- Aerospace & Defense

- Air Transport Modification Market

Air Transport Modification Market Size, Share, and Growth Forecast, 2026 - 2033

Air Transport Modifications Market by Aircraft Type (Commercial Aircraft, Cargo Aircraft, Military Aircraft, Private Jets, Others), Service Model (Retrofit Services, Maintenance Services, Consulting Services, Full-Service Modification, Others), Modification Type (Cabin Modification, Aerodynamic Modification, Avionics Upgrade, Structural Modification, Engine Enhancement, Others), Modification Purpose and Regional Analysis for 2026 - 2033

Air Transport Modifications Market Size and Trends Analysis

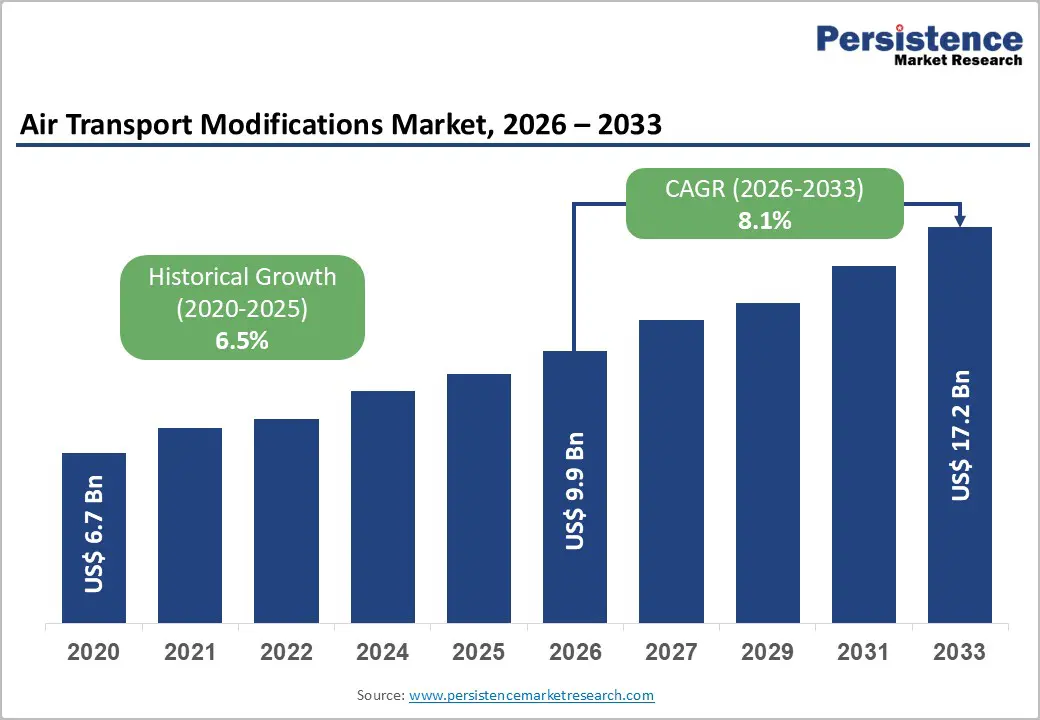

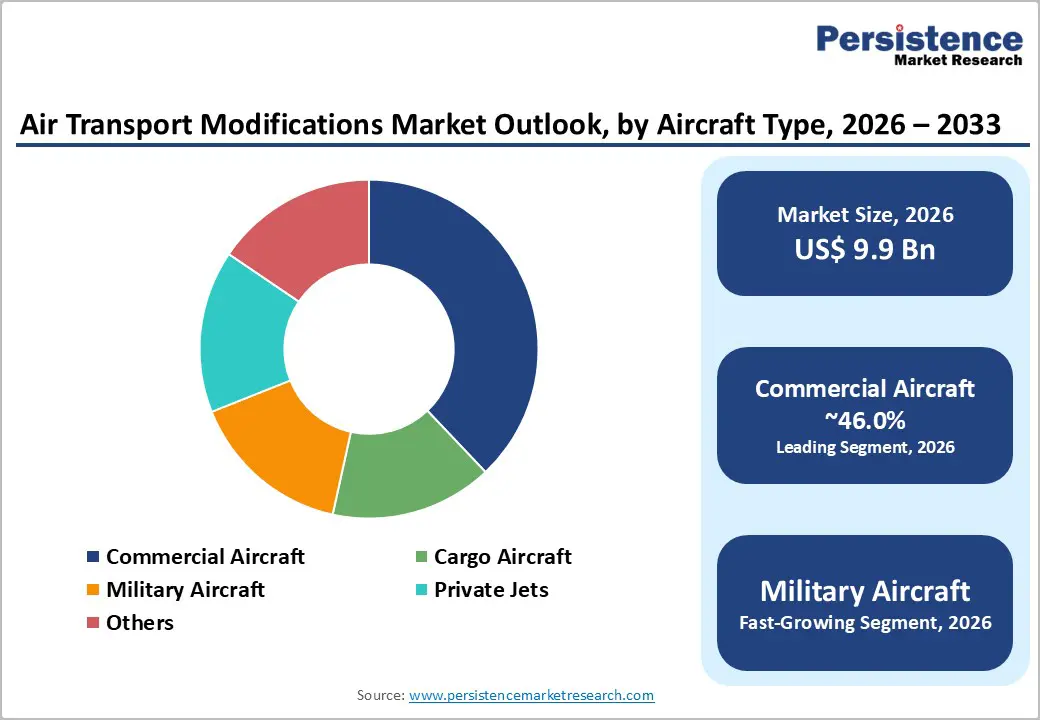

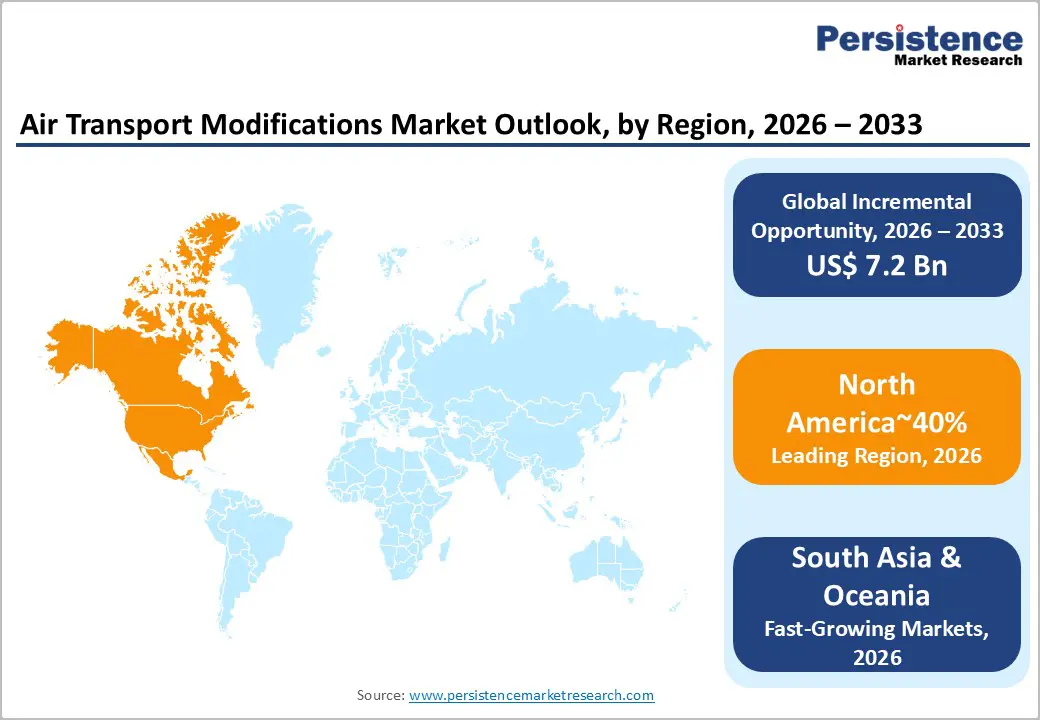

The global air transport modifications market size is likely to be valued at US$ 9.9 billion in 2026 and is projected to reach US$ 17.2 billion by 2033, growing at a CAGR of 8.1% during the forecast period.

The market growth is driven by the global aviation industry's commitment to environmental sustainability through fuel-efficiency upgrades and emissions reduction compliance, ageing commercial aircraft fleet demographics necessitating modernisation and lifecycle extension, and rise in defense spending focused on military aircraft modernisation and avionics system upgrades.

Airlines and defence operators are increasingly prioritising modification services over new aircraft acquisitions due to capital constraints and operational risk mitigation. The market's 8.1% forecast CAGR substantially exceeds the historical 6.5% rate, reflecting strengthening demand for retrofit technologies and consulting services as operators navigate regulatory mandates and technological innovation cycles.

Key Industry Highlights:

- Leading Region: North America commands 40% market share, driven by the largest commercial aircraft fleet, mature MRO infrastructure, and sustained military aircraft modification programs.

- High-Growth Region: East Asia is the fastest-growing market, fueled by fleet expansion, government-backed MRO investments, and rising demand for cabin, avionics, and SAF-compatible retrofits.

- Dominant Aircraft Segment: Commercial aircraft modifications hold 46% market share, led by narrow-body and wide-body retrofit programs focused on cabin upgrades, avionics modernisation, and fuel efficiency improvements.

- Fastest-Growing Aircraft Segment: Military aircraft modifications are rapidly expanding, driven by geopolitical tensions, defence budget increases, and advanced avionics, propulsion, and structural upgrades.

- Largest Service Segment: Retrofit services represent 48% share, encompassing cabin refurbishments, avionics upgrades, and aerodynamic enhancements that extend aircraft life and improve operational efficiency.

| Key Insights | Details |

|---|---|

|

Air Transport Modifications Market Size (2026E) |

US$ 9.9 Bn |

|

Market Value Forecast (2033F) |

US$ 17.2 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.5% |

Market Dynamics

Drivers - Environmental Compliance and Fuel Efficiency Optimisation

Regulatory frameworks, including the European Union's ReFuelEU Aviation Regulation, the International Civil Aviation Organization's (ICAO) Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA), and regional emissions standards, are fundamentally reshaping aircraft modification priorities across the Market.

The Refuel EU Aviation Regulation mandates minimum sustainable aviation fuel (SAF) supply thresholds commencing at 2% in 2025 and escalating to 70% by 2050, requiring aircraft system modifications to accommodate alternative fuel compatibility. CORSIA, implemented globally since 2019 and becoming compulsory for all international flights from 2027, creates a binding compliance mechanism whereby airlines must either reduce emissions through aircraft modifications or purchase expensive carbon offset credits.

Aerodynamic retrofit technologies such as winglet installations and riblet film surface modifications, exemplified by EVA Air's partnership with Lufthansa Technik and BASF to deploy AeroSHARK drag-reduction technology across its Boeing 777F fleet, deliver 1-2% fuel consumption reductions with rapid return-on-investment profiles. Current technology retrofitting programs target 20% fuel burn reductions by 2050 position aircraft modification services as economically superior to new aircraft procurement, particularly within the Market, where capital-constrained operators seek lifecycle extension solutions. The European aviation sector's completion of 300 implementation projects by the end of 2024, with nearly €17 billion in cumulative benefits, including over 4 million tonnes of fuel savings, validates retrofit service scalability and financial viability.

Defense Modernization and Geopolitical Tensions

The military aircraft modernisation and retrofit segment of the Air Transport Modifications Market has experienced significant acceleration following Russia's invasion of Ukraine and the intensifying Asia-Pacific geopolitical tensions.

The global military aircraft modernisation market has expanded, with avionics upgrades commanding around 45 percent of modification demand. India's defence manufacturing sector achieved historic production targets of INR1.54 lakh crore in FY 2024-25, with defence capital procurement contracts valued at INR2,09,050 crore signed in FY 2024-25, representing a decisive pivot toward indigenous military aircraft modifications and upgrades.

The United States Air Force's FY 2025 budget allocation of nearly USD 20 billion for legacy aircraft fleet modification and sustainment demonstrates a sustained commitment to extending operational life through comprehensive avionics, propulsion, and structural upgrades rather than replacement procurement.

Poland's agreement with the U.S. government and Lockheed Martin in August 2025 to modernise 48 F-16 Block 52 plus aircraft to F-16 Viper configuration, integrating advanced avionics, radar systems, mission computers, and structural enhancements, exemplifies large-scale military modification activity within the Air Transport Modifications Market. NATO's commitment to increased defence expenditures and European defence industrial corridor investments in Uttar Pradesh and Tamil Nadu, India, collectively exceeding INR75,000 crore, underscores the magnitude of military modification activity driving sustained market expansion.

Restraint - Capital Investment and Supply Chain Complexity

Aircraft modification projects require substantial upfront capital investments and extended certification timelines, creating barriers to entry and restricting modification frequency. Narrow-body aircraft cabin refurbishment programs typically demand USD 2-5 million per aircraft, while wide-body avionics and structural modifications escalate to USD 8-15 million per unit, creating financial constraints for regional and low-cost carriers.

Global supply chain disruptions affecting aerospace components, including persistent shortages of serviceable used engine parts and avionics components, extend modification project timelines by 6-12 months and inflate procurement costs by 15-25%, eroding the economic viability of retrofit investments within the Air Transport Modifications Market. The semiconductor shortage's cascading effects on avionics system production have created backlogs extending into 2026, limiting modification service provider capacity and creating scheduling constraints that delay project execution.

Opportunity - Emerging Markets and Regional Fleet Expansion

The Asia-Pacific aviation sector is projected to achieve global leadership in passenger traffic within 15 years, with fleet expansion at approximately 4% annually, exceeding the global average of 3% and aircraft in service expected to exceed 6,000 units. India's civil aviation sector, supported by government initiatives including the Vande Bharat Mission and Regional Connectivity Scheme (RCS), has accelerated fleet growth among domestic carriers, creating substantial modification demand within the Market for cabin upgrades, avionics modernisation, and SAF compatibility retrofits.

The Asia-Pacific Aircraft MRO market is expected to grow, with modifications representing the fastest growing segment within the regional Air Transport Modifications Market activity. Emerging market operators, particularly in ASEAN nations and South Asia, increasingly lack access to modern modifications at competitive pricing, creating opportunities for regional modification providers and technology transfer partnerships. Government-backed MRO facility investments, including the Tata Advanced Systems–Lockheed Martin joint venture for C-130J Super Hercules aircraft maintenance and modification in India, announced in December 2025, demonstrate recognition of regional modification market potential and establishment of sustainable competitive positioning within the air transport modifications market.

Sustainable Aviation Fuel Integration and Compatibility Upgrades

The rapid scaling of sustainable aviation fuel (SAF) production with IATA confirming sufficient feedstock availability to achieve net-zero emissions by 2050 creates substantial modification service demand within the Market for fuel system compatibility upgrades, engine re-certification, and infrastructure adaptations.

Current certifications enable SAF blending at 10-50% levels depending on feedstock and production methodology, but regulatory pathways toward 100% SAF operations by 2030 necessitate comprehensive fuel system, engine component, and avionics software modifications across global commercial and military fleets. The consulting services segment of the Air Transport Modifications Market, the fastest-growing service category, is experiencing demand expansion driven by operator requirements for SAF compatibility assessments, modification feasibility studies, and regulatory pathway development.

Airlines investing in SAF conversion programs simultaneously engage modification providers for propulsion system upgrades, landing gear inspections, and structural reinforcements mandated by transition protocols, creating bundled service revenue opportunities. Air India's completion of mandatory software upgrades on 323 Airbus A320 family aircraft in November 2025 to address flight control data corruption risks, conducted under DGCA oversight within the Market, demonstrates the magnitude of avionics-focused retrofit activity and validates consulting services demand for regulatory compliance, navigation and implementation oversight.

Category-wise Analysis

Aircraft Type Insights

Commercial aircraft modifications holding share of 46% represent the dominant segment within the Market, driven by fleet size, regulatory compliance imperatives, and competitive pressures on operating economics. The commercial aircraft segment encompasses narrow-body aircraft, which contain around 45% of refurbishment volumes, and wide-body aircraft , with modifications spanning cabin interior upgrades, avionics system modernisation, and propulsion system enhancements.

Airlines have increased retrofitting activity by 12% year-on-year, prioritising modifications that extend aircraft service life, enhance passenger experience, and improve fuel efficiency without capital expenditure associated with new aircraft procurement. Lightweight composite cabin panels and modular seating systems integrated during modification programs reduce aircraft weight by 8-10%, generating 2-3% fuel consumption improvements and yielding payback periods of 3-5 years within the Air Transport Modifications Market.

Air India's USD 400 million fleet retrofit program, commenced in August 2025 with the modification of 26 legacy Boeing 787-8 aircraft, including new cabin interiors, advanced seating systems, and avionics upgrades to current service standards, executed at Boeing's Victorville facility with completion targeted by mid-2027, exemplifies the magnitude and complexity of commercial aircraft modification initiatives within the Market.

Military aircraft modifications have emerged as the fastest-growing segment within the Air Transport Modifications Market, driven by escalating geopolitical tensions, defense budget expansion, and technology integration requirements for next-generation warfare capabilities.

Service Model Insights

Retrofit services represent the largest service category within the Air Transport Modifications Market, encompassing cabin interior refurbishments, avionics system upgrades, and aerodynamic enhancement installations that extend aircraft service life while improving operational efficiency. Retrofit services command 48% market share through their direct correlation with fleet modernisation cycles and regulatory compliance requirements, with commercial airlines executing refurbishment programs at 5–7-year intervals to maintain passenger experience competitiveness and operational standards.

Digital refurbishment solutions integrating 3D modelling, virtual reality simulation, and predictive maintenance analytics have enhanced retrofit service productivity and reduced aircraft downtime by 20-30%, improving customer value proposition and market adoption rates within the Air Transport Modifications Market. Lufthansa Technik's completion of over 100 MRO events for Boeing 787 nacelles since 2014 through global workshop facilities in Hamburg, Shenzhen, and Dubai and subsequent expansion to Airbus A350 and A320neo nacelle services, demonstrates retrofit service scalability and geographic distribution capabilities, driving sustained market expansion within the Air Transport Modifications Market.

Consulting services have emerged as the fastest-growing segment within the Air Transport Modifications Market, driven by operator requirements for regulatory compliance navigation, modification feasibility assessments, SAF compatibility evaluations, and technology integration strategies.

Regional Insights and Trends

North America Market Trend

North America dominates the Air Transport Modifications Market with 40% regional share, driven by the world's largest commercial aircraft fleet over 7,000 aircraft requiring regular maintenance and modifications, robust military aviation segments, and mature modification service infrastructure.

The U.S. aerospace and defence industry generated USD 995 billion in total business activity in 2024, with 914,000 direct employees supported across aeronautics, space, land and sea systems, and cyber domains. Airlines across North America have prioritised cabin retrofit programs averaging USD 2-3 million per narrow-body aircraft and USD 5-8 million per wide-body aircraft, with major carriers including United Airlines, American Airlines, and Southwest Airlines executing fleet-wide cabin modernisation initiatives within the Air Transport Modifications Market.

The United States Air Force's sustained investment in legacy aircraft modifications with FY 2025 budget allocations of USD 20 billion for fleet modification and sustainment ensures continuous demand for avionics upgrades, propulsion system enhancements, and structural modifications within military segments of the Air Transport Modifications Market. Boeing's designation of Lufthansa Technik as a licensed service centre for 787 Dreamliner cabin modifications expands North American modification capacity and validates market growth potential, with Virgin Atlantic's October 2025 Boeing partnership implementing high-speed Wi-Fi connectivity modifications across its 787 Dreamliner fleet, further demonstrating technological innovation and modification service expansion within the Market.

East Asia Air Transport Modifications Market Trend

East Asia contributes 15% to the global Air Transport Modifications Market, with rapid expansion potential driven by unprecedented commercial aviation growth, military modernisation acceleration, and government investments in aerospace manufacturing infrastructure. The Asia-Pacific aviation sector is experiencing unprecedented growth, positioning it as one of the fastest-expanding markets globally, with aircraft fleet expected to grow 4% annually, exceeding global averages and fleet size projected to exceed 6,000 aircraft in service.

Europe Air Transport Modifications Market Trends

Europe represents 25% of the global Air Transport Modifications Market, supported by the region's significant civil aviation recovery, robust defense modernization initiatives, and advanced aerospace technology infrastructure.

The European aerospace and defense industry achieved €325.7 billion in turnover in 2024, with 10.1% year-on-year growth, with civil aeronautics growing 4.7% and defence sectors demonstrating robust expansion reflecting geopolitical security priorities. European airlines have accelerated cabin refurbishment programs to compete in premium leisure and business travel segments, with modifications incorporating premium seating configurations, advanced in-flight entertainment systems, and enhanced cabin connectivity, driving demand within the Air Transport Modifications Market.

European defence budgets demonstrate sustained expansion, with Germany, France, and the United Kingdom collectively investing €50+ billion annually in defense modernization, creating substantial military aircraft modification demand for avionics upgrades, electronic warfare system integration, and structural enhancement programs within the Air Transport Modifications Market. The European defence industry's EUR 183.4 billion turnover in 2024 represented 13.8% year-on-year growth, with military aeronautics achieving 13.6% expansion and supporting 240,000 jobs, validating the scale of defence-sector aircraft modification activity within the Air Transport Modifications Market. Poland's F-16 Viper modernisation agreement and NATO allies' coordinated defence modernisation initiatives ensure sustained modification demand through 2030+ within the European air transport modifications segment.

Competitive Landscape

The global air transport modifications market is fragmented, with both large corporations and specialized players competing in various sectors such as cabin upgrades, avionics enhancements, and MRO services. Major players like Boeing, Airbus, Lockheed Martin, and Lufthansa Technik dominate the high-value modification segments due to their extensive capabilities and global networks. Smaller firms, such as RUAG Aviation and STS Aviation Services, focus on niche areas like cabin refurbishments and specific MRO services.

While the market remains diverse, partnerships and joint ventures, like those between Tata Advanced Systems and Lockheed Martin, suggest a trend toward consolidation in certain segments, particularly in military and high-value commercial modifications. This evolving dynamic reflects a balance between large-scale operators and specialised service providers, ensuring both competition and collaboration.

Key Industry Developments

- In Oct 2024, Air India received Design Organisation Approval (CAR 21) from India’s DGCA, enabling the airline to independently design and implement aircraft interior modifications in-house. Through collaboration with Tata Technologies, this development strengthens Air India’s engineering, digital MRO, and modification capabilities, enhancing safety, operational efficiency, and passenger experience.

- On Nov. 29, 2025 – Airbus: Airbus issued an urgent directive calling for immediate modifications across approximately 6,000 A320-family aircraft after identifying risks of solar radiation corrupting critical flight control data. The majority of affected aircraft are expected to be addressed through software updates, minimising downtime while ensuring flight safety and regulatory compliance. This development highlights the growing importance of avionics and software-level modifications within the Air Transport Modifications market.

- On Aug 23, 2024, EVA Air became the first airline in Asia to equip its entire Boeing 777F freighter fleet with drag-reducing AeroSHARK riblet films developed by Lufthansa Technik and BASF. The modification delivers ~1% fuel and CO2 emission reduction per aircraft, supporting EVA Air’s net-zero 2050 strategy and highlighting aerodynamic retrofit technologies in the Air Transport Modifications market.

Companies Covered in Air Transport Modification Market

- Schneider Electric SE

- ABB Ltd.

- Eaton Corporation plc

- Siemens AG

- Mitsubishi Electric Corporation

- LS Electric Co., Ltd.

- Fuji Electric Co., Ltd.

- Hyundai Electric & Energy Systems Co., Ltd.

- Hager Group

- Rockwell Automation, Inc.

- Terasaki Electric Co., Ltd.

- Chint Group Corporation

- Legrand S.A.

- Toshiba Corporation

Frequently Asked Questions

The Global Air Transport Modifications Market is projected to be valued at US$ 9.9 Bn in 2026.

The Retrofit Services segment is expected to account for approximately 48% of the Global Air Transport Modifications Market by Service Model in 2026.

The air transport modifications market is expected to witness a CAGR of 8.1% from 2026 to 2033.

Air Transport Modifications Market growth is driven by environmental compliance and fuel efficiency optimization through SAF-compatible retrofits and aerodynamic technologies, alongside defense modernization and geopolitical tensions fueling avionics, structural, and propulsion upgrades.

Key opportunities in the Air Transport Modifications Market lie in Asia-Pacific fleet expansion and emerging market demand for cabin, avionics, and SAF-compatible retrofits, alongside growth in consulting and regulatory compliance services for sustainable aviation fuel integration.

Key players in the Air Transport Modifications Market include Boeing, Airbus, Lockheed Martin, and Lufthansa Technik.