- Bulk Chemicals

- Australia Lime Market

Australia Lime Market Size, Share, and Growth Forecast, 2025 - 2032

Australia Lime Market By Product Type (Aglime, Quicklime, Hydrated Lime), Application (Agriculture, Metallurgy, Building Material, Water Treatment), End-user Industry (Mining, Chemicals, Construction, Environmental), and State Analysis for 2025 - 2032

Australia Lime Market Size and Trends Analysis

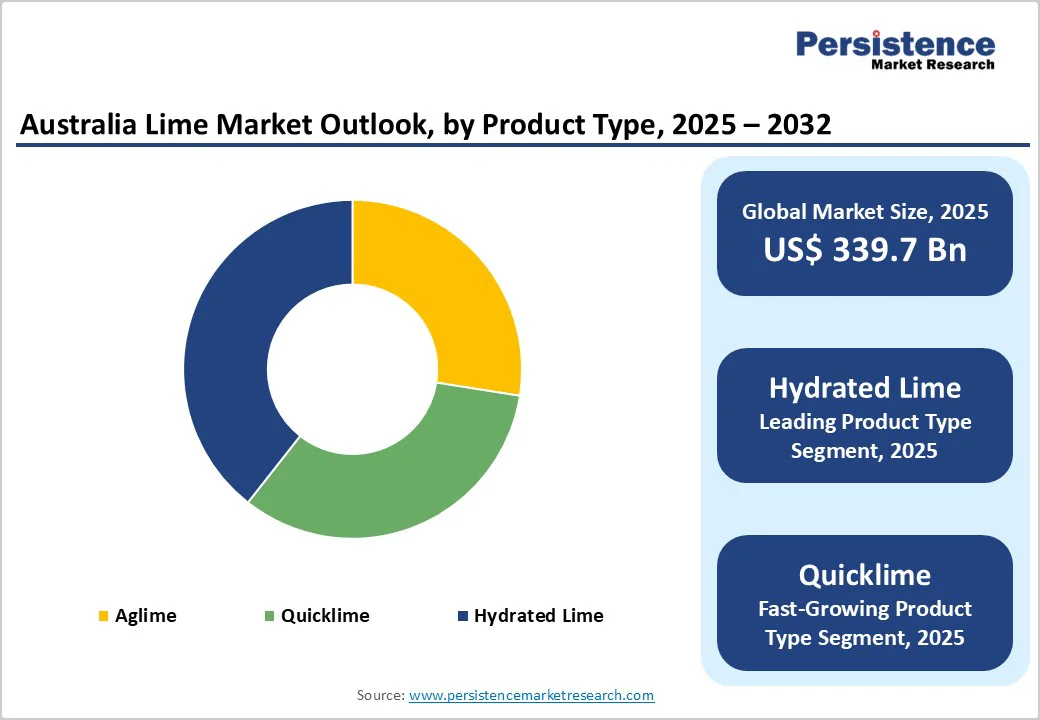

The Australia lime market size is likely to be valued at US$339.7 Billion in 2025 and is estimated to reach US$435.1 Billion in 2032, growing at a CAGR of 3.6% during the forecast period 2025 - 2032, boosted by its superior linkages to the country’s mining, construction, and infrastructure sectors.

Key Industry Highlights

- Leading State: Queensland, approximately 41.6% of the share in 2025, as it hosts abundant limestone reserves and several large-scale lime plants.

- Fastest-growing State: Northern Territory, owing to the expansion of mining projects in Tennant Creek and Gove.

- Sustainability Initiative: Adbri announced that it is working with Calix on a zero-emissions lime calciner project. This collaboration aims to develop a commercial-scale lime production facility with CO2 capture.

- Leading Product Type: Hydrated lime holds nearly 39.4% share in 2025, as it provides better handling safety, controlled reactivity, and easier blending than quicklime.

- Dominant Application: Metallurgy, approximately 37.3% of the Australia lime market share in 2025, since lime is indispensable in smelting and refining metals such as steel, copper, and gold by removing impurities.

- Key End-user Industry: Mining recorded about 35.8% share in 2025, with the surge in critical minerals and gold mining projects.

| Key Insights | Details |

|---|---|

| Australia Lime Market Size (2025E) | US$339.7 Bn |

| Market Value Forecast (2032F) | US$435.1 Bn |

| Projected Growth (CAGR 2025 to 2032) | 3.6% |

| Historical Market Growth (CAGR 2019 to 2024) | 2.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Increasing Use of Lime in Infrastructure Projects

Australia’s ongoing infrastructure boom, especially in large-scale transport projects, has drastically boosted lime consumption. The material is widely used for soil stabilization and base improvement in highways, airports, and rail developments. Projects such as the Inland Rail and Western Sydney Airport have relied heavily on lime-treated soils to improve load-bearing capacity and durability.

State governments, including those in Queensland and Victoria, are also investing in road rehabilitation programs that specify lime stabilization to extend pavement life. This sustained public and private sector investment continues to bolster consistent demand for lime across multiple construction phases.

Improved Soil Strength and Stability through Lime Treatment

Lime plays a key role in improving weak and moisture-sensitive soils, making it indispensable for Australia’s varied terrain. When mixed with clay-rich or expansive soils, lime triggers chemical reactions that reduce plasticity, increase density, and prevent shrink-swell behavior.

This is particularly valuable in regions such as Queensland and New South Wales, where reactive clay soils can compromise road and foundation stability. Engineers mainly prefer lime modification because it delivers a cost-effective and environmentally stable alternative to complete soil replacement, ensuring long-term structural reliability even under changing moisture conditions.

Barrier Analysis - High Carbon Emissions and Rising Compliance Burden

Lime manufacturing, especially quicklime calcination, is one of the most carbon-intensive industrial processes due to the thermal decomposition of limestone. Each ton of lime produced releases almost an equivalent amount of CO2, attracting scrutiny under Australia’s Safeguard Mechanism, which tightened emission limits in 2024. Producers such as Adbri and Graymont are now under pressure to adopt carbon capture and alternative fuel technologies to meet emission thresholds.

While these initiatives comply with national climate goals, they demand large upfront investments and add to production costs, making it difficult for small operators to remain competitive. The requirement for clean and low-carbon lime production has hence become both a technological challenge and a financial constraint for the market.

Health and Safety Concerns in Lime Handling

Lime dust, especially from hydrated lime, poses occupational hazards such as respiratory irritation, skin burns, and eye damage. The Australian Work Health and Safety (WHS) regulations have become stricter in recent years, requiring producers and contractors to implement better dust suppression systems, protective gear, and handling protocols. Non-compliance can result in heavy penalties and project delays.

For example, several construction firms across New South Wales have had to invest in sealed transport systems and improved ventilation to reduce worker exposure. These health-related safety requirements not only increase operational expenses but also slow down on-site efficiency, creating an additional barrier to growth for lime producers and end users alike.

Opportunity Analysis - Rising Potential for High-purity and Specialty Lime Applications

The market is witnessing increasing opportunities in the production of high-purity and nano-grade lime, pushed by emerging applications in pharmaceuticals, electronics, and advanced materials. These ultra-fine lime variants are being adopted for pH control in chemical synthesis and as fillers in precision manufacturing processes. Research collaborations between Australia’s universities and chemical firms are focusing on engineered lime composites with improved reactivity and purity.

For example, research and development projects in Western Australia are exploring nano-lime for use in corrosion-resistant coatings and biomedical materials. This shift toward specialized, high-value applications presents a new frontier for producers seeking to diversify beyond traditional construction and mining sectors.

Emergence of New Players Expanding Domestic Lime Supply

Australia’s market is gaining momentum with the entry of new producers aiming to strengthen regional supply chains. In 2024, Pacific Lime and Cement Limited launched its quicklime operations in Western Australia, targeting prominent mining and mineral processing clients.

The company’s strategy involves establishing regional supply hubs to reduce reliance on imported or interstate lime and ensure consistent availability for large industrial users. This expansion not only supports the fast-growing resources sector but also improves domestic production capacity, creating opportunities for partnerships, logistics development, and technology upgrades across Australia’s lime value chain.

Category-wise Analysis

Product Type Insights

Hydrated lime is anticipated to lead with approximately 39.4% of share in 2025, owing to its versatility and ease of handling compared to quicklime. It is less reactive and safer to transport and store, making it ideal for use in water treatment, flue gas desulfurization, and soil stabilization.

Its fine particle size allows for better mixing and consistent chemical reactions in industrial applications. In Australia, hydrated lime is widely used by municipal water utilities for pH correction and heavy metal removal. Its increasing use in environmental management projects and road soil improvement further reinforces its preference over other lime forms.

Quicklime is seeing steady demand as it remains indispensable in high-temperature industrial processes. It is a core reagent in steelmaking, alumina refining, and gold extraction, where it reacts instantly and delivers superior alkalinity.

In Queensland and Western Australia, mining and metallurgical operations continue to consume large volumes of quicklime, especially for gold ore processing and pH regulation in flotation circuits. Quicklime’s role as a flux in metallurgical reactions and a neutralizing agent in acid waste treatment ensures its relevance even as new technologies evolve.

Application Insights

Metallurgy is speculated to capture nearly 37.3% of the share in 2025, as lime is essential in refining metals such as steel, copper, nickel, and gold. It acts as a flux to remove impurities, including silica, sulfur, and phosphorus, from molten metal, improving product quality and reducing operational costs.

Australia’s well-established mining and metallurgical sector, especially in Western Australia and Queensland, pushes massive lime consumption. For example, leading steel producers and gold refineries in the Pilbara and Gladstone regions rely on locally sourced lime for smelting and processing.

Agriculture is a key application because lime is essential for correcting soil acidity, improving nutrient absorption, and promoting high crop yields. Australian farmlands, specifically in Queensland and New South Wales, often have naturally acidic soils that require regular liming to maintain productivity.

Aglime (agricultural lime) improves the effectiveness of fertilizers and improves microbial activity in the soil. The rise of regenerative and precision farming practices has further increased the use of lime, as farmers now focus on soil health as a long-term investment.

End-user Industry Insights

Mining will likely hold a share of about 35.8% in 2025, as lime plays multiple key roles across mineral extraction and processing stages. It is used for pH control in flotation, cyanide destruction in gold processing, and acid neutralization in mine wastewater.

The demand is skyrocketing in Australia’s gold, nickel, and copper mining belts. For example, the Kalgoorlie and Mount Isa mining hubs use large quantities of lime daily to treat tailings and maintain process water quality. Mining companies prefer high-purity quicklime as it reduces reagent consumption and improves metallurgical recovery rates.

Construction is a fast-growing end-use industry as lime improves the durability and strength of materials used in infrastructure projects. It improves soil stability, strengthens road bases, and is a key ingredient in mortar and plaster.

In Australia, lime-treated soils are commonly used in highway and railway foundation projects to handle reactive clay soils, especially in Queensland and Victoria. The Inland Rail Project, for instance, utilized lime stabilization to improve subgrade performance across long stretches of track.

State Insights

Queensland Lime Market Trends

Queensland is predicted to account for approximately 41.6% of the share in 2025, supported by both national producers and regional suppliers catering to the mining, agriculture, and construction industries.

Companies such as Graymont operate lime plants in areas, including Gympie, supplying quicklime and hydrated lime to industrial clients. Local producers such as South Queensland Lime have also been expanding production to meet the rising demand from the state’s agriculture sector, especially in soil treatment and crop management.

The mining industry, mainly around Mount Isa and Gladstone, remains a key consumer due to lime’s use in ore processing and environmental control. In recent years, the state has also seen increasing emphasis on sustainable lime production, with projects exploring low-emission kiln technologies and alternative fuels to comply with Queensland’s decarbonization goals.

Northern Territory Lime Market Trends

In the Northern Territory, the market is relatively small but important for supporting the region’s mining and water treatment activities. Due to its remote geography, lime supply here is dominated by a few local producers and quarry operators that focus on bulk deliveries to mining sites. Companies such as Micronized Minerals and local quarries near Katherine and Tennant Creek provide quicklime and agricultural lime for use in mineral extraction, soil conditioning, and wastewater management.

Logistics costs remain a major challenge since most lime must be transported over long distances, often from interstate suppliers. To overcome this, some local operators maintain storage depots and dedicated truck fleets to ensure timely supply to remote mines and construction projects.

New South Wales Lime Market Trends

New South Wales has one of Australia’s most established lime production networks, anchored by Graymont’s Galong plant, which supplies quicklime to steelmakers, water treatment plants, and construction companies across the state.

The region’s demand is mainly propelled by industrial and infrastructure projects, as well as by the agricultural sector in inland areas. Environmental compliance is a defining factor here, with producers required to meet strict emissions and sustainability standards.

Several lime suppliers in New South Wales are adopting energy-efficient kilns and clean production methods to meet government regulations and customer expectations. The market is also competitive among mid-sized producers catering to niche uses, including high-purity lime for chemical applications and hydrated lime for wastewater treatment.

Competitive Landscape

The Australia lime market is dominated by a few key players such as Adbri Ltd, Graymont, and Omya Australia, which have superior control over production and distribution networks.

Adbri, formerly Adelaide Brighton, operates several lime plants across South Australia and Western Australia, catering to the construction, mining, and industrial sectors. Graymont, a global lime producer, strengthened its presence in the country by acquiring Sibelco’s lime business in 2019, giving it access to key facilities in New South Wales and Victoria.

Key Industry Developments

- In April 2025, Graymont announced a new lime-production investment in Victoria. The expansion is at its Traralgon plant and associated limestone quarry in Buchan.

- In June 2025, Adbri published a new Environmental Product Declaration (EPD) for its lime products, including quicklime and hydrated lime.

Companies Covered in Australia Lime Market

- Lime Group Australia

- Wagners

- Omya Australia Pty Ltd.

- Sibelco Australia

- Boral Ltd.

- Adelaide Brighton Ltd.

- Calcimo Lime & Fertilizers Pty Ltd.

- Agricola Mining Pty Ltd

- Swan Cement Limited

- Cockburn Cement Limited

Frequently Asked Questions

The Australia lime market is projected to reach US$339.7 Billion in 2025.

Increasing lime consumption in mining and surging adoption of low-carbon lime kilns are the key market drivers.

The Australia lime market is poised to witness a CAGR of 3.6% from 2025 to 2032.

Rising investments in low-emission lime technologies and the entry of new producers are the key market opportunities.

Lime Group Australia, Wagners, and Omya Australia Pty Ltd. are a few key market players.