- Sensors & Controls

- Air Flow Sensors Market

Air Flow Sensors Market Size, Share, and Growth Forecast, 2026 – 2033

Air Flow Sensors Market by Sensor Type (Mass Air Flow, Volume Air Flow), Output Signal (Variable Voltage, Frequency Output), Sensing Wire Type (Hot Wire, Cold Wire), End-user Industry (Automotive, HVAC, Others), and Regional Analysis 2026 – 2033

Air Flow Sensors Market Size and Trends Analysis

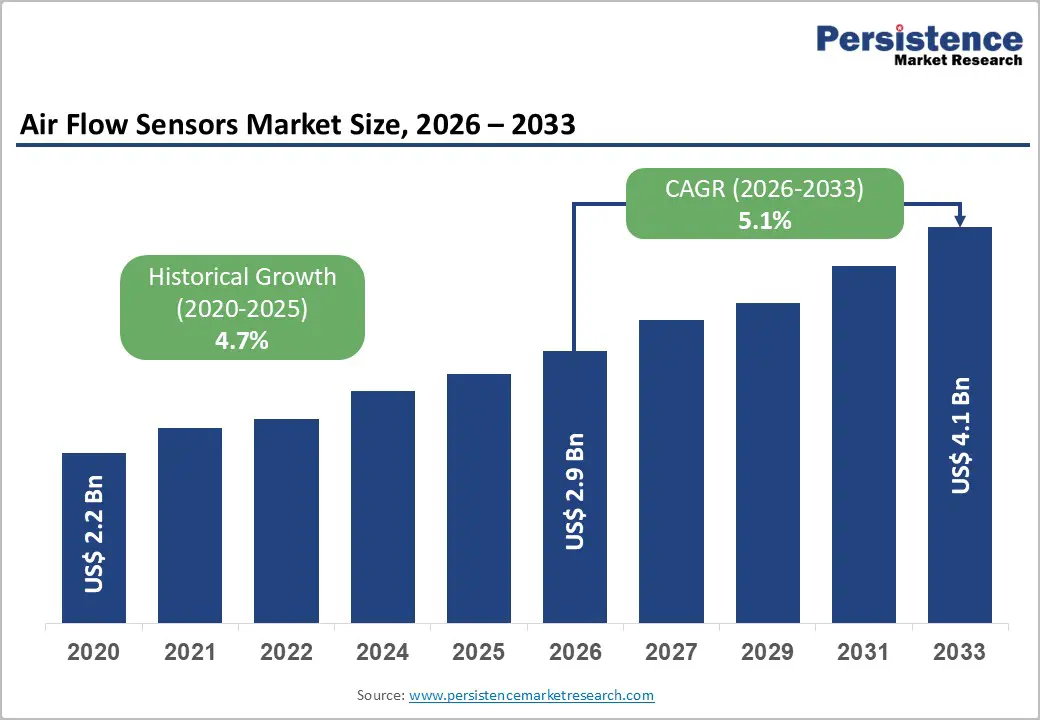

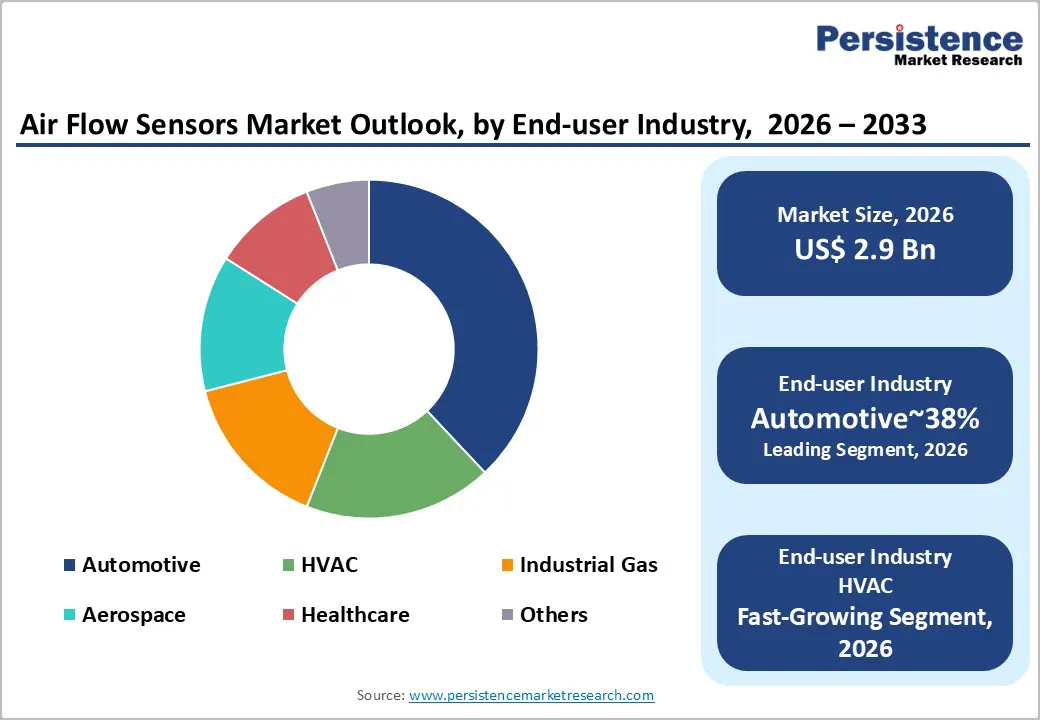

The global air flow sensors market size is likely to be valued at US$2.9 billion in 2026 and is expected to reach US$4.1 billion by 2033, growing at a CAGR of 5.1% during the forecast period from 2026 to 2033, driven by the intensifying demand for fuel-efficient engine management systems and the rapid expansion of smart HVAC infrastructure globally. Growth stems from stringent emission regulations in automotive applications and rising demand for energy-efficient HVAC systems in commercial buildings.

The integration of Micro-Electro-Mechanical Systems (MEMS) technology has also revolutionized sensor accuracy and miniaturization, enabling broader adoption in portable medical devices and high-density data center cooling systems. As industrial automation accelerates, the requirement for real-time, digital air flow data is shifting the market toward frequency-output and IoT-enabled sensing solutions.

Key Industry Highlights:

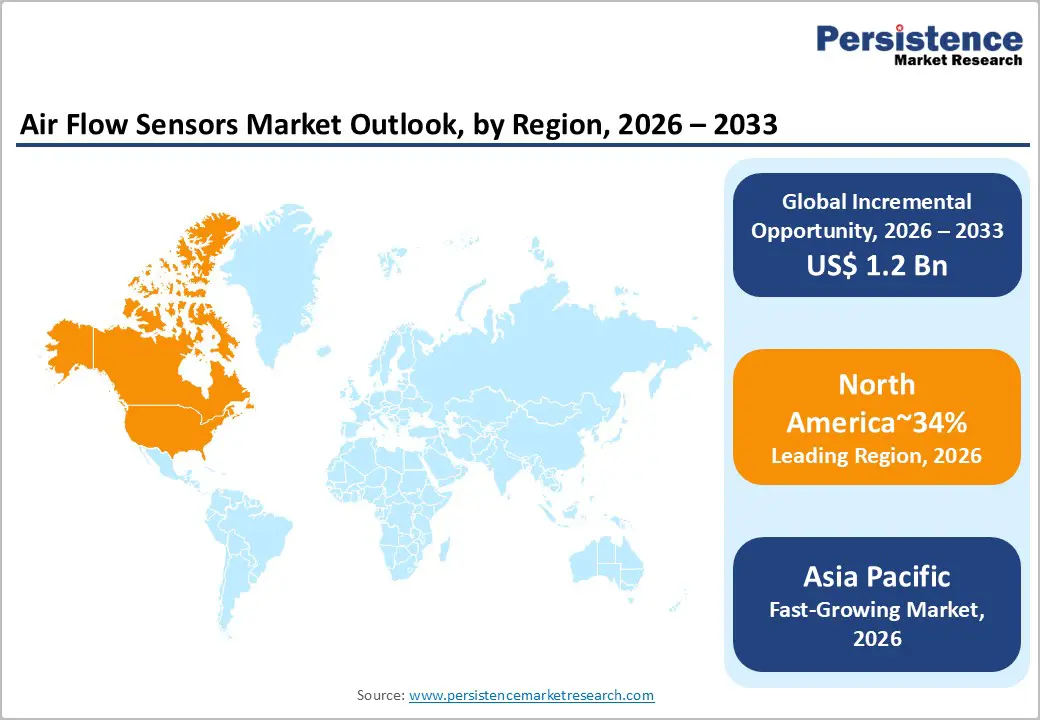

- Leading Region: North America is projected to lead due to strong automotive production, advanced emission control regulations, and early adoption of precision sensing technologies, accounting for approximately 34% share.

- Fastest-Growing Region: Asia Pacific is anticipated to grow the fastest due to expanding automotive manufacturing, rapid industrialization, and infrastructure growth in HVAC and data center construction.

- Leading Sensor Air Type Segment: Mass Air Flow (MAF) sensors are projected to dominate, with approximately 74% share, supported by high-precision measurement capabilities and a critical role in fuel-air ratio optimization.

- Leading End-user Industry: The automotive segment is expected to lead, accounting for approximately 38%, driven by widespread integration in internal combustion engine control systems and regulatory-driven emission monitoring requirements.

| Key Insights | Details |

|---|---|

| Air Flow Sensors Market Size (2026E) | US$ 2.9 Bn |

| Market Value Forecast (2033F) | US$ 4.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Technological Shift Toward Industry 4.0 and Industrial IoT Integration

The transition toward industry paradigms and interconnected manufacturing architectures is structurally elevating demand for digitally enabled air flow sensing technologies. Industrial Internet of Things (IIoT) architectures increasingly integrate airflow meters into predictive maintenance ecosystems, enabling continuous performance diagnostics across compressed air distribution networks. Given that compressed air systems account for a material proportion of industrial electricity consumption, operational oversight has intensified around flow inefficiencies, leakage detection, and pressure optimization. Real-time airflow analytics facilitate condition-based maintenance strategies, minimizing unplanned downtime while improving asset utilization across energy-intensive process industries.

Parametric optimization of airflow yields quantifiable energy savings, thereby strengthening the economic rationale for retrofits in mature industrial markets. Regulatory prioritization of industrial energy efficiency across North America and Europe further accelerates adoption within established manufacturing clusters. From a value-chain perspective, procurement patterns are shifting toward network-compatible, digitally calibrated sensing platforms equipped with embedded communication protocols to support system interoperability. This transition reallocates cost structures toward elevated upfront instrumentation expenditure, offset by reductions in lifecycle maintenance costs and aggregate energy consumption.

Rise in HVAC (Heating, Ventilation, and Air Conditioning) and Data Center Demand

Escalating energy intensity across commercial infrastructure is strengthening structural demand for air flow sensors within HVAC architectures. Advanced airflow sensing facilitates adaptive load balancing, strengthens adherence to ventilation standards, and enables interoperability within integrated building automation architectures characteristic of smart infrastructure frameworks. Simultaneously, the accelerated proliferation of hyperscale data centers, largely attributable to artificial intelligence computational demand, has heightened the necessity for precision cooling, thereby institutionalizing sophisticated airflow sensing within contemporary thermal management design protocols.

Compliance-oriented modernization initiatives increasingly incorporate airflow sensors into centralized energy management systems, reinforcing aftermarket demand and expanding service-based revenue models. Across the value chain, procurement dynamics are correspondingly shifting toward high-accuracy, digitally integrated sensing platforms characterized by superior calibration resilience. In parallel, accelerated urbanization across the Asia Pacific region continues to enlarge the installed base of HVAC infrastructure, underpinning sustained structural demand across both building and data infrastructure verticals.

Barrier Analysis – High Sensor Costs and Contamination Sensitivity in Advanced MEMS Platforms

Elevated capital intensity associated with advanced MEMS (Micro-Electro-Mechanical Systems) air flow sensors constrains broader market penetration in cost-sensitive segments. Manufacturing processes necessitate advanced semiconductor fabrication, precision micro-structuring, and sustained research and development investment, thereby elevating unit cost structures relative to conventional volumetric airflow meters. For small and medium-sized enterprises in emerging markets, capital allocation is typically constrained by short-term return-on-investment thresholds. Consequently, procurement decisions remain closely tied to immediate operational payback, moderating replacement cycles within entry-level consumer appliances and cost-sensitive industrial equipment segments.

In addition to capital expenditure considerations, MEMS-based architectures demonstrate increased susceptibility to particulate contamination and environmental variability. Exposure to dust, moisture ingress, or chemical residues can impair calibration stability and measurement integrity, amplifying maintenance intensity in harsh operating conditions. These reliability risks introduce lifecycle cost volatility, particularly for value-oriented buyers who prioritize durability and robustness over incremental precision enhancements. Across the value chain, manufacturers must therefore reconcile the advantages of miniaturization with investments in protective housing, integrated filtration mechanisms, and disciplined cost-containment frameworks to sustain competitive positioning.

Performance Degradation and Maintenance Burden in Harsh Operating Environments

Air flow sensors, particularly hot wire architectures, exhibit vulnerability to particulate contamination and fluid ingress in demanding environments. Exposure to dust, oil vapor, and moisture induces calibration drift, progressively impairing measurement fidelity and control stability. Within heavy industrial environments and off-road automotive applications, operating conditions materially increase exposure to fouling, particulate accumulation, and thermal stress. Sustained measurement accuracy under such conditions necessitates structured maintenance protocols, including periodic cleaning, recalibration cycles, and integration of protective filtration across system assemblies.

Heightened maintenance requirements elevate operating expenditure and introduce variability into lifecycle cost projections for end users. In industrial jurisdictions characterized by limited regulatory enforcement, weaker compliance incentives diminish investment in preventive maintenance regimes. Documented efficiency losses ranging between five and eight percent underscore the systemic impact of unmanaged sensor degradation. These structural constraints moderate large-scale deployment, as reliability risk and incremental service overhead become embedded within capital procurement and total-cost-of-ownership evaluations.

Opportunity Analysis – Expansion Across Electric Vehicle and Healthcare System Architectures

The rapid electrification of mobility platforms is expanding functional demand for precision air flow sensing technologies within electric vehicle architectures. Thermal management systems governing battery packs, inverters, and cabin climate modules require accurate airflow modulation to maintain performance stability and regulatory safety compliance. Accelerated electrification across mobility platforms is materially increasing functional demand for high-precision airflow sensing technologies within electric vehicle system architectures. Thermal management assemblies regulating battery modules, power inverters, and cabin climate control systems require tightly controlled airflow modulation to preserve performance stability and ensure adherence to safety regulations. As power electronics density intensifies, airflow optimization becomes central to heat dissipation engineering, thereby embedding sensing technologies within critical vehicle subsystems.

Parallel expansion within healthcare infrastructure is strengthening adoption across respiratory devices, anesthesia delivery systems, and diagnostic equipment. Clinical airflow monitoring imposes rigorous requirements for measurement accuracy, sterility compatibility, and regulatory certification under medical device governance frameworks. Growing deployment of portable ventilation systems and home-based healthcare equipment further decentralizes demand, increasing reliance on miniaturized, high-reliability sensing platforms. Across the value chain, these end markets elevate margins toward specialized, compliance-intensive products characterized by extended validation timelines and stringent quality assurance protocols.

Intensified Data Center Thermal Management Requirements

The acceleration of artificial intelligence and cloud computing workloads is reshaping thermal management architectures within high-density data centers. Escalating server power densities elevate heat flux concentrations, increasing reliance on precision airflow monitoring for stable operating conditions. Increasing server power densities intensifies localized heat flux, thereby heightening dependence on precision airflow monitoring to maintain operational stability. Rack-level airflow optimization facilitates dynamic workload distribution, targeted cooling deployment, and improved power usage effectiveness (PUE) across hyperscale facilities.

As operators prioritize energy efficiency and uptime assurance, sensing technologies become embedded within core infrastructure design standards. This evolution reallocates procurement toward high accuracy, network-compatible sensors capable of operating within tightly controlled thermal envelopes. Airflow sensors embedded within containment architectures and intelligent building management systems enhance granular environmental visibility across server corridors. Real-time airflow analytics enable adaptive fan modulation, coordinated liquid cooling integration, and predictive maintenance protocols in mission-critical settings. As data center operators prioritize energy efficiency and uptime resilience, airflow sensing technologies are increasingly codified within core infrastructure design specifications.

Category–wise Analysis

Sensor Air Type Insights

The Mass Air Flow (MAF) segment is expected to dominate, accounting for approximately 74% share in 2026, supported by its superior ability to measure actual air mass independent of density and temperature variations. This measurement precision, typically within narrow tolerance bands, is fundamental for modern internal combustion engine control units that require accurate stoichiometric calibration and combustion optimization. Automotive applications, which constitute a major end-use segment, rely on mass airflow (MAF) sensor integration to optimize fuel efficiency, emissions management, and adaptive engine calibration under variable load conditions. Established suppliers, including Robert Bosch GmbH, DENSO Corporation, and Continental AG, embed sophisticated MAF platforms within engine management systems, reinforcing installed base advantages and long-term OEM qualification cycles. This entrenched integration across powertrain architectures underpins sustained segment dominance in automotive deployment models.

MAF is expected to be the fastest-growing segment, propelled by tightening emission frameworks such as Euro 7 and China 6b that require real-time air mass monitoring for catalytic efficiency optimization. Relative to pressure-based volumetric airflow sensors, MAF technologies exhibit superior responsiveness under variable air density conditions, complementing trends in engine downsizing and turbocharging. Suppliers are further enhancing MAF platforms through advanced signal processing, temperature compensation, and digital communication protocols to support next-generation powertrain architectures. Collectively, these performance characteristics position MAF sensors to outperform legacy airflow technologies as global regulatory stringency and engine system complexity continue to escalate.

End-user Industry Insights

The automotive segment is expected to lead, accounting for approximately 38% share in 2026, driven by the structural role of sensors within engine control units across passenger and light commercial vehicles. High production volumes and the integration of mass air flow sensors for precise air-fuel ratio management reinforce its entrenched position in powertrain architectures. High production volumes, combined with the deployment of MAF sensors for precise air–fuel ratio regulation, reinforce the segment’s entrenched role in powertrain architectures. Adoption is underpinned by real-time measurement accuracy, resilience to thermal and vibrational stresses, and compatibility with advanced ECU calibration protocols. Leading suppliers, including Robert Bosch GmbH, DENSO Corporation, and Continental AG, offer sensor platforms that integrate seamlessly within OEM manufacturing workflows.

HVAC and data centers are expected to be the fastest-growing segment, fueled by rising demand for energy efficiency and thermal management optimization in commercial infrastructure. Growth is catalyzed by smart building initiatives, Expansion is supported by smart building initiatives, widespread adoption of Variable Air Volume (VAV) systems, and the proliferation of high-performance computing facilities, where precise airflow control directly affects cooling efficiency. Integration of AI-enabled monitoring, digital control platforms, and predictive optimization tools enhances operational performance while mitigating carbon intensity. As adoption continues to mature, HVAC and data center applications are expected to outpace overall market expansion.

Regional Insights

North America Air Flow Sensors Market Trends

North America is expected to remain the leading market, accounting for approximately 34% of global revenue in 2026, supported by deep enterprise penetration, mature innovation ecosystems, and high-specification adoption across aerospace, automotive, and commercial building sectors. The presence of major industrial and aerospace players drives sustained integration of precision airflow sensors in turbine, cabin pressure, and engine management systems, reinforcing structural demand. Advanced MEMS fabrication and sensor miniaturization are increasingly localized within domestic semiconductor supply chains, while regulatory energy-efficiency mandates and electrification initiatives are accelerating deployment across commercial HVAC systems and vehicle thermal management platforms.

The U.S. anchors North America’s market positioning, driving regional momentum through regulatory enforcement, industrial scale, and concentrated investment. Federal energy efficiency initiatives and EPA Tier 3 emission standards are expected to stimulate adoption of high-precision sensors across automotive and building applications, while CARB Low NOx compliance further amplifies demand for catalytic monitoring solutions. Large-scale deployments by technology and automotive firms reinforce predictive airflow control adoption, ensuring North America’s structural dominance, while ongoing technology evolution, regulatory alignment, and industrial investments continue to expand deployment intensity across the region.

Europe Air Flow Sensors Market Trends

Europe is expected to remain a structurally important air flow sensor market, supported by regulatory harmonization, mature industrial ecosystems, and sustainability-driven adoption across automotive and commercial building sectors. Germany and France anchor advanced sensor utilization, particularly within engine management and smart HVAC deployments, while the European Green Deal accelerates retrofits requiring precision airflow monitoring. A consolidated vendor presence, led by Bosch and DENSO, supports platform standardization, high-quality manufacturing, and ISO 14001-compliant Industrie 4.0 production processes. Investment in sensor R&D and domestic fabrication capacity further strengthens structural demand, while industrial digitization and automation reinforce replacement cycles and high-volume integration.

Germany anchors Europe’s regional momentum, shaping market trajectory through advanced automotive production, smart building initiatives, and centralized R&D investments. Euro 7 emission mandates drive the adoption of high-precision MAF sensors to achieve NOx reduction targets, while energy-efficient HVAC retrofits integrate IoT-enabled airflow monitoring. Vendor strategies increasingly emphasize MEMS fabrication, digital connectivity, and factory-level automation to capture industrial scaling advantages. As policy alignment, industrial capability, and platform innovation converge, Germany is projected to sustain leadership influence, supporting Europe’s stable yet forward-looking market position within the global air flow sensor ecosystem.

Asia Pacific Air Flow Sensors Market Trends

Asia Pacific is expected to register the fastest growth trajectory, as industrialization, automotive expansion, and EV adoption accelerate technology deployment across the region. China and Japan lead in automotive production, while India and ASEAN countries are scaling industrial and commercial infrastructure, creating structural demand for high-precision sensors. Policy incentives targeting electric vehicle components and advanced manufacturing further catalyze adoption, while low-cost fabrication capacity supports regional supply chain competitiveness. Consolidated vendor presence, including DENSO and Hitachi, enables platform standardization and rapid scaling of MEMS-based sensor solutions. Technological integration within smart HVAC, industrial ventilation, and EV thermal management is expected to reinforce replacement cycles and operational efficiency, sustaining high-volume deployment momentum across Asia Pacific.

China anchors regional momentum, shaping Asia Pacific’s trajectory through regulatory mandates, industrial modernization, and domestic manufacturing depth. The “Dual Carbon” policy and China VI emission standards drive extensive adoption of MAF and industrial airflow sensors across automotive and factory operations, particularly in high-density production zones. Large-scale industrial clusters and EV manufacturing hubs, such as BYD’s facilities in India and China, integrate advanced sensors for thermal and airflow efficiency gains, reinforcing regional adoption patterns. As policy alignment, industrial capacity, and technology sophistication converge, China is expected to sustain its role as the principal growth engine for Asia Pacific’s air flow sensor ecosystem.

Competitive Landscape

The global airflow sensor market exhibits a moderately consolidated structure, with the top five suppliers accounting for an estimated 45–50% of total revenue. High entry barriers in automotive and aerospace applications, particularly the requirement for IATF 16949 certification, reinforce the competitive advantage of established Tier-1 suppliers, sustaining their dominant market positions. In contrast, the industrial and HVAC segments remain comparatively fragmented, providing opportunities for niche providers to compete through specialized sensor technologies, including ultrasonic and thermal dispersion solutions.

Regional supply networks and strategic OEM partnerships reinforce their structural footprint, ensuring that new product introductions and standardization initiatives propagate rapidly throughout the market while maintaining compatibility with evolving regulatory and energy-efficiency requirements. Industry behavior demonstrates gradual consolidation, sustained platform evolution, and ecosystem embedding, with digital transformation initiatives and predictive maintenance adoption accelerating demand for integrated solutions.

Key Industry Developments:

- In January 2026, Airflow Sciences Corporation received US$1.15 million from the U.S. Department of Energy to develop a specialized vapor-liquid flow meter for geothermal wells. This development expanded the company's footprint into the renewable energy sector and introduced high-precision monitoring for unconventional geothermal systems.

- In January 2026, Sensirion AG announced the development of the SCD53, a highly intrinsically stable CO2 sensor designed for long-term accuracy without manual recalibration. It addressed the critical industry challenge of sensor drift in demanding environments, reducing maintenance costs for indoor air quality and industrial systems.

- In December 2025, Posifa Technologies introduced new models in its PLF2000 Series of ultra-low-flow liquid flow sensors, expanding calibrated ranges to support up to 200 mL/min. These new variants improved precision and linearity for demanding microfluidic, medical, and life science applications, helping engineers prevent dosing overshoot and reduce reagent waste.

Companies Covered in Air Flow Sensors Market

- Robert Bosch GmbH

- DENSO Corporation

- Honeywell International Inc.

- Sensirion AG

- TE Connectivity

- Siemens AG

- Hitachi Automotive Systems

- Sensata Technologies

- Analog Devices Inc.

- SMC Corporation

- Delphi Technologies

- Mitsubishi Electric

- ABB Ltd

- First Sensor AG

- Degree Controls Inc.

Frequently Asked Questions

The global air flow sensors market is projected to be valued at US$2.9 billion in 2026 and is expected to reach US$4.1 billion by 2033, driven by adoption across automotive internal combustion engine systems, smart HVAC infrastructure, and high-density data center cooling applications.

MEMS technology enhances measurement precision, miniaturization, and digital output capabilities, enabling broader deployment across automotive engines, industrial HVAC systems, portable medical devices, and IoT-enabled thermal management solutions. Enhanced accuracy supports regulatory compliance, energy optimization, and predictive maintenance, making MEMS adoption a structural growth factor across multiple end-user segments.

The air flow sensors market is forecast to grow at a CAGR of 5.1% from 2026 to 2033, reflecting structural demand from automotive emissions monitoring, industrial automation, and precision cooling requirements in commercial infrastructure and data centers.

Asia Pacific is the fastest-growing regional market, anchored by China’s industrial modernization, Japan’s automotive production, and India’s infrastructure expansion. Policy incentives for electric vehicle components, regulatory emissions standards, and low-cost MEMS fabrication capacity are expected to accelerate adoption across automotive, HVAC, and industrial sensor applications.

The air flow sensors market is moderately consolidated, with leading suppliers including Robert Bosch GmbH, DENSO Corporation, Honeywell International Inc., Sensirion AG, TE Connectivity, Siemens AG, Hitachi Automotive Systems, Sensata Technologies, Analog Devices Inc., SMC Corporation, Delphi Technologies, Mitsubishi Electric, ABB Ltd, First Sensor AG, Degree Controls Inc., and Continental AG. These players compete through high-accuracy platforms, regulatory-aligned solutions, system integration, and global OEM partnerships.