- Hardware & Software IT Services

- Application Delivery Controller Market

Application Delivery Controller Market Size, Share, and Growth Forecast, 2026 - 2033

Application Delivery Controller market by Component Type (Hardware ADC and Software/Virtual ADC.), Organisation Size (Small & Medium Enterprises (SMEs), Large Enterprises), Deployment Mode (Public Cloud, Private Cloud, Hybrid iPaaS), Industry (Banking, Financial Services & Insurance (BFSI), IT & Telecom, Retail & E-commerce, Healthcare & Life Sciences, Manufacturing, Government & Public Sector) and Regional Analysis for 2026 - 2033

Application Delivery Controller Market Size and Trends Analysis

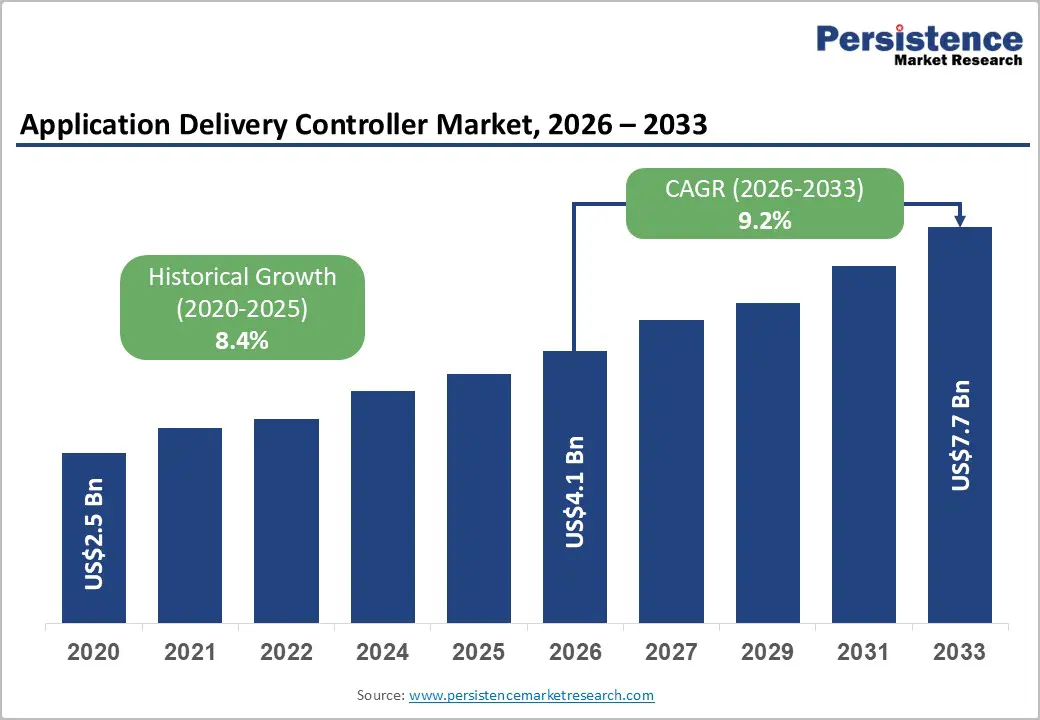

The global application delivery controller market size is likely to be valued at US$ 4.1 billion in 2026 and is projected to reach US$ 7.7 billion by 2033, expanding at a CAGR of 9.2% between 2026 and 2033. This substantial growth trajectory reflects the critical role of application delivery controllers in modern enterprise infrastructure, driven by the accelerating digital transformation across financial services, telecommunications, and cloud-native computing environments.

The market's expansion is underpinned by three primary factors: the proliferation of multi-cloud and hybrid infrastructure deployments requiring sophisticated load-balancing and security capabilities; the exponential growth of API-driven architecture and AI-powered applications necessitating advanced traffic management; and the intensifying cybersecurity threats demanding integrated application delivery and security solutions. As enterprises worldwide transition from legacy, hardware-dependent systems to flexible, software-defined architectures, the Application Delivery Controller Market is positioned as a strategic enabler of digital resilience and operational efficiency.

Key Industry Highlights:

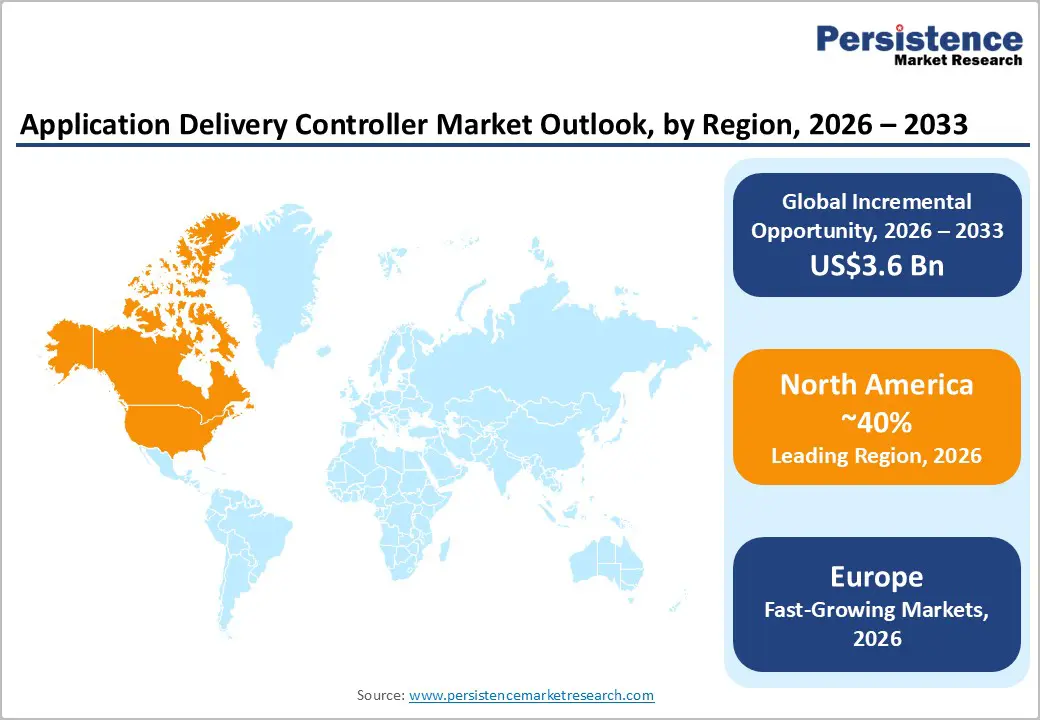

- Regional Leadership: North America dominates the global Application Delivery Controller market with ~40% share, supported by mature cloud adoption, high enterprise IT spending, and continuous innovation from leading ADC vendors.

- Fast-growing Regional Market: Europe holds ~25% market share, driven by a large BFSI sector, stringent regulatory frameworks (GDPR, cybersecurity, payment systems), and sustained investment in secure application delivery infrastructure

- Fast-performing Market: East Asia accounts for ~18% of the market, with China and Japan fueling growth through rapid digital banking expansion, large-scale cloud infrastructure buildout, and rising containerised workloads.

- Leading End-user: BFSI leads application demand with ~26% share, reflecting the sector’s dependence on high-availability, secure, and compliant application delivery for digital banking and transaction processing

- Growth Indicator: Accelerating digital transformation and multi-cloud infrastructure adoption are pushing enterprises toward software-defined ADC platforms with unified management, automation, and Kubernetes integration.

| Key Insights | Details |

|---|---|

|

Application Delivery Controller Market Size (2026E) |

US$ 4.1 Bn |

|

Market Value Forecast (2033F) |

US$ 7.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

9.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

8.4% |

Market Dynamics

Drivers - Digital Transformation and Multi-Cloud Infrastructure Adoption

Digital transformation initiatives have fundamentally reshaped enterprise IT infrastructure requirements, compelling organisations to deploy applications across heterogeneous environments spanning on-premises data centres, public cloud platforms, and edge computing nodes. The Application Delivery Controller Market has responded to this structural shift by evolving from hardware-centric solutions toward flexible, software-defined architectures capable of managing traffic across AWS, Azure, Google Cloud, and private infrastructure simultaneously.

Financial institutions in developed economies have accelerated their cloud migration timelines, with banking-sector digitalisation projects driving ADC adoption for secure, high-performance application delivery across distributed infrastructure. The transition creates demand for ADC solutions offering unified management interfaces, automated scaling capabilities, and seamless integration with containerized and Kubernetes-based workloads. This infrastructure evolution directly correlates with the projected CAGR of around 9%-10% for the Application Delivery Controller Market through 2033, as organisations require mature, enterprise-grade solutions to orchestrate application delivery across multiple cloud environments while maintaining security, compliance, and performance standards.

API Proliferation and AI-Powered Application Complexity

The exponential expansion of Application Programming Interface (API) ecosystems and the integration of artificial intelligence capabilities into enterprise applications have created unprecedented complexity in application delivery infrastructure. Modern enterprises operate thousands of APIs across their digital ecosystems, each requiring granular traffic management, security validation, and performance optimization.

Recent product enhancements announced by major ADC vendors demonstrate market responsiveness to this driver: F5's expanded API discovery tools and Large Language Model vulnerability scanning capabilities directly address organizations' needs to identify, catalogue, and secure their burgeoning API inventory. Similarly, emerging threats from AI-generated attacks and prompt-injection vulnerabilities necessitate ADC solutions with specialised threat-detection mechanisms.

The integration of AI-driven analytics into Application Delivery Controller solutions enables organisations to predict performance degradation, automatically remediate configuration anomalies, and implement self-healing network functions. This technological convergence between application delivery, API management, and artificial intelligence security represents a fundamental evolution of the ADC market, with vendors differentiating through intelligent, learning-based solutions rather than static rule engines.

Restraint - Capital Intensity and Operational Complexity

Implementing comprehensive Application Delivery Controller solutions requires substantial capital expenditure, particularly for organizations managing diverse infrastructure portfolios that span hardware ADC deployments, virtual instances, and cloud-native variants. The transition from traditional hardware ADC systems to software-defined and cloud-native architectures demands significant retraining of IT personnel, architectural redesigns, and extended implementation timelines.

Organizations must navigate licensing complexities across multiple deployment models, negotiate vendor commitments for long-term partnerships, and manage integration challenges with existing monitoring, automation, and security infrastructure. These operational barriers particularly constrain adoption among mid-market organizations and smaller financial institutions, limiting the Application Delivery Controller Market's penetration in segments where legacy systems continue to function adequately despite performance limitations.

Opportunity - Managed Service Provider (MSP) and ADC-as-a-Service Expansion

The transition toward Application Delivery Controller consumption models that emphasize managed services, software-as-a-service delivery, and outcome-based pricing represents a fundamental market evolution that enables broader organizational access to enterprise-grade ADC capabilities. Rather than requiring organizations to manage complex ADC infrastructure internally, MSPs can aggregate customer workloads onto shared, multi-tenant Application Delivery Controller platforms offering flexible licensing, automatic scaling, integrated security, and operational intelligence. This service model particularly addresses the needs of mid-market organizations, regional banks, and smaller financial institutions that lack specialised ADC expertise. Recent market developments demonstrate vendor recognition of this opportunity: Radware's emphasis on ADC-as-a-Service solutions supporting hardware and virtual form factors with flexible licensing and auto-scaling capabilities directly targets MSP requirements for resilient, scalable platforms.

The MSP opportunity enables the Application Delivery Controller Market to expand beyond traditional enterprise segments into underserved organizational categories, potentially accelerating market growth as service-based consumption models reduce capital barriers and operational complexity.

Emerging Managed Service Provider platforms are integrating advanced capabilities previously available only to large enterprises, including AI-powered operational intelligence, automated threat response, and multi-cloud orchestration. This democratization of ADC capabilities through service-based consumption models can stimulate demand across previously underserved segments, extending the addressable market beyond current boundaries and enabling organizations of all sizes to implement sophisticated application delivery and security strategies.

AI-Driven Security and Intelligent Traffic Orchestration

The convergence of artificial intelligence capabilities and application delivery infrastructure creates an opportunity for next-generation ADC solutions offering intelligent threat detection, predictive performance optimization, and autonomous remediation of infrastructure anomalies. Rather than relying on static rules and manual configuration, AI-augmented Application Delivery Controller solutions can analyse traffic patterns, identify anomalous behaviours indicative of security threats or performance degradation, and automatically implement corrective actions without human intervention. Vendor developments illustrate this opportunity: F5's expanded LLM vulnerability-scanning tools and AI-driven threat-intelligence mechanisms address the emerging category of AI-generated attacks and prompt-injection exploits targeting AI-integrated applications.

Radware's integration of AI-powered operational intelligence enables organizations to implement real-time performance monitoring, dynamic threat response, and self-healing network functions. This opportunity enables the Application Delivery Controller Market to establish itself as a critical component of AI-native security architectures rather than a commodity infrastructure element, potentially commanding premium valuations and sustaining high growth rates as organizations invest substantially in intelligent security infrastructure.

The AI-driven security opportunity particularly addresses emerging threat vectors, including encrypted exploits, advanced persistent threats targeting API infrastructures, and adversarial attacks against AI-powered applications. Organizations deploying AI capabilities throughout their digital ecosystems require sophisticated, learning-based application delivery solutions that can identify novel attack patterns and implement autonomous protective measures without human analysis overhead.

Category-wise Analysis

Solution Type Insights

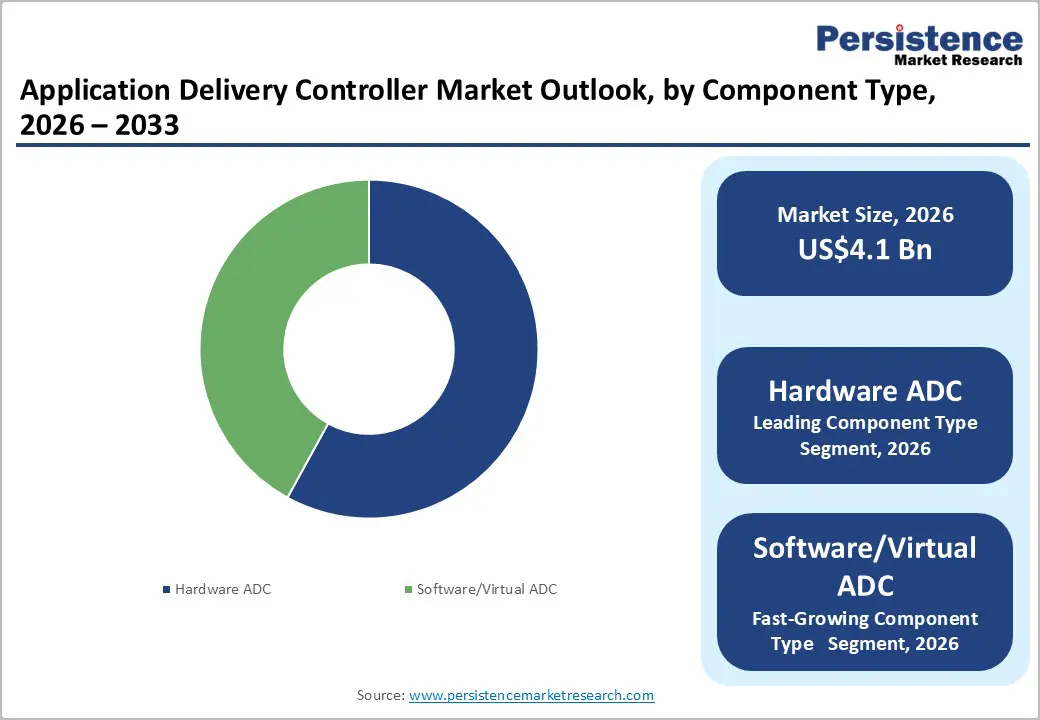

Hardware application delivery controllers maintained 58% share in 2026, representing the dominant component type within the broader ADC market. This leadership position reflects the persistence of hardware-based solutions in large enterprise environments where organizations require dedicated, high-performance appliances for managing mission-critical application traffic with minimal latency and maximum throughput.

Hardware ADC solutions offer deterministic performance characteristics, integrated security modules combining DDoS protection, TLS/SSL offload, and Web Application Firewall capabilities, and deep integration with enterprise network infrastructure. Organizations managing high-traffic financial services platforms, e-commerce infrastructure, and telecommunications networks continue to deploy hardware ADC solutions as foundational infrastructure components, recognizing their reliability, performance characteristics, and long operational life cycles.

The sustained share of hardware ADCs reflects organizational risk aversion regarding mission-critical application delivery, with enterprises preferring dedicated hardware appliances over shared virtualized or cloud-based alternatives for performance-sensitive workloads. However, this hardware-dominant market structure is evolving as organizations recognize operational benefits of software-defined and cloud-native architectures, creating opportunities for alternative deployment models.

Software-defined and virtual Application Delivery Controller solutions are the fastest-growing component type in the market, as organizations transition to flexible, scalable architectures that adapt to dynamic cloud infrastructure requirements. Virtual ADC solutions operating on virtualized hypervisors (vSphere, Hyper-V) and cloud-native variants deployed within public cloud environments (AWS, Azure, GCP) enable organizations to scale application delivery capacity dynamically, reduce capital expenditures through software-based consumption models, and simplify management through unified interfaces.

Industry Insights

The Banking, Financial Services, and Insurance (BFSI) sector commands approximately 26.0% market share, reflecting the sector's strategic dependence on sophisticated, secure, and reliable application delivery infrastructure. BFSI organizations operate globally distributed transaction-processing systems that manage extreme traffic volumes with zero-downtime requirements, necessitating application delivery controller solutions that offer high availability, advanced security, and compliance validation mechanisms.

European financial and insurance activities generated €0.9 trillion in value added in 2022, with financial services across Germany, France, Italy, Spain, and Poland accounting for over 65% of sector value added. European banking assets reached €43.6 trillion in 2023, supporting complex transaction ecosystems requiring Application Delivery Controller solutions for performance assurance and regulatory compliance.

China's banking assets totalled RMB 467.3 trillion by Q2 2025, with inclusive loans to micro and small enterprises reaching RMB 36 trillion, representing massive infrastructure supporting diverse financial products and services. Latin American banking sectors, facing legacy system limitations and fintech competition, are undertaking comprehensive modernisation initiatives that emphasise real-time payment capabilities and digital customer experiences, driving demand for modern Application Delivery Controller solutions to replace deprecated infrastructure.

Regional Insights and Trends

North America Application Delivery Controller Market Trends

North America commands 40% of the global Application Delivery Controller Market, representing the largest regional market and primary driver of innovation within the ADC industry. The region's dominance reflects mature cloud computing adoption, high enterprise IT spending, and concentration of global ADC vendors headquartered in North America.

United States financial services organisations, representing the world's largest banking sector with total assets exceeding US$ 20 trillion, have extensively deployed Application Delivery Controller solutions to manage complex transaction processing infrastructure, API-driven banking platforms, and integrated security systems. American technology companies and cloud platform providers (Amazon Web Services, Microsoft Azure, Google Cloud) have standardised ADC technologies within their infrastructure, establishing Application Delivery Controller solutions as fundamental components of cloud computing platforms consumed globally.

Recent developments demonstrate North America's continued leadership in ADC innovation: F5's February 2025 unveiling of expanded API discovery tools and LLM vulnerability scanning capabilities addresses emerging security requirements for AI-integrated applications, while the April 2025 launch of F5's unified Application Delivery and Security Platform represents the vendor's strategy to converge load balancing and security functions. These vendor innovations, prioritising North American market requirements, subsequently influence global ADC technology trends.

The region's regulatory environment, particularly Securities and Exchange Commission (SEC) requirements for cybersecurity disclosure and financial system resilience mandates, drives organisational investments in sophisticated application delivery and security infrastructure. Investment in North American ADC infrastructure is expected to remain robust through the forecast period, with enterprises continuously upgrading solutions to incorporate AI-driven intelligence, enhanced API security capabilities, and multi-cloud orchestration features.

East Asia Application Delivery Controller Market Trends

East Asia represents 18% of the global Application Delivery Controller Market, with China and Japan emerging as critical growth markets driven by rapid digital transformation, large financial services sectors, and expansion of cloud computing infrastructure. China's banking assets reached RMB 467.3 trillion by Q2 2025, growing 7.9% year-on-year, with large commercial banks accounting for 43.7% of total banking assets and supporting massive digital transformation initiatives emphasizing real-time payment systems and mobile financial services.

The Chinese financial services sector's growth has necessitated substantial investments in application delivery infrastructure, with state-owned and commercial banks deploying ADC solutions to manage explosive traffic growth from digital banking services, fintech platforms, and cross-border payment systems.

China's telecommunications sector, operating the world's largest mobile networks and fibre optic infrastructure, has become a significant driver of ADC adoption as operators implement software-defined networking, network function virtualization, and edge computing capabilities.

The region's rapid containerization and Kubernetes adoption among technology companies is driving demand for container-native Application Delivery Controller solutions, with Chinese cloud providers and technology enterprises establishing themselves as significant ADC consumers. Regulatory requirements, including data localisation mandates, payment system security standards, and compliance with Chinese cybersecurity frameworks, are influencing ADC infrastructure investments, with organisations prioritising solutions offering comprehensive threat detection and compliance validation capabilities. Japan's mature financial services sector and advanced telecommunications infrastructure similarly support significant ADC markets, with organizations investing in next-generation solutions incorporating AI-driven intelligence and multi-cloud orchestration capabilities.

Europe Application Delivery Controller Market Trends

Europe accounts for 25% of the global Application Delivery Controller Market, reflecting the region's mature financial services sector, advanced telecommunications infrastructure, and stringent regulatory environment influencing application delivery requirements. The European financial and insurance sector generated €0.9 trillion in value added in 2022, employing nearly 5 million people across almost 867,000 enterprises, with Germany, France, Italy, Spain, and Poland accounting for over 65% of sector value added.

European banking sector assets totalled €43.6 trillion in 2023, with deposits rising 1.2% to €17.3 trillion, supporting complex regulatory requirements including General Data Protection Regulation (GDPR) compliance, payment system regulations, and market infrastructure regulations. These regulatory frameworks establish mandatory requirements for application availability, data protection, and transaction integrity that drive organizations' investments in sophisticated Application Delivery Controller solutions.

Competitive Landscape

The global application delivery controller market is largely consolidated, with a few key players capturing significant market share while smaller vendors compete in niche segments. Leading companies such as Informatica Inc., Boomi, Inc. (Dell Boomi), SAP SE, Oracle Corporation, Salesforce’s MuleSoft, and IBM Corporation dominate the market with enterprise-grade integration solutions that offer hybrid and multi-cloud support, AI-driven automation, and low-code/no-code capabilities. These top players invest heavily in platform enhancements, API management, and real-time, event-driven workflows to maintain leadership and address complex IT integration needs.

The market shows fragmented characteristics in mid-market and specialised sectors, where agile vendors like Workato, SnapLogic, TIBCO Software, Jitterbit, and Zapier compete on usability, flexible pricing, and niche-focused connectors. This dual dynamic of consolidation at the top and fragmentation in niche areas ensures continuous innovation and competitive pressure. Overall, the iPaaS market balances strong dominance by major global leaders with opportunities for smaller, specialised providers to thrive, driving ongoing advancements in integration technology.

Key Industry Developments:

- February 26, 2025 – F5 unveiled significant cybersecurity enhancements to its Application Delivery and Security Platform (ADSP), including expanded API discovery tools and LLM vulnerability scanning. These updates help organisations strengthen security and reduce complexity in AI-driven hybrid multicloud environments, addressing the growing threats from AI applications and API sprawl.

- March 12, 2025 – Radware introduced next-gen Application Delivery Controllers (ADCs) designed for the multi-cloud era. These modern ADCs offer seamless integration across platforms like AWS, Azure, and GCP, with features such as dynamic capacity allocation through Global Elastic Licensing, AI-driven threat intelligence, and real-time performance monitoring. The solution also enhances security, privacy, and access management, ensuring businesses stay ahead of disruptions and cyber threats.

Companies Covered in Application Delivery Controller Market

- F5 Networks

- A10 Networks

- Citrix Systems

- Radware

- Array Networks

- Kemp Technologies

- Fortinet, Inc.

- Cisco Systems

- Barracuda Networks

- ZEVENET (now rebranded/forked projects)

Frequently Asked Questions

The global Application Delivery Controller market is projected to be valued at US$ 4.1 Bn in 2026.

The Banking, Financial Services & Insurance (BFSI) segment is expected to account for approximately 26.0% of the global Application Delivery Controller market by Use Industry in 2026.

The market is expected to witness a CAGR of 9.2% from 2026 to 2033.

The Global Application Delivery Controller market growth is driven by enterprise digital transformation and multi-cloud adoption, coupled with rapid API proliferation and AI-enabled application complexity that require secure, intelligent, and scalable application traffic management.

Key opportunities in the global Application Delivery Controller market stem from MSP-led ADC-as-a-Service adoption that lowers cost and complexity for mid-market users, alongside AI-driven security and intelligent traffic orchestration enabling autonomous threat detection, performance optimization, and premium AI-native application delivery.