economy and emissions mandates worldwide accelerating the adoption of lightweight hollow drive shafts and rapid electrification of vehicle powertrains reshaping drive shaft design requirements are key market opportunities.

GKN Automotive Limited, NTN Corporation, Nexteer Automotive, and Hyundai WIA Corporation are some of the leading players in the market.