- Pharmaceuticals

- Asia Pacific Alopecia Treatment Market

Asia Pacific Alopecia Treatment Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Asia Pacific Alopecia Treatment Market by Disease Type (Alopecia Areata, Androgenetic Alopecia, Central Centrifugal Cicatricial Alopecia, Chemotherapy Induced Alopecia, and Others), by Treatment Type (Pharmaceuticals Drugs, Topical Formulations, Device-based Therapies, Surgical Procedures, and Others), Route of Administration (Oral, Injectable, and Topical), End-user, and Regional Analysis from 2026 to 2033

Asia Pacific Alopecia Treatment Market Share and Trends Analysis

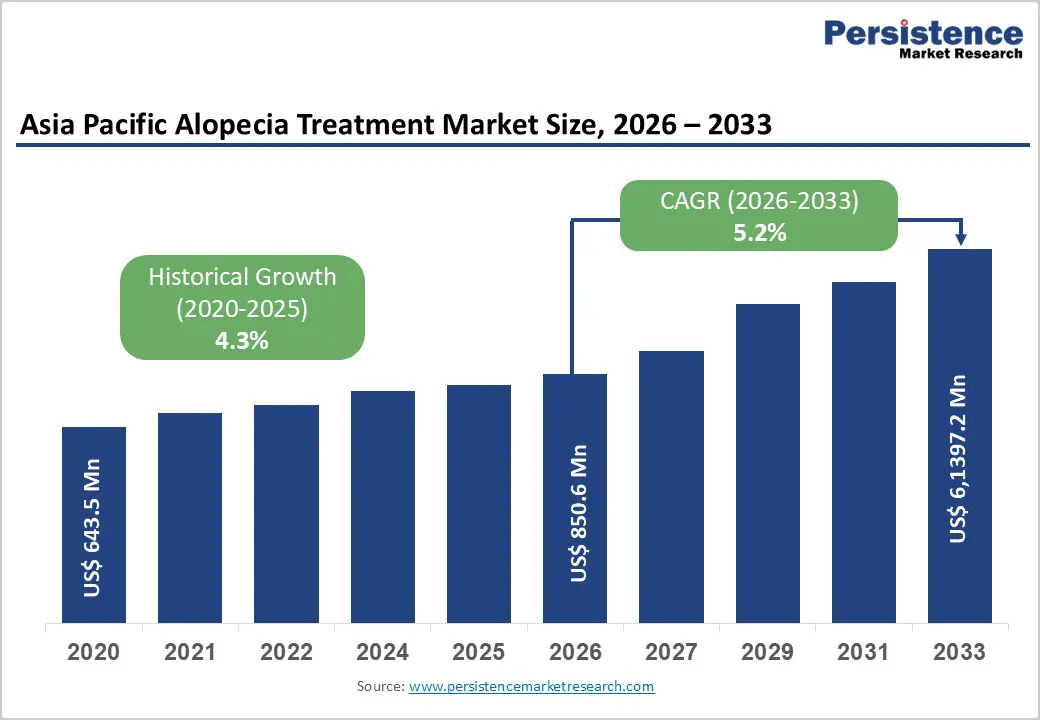

Asia Pacific alopecia treatment market size is likely to be valued at US$ 850.6 million in 2026 to reach US$ 1,397.2 million by 2033, growing at a CAGR of 5.2% during the forecast period from 2026 to 2033.

Global demand for alopecia treatment solutions in the Asia Pacific is rising steadily, driven by the increasing prevalence of hair loss conditions, growing aesthetic awareness, and the rapid shift toward early diagnosis and long-term management of alopecia. Dermatology and trichology clinics are increasingly adopting a wide range of treatment options, including topical formulations, oral medications, injectable therapies, and device-based solutions, to support accurate diagnosis, personalized treatment planning, and improved clinical outcomes.

Growing investments in healthcare infrastructure, expansion of organized dermatology and aesthetic clinic chains, and wider availability of cost-effective treatment options are accelerating adoption across both developed and emerging markets. Continuous advancements in drug formulations, delivery mechanisms, combination therapies, and clinic-based technologies are improving treatment efficacy, patient compliance, and overall care experience. In addition, rising patient awareness, expanding access to specialist care, and increasing acceptance of aesthetic and medical hair loss treatments are further supporting sustained regional market growth.

Key Industry Highlights

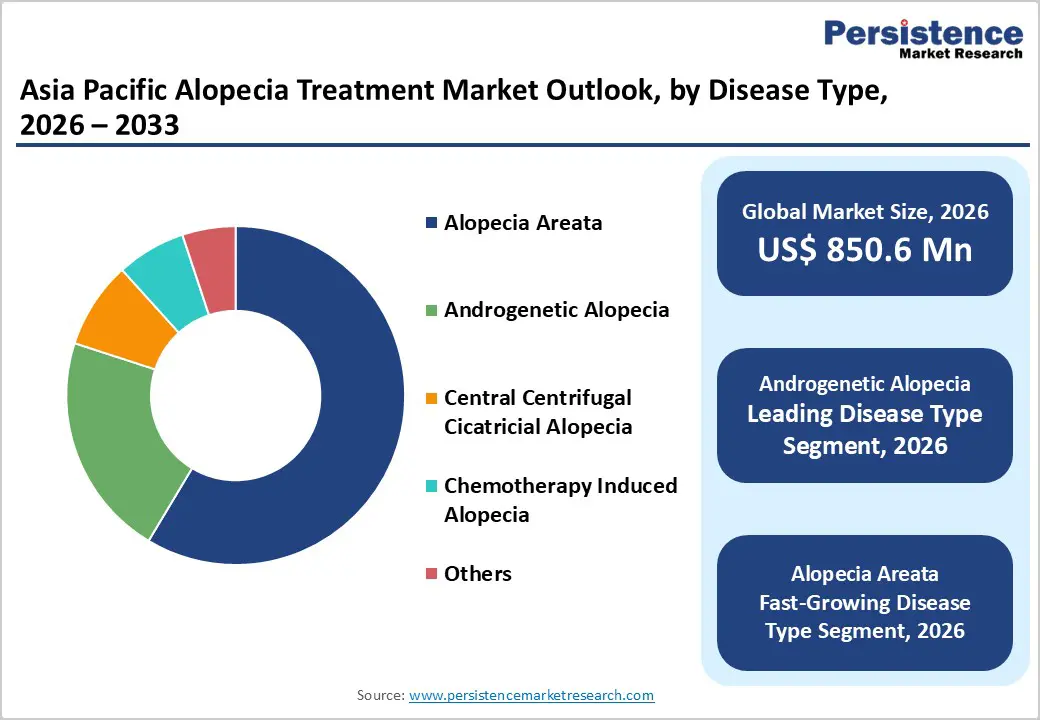

- Leading Disease Type Segment: Androgenetic alopecia dominates the market due to its high prevalence among both men and women, chronic treatment requirements, and widespread use of topical and oral maintenance therapies.

- Fastest-Growing Disease Type Segment: Alopecia areata is witnessing rapid growth driven by increasing diagnosis rates, rising adoption of injectable and systemic therapies, and growing availability of advanced treatment options.

- Leading Treatment Type Segment: Topical formulations remain the leading treatment type, supported by over-the-counter availability, high patient compliance, suitability for long-term use, and strong presence across retail and online channels.

- Fastest-Growing Treatment Type Segment: Device-based therapies are growing rapidly due to rising adoption of PRP, microneedling, low-level laser therapy, and combination treatment approaches in clinical and aesthetic settings.

- Leading End-user Segment: Dermatology and trichology clinics remain the leading end-users, driven by high patient volumes, specialist-led diagnosis, and increasing utilization of prescription, injectable, and procedural treatments.

- Fastest-Growing End-user Segment: Aesthetic clinics are expanding rapidly as demand rises for cosmetic hair restoration procedures, minimally invasive therapies, and personalized treatment programs among urban populations.

| Key Insights | Details |

|---|---|

| Asia Pacific Alopecia Treatment Market Size (2026E) | US$ 850.6 Mn |

| Market Value Forecast (2033F) | US$ 1397.2 Mn |

| Projected Growth (CAGR 2026 to 2033) | 5.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Dynamics

Driver - Rising Aesthetic Consciousness and Expanded Access to OTC and Digital Alopecia Therapies

Growing aesthetic awareness across Asia Pacific is significantly influencing the demand for alopecia treatment solutions, as personal appearance is increasingly linked to social confidence, professional image, and overall quality of life. The widespread use of social media platforms, growing visibility of cosmetic procedures, and heightened exposure to appearance-driven content have amplified awareness of hair loss and available treatment options. In parallel, evolving workplace norms and competitive professional environments are encouraging both men and women to proactively seek medical and cosmetic interventions for hair restoration. This shift in perception has reduced stigma associated with hair loss and increased acceptance of long-term treatment, driving higher consultation rates at dermatology, trichology, and aesthetic clinics. Rising disposable incomes and greater emphasis on preventive and appearance-enhancing healthcare further support sustained market growth, particularly in urban and semi-urban regions.

Improved access to over-the-counter and online therapies is further accelerating market penetration by making alopecia treatments more convenient, affordable, and widely available. Topical formulations such as minoxidil are now easily accessible through retail pharmacies, e-commerce platforms, and direct-to-consumer brands, enabling early intervention without the need for immediate specialist consultation. The rapid expansion of digital health platforms and tele-dermatology services allows patients to receive guidance, prescriptions, and follow-up care remotely, improving adherence and continuity of treatment. Subscription-based models, bundled product offerings, and targeted digital marketing are also enhancing patient engagement and repeat purchases. Collectively, these developments are lowering access barriers, expanding the treated population, and strengthening long-term demand for alopecia treatments across the Asia Pacific region.

Restraints - Treatment Efficacy Variability and High Cost of Advanced Therapies Limit Market Adoption

Variable treatment outcomes remain a key restraint in the Asia Pacific alopecia treatment market, as clinical response to available therapies often differs significantly among patients. Many treatments require prolonged or lifelong use to maintain results, particularly in chronic conditions such as androgenetic alopecia. Delayed visible improvement, partial hair regrowth, or relapse after discontinuation can lead to patient dissatisfaction and reduced adherence. Inconsistent outcomes also affect patient trust, especially in early-stage or self-directed treatment through OTC products, resulting in treatment discontinuation and lower long-term engagement with therapy. These factors collectively constrain sustained treatment uptake despite rising awareness and availability of solutions.

The high cost of advanced therapies further limits market penetration, particularly in price-sensitive Asia Pacific markets. Injectable treatments, platelet-rich plasma (PRP) procedures, device-based therapies, and newer systemic drugs often involve significant out-of-pocket expenditure, as most alopecia treatments are not covered by insurance. Repeated treatment sessions and maintenance protocols add to the overall financial burden, restricting access to higher-income urban populations. This cost barrier slows adoption of innovative therapies, widens the gap between basic and advanced treatment utilization, and limits broader market expansion across emerging economies in the region.

Opportunity - Product Innovation and Digital Care Models Create New Growth Opportunities

Product innovation and the development of combination therapies present significant growth opportunities in the Asia Pacific alopecia treatment market. Advances in topical formulations with improved penetration, enhanced stability, and reduced side effects are increasing treatment effectiveness and patient compliance. Combination regimens that integrate topical agents, oral medications, nutraceuticals, and device-based therapies are gaining traction as they address multiple underlying causes of hair loss and deliver better clinical outcomes. In parallel, growing interest in personalized treatment approaches based on hair loss severity, gender, and lifestyle factors is enabling differentiation for manufacturers and clinics, supporting premium pricing and improved patient retention.

Furthermore, the expansion of tele-dermatology and direct-to-consumer (DTC) models is further boosting market growth. Digital consultation platforms allow patients to seek specialist advice remotely, reducing geographic and time-related barriers to care. Online prescription services and subscription-based hair care programs ensure continuous treatment access, improve adherence, and generate recurring revenue streams. DTC brands are leveraging data-driven marketing, remote monitoring, and customized product offerings to reach younger, tech-savvy consumers. Collectively, these digital care models are expanding the addressable patient base, improving continuity of treatment, and accelerating long-term growth of the alopecia treatment market across the Asia Pacific region.

Category-wise Analysis

By Disease Type, Androgenetic Alopecia Dominates Owing to High Prevalence and Long-Term Treatment Demand

The androgenetic alopecia segment is projected to dominate the Asia Pacific alopecia treatment market in 2026, accounting for a revenue share of 58.6%. This dominance is driven by the high prevalence of male and female pattern hair loss across the region, coupled with genetic predisposition, lifestyle factors, and rising stress levels. The chronic and progressive nature of the condition necessitates long-term, often lifelong, management, resulting in sustained demand for treatment. Widespread adoption of topical formulations such as minoxidil, oral DHT inhibitors including finasteride and dutasteride, and adjunct therapies such as nutraceuticals and device-based solutions supports consistent treatment uptake. Additionally, increasing aesthetic awareness, improved access to dermatology and trichology services, early diagnosis, and growing availability of OTC and online treatment options continue to reinforce strong and recurring demand for this segment across Asia Pacific.

By Treatment Type, Topical Formulations Dominate Due to High Adoption and OTC Accessibility

The topical formulations segment is projected to dominate the Asia Pacific alopecia treatment market in 2026, accounting for a significant revenue share of 34.2%. This leadership is attributed to the widespread availability of topical agents such as minoxidil through both over-the-counter and prescription channels, high patient compliance, ease of application, and suitability for long-term maintenance therapy. Topical treatments are commonly adopted as first-line therapy for androgenetic alopecia and early-stage alopecia areata due to their favorable safety profile and minimal systemic side effects. The strong presence of domestic and multinational brands, expanding penetration of e-commerce and direct-to-consumer platforms, increasing dermatologist recommendations, and rising preference for non-invasive and cost-effective treatment options further support sustained demand for topical formulations across Asia Pacific.

By End-user, Dermatology and Trichology Clinics Dominate Globally Due to High Patient Volumes and Chairside Imaging Adoption

The dermatology and trichology clinics segment is expected to dominate the Asia Pacific alopecia treatment market in 2026, capturing a revenue share of 47.8%. These clinics serve as the primary point of diagnosis and treatment initiation for both medical and cosmetic hair loss conditions, driving consistent utilization of prescription drugs, injectable therapies, and device-based procedures. Rising patient awareness, growing emphasis on early and accurate diagnosis, and increasing demand for specialist-led and customized treatment plans are accelerating clinic-based adoption. The wider availability of advanced therapies such as PRP, intralesional injections, and systemic treatments, along with improved clinical outcomes, is further supporting growth. Additionally, the rapid expansion of organized dermatology chains, trichology centers, and aesthetic clinic networks across major urban centers, supported by medical tourism and improving healthcare infrastructure, continues to reinforce this segment’s leading position in the region.

Competitive Landscape

Asia Pacific alopecia treatment market is moderately to highly competitive, with prominent players such as Pfizer Inc., Teva Pharmaceutical Industries Ltd., Merck & Co., Inc., Johnson & Johnson, and Dr. Reddy’s Laboratories. These companies leverage diversified pharmaceutical portfolios, strong dermatology and immunology pipelines, established brands, and extensive regional distribution networks to strengthen their presence across hospitals, dermatology clinics, specialty hair clinics, and retail and online pharmacy channels.

Manufacturers are increasingly focused on expanding therapeutic options and improving treatment outcomes through the development of advanced systemic therapies, novel topical formulations, and combination treatment approaches. Strategic priorities include continuous product innovation, expansion into high-growth Asia Pacific markets, partnerships with dermatology clinics and aesthetic chains, and alignment with evolving regulatory and reimbursement frameworks to support wider adoption of alopecia treatments and sustain long-term market growth.

Key Industry Developments:

- In December 2025, Nektar Therapeutics announced positive topline results from the 36-week induction phase of its Phase 2b REZOLVE-AA trial evaluating rezpegaldesleukin, a first-in-class IL-2 pathway agonist and regulatory T-cell (Treg) proliferator, for the treatment of alopecia areata, highlighting its potential as a novel immunomodulatory therapy in this indication.

- In December 2025, Cosmo Pharmaceuticals N.V., announced compelling topline results from its two pivotal Phase III clinical trials evaluating clascoterone 5% topical solution for the treatment of male androgenetic alopecia (AGA), marking a potential first major therapeutic breakthrough in hair-loss treatment in more than three decades.

- In June 2023, Pfizer Inc. announced that the U.S. Food and Drug Administration (FDA) approved LITFULO™ (ritlecitinib), a once-daily oral treatment, for individuals 12 years of age and older with severe alopecia areata. The approved recommended dose is 50 mg, making LITFULO the first and only FDA-approved treatment for adolescents (12+) with severe alopecia areata.

Companies Covered in Asia Pacific Alopecia Treatment Market

- Pfizer Inc.

- Teva Pharmaceutical Industries Ltd.

- Merck & Co., Inc.

- Johnson & Johnson

- Dr.Reddy’s Laboratories

- Cipla

- AbbVie Inc.

- Anagenics Limited.

- Himalaya Wellness Company

- Taisho Pharmaceutical Co., Ltd.

- Shiseido Company, Limited

- Beijing Zhangguang 101 Science & Technology Co., Ltd.

- Giuliani

- Pelage

- Others

Frequently Asked Questions

Asia Pacific alopecia treatment market size is projected to be valued at US$ 850.6 million in 2026.

Rising prevalence of hair loss, increasing aesthetic consciousness, expanding middle-class healthcare spending, and rapid adoption of OTC, clinic-based, and digital dermatology solutions drive market growth.

Asia Pacific alopecia treatment market is poised to witness a CAGR of 5.2% between 2026 and 2033.

Strong opportunities exist in affordable OTC topicals, DTC and tele-dermatology platforms, clinic-based device therapies, and gradual uptake of advanced systemic treatments in urban centers.

Pfizer Inc., Teva Pharmaceutical Industries Ltd., Merck & Co., Inc., Johnson & Johnson, and Dr.Reddy’s Laboratories are some of the key players in the Asia Pacific alopecia treatment market.