- Automotive Components & Materials

- Automotive Camless Piston Engine Market

Automotive Camless Piston Engine Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Camless Piston Engine Market by Actuator Type (Hydraulic, Electromechanical, Pneumatic), Propulsion Type (Hybrid/HEV, Conventional ICE), Vehicle Type (Passenger Vehicles, Commercial Vehicles), and Regional Analysis 2026 - 2033

Automotive Camless Piston Engine Market Size and Trends Analysis

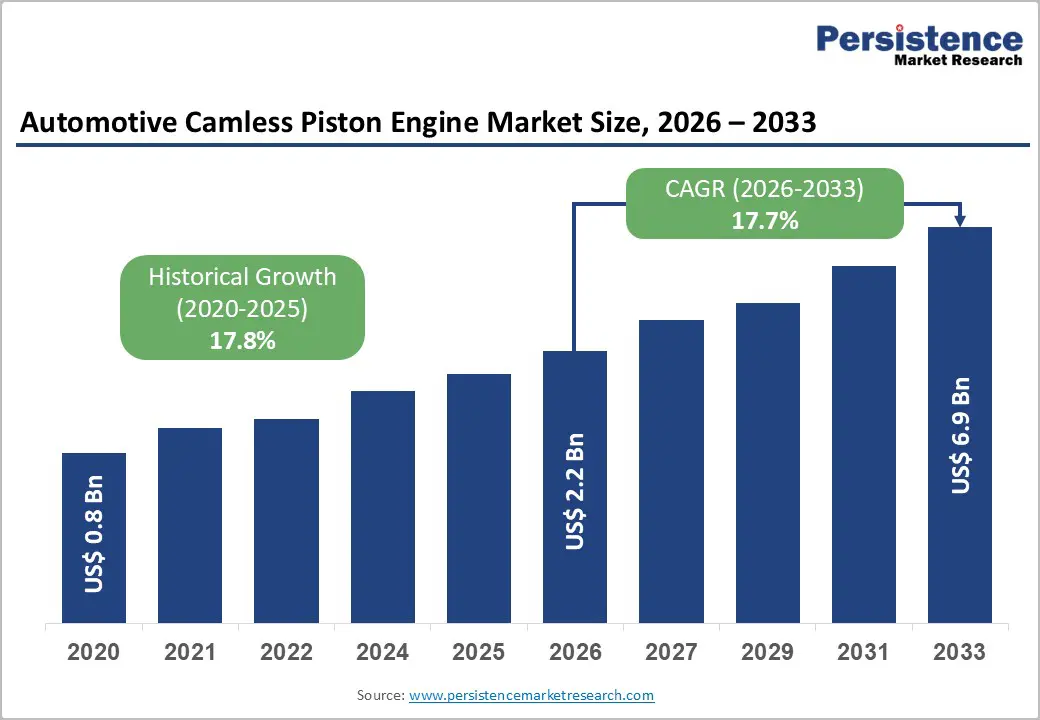

The global automotive camless piston engine market size is likely to be valued at US$2.2 billion in 2026 and is expected to reach US$6.9 billion by 2033, growing at a CAGR of 17.7% during the forecast period from 2026 to 2033, driven by the tightening of global emission regulations, prompting manufacturers to adopt camless technology, which enables independent control of valves.

This advancement enhances the longevity of internal combustion engines (ICE) and hybrid electric vehicle (HEV) powertrains. The market is transitioning from being focused on niche, high-performance uses to broader adoption within hybrid systems, where optimizing combustion is essential. This shift allows manufacturers to achieve higher thermal efficiency, reduced cold-start emissions, and greater flexibility in combustion strategies. As a result, camless systems are increasingly seen as a crucial tool in meeting future emissions standards while still utilizing combustion-based powertrains.

Key Industry Highlights:

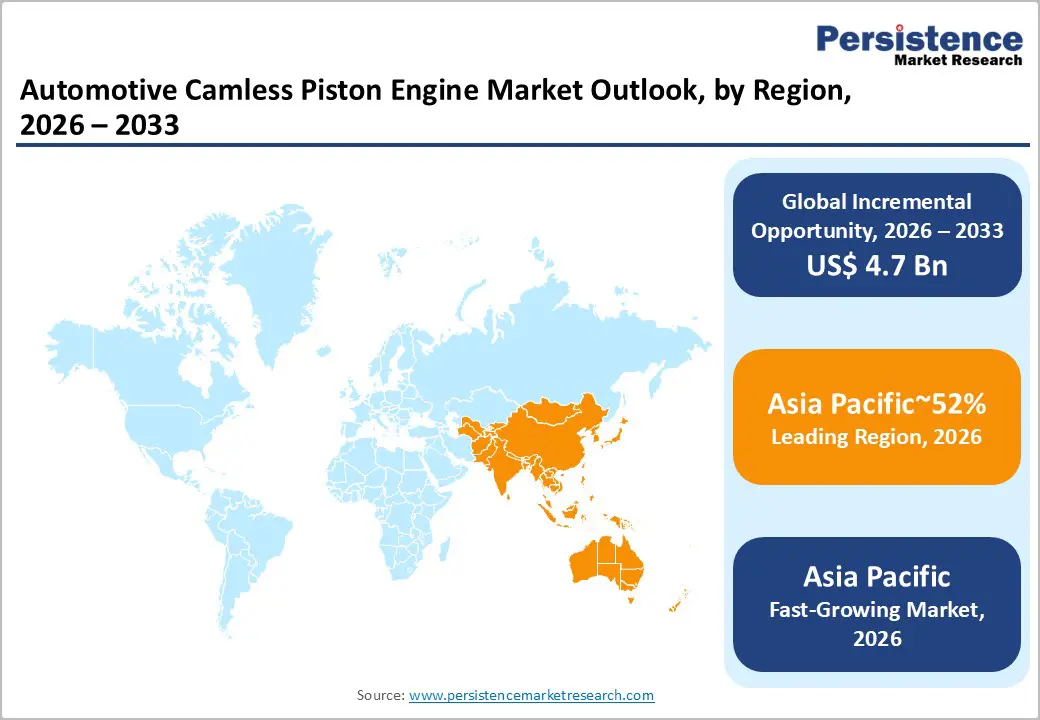

- Leading and the Fastest-Growing Region: Asia Pacific, with approximately 52% share, supported by its position as the largest automotive manufacturing hub, rapid adoption of hybrid powertrains, and strong regulatory drivers.

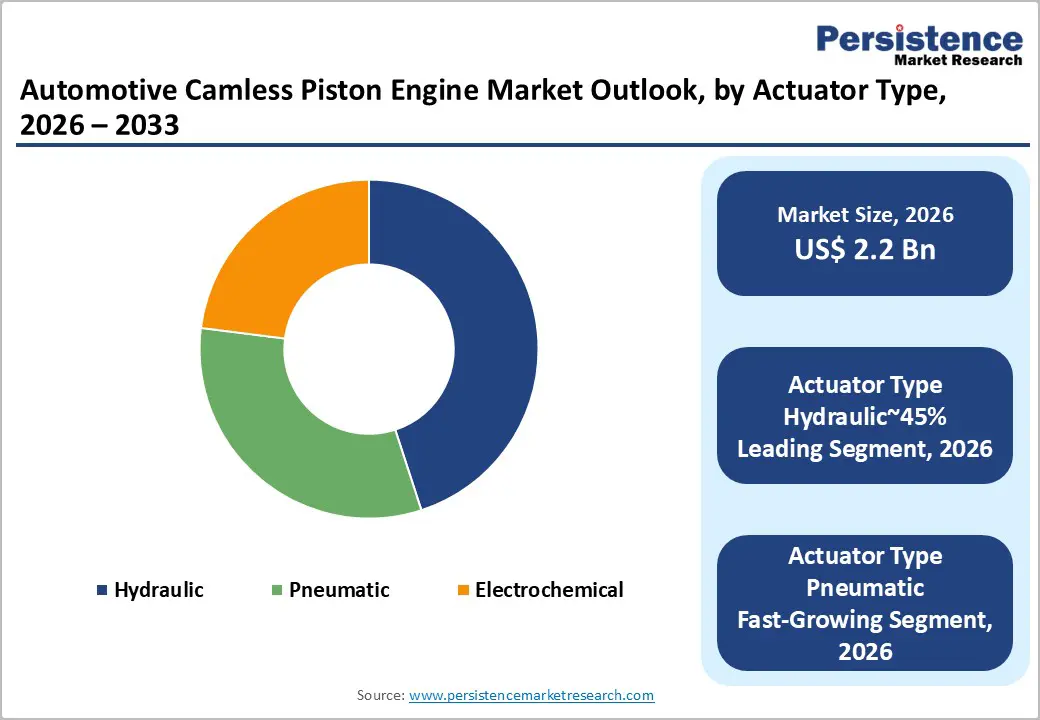

- Leading Actuator Type: Hydraulic actuators are anticipated to remain the leading actuator type with approximately 45% market share, due to their proven durability, high force density, and adoption in heavy-duty and high-performance ICE platforms across global OEMs.

- Leading Propulsion Type: Hybrid and HEV powertrains are expected to lead the market with approximately 60% share, supported by operational synergy between electric motors and camless ICEs, frequent start-stop cycles, and regulatory pressure favoring efficiency-focused electrified architectures.

| Key Insights | Details |

|---|---|

| Automotive Camless Piston Engine Market Size (2026E) | US$2.2 Bn |

| Market Value Forecast (2033F) | US$6.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 17.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 17.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Emission Compliance Pressure Accelerating Camless Engine Adoption Stringent Global Emission Regulations (Euro 7 & EPA 2027)

The stringent global emission regulations under Euro 7 and U.S. EPA 2027 are significantly altering internal combustion engine (ICE) design priorities, with camless technology emerging as a key enabler for compliance. Both regulatory frameworks focus on reducing emissions during cold-start, low-load, and real-world driving conditions, where traditional camshaft and mechanical VVT systems face limitations. Camless systems, offering fully variable control over valve timing, lift, and duration at the cylinder level, enable OEMs to adopt more efficient exhaust gas thermal management, enhancing catalyst light-off. This capability directly addresses cold-start emissions, a significant contributor to fleet NOx and CO emissions, with studies showing reductions of up to 60% for NOx and over 65% for CO.

The timeline for compliance further accelerates the adoption of camless technology. Euro 7 introduces expanded Real Driving Emissions testing and stricter low-load duty cycles, requiring precision air-charge control, where camless systems excel. EPA 2027 mandates an 80% NOx reduction for heavy-duty engines with durability requirements extending emissions compliance to 650,000 miles. Camless systems, particularly pneumatic or electro-hydraulic actuators, provide scalable solutions, offering the flexibility to meet near-zero emissions targets while maintaining the viability of ICE engines in increasingly regulated markets.

Accelerating Shift toward Full Electrification, Limiting Camless Engine Upside

The rapid shift towards battery electric vehicles (EVs) is creating a structural challenge for advanced internal combustion engine (ICE) technologies such as camless engines. Major automakers, such as Volkswagen, Stellantis, and General Motors, are prioritizing electrification and investing heavily in battery systems and EV platforms. As a result, camless engine programs are being sidelined, viewed as transitional rather than foundational, despite their advantages in combustion control and emissions performance. This creates an "efficiency versus obsolescence" dilemma for camless technology.

While it improves ICE efficiency and reduces emissions, its complexity contrasts with the industry's growing focus on simplifying drivetrains, as seen in EVs from Tesla and BYD. With increasing regulatory pressure for electric roadmaps, OEMs are hesitant to scale complex valve technologies, limiting camless adoption. As the market for ICEs continues to shrink, the long-term viability of camless technology may be capped, despite its technical benefits.

Camless Engines as a Transitional Decarbonization Lever for Heavy-Duty Fleets

Decarbonizing heavy-duty commercial transport is more challenging than for passenger vehicles due to trade-offs between vehicle weight, operating range, and refueling downtime. Large battery packs would reduce payload capacity, and fast-charging and hydrogen infrastructure along freight corridors remain uneven and costly. As a result, fleet operators continue to rely on high-utilization diesel platforms for margin protection and service reliability. This creates an opportunity for transitional technologies such as camless engines, which reduce emissions and fuel consumption without requiring a full drivetrain overhaul.

Camless technology is an ideal retrofit for commercial fleets, replacing mechanical valve actuation with electronically controlled systems. This offers load-responsive optimization, improved low-speed torque, and consistent emissions across duty cycles. Reduced complexity supports longer service intervals and predictive maintenance, crucial for high-mileage trucks. Companies, including FreeValve and BorgWarner, are targeting this market, recognizing that heavy-duty transport will remain liquid-fuel dependent longer. Camless engines enable decarbonization while infrastructure matures. Koenigsegg’s ongoing commitment to FreeValve camless tech highlights its long-term potential, offering benefits such as ~5% fuel savings and lighter components for heavy-duty applications.

Category–wise Analysis

Actuator Type Insight

Hydraulic actuators are expected to maintain a dominant 45% market share in 2026, due to their superior force density and proven durability in extreme conditions. Their strength lies in heavy-duty commercial vehicles and high-performance turbocharged engines, where precise valve control is crucial under high cylinder pressures. OEMs such as Cummins, Daimler, and Volvo rely on hydraulic valvetrains in diesel and hybrid platforms, especially for Euro VI and Euro 7 compliance. In motorsport, Bosch and Eaton favor hydraulic systems for thermal stability and longevity. This widespread adoption in commercial fleets ensures predictable demand, standardized integration, and reduced validation risk.

Pneumatic actuators are likely to represent the fastest-growing segment during the forecast period, driven by their suitability for next-generation passenger hybrids and camless engine architectures. Freevalve AB provides the clearest validation, deploying pneumatic springs in its camless systems used by partners such as Koenigsegg and Geely, enabling rapid valve response, reduced parasitic losses, and partial energy recovery during valve closing. This aligns with the broader industry shift toward “energy-neutral” actuation, where efficiency gains support hybrid synergy rather than full electrification. The trend toward compact, software-driven valve control units, supported by suppliers such as Marelli and Schaeffler, further accelerates pneumatic adoption in space-constrained hybrid platforms targeting Euro 7 and EPA 2027 compliance.

Propulsion Type Insights

Hybrid/HEV powertrains are expected to dominate camless engine adoption, representing an estimated 60% of total value share in 2026, and are expected to remain the fastest-growing category in this segment. OEMs prioritize efficiency-focused electrified architectures over pure ICE or full BEV pathways. This leadership is structurally supported by the operational synergy between electric motors and camless internal combustion engines, where electric drive systems manage low-speed torque while camless ICEs operate intermittently at optimized efficiency points. Platforms from Toyota, Hyundai Motor Group, and Geely are likely to continue integrating camless or semi-camless concepts into full-hybrid architectures, where rapid engine start-stop events demand valve systems with minimal inertia. Suppliers such as Freevalve AB and Schaeffler are expected to benefit as their actuator technologies enable near-instant combustion control, improving drivability and emissions compliance during frequent engine cycling.

The conventional ICE segment represents about 40% of the camless engine market, with a strong presence in heavy-duty trucking and off-highway equipment, where diesel's energy density is crucial. Camless technology enhances efficiency, durability, and regulatory compliance, reducing pumping losses and mechanical friction to improve thermal efficiency and lower the total cost of ownership. It also enables engine downsizing without hybridization. Recent innovations such as digital valve control, advanced cylinder deactivation, and e-fuel compatibility are boosting performance. With tightening EPA 2027 and Euro 7 standards, camless adoption is growing, especially for flex-fuel applications in regions, including India and Latin America, where the system can adapt to varying ethanol blends without mechanical redesign.

Regional Insights

Asia Pacific Automotive Camless Piston Engine Market Trends

The Asia Pacific region is expected to remain both the leading and fastest-growing market for camless engine technology, accounting for over 52% of the global share. Its dominance is underpinned by the region’s position as the world’s largest automotive manufacturing hub and its aggressive adoption of transitional hybrid powertrains. China, Japan, and India serve as primary production centers, enabling rapid integration of camless actuators across commercial and passenger vehicles. APAC’s high reliance on internal combustion engines for logistics and urban mobility ensures that retrofits offer substantial total cost-of-ownership benefits, particularly in India and Southeast Asia.

China is advancing AI-driven powertrains, where real-time software control optimizes camless valve timing. Japan is leading miniaturization for KEI-Car and compact engine applications, while India and ASEAN nations benefit from “China+1” supply chain diversification, attracting precision component manufacturing. Regulatory drivers, including Bharat Stage 7 and China 7 standards, are expected to accelerate adoption, supported by subsidies for high-efficiency ICE technologies. Leading brands such as Qoros Auto, Aisin Corporation, Toyota Industries, Musashi Seimitsu, and India Pistons Ltd. are anticipated to expand production and R&D, reinforcing APAC’s dual role as both market leader and fastest-growing region in camless technology.

North America Automotive Camless Piston Engine Market Trends

North America is projected to hold a substantial 28% share of the camless engine technology market, driven by a strong focus on high-performance and commercial applications. The region's regulatory environment, particularly the EPA's stringent nitrogen oxide (NOx) standards, is expected to accelerate the adoption of camless systems, as they help maintain engine torque and efficiency in heavy-duty and long-haul vehicles. The widespread presence of commercial fleets in the U.S. and Canada will sustain demand for camless retrofits and high-precision valve actuation, allowing compliance with emissions mandates without sacrificing power output.

North America's performance-oriented vehicle culture will continue to favor camless technology in passenger cars, where engine downsizing and power density remain key competitive advantages for OEMs targeting premium segments. Technological advancements in AI-driven calibration platforms are expected to further strengthen the region's market position. These platforms will enable real-time valve timing optimization, compensating for variations in altitude, fuel composition, and operating conditions across North America—particularly in areas with diverse geographies. Leading suppliers such as Tesla, BorgWarner, Tenneco, and Parker Hannifin are expected to enhance their focus on hydraulic and pneumatic motion control systems. This will reinforce North America’s capability to integrate camless solutions into both commercial and performance vehicle portfolios, supporting regulatory compliance and boosting operational efficiency.

Europe Automotive Camless Piston Engine Market Trends

Europe is expected to maintain a moderate share of 17% of the camless engine technology market, driven primarily by its role as a regulatory and technological bridge between traditional internal combustion engines and the continent’s aggressive shift toward Battery Electric Vehicles (BEVs). The region is likely to see camless adoption focused on compliance with Euro 7 standards, which require near-zero emissions during cold starts, positioning camless systems as essential for hybrids and low-displacement ICEs operating in urban environments. European OEMs are anticipated to prioritize precision and fuel efficiency over raw power, developing highly refined camless engines that integrate seamlessly with advanced emission-control modules. OEMs such as Volkswagen and Ford have publicly stated they are prioritizing zero-emission R&D over combustion, potentially capping the camless market's growth.

Germany, as a high-precision engineering hub, is expected to continue leveraging camless engines alongside emerging e-fuels strategies, effectively extending ICE relevance while meeting strict environmental mandates. Sweden is projected to remain the center of technological innovation, with Freevalve AB leading the development of pneumatic-hydraulic camless systems for both passenger and commercial vehicles. France and Germany are likely to focus on actuator integration and emission optimization through companies such as Forvia and Eberspächer, targeting hybrid and low-displacement applications. Spain is expected to drive camless adoption in larger gasoline-powered SUVs, balancing emissions compliance with consumer demand for high-performance vehicles. Overall, Europe will maintain a specialized, regulatory-driven role, emphasizing precision engineering, hybrid integration, and city-centered emissions reduction strategies.

Competitive Landscape

The global automotive camless piston engine market is moderately consolidated, with the top five players, including Freevalve, BorgWarner, Valeo, Schaeffler, and Marelli, controlling approximately 55–60% of technological IP and market influence. The market is characterized by a mix of specialized technology developers and large Tier-1 automotive suppliers, reflecting high barriers to entry due to extensive R&D investments and sophisticated ECU software requirements. Hydraulic actuators currently lead in adoption, supported by proven durability in heavy-duty and high-performance engines, while pneumatic actuators are the fastest-growing segment, driven by their compatibility with hybrid powertrains and rapid valve response capabilities.

Regionally, Asia Pacific leads both in share and growth, anchored by China, Japan, and India as production and adoption hubs, with regulatory drivers such as China 7 and Bharat Stage 7 accelerating integration. The North America market is driven by commercial fleets, high-performance passenger applications, and AI-enhanced calibration for valve timing. Europe is focusing on Euro 7 compliance, hybrid integration, and precision engineering, positioning the region as a regulatory and technological bridge amid the transition toward full electrification.

Key Industry Developments:

- In December 2025, Koenigsegg updated the Gemera with the F10 package, switching from TFG Freevalve to twin-turbo V8. This change addresses customer preferences for proven V8 performance and power (2,300 hp combined hybrid), but illustrates barriers to camless adoption in high-end applications due to complexity and demand.

- In July 2025, Koenigsegg reaffirmed the ongoing development of Freevalve camless technology. This update highlights Freevalve's potential in niche applications such as trucks and small engines, offering ~5% fuel savings during cruising, over 65 lbs weight reduction in cylinder heads, and enabling advanced cycles such as two-stroke operation for better efficiency and packaging.

- In February 2025, BorgWarner expanded variable cam timing supply for East Asian OEM hybrid/gasoline engines. This optimizes valve events for better combustion efficiency and emissions, supporting the broader trend toward advanced valvetrain technologies that could evolve to camless.

Companies Covered in Automotive Camless Piston Engine Market

- Freevalve AB

- BorgWarner Inc.

- Valeo S.A.

- Schaeffler AG

- Marelli

- Parker Hannifin Corp.

- Linamar Corporation

- Mahle GmbH

- Hitachi Astemo

- Denso Corporation

- Eaton Corporation

- Ricardo PLC

- Camcon Auto Ltd.

- AVL List GmbH

- Koenigsegg Automotive AB

- Qoros Auto Co., Ltd.

Frequently Asked Questions

The global automotive camless piston engine market is projected to be valued at US$2.2 billion in 2026 and is expected to reach US$6.9 billion by 2033, driven by stringent emission regulations and the need to optimize internal combustion and hybrid powertrains.

The implementation of strict global standards such as Euro 7 and EPA 2027 is a primary driver, as camless technology enables precise, independent valve control to drastically reduce cold-start emissions, improve thermal efficiency, and meet near-zero emission targets where conventional valvetrains fall short.

The automotive camless piston engine market is forecast to grow at a CAGR of 17.7% from 2026 to 2033, reflecting its critical role as a transitional technology for emission compliance.

Asia Pacific is the leading regional market, accounting for approximately 52% share, supported by its position as the largest automotive manufacturing hub, rapid adoption of hybrid powertrains, and strong regulatory drivers in China, Japan, and India.

Key players include Freevalve AB, BorgWarner, Valeo, Schaeffler, and Marelli; the top five players collectively control the technological IP and market influence, with competition centered on actuator technology and system integration.