- Specialty & Fine Chemicals

- Antimicrobial Additives Market

Antimicrobial Additives Market Size, Trends, Share, and Growth Forecast for 2025 - 2032

Antimicrobial Additives Market by Product Type (Organic and Inorganic), Application (Plastics, Paints & coatings, Pulp & paper, and Others), Industry (Healthcare, Food & beverage, Packaging, Automotive, Building & construction, and Others), Regional Analysis from 2025 to 2032

Antimicrobial Additives Market Size and Share Analysis

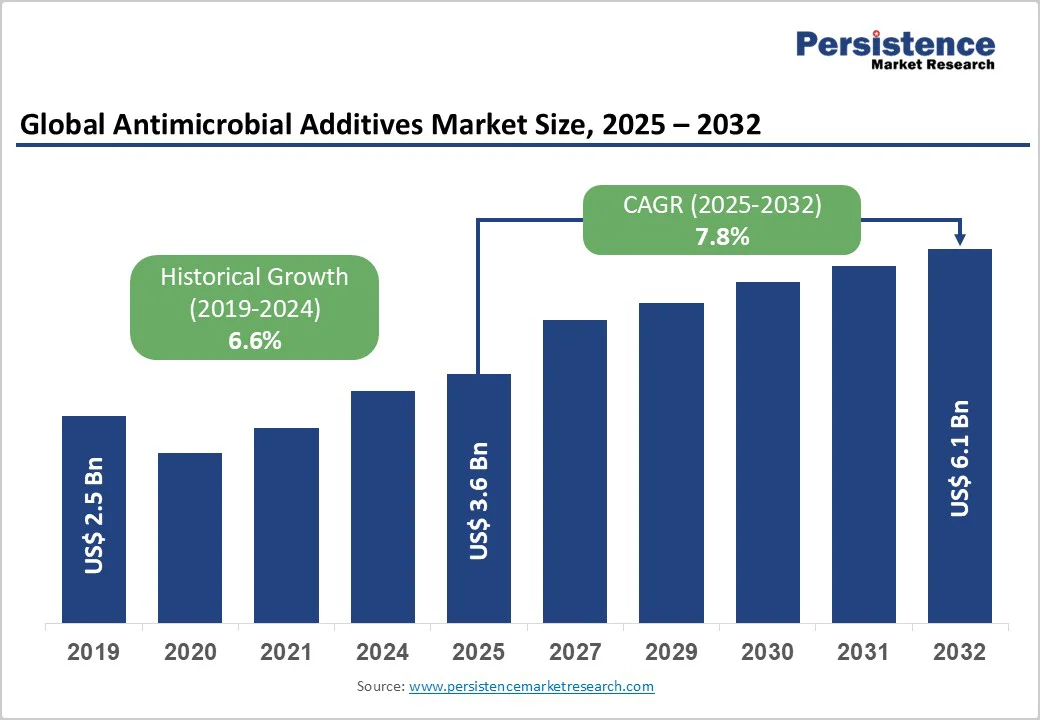

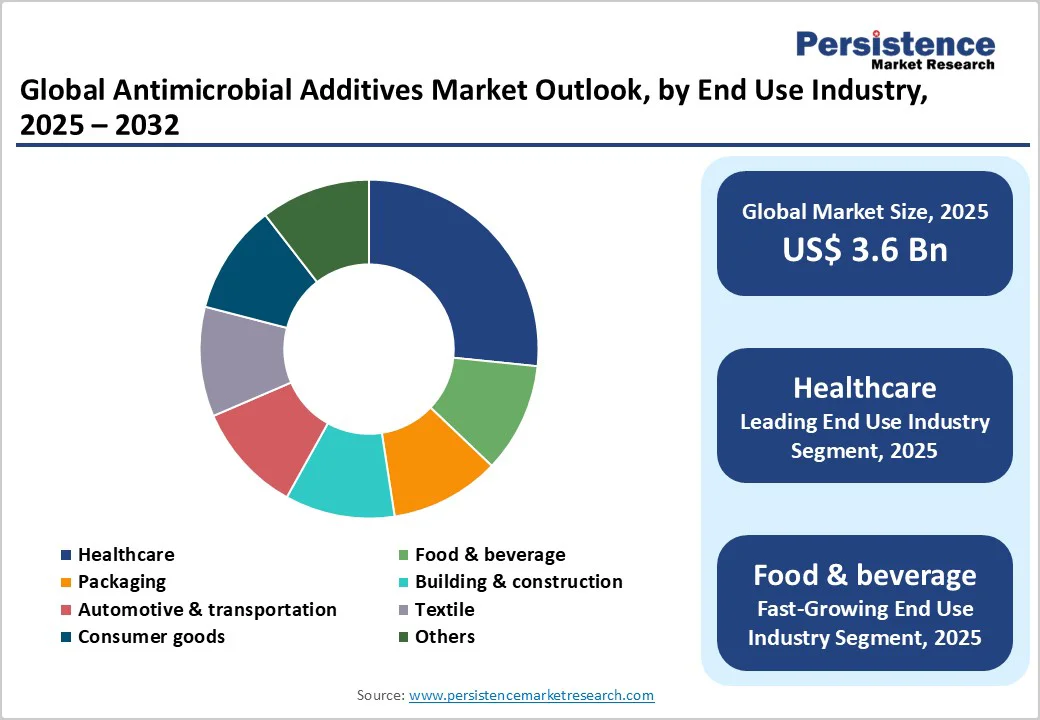

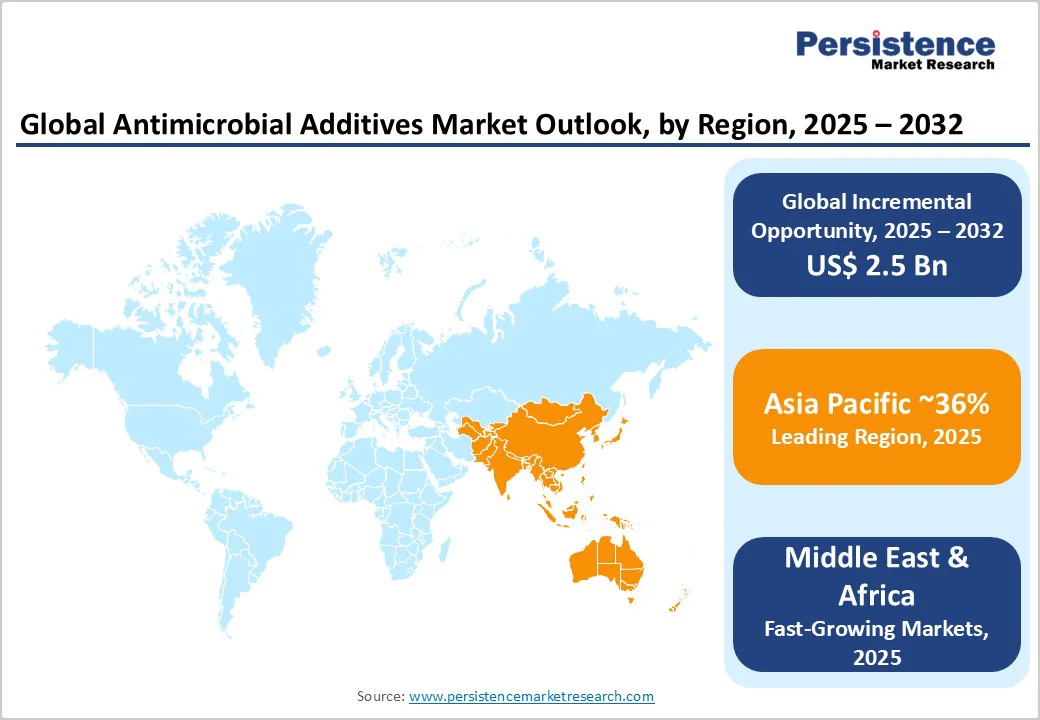

The global antimicrobial additives market size is likely to value at US$ 3.6 billion in 2025 and is projected to reach US$ 6.1 billion by 2032, growing at a CAGR of 7.8% between 2025 and 2032.

Rising concern over healthcare-associated infections, amplified hygiene regulations in food and packaging industries, and increased antimicrobial usage in plastics and coatings are driving expansion.

Regulatory mandates on antimicrobial efficacy, combined with advances in nanotechnology, are enhancing additive performance and adoption across various end-use industries.

Key Industry Highlights:

- Regional Leaders: Asia Pacific is the leading region, accounting for over 36% of global volume in 2025, fueled by strong government support, cost-competitive manufacturing, infrastructure development in China and India, and rising demand in packaging, textiles, and consumer goods.

- Leading Segments: Inorganic antimicrobial additives lead the market with 57% share in 2025, driven by their thermal stability, broad-spectrum efficacy, and regulatory acceptance under EPA and EU BPR frameworks. Organic additives, including silver, copper, and zinc-based chemistries, are also seeing growing adoption in healthcare and consumer segments.

- Industry Applications: Plastics constitute the largest application segment with 32% share, led by antimicrobial masterbatches for medical disposables, food-contact films, high-touch consumer products, and emerging biodegradable plastics.

- Industry: The Healthcare segment dominates, accounting for 24% of market value, reflecting widespread adoption in hospital equipment, surgical textiles, wound-care dressings, and other medical devices.

- Market Drivers: Key drivers include the prevention of healthcare-associated infections (HAIs), stringent food-packaging regulations, increasing hygiene awareness in consumer goods, and the adoption of antimicrobial additives in automotive and building materials.

- Market Restraints: Regulatory hurdles on biocidal substances (e.g., EPA, EU BPR) and volatility in raw material prices (silver, copper) are limiting flexibility and increasing production costs, particularly for smaller formulators.

- Market Opportunities: Emerging opportunities include antimicrobial car care products with double-digit CAGR potential and circular economy initiatives, such as reclaiming over 90% of silver from end-of-life polymer products, reducing virgin material usage, and meeting ESG goals.

| Key Insights | Details |

|---|---|

| Antimicrobial Additives Market Size (2025E) | US$ 3.6 Bn |

| Projected Market Value (2032F) | US$ 6.1 Bn |

| Global Market Growth Rate (CAGR 2025 to 2032) | 7.8% |

| Historical Market Growth Rate (CAGR 2019 to 2024) | 6.6% |

Market Dynamics

Driver - Hospitals and Clinics Are Strengthening Measures to Prevent Healthcare-Associated Infections

Hospitals and clinics worldwide are intensifying efforts to curb the incidence of healthcare-associated infections (HAIs), which not only compromise patient safety but also inflate treatment costs by up to US$ 45,000 per case. This urgency has propelled medical device manufacturers to integrate antimicrobial agents, most notably organic silver and copper-based compounds, into high-touch surfaces, catheter coatings, and surgical textiles.

Clinical studies have demonstrated that surfaces embedded with silver nanoparticles can reduce bacterial counts by over 99% within hours, aligning with CDC and WHO recommendations for infection control. Such proven efficacy is fostering wider adoption across the Healthcare segment, where regulatory bodies now recommend or require validated antimicrobial performance as part of product approval protocols.

Rising Demand for Antimicrobial Packaging to Enhance Food Safety and Shelf Life

The global surge in fresh and minimally processed foods has intensified demand for packaging solutions that extend product shelf life while ensuring safety. In 2024, the U.S. meat and poultry sector processed over 50 billion pounds of product, with consumer expectations driving manufacturers to seek active-packaging technologies that inhibit microbial growth.

Antimicrobial additives, particularly zinc pyrithione and organic silver formulations, are being incorporated into polymer films and coatings, delivering continuous protection against spoilage organisms such as Listeria and E. coli.

This trend intersects with the Agricultural Microbial Market, where research on bio-based antimicrobial systems is advancing synergistic performance in bioplastic packaging. Regulatory frameworks from the FDA for antimicrobial food-contact materials further validate efficacy requirements, encouraging brands to adopt such innovations to differentiate on safety and freshness.

Restraint - Stringent Regulatory Requirements on Biocidal Substances Are Limiting Market Flexibility

The U.S. EPA and European Biocidal Products Regulation (BPR) impose rigorous testing and registration requirements for novel antimicrobial chemistries, extending time-to-market by 12–18 months and increasing compliance costs by up to 20%. Manufacturers of nanosilver and other emerging agents face complex data demands, including ecotoxicity, human health risk assessments, and environmental fate studies.

Smaller formulators often lack the resources to navigate these protocols, resulting in market consolidation around established chemical majors. Even after registration, label claims and usage levels remain tightly controlled, limiting formulators’ flexibility to tailor additive concentrations for diverse applications.

Volatility in Raw Material Prices Is Increasing Production Costs and Constraining Adoption

Key antimicrobial ingredients such as silver and copper are subject to global commodity market fluctuations. In early 2025, silver spot prices surged by 25% due to mine disruptions and speculative trading, significantly increasing costs for product formulators. This volatility forces manufacturers to either absorb margin pressure or raise prices for end users in sensitive markets like medical devices and consumer goods.

Some companies have begun exploring alternative chemistries, such as zinc-based and organic biocides, to mitigate reliance on precious metals, but these substitutes often exhibit lower efficacy or compatibility challenges, constraining widespread adoption.

Opportunity - Rapid Growth in Antimicrobial Car Care Products Creates New Revenue Opportunities

The antimicrobial car care products market is creating new avenues for additive suppliers. Consumers increasingly demand in-vehicle hygiene solutions, sprays, coatings, and interior treatments, that can neutralize bacteria and viruses on high-contact surfaces.

Formulators can capitalize by offering specialized antimicrobial masterbatches and coatings compatible with automotive-grade plastics, textiles, and composites. Partnerships with OEMs and aftermarket brands to develop custom formulations for cabin air filters and touchpoints present significant revenue potential.

Circular Economy and Recycling Initiatives Are Driving Sustainable Antimicrobial Solutions

Sustainability imperatives are driving the development of closed-loop recovery systems for precious-metal antimicrobials. Recent studies indicate that pyrolysis and electrochemical processes can reclaim over 90% of silver from end-of-life polymer products, enabling manufacturers to reduce virgin silver usage by 50% without compromising antimicrobial performance.

Such innovations align with ESG requirements and circular-economy frameworks, appealing to environmentally conscious customers and investors. Leading players are collaborating with recycling firms and academic institutions to commercialize cost-effective recovery technologies, positioning themselves as providers of both antimicrobial additives and sustainable material-management solutions.

Category-wise Insights

Product Type Analysis

Inorganic antimicrobial additives, including OBPA, DCOIT, and Triclosan, command 57% of market value in 2025, owing to their exceptional thermal stability, broad-spectrum efficacy, and compatibility with a wide range of polymer matrices. Applications in marine coatings, outdoor textiles, and injection-molded plastics benefit from the long-term durability and rapid microbial kill rates of these chemistries.

Regulatory acceptance under EPA and EU BPR frameworks further entrenches their use in infrastructure and industrial goods, where routine sanitization is impractical. Their performance consistency at elevated temperatures and in harsh chemical environments continues to justify premium pricing, reinforcing market leadership.

Application Analysis

The plastics segment holds a 32% share, propelled by antimicrobial masterbatches and additives for medical disposables, food-contact films, and high-touch consumer products. Embedding antimicrobials during compounding ensures homogeneous distribution and sustained efficacy, crucial for products such as IV tubing, catheter components, and single-use packaging.

The ongoing shift toward sustainable polymers has prompted formulators to tailor additive chemistries compatible with biodegradable and bio-based plastics, meeting both performance and environmental mandates. This convergence with the Agricultural Microbial Market underscores cross-sector innovation in active packaging solutions.

Industry Analysis

The Healthcare segment accounts for 24% of market value, reflecting extensive integration of antimicrobial additives into hospital equipment, surgical textiles, and wound-care dressings.

Rising HAI rates have prompted hospital systems to mandate antimicrobial surfaces and device components, driving formulators to develop low-leach, high-efficacy additives compliant with FDA and ASTM standards. Innovations in silver nanoparticle stabilization and controlled-release systems are delivering multi-day protection on surfaces and textiles, further boosting adoption in long-term care and outpatient facilities.

Regional Insights

North America Antimicrobial Additives Market Trends

North America is witnessing significant growth in antimicrobial additives, supported by stringent infection-control regulations and a mature healthcare infrastructure. The FDA’s 2024 guidance on antimicrobial food-contact materials has accelerated innovations in film and coating formulations, while the EPA’s conditional registration of new nanosilver products in mid-2025 has broadened approved applications to include textiles, sportswear, and household linens.

Active R&D clusters across the U.S. are developing next-generation nano-enabled additives with tailored release profiles, optimizing particle size and surface chemistry to maximize microbial inhibition.

Europe Antimicrobial Additives Market Trends

Europe’s market growth is driven by regulatory alignment under EU BPR and REACH, which standardize biocidal approval processes across member states. Germany, France, the U.K., and Spain are at the forefront, integrating antimicrobial pigments and masterbatches into industrial coatings, building materials, and automotive interiors to meet hygiene certifications.

Collaborative initiatives among chemical manufacturers and coating formulators are exploring hybrid copper–silver systems to achieve synergistic efficacy and reduced metal content, aligning with the region’s sustainability goals.

Asia Pacific Antimicrobial Additives Market Trends

Asia Pacific is the leading region in antimicrobial additive consumption, accounting for over 36% of global volume by 2025. Rapid infrastructure development in China and India, along with government-led initiatives to combat antimicrobial resistance in agriculture, is driving strong demand for additives in food packaging, textiles, and consumer goods.

ASEAN countries are expanding local polymer compounding capacities, enabling cost-competitive antimicrobial masterbatches. Additionally, public–private partnerships in China are fostering research on bio-based antimicrobial systems, positioning the region as a key hub for scale-up and export to mature markets.

Competitive Landscape for the Antimicrobial Additives Market

The antimicrobial additives market is moderately fragmented, with major chemical conglomerates, such as BASF SE, Clariant AG, and Dow Inc., competing alongside specialized technology providers such as Microban International and BioCote Limited.

Key differentiators include proprietary nanoparticle synthesis, controlled-release coatings, and integrated regulatory support services. R&D alliances with academic institutions and cross-industry collaborations on sustainability and recycling further enhance competitive positioning. Companies are also pursuing capacity expansions in Asia to reduce lead times and improve cost efficiencies for global customers.

Recent Industry Developments

- In July 2025, The U.S. Environmental Protection Agency (EPA) granted unconditional registration for NanoBioMatters’ latest nanosilver-based antimicrobial formulation. This regulatory approval allows the company to deploy its product broadly across textiles, plastics, and polymer-based surfaces, expanding commercial opportunities in medical devices, consumer goods, and high-touch public surfaces.

- In March 2024, BioCote Limited launched a recycled-content silver additive in partnership with leading plastics compounders, marking a significant step toward sustainable antimicrobial solutions. The innovation enables manufacturers to reduce virgin silver consumption by 50%, cutting raw material costs while maintaining antimicrobial performance.

- In January 2023, Clariant AG inaugurated a dedicated antimicrobial R&D center in Germany, focused on advancing sustainable copper-based and hybrid additive chemistries. The facility is equipped to develop next-generation antimicrobial solutions tailored for industrial, healthcare, and consumer applications, emphasizing eco-efficiency, regulatory compliance, and performance optimization.

Companies Covered in Antimicrobial Additives Market

- BASF SE

- NanoBioMatters Industries S.L

- RTP Company

- Milliken Chemical

- BioCote Limited

- Microban International

- Clariant AG

- PolyOne Corporation

- Momentive Performance Materials Inc.

- Life Materials Technologies Limited

- SteriTouch Limited

- Sanitized AG

- Dow Inc.

- LyondellBasell Industries Holdings B.V.

- Plastics Color Corporation

- Lonza

Frequently Asked Questions

The antimicrobial additives market is expected to reach US$ 6.1 Bn by 2032, up from US$ 3.6 Bn in 2025.

Key drivers include prevention of HAIs, stringent food-packaging regulations, and rising hygiene awareness in consumer products.

Inorganic additives lead with 57% share due to thermal stability, broad-spectrum efficacy, and regulatory acceptance.

North America leads adoption, driven by advanced healthcare infrastructure and robust regulatory frameworks.

Implementing circular economy recovery methods for silver and copper to reduce raw-material usage and support ESG goals.

Leading companies include BASF SE, Microban International, and Clariant AG, recognized for extensive portfolios and technical expertise.