- Industrial Goods & Service

- Container Homes Market

Container Homes Market Size, Share, and Growth Forecast, 2026 - 2033

Container Homes Market by Structure Type (Fixed, Movable), End-User (Residential, Commercial, Industrial, Emergency & Disaster Relief, Others), Distribution Channel (Direct Manufacturer Sales, Online Platforms, Dealers, Retail Exhibitions), and Regional Analysis for 2026 - 2033

Container Homes Market Share and Trends Analysis

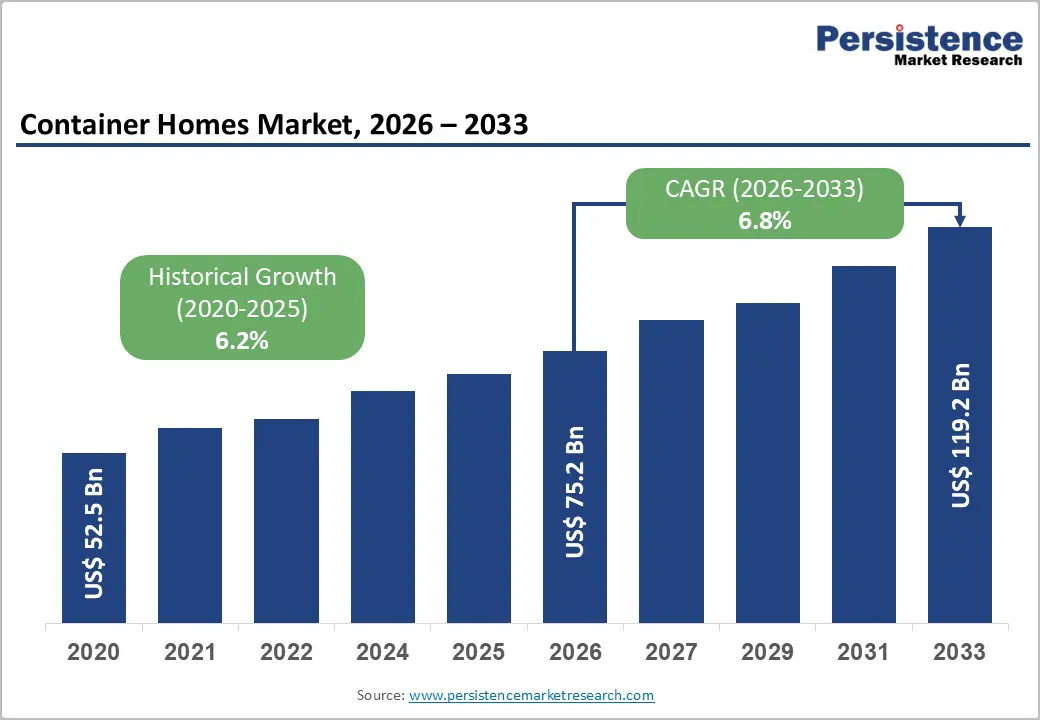

The global container homes market size is likely to be valued at US$ 75.2 billion in 2026, and is projected to reach US$ 119.2 billion by 2033, growing at a CAGR of 6.8% during the forecast period 2026 - 2033.

The market demonstrates sustained expansion driven by structural shifts in global housing demand and construction economics. Rapid urban population growth, rising housing affordability constraints, and increased pressure on traditional construction timelines have accelerated the adoption of modular housing formats. Container-based housing solutions address these challenges by enabling standardized, scalable, and time-efficient construction across residential and non-residential applications. Government-backed affordable housing initiatives and disaster-resilient infrastructure programs further reinforce demand by prioritizing deployable and cost-managed housing alternatives.

Key Industry Highlights

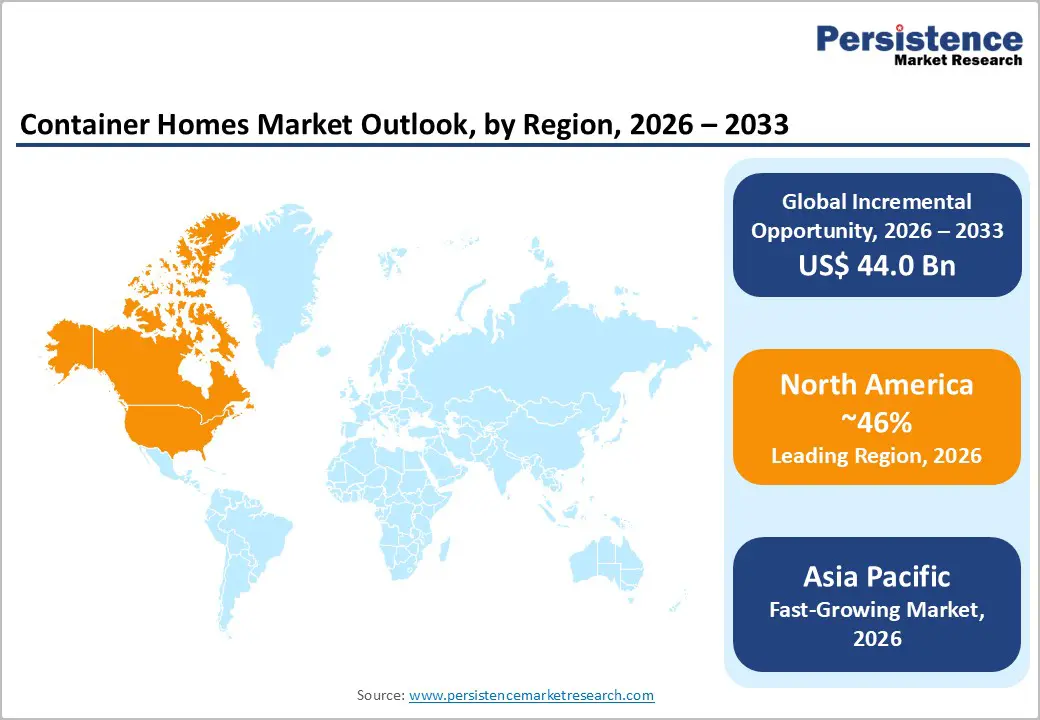

- Dominant Region: North America is expected to hold about 46% share in 2026, driven by the early adoption of modular construction and well-established infrastructure networks.

- Fastest-growing Market: Asia Pacific is forecasted to be the fastest-growing market from 2026 to 2033, fueled by a surging demand for affordable, flexible housing solutions.

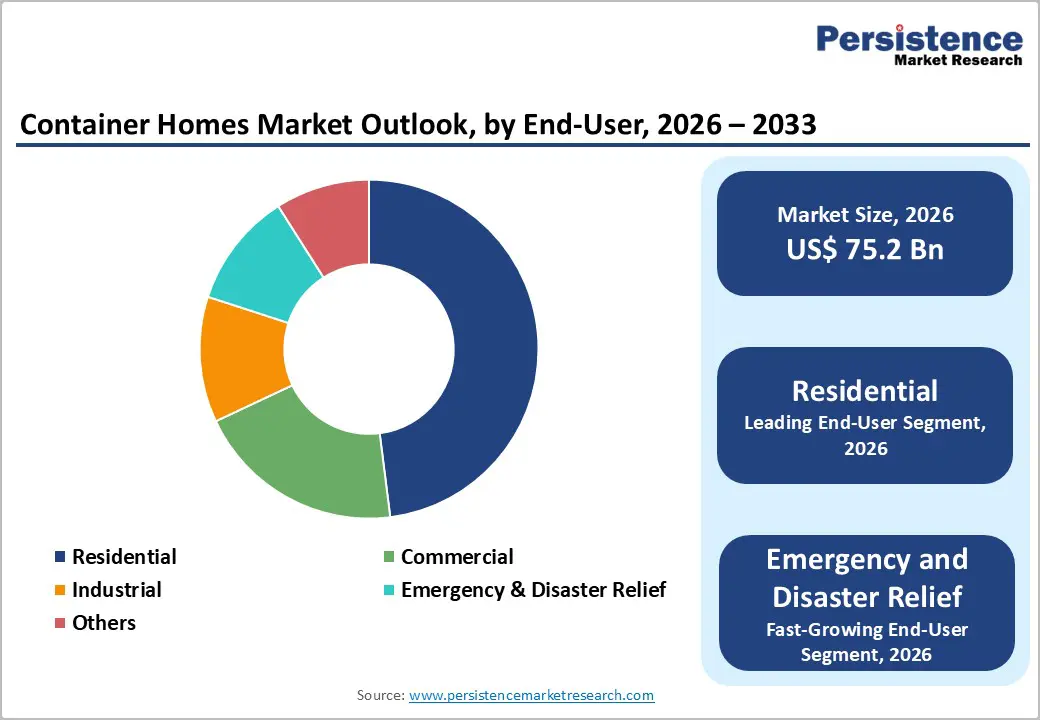

- Leading End-User: Residential users are likely to lead with around 48% revenue share in 2026 due to worsening housing affordability challenges and growing acceptance of modular living.

- Fastest-growing End-User: Emergency and disaster relief users are slated to grow the fastest through 2033, owing to the increasing frequency and intensity of natural disasters.

- December 2025: St. Louis Development Corporation approved 10 modular homes on vacant lots in tornado-damaged north city neighborhoods using US$ 3.2 million in federal funds.

| Key Insights | Details |

|---|---|

| Container Homes Market Size (2026E) | US$ 75.2 Bn |

| Market Value Forecast (2033F) | US$ 119.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Supportive Sustainability and Environmental Regulations

Strengthening support from sustainability and environmental regulations is a powerful factor fueling the container homes market growth, as policy frameworks increasingly prioritize low-impact construction, resource efficiency, and carbon reduction across the built environment. Regulatory pressure on traditional construction methods has intensified through stricter limits on emissions, material waste, water usage, and land disruption, creating structural cost and compliance challenges for conventional housing models. In contrast, modular steel-based structures align closely with regulatory objectives through reuse of existing materials, controlled off-site fabrication, and reduced construction waste. Regulatory incentives, green building certifications, and public-sector sustainability targets reinforce preference for solutions that demonstrate measurable environmental performance, shorter construction timelines, and predictable compliance outcomes. This alignment positions container-based structures as a practical response to regulatory expectations rather than an experimental alternative.

Environmental regulations also reshape procurement behavior among developers, institutional buyers, and public authorities by shifting evaluation criteria toward lifecycle efficiency and long-term environmental value. Policies addressing circular economy adoption, embodied carbon reduction, and energy performance standards elevate demand for building formats that integrate these requirements at the design stage. Container-based construction supports regulatory compliance through standardized insulation integration, renewable energy compatibility, and efficient space utilization, reducing approval complexity and project risk. Urban planning authorities increasingly favor compact, relocatable, and low-disruption housing formats to meet zoning and sustainability objectives, reinforcing acceptance of this construction approach.

Regulatory and Zoning Restrictions to Challenge the Market

Regulatory and zoning restrictions represent a critical restraint as existing land-use frameworks and building codes were primarily designed around conventional housing models. Several local authorities classify container-based structures under temporary, industrial, or non-residential categories, which limits approval for permanent habitation. Zoning ordinances in several urban and suburban areas restrict unconventional structures through minimum size requirements, aesthetic controls, height limitations, and neighborhood conformity standards. These constraints extend approval timelines, increase compliance complexity, and introduce uncertainty into project feasibility. Inconsistent interpretation of codes across municipalities further complicates large-scale deployment, reducing standardization benefits that modular construction seeks to deliver.

This restraint is further reinforced by safety, durability, and environmental compliance expectations embedded within regulatory frameworks. Authorities often require extensive structural modifications, insulation upgrades, fire resistance treatments, and foundation enhancements before granting occupancy permits. These requirements erode cost and speed advantages, weakening the value proposition for both residential and commercial adopters. Financing institutions and insurers also align risk assessments with regulatory acceptance, limiting access to capital when approvals remain uncertain. Public perception influenced by zoning resistance and neighborhood opposition further shapes regulatory enforcement intensity.

Integration of Smart Technologies to Elevate Production Output

The integration of smart technologies stands out as a key opportunity due to the inherent modular and standardized nature of container-based structures, which aligns effectively with digital systems integration. Factory-led fabrication enables pre-installation of sensors, energy management systems, smart lighting, and climate control units with high precision and minimal on-site variability. This approach supports consistent quality, faster commissioning, and predictable performance outcomes. Rising expectations for energy transparency, remote monitoring, and automated control across residential and commercial spaces elevate the relevance of connected solutions. Smart technologies transform compact steel units into data-driven living and working environments, improving space utilization, operational efficiency, and lifecycle performance while supporting compliance with evolving sustainability benchmarks.

Demand dynamics further strengthen this opportunity, driven by urban density pressures, remote workforce expansion, and increased preference for flexible living formats. Smart-enabled units support adaptive usage patterns through real-time energy optimization, security automation, and predictive maintenance, which enhances asset value and long-term operating efficiency. For example, in September 2025, Samsung unveiled its Smart Modular Home, integrating AI-powered appliances, efficient heating, ventilation, & air conditioning (HVAC) systems with SmartThings connectivity for seamless residential solutions. Digital integration also enables scalability across multi-unit deployments, supporting centralized control and standardized upgrades. For developers and operators, smart technologies create differentiation through service-oriented models such as monitoring subscriptions and performance-based maintenance frameworks. For end users, technology-enabled environments deliver measurable cost control, comfort consistency, and resilience against utility volatility.

Category-wise Analysis

Structure Type Insights

Fixed container homes are poised to lead with a forecasted 62% share in 2026, owing to regulatory acceptance for permanent housing, enhanced insulation performance, and compatibility with utility infrastructure. Fixed units benefit from alignment with long-term building codes, fire safety standards, and energy efficiency requirements, which supports approval certainty across jurisdictions. Integration with permanent foundations improves structural stability and thermal performance, enabling suitability for year-round occupancy. Financial institutions demonstrate stronger lending appetite toward fixed formats due to lower risk profiles and longer asset life cycles.

Movable container homes are anticipated to be the fastest-growing segment between 2026 and 2033, fueled by demand for flexible housing solutions across emergency relief, temporary workforce accommodation, and mobile commercial units. Movable formats offer rapid deployment advantages where speed, relocation capability, and short installation timelines remain critical decision factors. Asset reuse across projects improves capital efficiency for government agencies, mining operators, and infrastructure contractors. Advancements in chassis design, lightweight composites, and foldable configurations improve transport economics and site adaptability. For instance, Liansheng Assembly manufactures portable modular office container houses with quick-assembly and foldable designs for construction sites and remote workspaces.

These durable, customizable units cut costs through efficient transport and promote sustainability via reduced waste and repurposed materials.

End-User Insights

Residential users are likely to be the leading segment with a projected 48% of the container homes market revenue share in 2026, due to rising housing affordability challenges and increasing acceptance of modular living formats. Urban populations are experiencing growing cost pressures, which drives interest in smaller, efficient, and fully customizable housing units. Prefabricated container-based homes offer predictable construction timelines, reduced labor costs, and sustainable material use, enhancing appeal to first-time buyers and young families. Acceptance grows as developers integrate modern design aesthetics, green building practices, and energy-efficient systems. Supportive government policies, including incentives for affordable housing and streamlined permitting processes, further boost adoption.

Emergency and disaster relief users are expected to witness the fastest growth between 2026 and 2033, powered by climate adaptation strategies and humanitarian response investments. Rising frequency of natural disasters, extreme weather events, and humanitarian crises increases demand for rapidly deployable, resilient housing solutions. Container-based shelters offer the ability to pre-fabricate, transport, and install units within days, meeting urgent housing needs efficiently. Governments, aid organizations, and disaster management agencies prioritize solutions that allow reuse and repurposing, optimizing resource allocation across multiple projects. In the U.S., for instance, shipping containers have proven effective as emergency shelters due to their durability, rapid deployment, and versatility in disaster scenarios such as Hurricane Maria in Puerto Rico. Their steel construction withstands harsh weather, while modular designs enable quick customization and transport to affected areas.

Distribution Channel Insights

Direct manufacturer sales are slated to hold a dominant position, with an anticipated 55% of the revenue share in 2026, driven by project-based procurement and customization requirements. Large-scale residential, commercial, and institutional projects often require tailored designs, structural modifications, and integration with utility systems, which are best managed through direct engagement with manufacturers. Direct sales enable real-time communication regarding material selection, compliance with local building codes, and technical support during installation. This approach ensures higher quality assurance, consistent project timelines, and accountability across the supply chain.

Online platforms are forecasted to be the fastest-growing distribution channel between 2026 and 2033, boosted by digitalization of construction procurement and increased small-scale residential demand. Virtual configurators, 3D modeling tools, and interactive design software allow prospective buyers to personalize layouts, finishes, and energy systems remotely. E-commerce portals reduce intermediary costs, streamline ordering, and provide transparent pricing, making container-based solutions more accessible to individual homeowners and small developers. Online engagement also enables faster project approvals and coordination with logistics providers.

Regional Insights

North America Container Homes Market Trends

North America is expected to dominate with an estimated 46% of the container homes market share in 2026, reflecting early adoption of modular construction solutions, advanced manufacturing capabilities, and well-established infrastructure networks. High urban density in major metropolitan areas has created consistent demand for housing formats that optimize land utilization and reduce construction timelines. Integration of building code frameworks for prefabricated and modular structures enables rapid regulatory approvals compared with other markets. Public and private sector investment in urban infill projects, affordable housing initiatives, and mixed-use redevelopment has created a stable pipeline for container-based solutions. Advanced fabrication facilities, including automated welding and precision assembly, enhance quality consistency and reduce lead times for large-scale deployment. Established logistics networks for container handling support efficient supply chain management, allowing seamless transport and on-site assembly.

The dominance of North America is further reinforced by strategic collaboration between industrial developers and technology providers across the region. Container homes in commercial and residential applications benefit from integration with smart energy systems, modular utility connections, and energy-efficient insulation, enabling compliance with stringent environmental regulations. Institutional adoption by corporate campuses, universities, and government agencies demonstrates recognition of operational efficiency and lifecycle cost reduction. Investment flows favor projects combining sustainability, rapid deployment, and adaptability to urban growth, creating recurring demand channels. Competitive differentiation among local manufacturers through advanced design libraries, customization options, and turnkey delivery models strengthens market leadership.

Europe Container Homes Market Trends

The Europe container homes market is expected to demonstrate steady growth during the 2026-2033 forecast period, supported by strong regulatory frameworks for sustainable construction, established modular housing practices, and growing urban redevelopment initiatives. Countries such as Germany, the Netherlands, and the United Kingdom have integrated energy efficiency and circular construction requirements into building codes, encouraging adoption of container-based solutions that reduce material waste and lifecycle costs. Urban centers face moderate land constraints and rising housing demand, creating a niche for modular housing models that can be efficiently deployed within existing infrastructure. Investment in local manufacturing and prefabrication facilities enables scalable production, ensuring rapid delivery timelines and cost control. Public and private redevelopment programs in post-industrial zones and underutilized urban areas provide opportunities for container-based solutions in commercial and mixed-use projects.

Growth is further supported by technology adoption and market-oriented design innovation. Integration of energy-efficient insulation, modular utility connections, and smart building systems enhances operational efficiency and regulatory compliance. Developers leverage container homes for commercial applications, temporary accommodations, and flexible residential solutions, enabling adaptable use in urban regeneration projects. Policy incentives for sustainable housing, combined with strategic partnerships between local manufacturers and institutional developers, provide recurring deployment channels. Investment flows focus on green building initiatives, workforce housing, and rapid urban infill projects, enabling predictable market expansion. Competitive differentiation among manufacturers through design customization, turnkey solutions, and technology-enabled project delivery strengthens market position.

Asia Pacific Container Homes Market Trends

Asia Pacific is forecasted to be the fastest-growing market for container homes between 2026 and 2033, stimulated by rapid urbanization, large-scale infrastructure expansion, and rising demand for affordable, flexible housing solutions. High population density in emerging metropolitan centers drives demand for construction models that optimize land use and shorten project timelines. Governments across multiple economies prioritize modular and prefabricated housing programs to address urban housing shortages and improve disaster resilience. Industrial and infrastructure projects, including transportation corridors, logistics hubs, and temporary workforce accommodations, create recurring demand for container-based construction. Cost pressures on conventional construction methods, coupled with labor constraints, enhance the appeal of standardized container modules that reduce reliance on on-site skilled labor.

Technology integration and sustainability initiatives are also energizing regional market growth. Container homes increasingly incorporate energy-efficient insulation, modular utility systems, and solar-ready designs, aligning with environmental regulations and corporate sustainability objectives. Private developers leverage container-based solutions in commercial, hospitality, and co-living projects to enable flexible, reconfigurable spaces that respond to market demand. Disaster response and climate adaptation programs provide additional deployment channels, supporting large-scale rapid scaling. Digital design platforms, virtual project simulations, and online procurement tools enhance accessibility and reduce transactional barriers. Cross-border partnerships and capital inflows enable manufacturing capacity expansion and logistical efficiency, creating scalable delivery frameworks.

Competitive Landscape

The global container homes market exhibits a moderately fragmented structure with regional manufacturers and specialized modular housing providers. Multiple players operate across diverse geographies, focusing on project-specific solutions for residential, commercial, and emergency applications. Competition is influenced by local regulations, construction standards, and consumer preferences, which allows regional manufacturers to capture niche segments. Project-based procurement practices further disperse market share, as developers and institutions often engage with suppliers that can meet specific design, installation, and compliance requirements.

Key players in the market include SG Blocks, Inc., Algeco, Modulaire Group, Kubed Living, Container Homes USA., and SEABOX. These companies leverage experience in modular construction, standardized production processes, and project management expertise to maintain competitiveness. SG Blocks, Inc. and Container Homes USA focus on modular residential and commercial deployments with integrated utility systems. Algeco and Modulaire Group operate across multiple regions, offering scalable solutions for industrial, commercial, and institutional projects. Kubed Living and SEABOX emphasize innovative design, sustainability, and rapid deployment capabilities.

Key Industry Developments

- In December 2025, Guangdong WELLCAMP Steel Structure & Modular Housing Co., Ltd. launched and exhibited rapid-deployment folding and expandable container houses at major exhibitions across South America, Southeast Asia, and the Middle East, drawing global interest for mining, disaster relief, infrastructure, and remote accommodation solutions.

- In November 2025, Bermuda's Minister Zane DeSilva announced plans for 11 modular container homes to address urgent housing needs, including studio, one-bedroom, and expandable two- to three-bedroom units. These units will deploy on government land in the West End early next year as a pilot to test rapid, cost-effective construction methods for broader affordable housing expansion.

- In September 2025, remote residents of Punmu in Western Australia’s desert pooled community funds to buy prefabricated container homes made overseas to escape long-standing unsafe housing conditions after decades of inadequate government support.

Companies Covered in Container Homes Market

- SG Blocks, Inc.

- Algeco

- Modulaire Group

- Kubed Living

- Container Homes USA.

- SEABOX

- Falcon Structures.

- United Rentals Australia Pty Limited.

- Speed House Group of Companies.

Frequently Asked Questions

The global container homes market is projected to reach US$ 75.2 billion in 2026.

Rapid urbanization, rising demand for affordable and flexible housing, and integration of sustainable modular construction solutions drive the market.

The market is poised to witness a CAGR of 6.8% from 2026 to 2033.

Expansion of disaster-resilient housing programs and flexible commercial and mixed-use applications represent key market opportunities.

Key players in the market include SG Blocks, Inc., Algeco, Modulaire Group, Kubed Living, Container Homes USA., SEABOX, and Falcon Structures.