- Metals & Minerals

- Australia Titanium Dioxide Market

Australia Titanium Dioxide Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Australia Titanium Dioxide Market by Product Type (Pigments, Non-pigments), by Carrier Production Process (Sulfate, Chloride), by Application (Dyes and Paints, Plastics and Rubber, Paper, Pure Titanium Metal and Welding Rods), and State Analysis for 2025 - 2032

Australia Titanium Dioxide Market Size and Trends

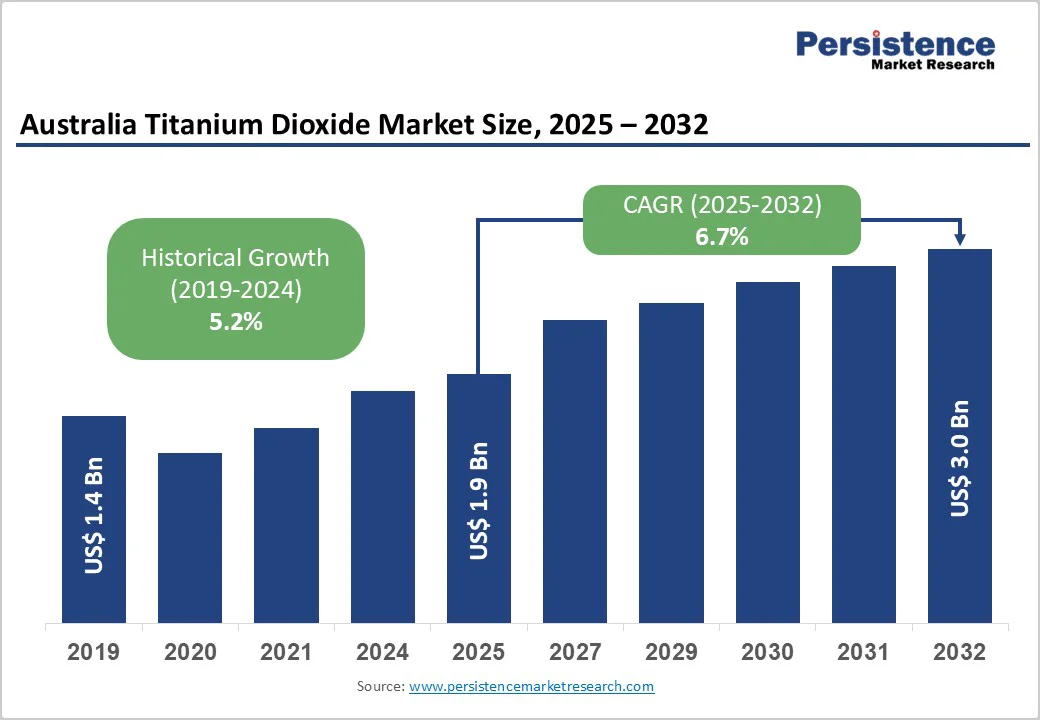

The Australia titanium dioxide market size is likely to be valued at US$ 1.9 Billion in 2025 and is estimated to reach US$ 3.0 Billion in 2032, growing at a CAGR of 6.7% during the forecast period 2025-2032, driven by rising demand from the paints and coatings, construction, and renewable energy sectors. High popularity of mineral-based cosmetics and sunscreens also fuels demand.

Key Industry Highlights

- Sustainability Initiative: In February 2025, Tronox published its 2024 Sustainability Report, noting a 21% reduction in scope-1 and scope-2 greenhouse gas emissions intensity relative to its 2019 baseline.

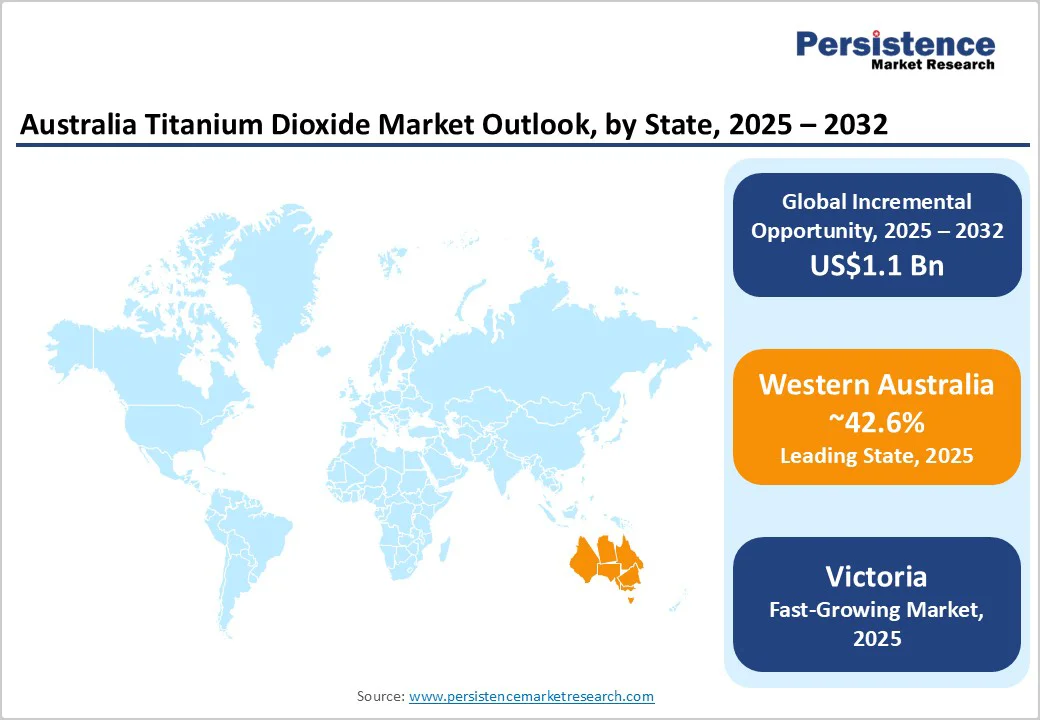

- Leading State: Western Australia, approximately 42.6% of share in 2025, owing to its abundant mineral sands reserves and integrated titanium dioxide operations.

- Fastest-growing State: Victoria, spurred by government-backed critical mineral programs, which are boosting investment.

- Leading Product Type: Pigments hold nearly 53.1% share in 2025, due to their exceptional brightness, opacity, and weather resistance.

- Dominant Carrier Production Process: Sulfate, approximately 77.4% of the Australia titanium dioxide market share in 2025, as it efficiently handles Australia’s ilmenite-rich ores and produces pigments with excellent opacity.

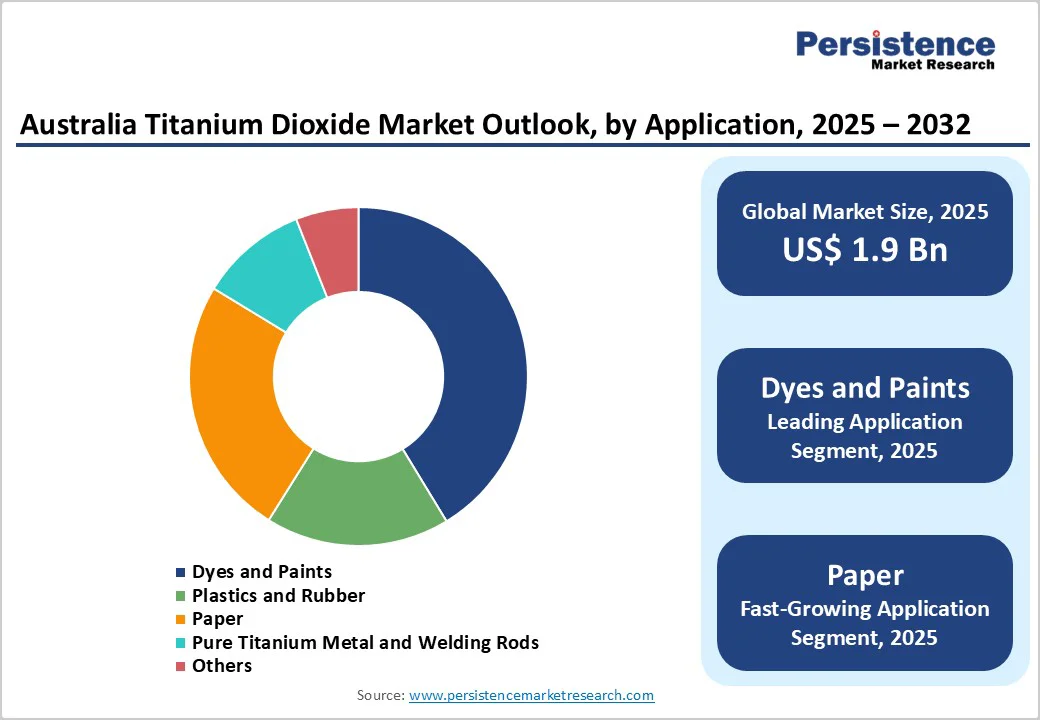

- Key Application: Dyes and paints recorded about 41.3% share in 2025, bolstered by extensive use of TiO2 in residential and industrial coatings that withstand harsh sunlight and humidity.

| Key Insights | Details |

|---|---|

|

Australia Titanium Dioxide Market Size (2025E) |

US$ 1.9 Billion |

|

Market Value Forecast (2032F) |

US$ 3.0 Billion |

|

Projected Growth (CAGR 2025 to 2032) |

6.7% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Surging Use of Titanium Dioxide in Industrial and Consumer Goods

The demand for titanium dioxide (TiO2) in Australia is increasing as industries diversify its use beyond traditional paints and coatings. The pigment’s excellent opacity and brightness make it indispensable in paper, plastics, and textile dye production. Growth in infrastructure projects and home renovations has also boosted the use of high-durability paints that rely on TiO2 for UV resistance and color stability.

For instance, the construction industry in Australia saw a notable uptick in residential repainting projects in 2024, pushing pigment consumption. Also, the rising output of packaging plastics and printing inks supports TiO2 usage in downstream applications.

Expanding Solar Infrastructure Improving TiO2 Consumption

Australia’s accelerating solar energy adoption is creating new opportunities for titanium dioxide. The material is used in the semiconductor layer of dye-sensitized and perovskite solar cells to improve light absorption and conversion efficiency.

With over 3.7 million rooftop solar systems installed nationwide as of 2025, the government’s continued focus on renewable expansion is encouraging research into TiO2-based photovoltaic materials. Local research groups, such as those at the University of New South Wales, are developing TiO2 nanostructures to improve next-generation solar panel performance, signaling superior long-term growth prospects for this application.

Barrier Analysis - Increasing Adoption of Alternative Materials Reducing Reliance

The use of titanium dioxide in coatings and industrial applications is being challenged by the rising preference for substitutes such as silica, zinc oxide, and calcium carbonate. Silica, in particular, delivers excellent surface passivation and UV-reflective properties, making it a competitive option in paints, paper coatings, and sunscreens.

Manufacturers are increasingly opting for silica-based formulations to lower production costs and meet sustainability targets. In 2024, several Australia-based coatings manufacturers began testing silica additives for architectural paints to improve weather resistance while reducing pigment loading, indicating a gradual shift away from traditional TiO2-heavy formulations.

Economic Headwinds Affecting End-user Demand

Australia’s economic slowdown has constrained industrial output and consumer spending, directly impacting sectors that push titanium dioxide demand. Weak construction activity and a cooling property market have reduced paint and coating consumption, while manufacturing cutbacks have lowered demand for TiO2 in plastics and paper.

The Reserve Bank of Australia’s recent interest rate hikes to control inflation have further dampened investment in building and renovation projects. This economic uncertainty has made producers cautious about expanding capacity or committing to long-term pigment contracts, putting downward pressure on TiO2 market growth.

Opportunity Analysis- Rising Potential in the Beauty and Skincare Segment

Australia’s cosmetics and personal care sector is emerging as a promising growth avenue for titanium dioxide, mainly due to its role as a UV filter and whitening agent in sunscreens, foundations, and lotions. With Australia experiencing some of the world’s highest UV exposure levels, consumer demand for effective sun protection products continues to rise.

The shift toward mineral-based and clean beauty formulations has further boosted TiO2 usage as a safer, non-toxic alternative to chemical UV blockers. Local brands such as Sukin and Nude by Nature are extensively adopting titanium dioxide nanoparticles in their sunscreen and makeup lines to improve coverage and transparency without compromising skin safety.

Developments in Environmental Photocatalysis Creating New Uses

Ongoing research into improving the photocatalytic performance of titanium dioxide is opening new sustainability-focused opportunities. Australia’s scientists are working on doping TiO2 with nitrogen and carbon to improve its ability to degrade air pollutants and greenhouse gases under visible light.

In 2024, researchers at the University of Melbourne developed a modified TiO2 coating capable of breaking down nitrogen oxides from vehicle emissions more efficiently. Such developments are expanding the pigment’s role beyond industrial applications to environmental purification technologies, including self-cleaning surfaces, air-purifying coatings, and water treatment systems.

Category-wise Analysis

Product Type Insights

The pigments segment is speculated to capture nearly 53.1% of share in 2025, backed by their excellent opacity, brightness, and UV resistance, which improve surface appearance and durability across paints, plastics, and coatings. In Australia, titanium dioxide pigments are favored in architectural and automotive paints to combat harsh UV conditions. The Kwinana plant operated by Tronox supplies high-purity pigment grades that maintain color stability even in extreme sunlight, a key factor for local industries.

Non-pigment grades of titanium dioxide, including ultrafine and nano forms, are witnessing consistent demand in cosmetics, photocatalysis, and solar applications. Their transparency and UV absorption properties make them ideal for sunscreens and personal care products, which are in high demand due to Australia’s high UV index. In addition, universities such as UNSW and Monash are researching nano-TiO2 coatings for antimicrobial surfaces and air purification systems, boosting interest in functional as well as non-pigment applications.

Carrier Production Process Insights

Sulfate carrier production process leads with approximately 77.4% of share in 2025 because it is better suited for processing local ilmenite ores, which contain high levels of impurities. This method is cost-effective for small to medium-scale producers and allows flexibility in feedstock quality. The process also produces pigments with excellent opacity and a blue undertone, favored in coatings and paper. Tronox continues to refine its sulfate-based pigment production to meet sustainability targets, using waste acid recovery systems to reduce emissions and effluent discharge.

The chloride process is gaining impetus due to its ability to produce high-purity pigments with superior brightness and low energy intensity. It complies well with Australia’s push for low-emission industrial processes. The Kwinana facility and new projects under consideration at Kemerton are exploring chloride technology to boost output efficiency. The process also generates less waste and allows continuous operation, which appeals to large-scale producers seeking high throughput. With global demand shifting toward premium-grade TiO2 for unique coatings and plastics, domestic companies are evaluating chloride-based expansions.

Application Insights

Dyes and paints are anticipated to hold about 41.3% of share in 2025 due to Australia’s ongoing infrastructure development, home renovations, and outdoor construction activities that demand high-performance coatings. Titanium dioxide’s superior covering power and weather resistance make it ideal for achieving long-lasting color stability in both decorative and industrial paints. Local paint manufacturers such as DuluxGroup rely heavily on TiO2 pigments to produce UV-stable coatings suited to Australia’s climate, where sunlight intensity accelerates paint degradation.

The paper industry remains a key consumer of titanium dioxide for improving brightness, opacity, and printability of specialty papers. In Australia, TiO2 is commonly used in high-grade packaging papers, art paper, and label stock, where visual clarity and surface smoothness are essential. As sustainable packaging rises, paper producers are incorporating TiO2 coatings to replace plastic-based laminations without compromising appearance.

State Insights

Western Australia Titanium Dioxide Market Trends

In 2025, Western Australia accounted for approximately 42.6% of share as it is the core of titanium dioxide activity in the country, with extensive mineral sands deposits and established processing infrastructure. Tronox operates one of its largest integrated pigment plants at Kwinana, supported by mineral sands mining at Cooljarloo. Iluka Resources also plays a key role with its synthetic rutile operations at Capel and Cataby.

However, in late 2025, Iluka announced it would suspend mining at Cataby and halt one of its synthetic rutile kilns due to weak pigment demand and rising global oversupply. At the same time, projects such as Empire Metals’ Pitfield discovery are drawing attention for their high-grade titanium potential, which could strengthen West Australia’s position as a feedstock hub.

Victoria Titanium Dioxide Market Trends

Victoria’s titanium dioxide presence is centered on its rich mineral sand resources rather than pigment manufacturing. The Murray Basin and Gippsland regions hold some of Australia’s most promising rutile and ilmenite reserves. Exploration activity has been increasing as miners seek new deposits to supply feedstock for domestic and export markets.

While the state lacks large-scale pigment plants, demand for TiO2 in construction, packaging, and coatings remains superior, especially in Melbourne’s booming infrastructure sector. The government’s support for important minerals exploration is also encouraging new investments in Victoria’s mineral sands corridor.

New South Wales Titanium Dioxide Market Trends

New South Wales contributes mainly as a source of titanium-bearing mineral sands and is emerging as an exploration hotspot. Iluka Resources’ Balranald project in the state is one of the most advanced, expected to supply high-grade feedstock once operational. The project uses unique underground mining technology suited for deep deposits found in the Murray Basin.

While New South Wales does not have major TiO2 pigment manufacturing facilities, its expanding resource base is essential for supplying feedstock to processing plants in Western Australia and overseas. Local research institutions are also studying novel extraction methods to improve recovery from low-grade deposits.

Competitive Landscape

The Australia titanium dioxide market is moderately competitive, with a few leading players dominating both mining and pigment production. Tronox is the most prominent name, operating an integrated value chain that covers mineral sands mining, synthetic rutile production, and TiO2 pigment manufacturing. The company’s operations in Western Australia, especially in Kwinana and Cooljarloo, give it a strategic edge in cost efficiency and supply reliability. Iluka Resources is another key player, focusing primarily on mining and producing feedstock materials such as rutile and synthetic rutile, which are essential for TiO2 pigment production.

Business Strategies

Competition in the Australia titanium dioxide market is mainly shaped by access to high-quality mineral sands rather than large-scale pigment plants. This is because Australia exports a significant portion of its ilmenite and rutile to countries such as China for further processing. This dependence on exports has made local producers vulnerable to global price fluctuations. For example, in 2024, Iluka announced a temporary halt in some Western Australian operations due to falling pigment demand and increased China-based oversupply, which lowered profitability.

Key Industry Developments

- In August 2025, Empire Metals reported metallurgical testwork successes at its Pitfield project in Western Australia, achieving 95% titanium recovery and confirming high-grade titanium dioxide grades at the Thomas prospect.

- In June 2025, Iluka Resources committed AUD 434 million to further develop its Balranald mineral sands project in New South Wales, advancing it toward commissioning later that year.

Companies Covered in Australia Titanium Dioxide Market

- Tronox Limited

- Iluka Resource Limited

- Cristal Australia Pty Ltd

- The Chemours Company

- Evonik Industries

- Argex Titanium Inc.

- The Kish Company, Inc.

- Tayca Corporation

- Ishihara Sangyo Kaisha Ltd.

- INEOS

- Others

Frequently Asked Questions

The Australia titanium dioxide market is projected to reach US$ 1.9 Billion in 2025.

Rising use of mineral-based sunscreens and expanding renovation projects are the key market drivers.

The Australia titanium dioxide market is poised to witness a CAGR of 6.7% from 2025 to 2032.

Increasing exploration of high-grade titanium deposits and developments in TiO2 photocatalysis are the key market opportunities.

Tronox Limited, Iluka Resource Limited, and Cristal Australia Pty Ltd are a few key market players.