- Automotive Components & Materials

- Automotive Cabin AC Filter Market

Automotive Cabin AC Filter Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Cabin AC Filter Market by Filter Type (Fuel Filter, Oil Filter, Intake Air Filter, Cabin Air Filter), Media Type (Cellulose, Synthetic, Others), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Off-road Vehicles, Power-sports, Other), Sales Channel (OEM, Original Equipment Supplier, Aftermarket), and Regional Analysis for 2026 - 2033

Automotive Cabin AC Filter Market Size and Trend Analysis

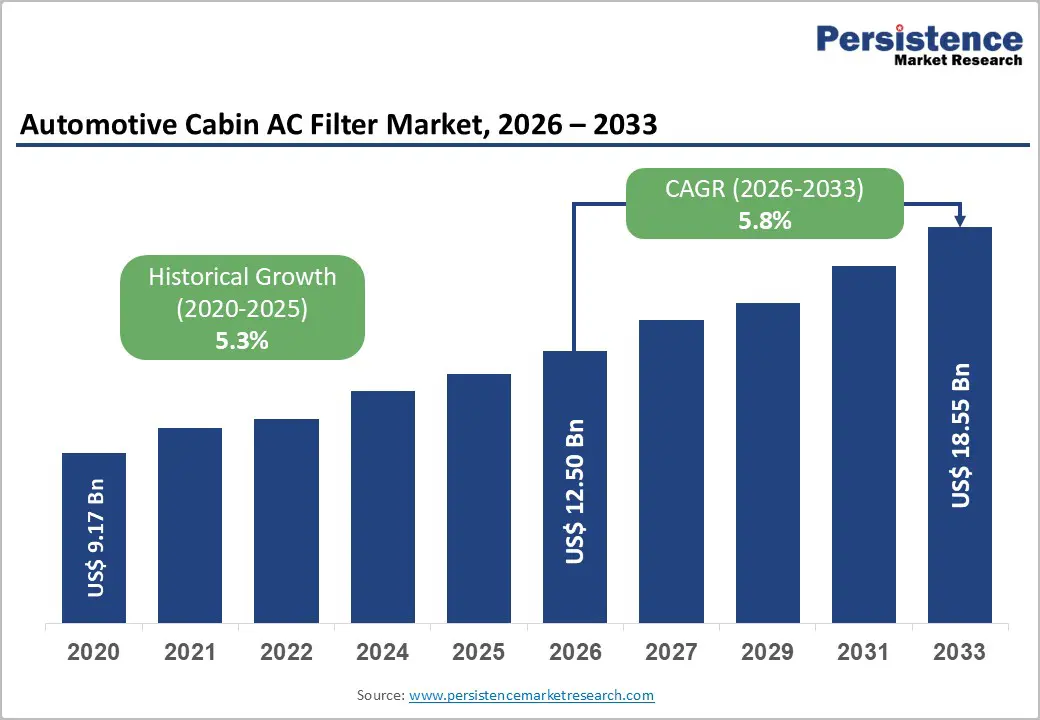

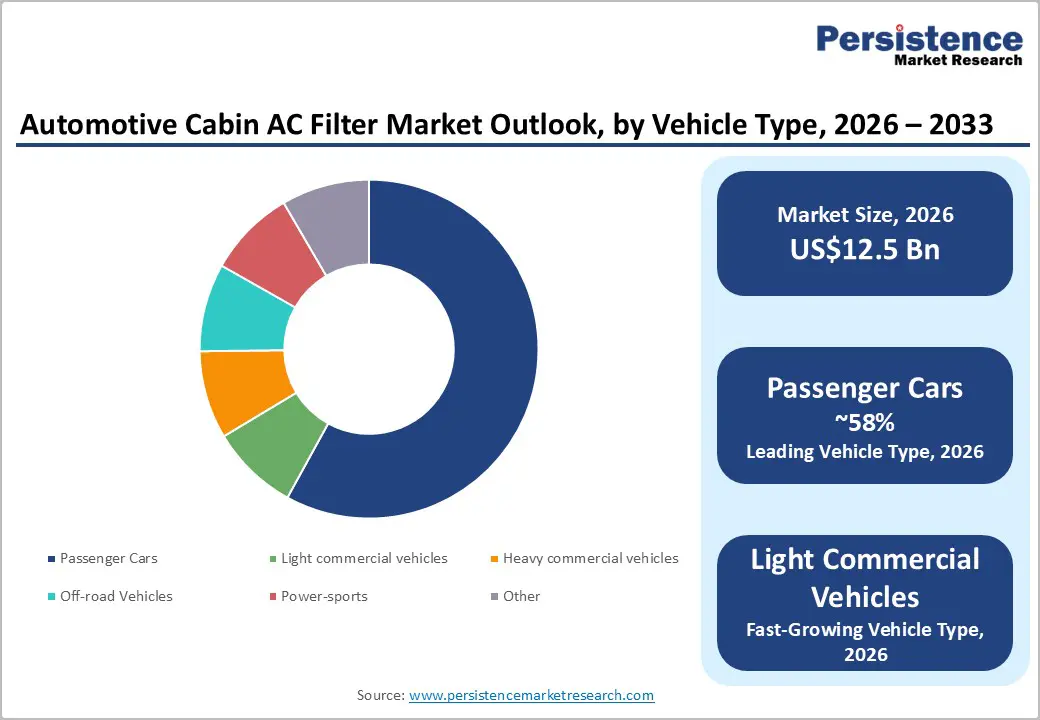

The global automotive cabin ac filter market size is supposed to be valued at US$ 12.5 Bn in 2026 and is projected to reach US$ 18.5 Bn by 2033, growing at a CAGR of 5.8% between 2026 and 2033. The market's robust expansion is primarily driven by stringent government regulations mandating improved in-vehicle air quality standards and rising consumer health consciousness regarding airborne pollutants.

According to the International Organization of Motor Vehicle Manufacturers (OICA), global vehicle production reached 92.5 million units in 2024, with China accounting for 31.28 million units, representing 34% of worldwide output. This substantial manufacturing base directly correlates with increased demand for cabin filtration systems across both original equipment manufacturer and aftermarket channels. Additionally, the United States Environmental Protection Agency's (EPA) strengthened National Ambient Air Quality Standards for particulate matter, setting the primary annual PM2.5 standard at 9.0 micrograms per cubic meter in February 2024, which has accelerated the adoption of high-efficiency cabin air filters capable of removing 99.97% of particles as small as 0.3 microns.

Key Industry Highlights:

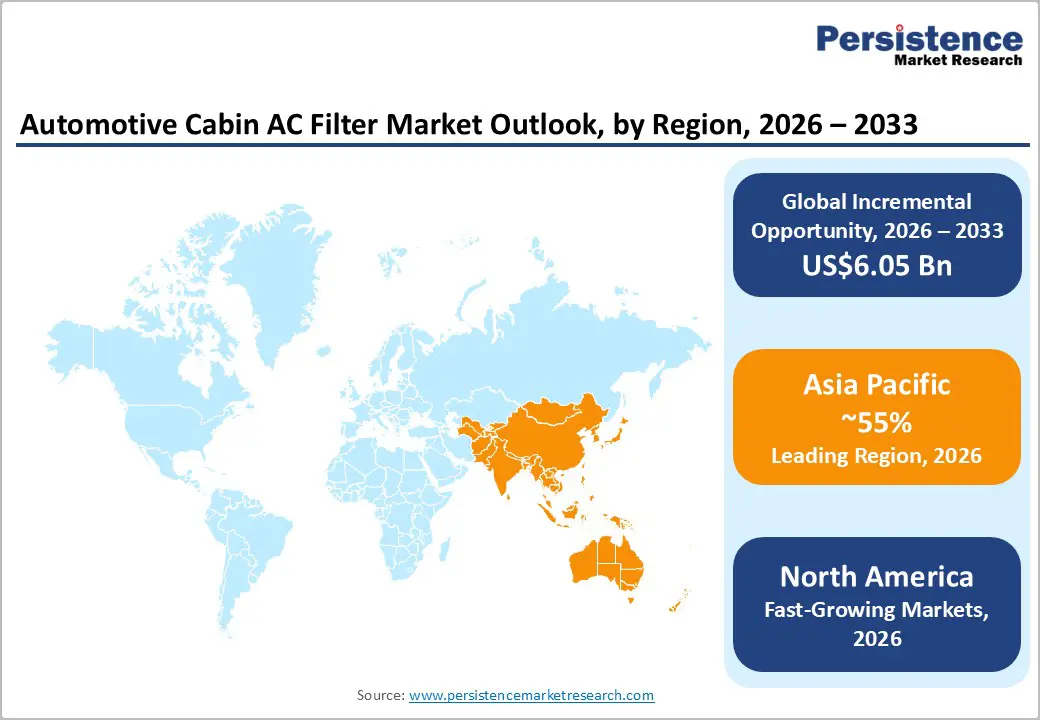

- Regional Leader: Asia-Pacific commands 55% of the global automotive cabin AC filter market share, driven by massive vehicle production exceeding 54.9 million units annually, with China manufacturing 31.28 million units and India producing 6+ million units, creating unparalleled OEM and aftermarket demand opportunities compared to mature North America and Europe.

- Fastest Growing Region: North America emerges as the fastest growing region, due to the leadership in technological advancement and regulatory stringency, with the U.S. Environmental Protection Agency setting primary annual PM2.5 standards at 9.0 micrograms per cubic meter in February 2024.

- Leading Segment: Cabin Air Filter segment dominates filter type category with approximately 42% market share, benefiting from dual revenue streams encompassing OEM installations in 68 million annual passenger vehicle production and robust aftermarket replacement demand from aging fleet requiring 40% more filters per service life beyond year 6.

- Fastest Growing Segment: Synthetic media types demonstrate the fastest growth trajectory, commanding 48% market share driven by superior filtration efficiency, enhanced durability withstanding temperatures to 90°C, resistance to moisture and microbial growth, and electrostatic charging capabilities enabling HEPA-level performance without airflow restriction penalties increasingly demanded in premium and electric vehicle segments.

- Key Market Opportunity: Electric vehicle proliferation presents a transformative opportunity with approximately 785 EV models available globally in 2024, creating an addressable market for advanced HEPA filtration systems capturing 99.97% of 0.3-micron particles, positioned as premium differentiators in quieter EV cabins where interior air quality assumes heightened importance and optimized airflow characteristics directly impact battery range efficiency.

| Key Insights | Details |

|---|---|

| Automotive Cabin AC Filter Market Size (2026E) | US$ 12.5 Bn |

| Market Value Forecast (2033F) | US$ 18.5 Bn |

| Projected Growth CAGR (2026 - 2033) | 5.8% |

| Historical Market Growth (2020 - 2025) | 5.3% |

Market Dynamics

Driver - Stringent Regulatory Framework and Emission Standards Enforcement

Regulatory authorities worldwide are increasingly imposing stringent emissions and air-quality standards that mandate the use of advanced filtration technologies in automotive applications. The European Union limits sulfur content in fuels to 10 ppm to reduce particulate emissions, thereby increasing the need for advanced filtration technologies. VDI 6032 guidelines by the German Association of the Motor Trade recommend replacing cabin air filters every 12 months or 15,000 kilometers to mitigate risks from pollutants and microbial accumulation.

With the World Health Organization reporting that 99% of the global population is exposed to unhealthy air, demand for high-efficiency cabin filtration continues to rise. Regulatory bodies worldwide are enforcing stricter air quality standards, including the EPA’s phase-out of high-GWP hydrofluorocarbons from Model Year 2025 and Europe’s Euro 7 standards requiring filtration of particles as small as 10 nm. These measures are accelerating the adoption of advanced cabin air filters across OEM and aftermarket segments.

Rapid Growth in Electric Vehicle Production and Advanced HVAC System Integration

The accelerating transition toward electric mobility is creating substantial opportunities for cabin air filter manufacturers as electric vehicles require sophisticated thermal management and air purification systems. India's automotive sector, as reported by the India Brand Equity Foundation (IBEF), achieved an overall production output of 27,73,039 units in September 2024, with electric vehicle adoption gaining significant momentum. Electric vehicles utilize cabin air filters not only for passenger comfort but also for battery cooling systems and electronic component protection, expanding the application scope beyond traditional internal combustion engine vehicles.

Leading manufacturers such as DENSO Corporation introduced the ClearAir+ premium cabin air filter range in January 2026, featuring five active layers incorporating antiviral and antibacterial technology that eliminates 99% of bacteria and viruses. Similarly, MAHLE GmbH developed smart air conditioning systems with integrated fine-particle sensors that maintain near-constant dust-extraction capacity throughout the filter's lifetime, ensuring sustained cabin air quality even under heavy-pollution conditions prevalent in urban environments.

Restraints - Extended Filter Replacement Cycles Impacting Aftermarket Volume

The automotive cabin air filter market faces volume pressure from extended replacement intervals recommended by manufacturers and improved filter durability. Modern cabin air filters, particularly those in electric vehicles, typically have longer service life than traditional filters, with replacement recommended every 12,000 to 15,000 miles or 12 to 18 months. The Allergy Standards Limited certification requirements specify that automotive cabin air filters must demonstrate greater than 90% capture efficiency for three major pollen allergens and at least 85% capture of particles exceeding 3.0 microns, yet many consumers perceive cabin filters as optional maintenance items rather than essential safety components.

Advanced synthetic media and HEPA filtration technologies, while offering superior performance, also exhibit enhanced durability that reduces replacement frequency. This extended service interval directly constrains aftermarket sales velocity, particularly in developed markets where consumers strictly adhere to manufacturer maintenance schedules. Furthermore, improved air quality in certain geographic regions reduces filter saturation rates, inadvertently lengthening functional lifespan and diminishing replacement demand.

Competitive Price Pressure from Unbranded Aftermarket Alternatives

The cabin air filter aftermarket faces intense price competition from unbranded and lower-quality alternatives that undercut premium original equipment quality products. Price-sensitive consumers, particularly in developing markets and among cost-conscious vehicle owners, frequently opt for cheaper replacement filters that lack advanced filtration capabilities but satisfy basic functional requirements.

The aftermarket segment, which controlled 77.26% of the U.S. automotive air filters market in 2024, demonstrates significant price elasticity, with many consumers prioritizing initial cost over long-term filtration efficiency. This pricing dynamic compresses profit margins for established manufacturers and creates barriers to premium product adoption, particularly for advanced technologies such as activated carbon layers and electrostatic filtration media.

Opportunity - Expansion of Antiviral and Antibacterial Filter Technologies Post-Pandemic

The global health crisis has significantly reshaped consumer expectations for in-vehicle air quality, creating strong opportunities for manufacturers of advanced antimicrobial cabin filtration systems. DENSO Corporation’s ClearAir+ filter, introduced in January 2026, reflects this shift by integrating five active layers that protect against allergens, bacteria, and viruses while ensuring compatibility with OEM HVAC systems. Similarly, EcoDrive Components’ AI-enabled Smart Air Sense Filter System, launched in 2025, enhances air purification by monitoring cabin conditions in real time and automatically adjusting filtration performance. Certification of Bosch’s FILTER+pro in 2024 further validates the growing acceptance of premium antimicrobial technologies.

Sustainability requirements are also driving innovation. MANN+HUMMEL’s CO2-reduced filters, along with regenerable and washable solutions developed by Ahlstrom and Toyota Boshoku, support circular economy objectives. With rising regulatory pressures and OEM carbon-neutrality goals, eco-certified filters increasingly command premium market positioning.

Technological Innovation in Multi-Layer and Smart Filtration Systems

Rapid advancements in filtration material science and sensor integration are creating significant opportunities for manufacturers to develop next-generation cabin air filters with enhanced efficiency and premium-pricing potential. Leading companies such as MAHLE and MANN+HUMMEL are focusing on continuous innovation to engineer multi-layer, progressive-density filtration systems capable of capturing increasingly smaller airborne particles. MANN+HUMMEL has introduced more than 125 new filter types in its 2024-2026 catalog, covering passenger cars, trucks, and off-highway vehicles while maintaining original equipment quality standards.

Advanced combi-filters featuring sandwich construction integrate activated carbon layers to address both particulate and gaseous contaminants. Furthermore, emerging smart filtration solutions utilize sensors to monitor external air toxicity and automatically adjust HVAC settings, with some systems temporarily closing vents under hazardous conditions. Freudenberg Filtration Technologies has also expanded its portfolio with next-generation fan filter units and Bag-In/Bag-Out systems, extending applications into cleanroom and battery-manufacturing environments.

Category-wise Analysis

Filter Type Insights

The cabin air filter segment holds a leading position in the filter type category, accounting for approximately 42% of the Automotive Cabin AC Filter Market. This dominance is supported by its mandatory integration in modern vehicles and increasing consumer emphasis on superior in-cabin air quality. Once considered optional, cabin air filters have become standard across nearly all passenger vehicle segments, with automakers leveraging advanced air purification features as key competitive differentiators.

The segment benefits from steady OEM demand driven by global passenger vehicle production exceeding 68 million units in 2024, as well as strong aftermarket replacement needs. An aging vehicle fleet, particularly in North America, where around 110 million vehicles fall within the 6 to 14-year range, further sustains replacement volumes, with older vehicles requiring up to 40% more filters per service life. Increasing health awareness and tightening air-quality regulations continue to reinforce the segment’s robust growth trajectory.

Media Type Insights

Synthetic media leads the media type segment with about 48% market share due to its superior filtration efficiency, durability, and resistance to moisture and microbial growth. It is primarily composed of polyester fibers arranged in progressive-density layers, providing an optimal balance between airflow resistance and filtration performance essential for HVAC efficiency. These 10-20 mm fleece mats become increasingly compact on the clean-air side, ensuring strong dust-holding capacity.

Synthetic polyester foam also resists ozone, partially resists hydrolysis, withstands temperatures up to 90°C, and remains free from plasticizers and CFCs while being fully recyclable. Its structural stability under varying humidity prevents collapse and microbial buildup, issues common in cellulose-based filters. Additionally, electrostatically charged synthetic media enhances particle capture without restricting airflow, enabling HEPA-level performance and supporting its premium adoption among health-conscious consumers and high-end vehicle segments.

Vehicle Type Insights

Passenger cars represent the dominant vehicle type segment, accounting for approximately 58% of the Automotive Cabin AC Filter Market due to high global production volumes and broad consumer adoption. Global passenger vehicle output surpassed 68 million units in 2024, generating substantial OEM and aftermarket demand for cabin air filtration systems. The U.S. recorded 15.9 million new car sales, while China produced 27.48 million passenger cars, significantly contributing to installation and replacement requirements. Mid-sized passenger cars show strong adoption, driven by consumer preference for interior comfort and improved air quality.

The segment also experiences the highest aftermarket replacement frequency, as private owners prioritize cabin air quality more than commercial fleet operators. In the U.S., passenger cars held 63.14% of the automotive air filters market in 2024. Rising premium vehicle penetration and growing health awareness further reinforce segment leadership.

Sales Channel Insights

The aftermarket sales channel holds a dominant 55% share of the Automotive Cabin AC Filter Market, supported by a large installed vehicle base, longer vehicle lifespans, and the routine replacement cycles required for filtration products. Its strong position reflects the consumable nature of cabin air filters, which typically require replacement every 12 to 18 months or 12,000 to15,000 miles, generating recurring demand independent of new vehicle sales. North America demonstrates particularly high aftermarket penetration, capturing 72.8% to 77.26% of the market in 2023-24.

Extended vehicle ownership, especially during periods of economic uncertainty, further shifts consumer spending toward maintenance components, including cabin filters. Cost-conscious buyers often choose lower-priced aftermarket alternatives over OEM products, increasing volume despite tighter margins. The segment also benefits from broad distribution networks, including independent garages, quick-service centers, retail outlets, and fast-growing e-commerce channels, while aging vehicles beyond six years require more frequent replacements as filter efficiency declines.

Regional Insights

North America Automotive Cabin AC Filter Market Trends

North America represents a mature and technologically advanced market for Automotive Cabin AC Filters, characterized by stringent regulatory frameworks and high consumer awareness regarding vehicle air quality. The U.S. market continues to grow, driven by a vehicle parc exceeding 280 million units and an aging fleet, with roughly 110 million vehicles between 6 and 14 years requiring significantly higher filter replacement rates. Regulatory measures, including the EPA’s mandate for low-GWP refrigerants in upcoming light- and medium-duty vehicles, further encourage the adoption of advanced filtration technologies.

Aftermarket dominance in the U.S., with a 77.26% share in 2024, reflects price-sensitive consumer preferences and broad independent repair networks. Major urban regions show particularly strong filter demand due to high pollution levels. Canada and Mexico add depth to the regional market through their combined production of over 19 million vehicles in 2024.

Europe Automotive Cabin AC Filter Market Trends

Europe is a highly advanced market for automotive cabin air filtration, shaped by stringent environmental regulations, elevated emission standards, and strong consumer focus on in-vehicle air quality. Euro 7 standards introduce more demanding filtration requirements, including the capture of particulate matter down to 10 nm, while mandating significant reductions in nitrogen oxide and particulate emissions. These regulations compel automakers to integrate comprehensive emission control systems with advanced cabin filtration technologies.

Major automotive hubs such as Germany, the U.K., France, and Spain generate substantial OEM demand, particularly within premium vehicle segments where sophisticated filtration systems are standard. Germany’s strong innovation ecosystem, supported by leading automakers and filtration specialists, drives rapid technology development, as demonstrated by MANN+HUMMEL’s release of over 125 new filter types for 2024 - 2026. Unified EU regulatory frameworks, strong environmental consciousness, and accelerated EV adoption further support the adoption of premium, high-performance cabin filtration solutions.

Asia Pacific Automotive Cabin AC Filter Market Trends

Asia Pacific dominates the global automotive cabin AC filter market with an estimated 55% regional market share in 2026, driven by massive vehicle production capabilities and rapidly expanding middle-class vehicle ownership across emerging economies. China leads the region, producing 31.28 million vehicles in 2024, about 34% of global output, with 27.48 million passenger cars creating significant baseline demand. The country’s 4% year-over-year production growth and accelerated EV adoption, where advanced cabin filtration is increasingly standard, further strengthen demand. China is projected to reach 35 million vehicles by 2025.

Japan, producing 8.23 million vehicles in 2024, represents a technologically advanced market supported by major manufacturers such as Denso, Toyota Boshoku, and Ahlstrom. India is another high-growth market, with 6.01 million vehicles produced in 2024 and a projected 7.2% CAGR through 2028, driven by rising middle-class purchasing power and increasing focus on air-quality-related health protection.

Competitive Landscape

The global automotive cabin AC filter market is moderately consolidated, with 10-15 global manufacturers accounting for around 60-65% of total market share, while numerous regional players cater to localized demand. Leading companies employ multi-pronged growth strategies, including geographic expansion, deeper aftermarket penetration, and long-term supply partnerships with automotive OEMs. Innovation efforts focus on advanced filtration media, multi-layer system designs, and sensor-integrated solutions that enable smart cabin air management. Major players such as MANN+HUMMEL, Mahle GmbH, Robert Bosch GmbH, and Denso Corporation leverage extensive component portfolios to bundle filtration solutions with complementary products, strengthening customer retention. Emerging business models include subscription-based replacement services, direct-to-consumer e-commerce channels, and telematics-enabled performance monitoring that supports predictive maintenance scheduling.

Key Developments:

- February 2024: MANN+HUMMEL launched new MANN-FILTER catalogs for 2024-2026 featuring more than 125 new filter types for the latest passenger car, truck, and off-highway models, expanding coverage to almost 5,000 filter elements for over 67,500 vehicles and machines in the European market.

- November 2025: Freudenberg Filtration Technologies expanded its advanced product portfolio in India with next-generation fan filter units, integrated Bag-In/Bag-Out (BIBO) systems, and NMP-compatible filters for lithium-ion battery and lithium iron phosphate production facilities, demonstrating filtration technology applications beyond traditional automotive markets.

- January 2026: MANN+HUMMEL Filter India showcased an expanding portfolio for industrial and construction equipment at EXCON 2025, highlighting the company's diversification strategy beyond passenger vehicle applications into heavy equipment and off-highway segments.

Top Companies in the Automotive Cabin AC Filter Market

- MANN+HUMMEL GmbH (Ludwigsburg, Germany) operates a comprehensive portfolio spanning automotive, industrial, and specialty applications with strong emphasis on innovation and original equipment quality. The company maintains an extensive global manufacturing footprint with a presence across major automotive markets, supporting both OEM and aftermarket channels. MANN+HUMMEL's recent introduction of 125 new filter types for 2024-2026, covering 67,500 vehicles, demonstrates robust product development capabilities and commitment to maintaining comprehensive vehicle coverage, positioning the company as a preferred filtration partner for automakers and aftermarket distributors.

- Mahle GmbH (Stuttgart, Germany) represents a major automotive component supplier with extensive filtration technology expertise encompassing cabin air, oil, fuel, and intake air filtration applications. The company's cabin air filter portfolio features advanced combi-filter designs integrating activated carbon layers within sandwich construction, enabling simultaneous particulate capture and gaseous pollutant absorption. Mahle's strong OEM relationships with global automakers provide a stable revenue foundation while growing aftermarket presence captures replacement demand across the vehicle lifecycle.

- Denso Corporation (Kariya, Japan) operates as a major global automotive components manufacturer with operations in approximately 35 countries worldwide, producing a comprehensive range of filtration products meeting stringent emission and environmental standards. The company leverages strong relationships with Japanese automakers, including Toyota, Honda, and Nissan, while expanding its presence in North American, European, and emerging Asian markets.

Companies Covered in Automotive Cabin AC Filter Market

- Mahle GmbH

- Robert Bosch GmbH

- Donaldson Company Inc.

- FRAM Group IP LLC

- Sogefi S.p.A

- Mann+Hummel GmbH

- Denso Corportaion

- Ahlstrom Corporation

- Toyota Boshoku Coporation

- Parker Hannifin

- Cummins Inc.

- Freudenberg & Co. KG

- Hengst SE & Co. KG

- Hollingsworth & Vose Company

- Valeo S.A.

Frequently Asked Questions

The global Automotive Cabin AC Filter Market is valued at US$ 12.5 Bn in 2026 and is projected to reach US$ 18.5 Bn by 2033, expanding at a CAGR of 5.8% during the forecast period, driven by increasing vehicle production, stringent air quality regulations, and growing consumer health consciousness.

The market is primarily driven by stringent regulatory frameworks, including EPA restrictions and Euro 7 standards mandating advanced filtration, rising health awareness regarding in-cabin air quality with vehicle interiors potentially 10 times more polluted than outdoor air, and the proliferation of 785 EV models globally emphasizing air purification as a premium differentiator.

Passenger Cars dominate the vehicle type category with approximately 58% market share, supported by global production exceeding 68 million units in 2024, widespread consumer adoption across economic segments, and the highest aftermarket replacement frequency, with U.S. passenger cars capturing 63.14% of the automotive air filters market in 2024.

North America maintains market leadership driven by heightened consumer health awareness, mature aftermarket infrastructure commanding 77.26% of the U.S. market share in 2024, stringent EPA regulatory framework, and aging vehicle fleet of approximately 110 million units in an optimal 6 to14 year replacement age range generating consistent demand.

Electric vehicle proliferation presents a transformative opportunity with approximately 785 EV models available globally in 2024, enabling positioning of advanced HEPA filtration systems capturing 99.97% of 0.3-micron particles as premium differentiators, while technological innovation in multi-layer systems with sensor integration and smart cabin air management creates value-addition potential beyond commodity offerings.

Key market players include MANN+HUMMEL GmbH, Mahle GmbH, Robert Bosch GmbH, Denso Corporation, Donaldson Company Inc., Sogefi S.p.A, Freudenberg & Co. KG, Valeo S.A., Cummins Inc., and Parker Hannifin, competing through original equipment quality positioning, comprehensive vehicle coverage, and aftermarket channel penetration strategies.