- Retail

- AI Laptop Market

AI Laptop Market Size, Share, and Growth Forecast, 2025 - 2032

AI Laptop Market By Processor Architecture (x86-Based Processors, ARM-Based Processors, Others), Use Case (Productivity & Business Intelligence, Content Generation, Others), Operating System (Windows, macOS, Linux, Chrome OS, Others), and Regional Analysis for 2025 - 2032

AI Laptop Market Share and Trends Analysis

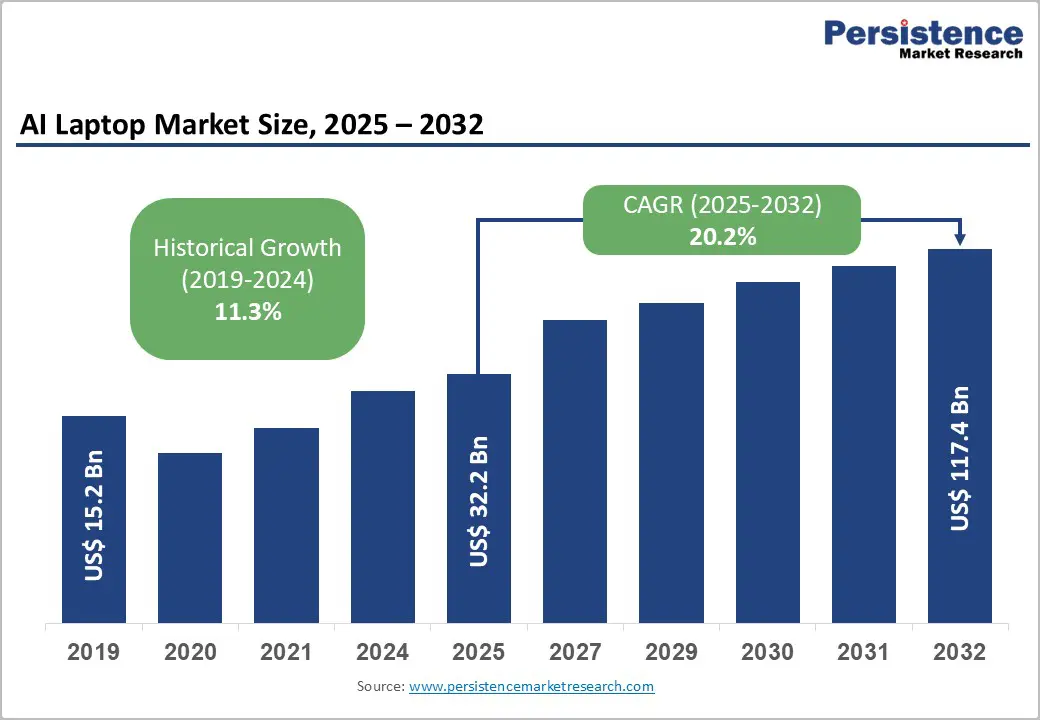

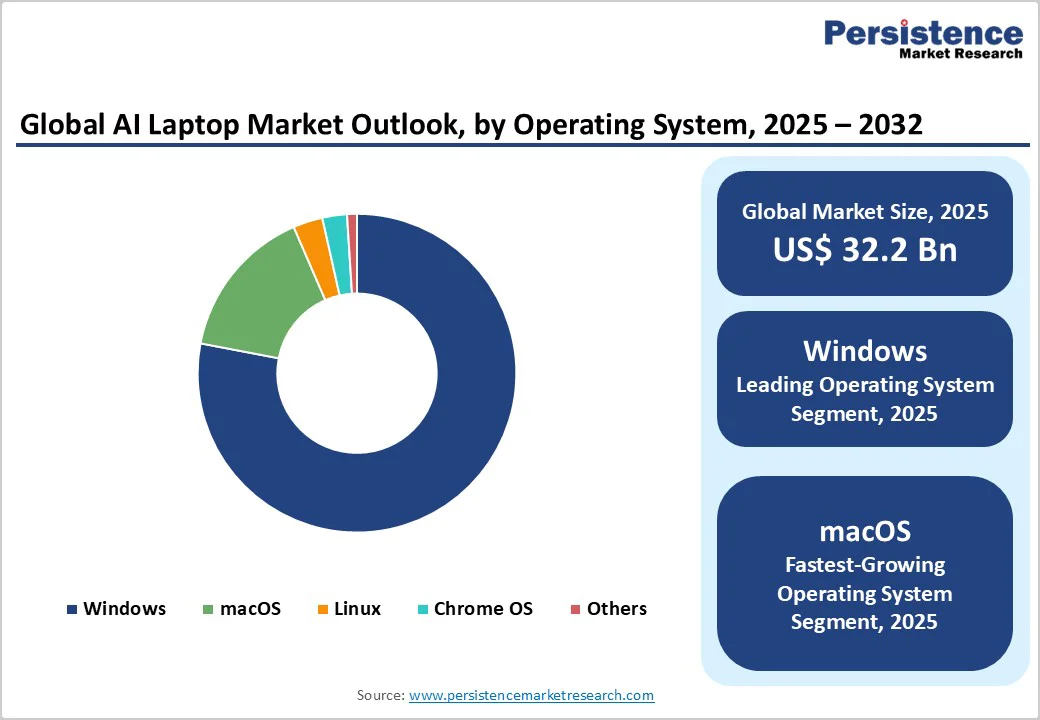

The global AI laptop market is expected to reach US$32.2 billion in 2025. It is estimated to reach US$117.4 billion by 2032, growing at a CAGR of 20.2% during the forecast period from 2025 to 2032, driven by the convergence of enterprise digital transformation imperatives, advancement in neural processing architectures, and the proliferation of hybrid work models that demand intelligent, on-device computing capabilities.

Market growth is being fueled by Microsoft’s Copilot+ PC certification baseline of 40 TOPS NPUs, chipmakers’ shift toward AI-first architectures across Intel, AMD, and Qualcomm, and rising enterprise adoption of on-device AI to meet data sovereignty, latency, and GDPR compliance requirements.

Key Industry Highlights

- Dominant Processor Architectures: Intel and AMD’s x86 processors hold 87% revenue share in 2025, while Qualcomm’s ARM-based Snapdragon chips are the fastest-growing, due to power efficiency and early 40+ TOPS achievement.

- Leading Use Cases: Productivity and business intelligence lead use cases with about 60% in 2025, with development and research growing the fastest through 2032.

- Operating System Dominance: Windows OS dominates 78% of AI laptops in 2025, boosted by Copilot+ certification and enterprise software support.

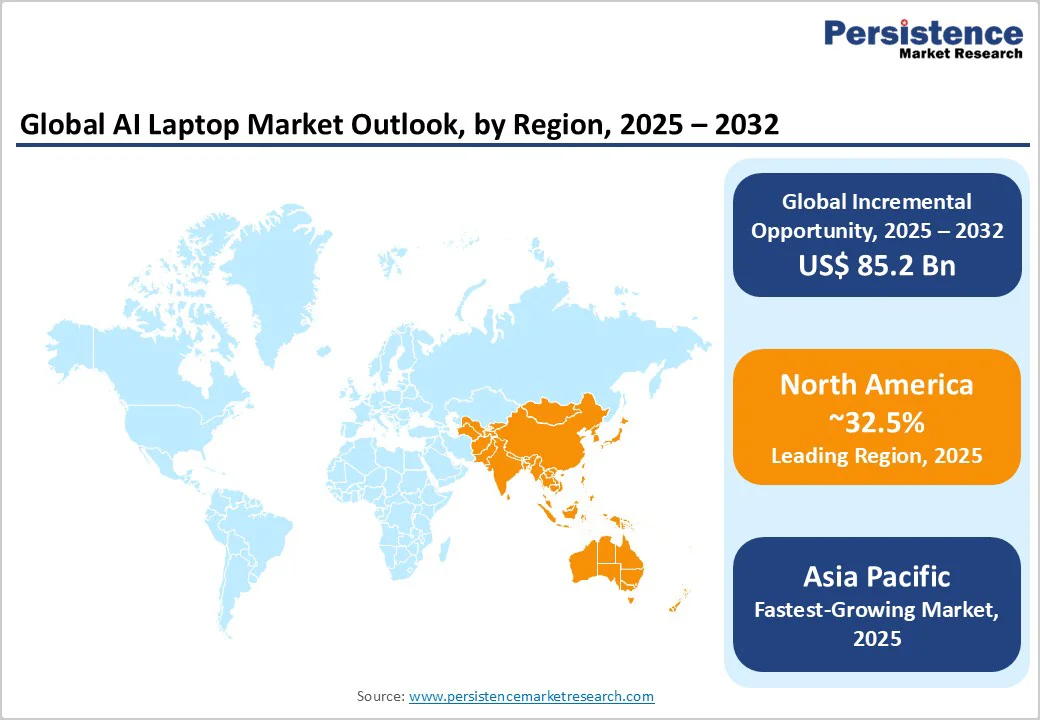

- Leading Region: North America leads with 32.5% market share in 2025, where the Asia Pacific market is set to grow the fastest at an estimated 24% CAGR through 2032, fueled by China and India’s digital initiatives and manufacturing strength.

- Market Structure: The top five vendors - Lenovo, HP, Dell, Apple, and ASUS - control about 70% market share in 2025.

- Key Driver: Growing acceptance of hybrid work models is driving the demand for AI laptops with smart power and collaboration features.

- April 2025: ASUS launched its AI-powered ExpertBook P series, targeting India’s growing SME sector with enterprise-grade performance, durability, and AI optimization powered by Intel Core Ultra processors.

| Key Insights | Details |

|---|---|

| AI Laptop Market Size (2025E) | US$32.2 Bn |

| Market Value Forecast (2032F) | US$117.4 Bn |

| Projected Growth (CAGR 2025 to 2032) | 20.2% |

| Historical Market Growth (CAGR 2019 to 2024) | 11.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Hybrid Work Model Institutionalization and Enterprise Productivity Mandate

The structural transformation of work arrangements following the global pandemic has evolved from temporary adaptation into a permanent organizational strategy, fundamentally reshaping enterprise technology procurement priorities and creating sustained demand for AI-enhanced mobile computing infrastructure.

According to Gallup's 2025 workforce analysis, 52% of U.S. employees who can work remotely are currently operating in hybrid arrangements, indicating that the five-day office model has been permanently displaced for knowledge workers. This distribution pattern is being reinforced by generational preferences, with Generation Z and Millennial employees actively seeking alternative employment if mandated to return to full-time office attendance.

The hybrid work paradigm is driving specific technical requirements for AI laptops that distinguish them from conventional mobile computing devices, particularly regarding intelligent battery management, adaptive performance optimization, and seamless connectivity across diverse network environments.

For AI laptop manufacturers and enterprise technology providers, this represents a lucrative growth driver with a multi-year recurring revenue stream. Organizations are systematically upgrading endpoint infrastructure to support distributed workforces that require advanced AI-powered videoconferencing capabilities.

Fragmented NPU Performance Standards and Software Ecosystem Compatibility Challenges

The AI laptop market's growth is constrained by the lack of universally accepted performance benchmarking standards for neural processing units and the resulting fragmentation of the software ecosystem, which complicates enterprise deployment decisions and constrains mainstream adoption velocity.

While Microsoft has established the Copilot+ PC certification baseline at 40 TOPS (trillion operations per second) of NPU performance with a minimum of 16GB RAM, the actual implementations vary dramatically across processor vendors, creating substantial compatibility and performance-prediction challenges for enterprise IT procurement teams and software developers optimizing applications for AI acceleration.

This fragmentation creates substantial friction in enterprise adoption cycles, as IT departments must conduct extensive compatibility testing across diverse application portfolios before committing to specific processor architectures, delaying procurement decisions and constraining market expansion velocity.

The challenge is particularly acute in regulated industries, including financial services, healthcare, and manufacturing, where legacy specialized software represents a significant capital investment and presents difficulties for workflow integration.

Regulatory Compliance and Data Sovereignty Requirements in Highly Regulated Sectors

The convergence of increasingly stringent data privacy regulations, AI governance frameworks, and sector-specific compliance mandates is creating an attractive yet untapped opportunity for companies engineering AI laptops optimized for on-device processing in highly regulated industries where data sovereignty and real-time compliance monitoring are critical operational requirements.

The EU GDPR establishes comprehensive requirements for lawfulness, fairness, transparency, purpose limitation, data minimization, accuracy, storage limitation, integrity, confidentiality, and accountability in the processing of personal data. Sector-specific regulations, such as the anti-money laundering (AML) requirements in the BFSI sector, have led to layered compliance frameworks that demand sophisticated technical solutions.

On-device AI processing capabilities embedded in modern AI laptops address these regulatory challenges through architectural advantages that cloud-based AI systems cannot replicate.

By executing machine learning (ML) inference, natural language processing (NLP), document classification, and predictive analytics operations locally on the NPU without transmitting sensitive data to external servers, organizations can implement Privacy by Design and Privacy by Default principles mandated under GDPR Article 25.

Category-wise Analysis

Processor Architecture Insights

Intel and AMD’s x86-based designs currently lead with a commanding 87% market revenue share in 2025, as enterprises prioritize compatibility with existing software ecosystems and IT infrastructure. Intel's position has been reinforced through strategic partnerships with original equipment manufacturers (OEMs) such as Dell, Lenovo, HP, and Acer.

Intel's Core Ultra series, incorporating Meteor Lake and Lunar Lake architectures, delivers integrated AI acceleration with 48 TOPS combined CPU-GPU-NPU performance, positioning the company to maintain an estimated 45-48% share of the AI laptop processor market in 2025. However, this represents moderate share erosion from traditional laptop dominance as ARM-based alternatives gain traction.

The fastest-growing segment between 2025 and 2032 is slated to be ARM-based designs, led predominantly by Qualcomm's Snapdragon X Elite and X Plus platforms.

Their exceptional growth is being driven by Qualcomm's first-mover advantage in achieving 45 TOPS NPU performance ahead of Intel and AMD's comparable offerings, superior power efficiency enabling all-day battery life exceeding 20 hours in typical productivity workloads, and a strategic partnership with Microsoft for Copilot+ PC certification, ensuring software optimization and marketing support.

Use Case Insights

In 2025, the productivity & business intelligence use case remains the leading segment, accounting for approximately 60% of AI laptop market revenue. These devices are integral to digital transformation initiatives across industries such as finance, healthcare, and manufacturing, where AI-powered analytics, automation, and intelligent decision support are driving efficiency gains.

Enterprises are leveraging AI laptops for real-time data analysis, predictive maintenance, supply chain optimization, and automated reporting, leading to documented performance improvements. As a result, organizations are allocating higher budgets for advanced AI-enabled endpoint devices that support secure, on-premise data processing in compliance-heavy sectors such as banking and government.

The development & research segment, particularly ML model training and AI software development, is forecast to grow at the highest rate through 2032. This surge stems from a proliferation of AI applications across an expanding array of verticals, including healthcare, automotive, and industrial automation, where developers require high NPU performance (>50 TOPS), discrete GPUs, and Linux support to accelerate workloads and reduce time-to-market.

The criticality of local, high-power AI processing in sensitive or latency-sensitive environments is propelling the demand for premium, purpose-built AI laptops tailored for deep learning and neural network training.

Operating System Insights

The operating system landscape for AI laptops is currently dominated by Windows, which commands an estimated 78% market share in 2025. This leadership position is reinforced by Microsoft's strategic Copilot+ PC certification framework, extensive enterprise deployment footprint, and comprehensive AI software ecosystem support from independent software vendors that optimize applications for Windows AI features.

Windows' dominance is being sustained through several structural advantages, including compatibility with AI frameworks such as TensorFlow, PyTorch, and ONNX Runtime. This has enabled developer productivity, OEM partnerships with Intel, AMD, and Qualcomm, ensuring hardware optimization across diverse processor architectures, and Microsoft's aggressive AI feature roadmap, incorporating the entire Windows suite.

MacOS is set to be the fastest-growing operating system segment during 2025 - 2032, driven by Apple's vertically integrated hardware-software optimization delivering exceptional AI performance-per-watt, strong macOS preference among content creators, and expanding Apple ecosystem adoption in the education sector.

Apple's M3 and M4 series processors with integrated Neural Engine deliver approximately 38 TOPS of AI performance according to independent benchmarking, while maintaining industry-leading battery efficiency, enabling higher-productivity workloads.

Regional Insights

North America AI Laptop Market Trends

North America is maintaining its leading position, commanding an estimated 32.5% of the AI laptop market share in 2025. The U.S. accounts for most of the regional revenue, driven by a concentrated technology company presence, robust enterprise AI adoption, substantial government and educational institution technology investments, and a favorable regulatory environment that encourages AI innovation.

The region's leadership reflects structural advantages, including headquarters concentration of leading AI laptop manufacturers, such as Dell, HP, Apple, and Microsoft, and a sophisticated venture capital ecosystem funding AI software startups, creating demand for high-performance development hardware.

Substantial growth opportunities are also emerging in mid-market enterprise adoption, where organizations employing 100-999 employees are beginning systematic AI laptop deployments to address competitive productivity pressures.

Beyond enterprises, digital transformations in the healthcare sector, adopting AI-enhanced diagnostic support and HIPAA-compliant telemedicine infrastructure, and education sector modernization programs are brightening regional market prospects.

Europe AI Laptop Market Trends

Europe represents the second-largest regional market for AI laptops, characterized by strong regulatory frameworks that shape product development priorities and sustainability requirements that influence hardware design and manufacturing processes.

Germany, the U.K., France, and Spain collectively lead the European AI laptop market revenue, with Germany at the top through manufacturing sector strength, financial services concentration in Frankfurt driving enterprise deployments, and Mittelstand company digital transformation initiatives prioritizing Industry 4.0 automation requiring AI-enhanced edge computing.

The accelerated growth of the European market is being propelled by GDPR compliance requirements necessitating on-device AI processing capabilities that maintain data sovereignty, the EU AI Act's risk-based regulatory framework incentivizing transparency, and sustainability mandates under the European Green Deal requiring energy-efficient computing solutions.

The competitive landscape reflects strong positions for U.S.-based OEMs, including Dell, HP, and Lenovo, maintaining 55-60% combined market share through enterprise channel partnerships and localized support infrastructure, while Apple commands around 25% of the market concentrated in creative industries and education segments.

European technology champions and emerging players focused on sustainability-differentiated offerings are gaining traction in government procurement and environmentally conscious enterprise segments.

Asia Pacific AI Laptop Market Trends

Asia Pacific is poised to emerge as the fastest-growing regional market for AI laptops, with a projected CAGR of about 24% during 2025 - 2032.

The market here is driven by rapid digitalization of the economy across China, India, and ASEAN countries, an expanding middle-class consumer base with rising disposable incomes, government-led AI development initiatives, and a concentrated manufacturing ecosystem that enables competitive pricing and rapid product iteration cycles.

China dominates regional market revenue owing to the government's strategic emphasis on achieving global AI leadership through initiatives such as the New Generation Artificial Intelligence Development Plan, substantial investments from technology giants including Alibaba and Tencent, and domestic vendor strength.

India represents the second-largest and fastest-growing country market within Asia Pacific. Its growth trajectory is being charted by the Digital India initiative, promoting technology adoption across education, healthcare, and public administration, the IT services sector’s strength in Bangalore, Hyderabad, and Pune, creating demand for software development and data science workstations, and expanding the premium consumer segment.

Japan's market exhibits mature adoption patterns, with strong enterprise-standardization on Windows platforms, a preference for domestic vendors, including NEC and Fujitsu, in government procurement, and creative professionals demanding high-specification configurations for video production and graphic design applications.

Competitive Landscape

The global AI laptop market landscape exhibits a moderately concentrated structure. Lenovo, HP, Dell, Apple, and ASUS collectively command approximately 70% market share in 2025, while the remaining 30% is fragmented among second-tier OEMs, specialized vendors, and regional players. This dynamic competitive environment is characterized by intense pricing pressure in mainstream segments and differentiation opportunities in vertical-specific and premium categories.

Lenovo maintains market leadership backed by a comprehensive product portfolio spanning IdeaPad, business ThinkPad, and gaming Legion lineups, competitive pricing enabled through manufacturing scale, and strong positions across enterprise, education, and consumer segments.

HP leverages enterprise channel strength through direct sales force and value-added reseller partnerships, premium positioning through Spectre and Envy consumer lineups and EliteBook business series, and a strategic focus on the commercial segment, where longer replacement cycles and higher average selling prices generate superior margins.

Key Industry Developments

- In November 2025, Apple announced a low-cost laptop targeting budget consumers and the education sector. Positioned to compete with Chromebooks and Windows PCs, the device will offer Apple Silicon performance and macOS integration, expanding Apple’s reach in education and emerging markets while strengthening its entry-level ecosystem presence.

- In September 2025, Qualcomm partnered with Saudi AI firm Humain to launch the Snapdragon X2 Elite-powered Horizon Ultra laptop with always-on 5G and AI-first Windows-on-ARM experiences. Aimed at consumers and enterprises, Humain also plans to release its “Adam” AI avatar in October to participate in corporate board meetings.

- In July 2025, HP launched its affordable AI laptops in India, the OmniBook 5 and 3 series, featuring AI-driven performance tuning, battery optimization, and security tools. Aimed at students and budget users, the lineup seeks to democratize AI computing with cost-effective devices capable of everyday AI workloads.

Companies Covered in AI Laptop Market

- Lenovo Group Limited

- HP Inc.

- Dell Technologies Inc.

- Apple Inc.

- ASUSTeK Computer Inc.

- Acer Inc.

- Microsoft Corporation (Surface)

- MSI (Micro-Star International Co., Ltd.)

- Samsung Electronics Co., Ltd.

- LG Electronics Inc.

- Razer Inc.

- Huawei Technologies Co., Ltd.

- Xiaomi Corporation

- HONOR Device Co., Ltd.

- Getac Technology Corporation

Frequently Asked Questions

The global AI laptop market is projected to reach US$32.2 Billion in 2025.

The convergence of enterprise digital transformation imperatives, advancement in neural processing architectures, and the proliferation of hybrid work models are driving the AI laptop market.

The AI laptop market is poised to witness a CAGR of 20.2% from 2025 to 2032.

Key opportunities stem from Microsoft’s formal Copilot+ PC certification framework, the shift toward AI-first chip architectures, and rising enterprise adoption of on-device AI to meet data-sovereignty, latency, and regulatory-compliance demands.

Lenovo Group Limited, HP Inc., Dell Technologies Inc., and Apple Inc. are some of the key players in the AI laptop market.