- Smart Packaging

- Essential Oil Containers Market

Essential Oil Containers Market Size, Share, and Growth Forecast, 2026 - 2033

Essential Oil Containers Market By Material (Glass, Aluminum, Others), Product Type (Bottles, Jars, Others), Capacity, End-user, and Regional Analysis for 2026 - 2033

Essential Oil Containers Market Size and Trends Analysis

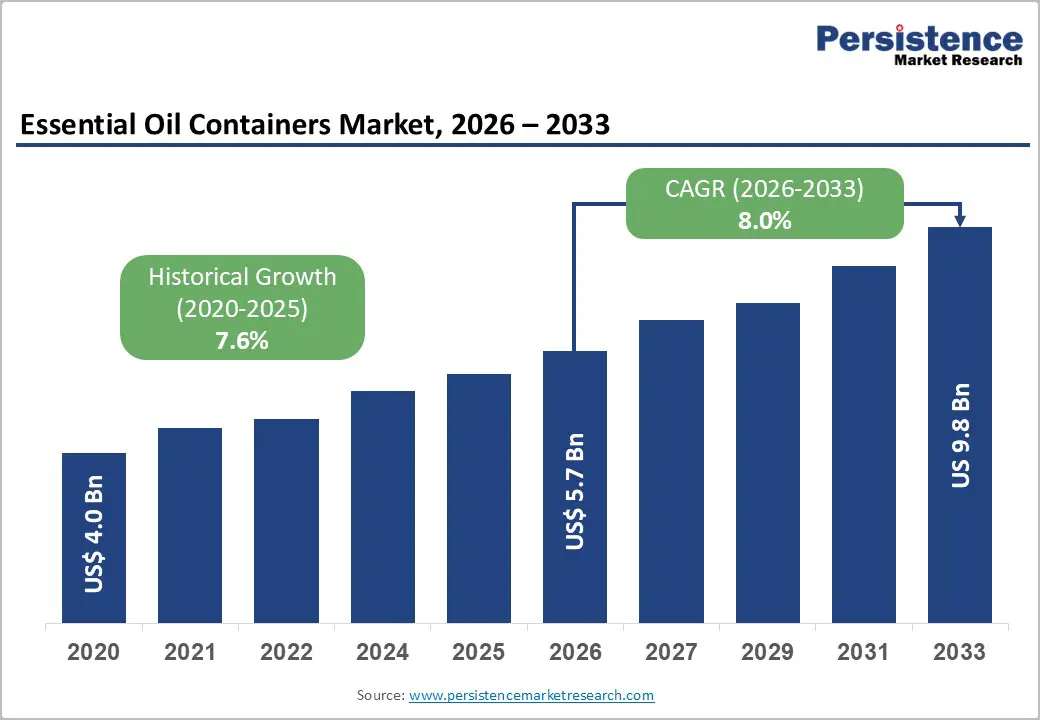

The global essential oil containers market size is likely to be valued at US$5.7 billion in 2026 and is expected to reach US$9.8 billion by 2033, growing at a CAGR of 8.0% during the forecast period from 2026 to 2033, driven by rising consumer adoption of aromatherapy and natural personal-care products, the rapid scaling of direct-to-consumer and e-commerce distribution models, and a sustained shift toward protective and sustainable packaging solutions, particularly glass and recycled materials that preserve volatile botanical compounds.

Rising use in pharmaceutical and wellness products is driving higher order volumes and a broader range of container formats, including droppers, roll-ons, and ampoules. Although demand remains robust, fluctuations in costs and ongoing supply-chain challenges are influencing investment decisions, opening focused opportunities in lightweight glass solutions, recyclable packaging, and advanced dispensing technologies.

Key Industry Highlights

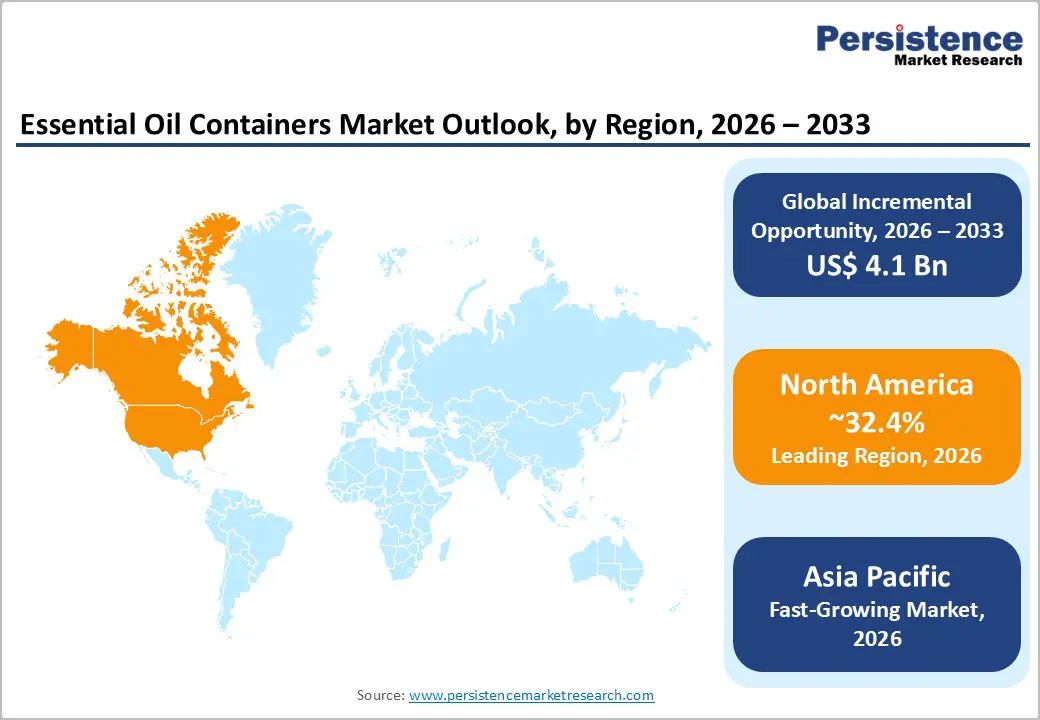

- Leading Region: North America is projected to lead the market with an estimated 32.4% share, supported by strong U.S. consumer spending on wellness products, stringent regulatory standards, and high adoption of premium glass and aluminum packaging formats.

- Fastest-growing Region: Asia Pacific is the fastest-growing regional market, driven by the rapid expansion of DTC wellness brands in China, India, and ASEAN, rising disposable incomes, and manufacturing cost advantages, resulting in above-average regional CAGR compared to the global average.

- Investment Plans: Investments are primarily directed toward automated lightweight glass production, aluminum roll-on and spray formats, and sustainable packaging innovations, including recycled content and refill-ready containers, particularly in North America and Europe, to meet regulatory and ESG requirements.

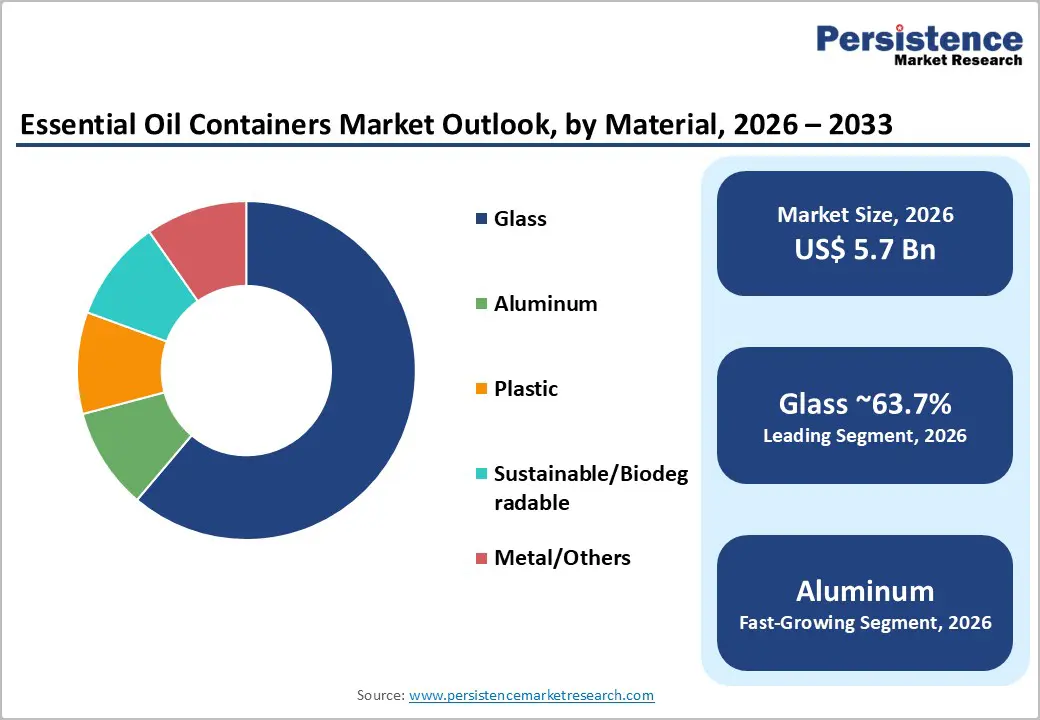

- Dominant Material: Glass is anticipated to dominate the market with approximately 63.7% share, owing to its chemical inertness, UV protection properties, regulatory acceptance for therapeutic applications, and strong preference among premium aromatherapy and pharmaceutical brands.

- Leading Product Type: Bottles are estimated to hold the largest share of the product type at approximately 51.6%, supported by their versatility, dosing accuracy, standardized filling infrastructure, and widespread use across personal care, aromatherapy, and wellness applications.

| Key Insights | Details |

|---|---|

| Essential Oil Containers Market Size (2026E) | US$5.7 Bn |

| Market Value Forecast (2033F) | US$9.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expansion of Aromatherapy, Wellness, and Natural Personal-Care Demand

Global demand for aromatherapy and essential-oil-based products has recorded sustained high single-digit to low double-digit growth, driven by consumer preference for natural, plant-based wellness solutions. This trend directly increases demand for small-capacity, dosing-sensitive containers, particularly in the 5-30 ml range. Product proliferation across categories such as therapeutic blends, topical serums, roll-ons, and home-fragrance oils is increasing the average number of container units per product portfolio. As a result, container suppliers are benefiting from both volume expansion and improved price realization, particularly for glass bottles and precision droppers. Growth in end-use markets correlates strongly with container consumption, reinforcing the structural nature of this demand driver.

Sustainability and Material Transitions Favoring Glass and Premium Closures

Brand owners and regulators increasingly prioritize reusable, recyclable, and high post-consumer recycled content packaging, particularly for essential oils that require inert, non-reactive storage. Glass, accounting for approximately 63.7% of material usage, remains the preferred choice for preserving oil integrity and preventing contamination. Investment in recycled glass, lightweight formulations, and circular takeback programs is accelerating across the supply chain. These developments are enabling higher realized average selling prices for premium glass containers and advanced dispensing systems, as brands are willing to pay for enhanced sustainability credentials and performance reliability.

Barrier Analysis - Cost Volatility in Energy-Intensive Glass Manufacturing

Glass container production remains highly sensitive to fluctuations in energy and raw material costs. Increases in electricity and natural gas prices directly impact manufacturing margins, often forcing producers to pass cost increases to customers. Smaller aromatherapy brands are particularly vulnerable, as packaging cost inflation can compress margins or delay new product introductions. The fragile nature of glass elevates logistics and freight costs, especially for exports to North America and Europe. A 10-15% rise in energy and freight expenses can increase pack-level costs by approximately 3-6%, affecting pricing strategies for mid-tier brands.

Regulatory Compliance Requirements for Pharmaceutical and Food-Contact Uses

Essential oils positioned for therapeutic or ingestible applications require containers that meet stringent pharmaceutical and food-contact standards. Compliance with Type I glass specifications, validated closures, and tamper-evident systems increases production costs and extends lead times. Smaller producers often lack the technical expertise or financial resources to meet these requirements, limiting their access to regulated distribution channels. This creates a structurally segmented market, with standardized decorative packaging serving general retail applications and higher-cost certified containers reserved for pharmaceutical-grade uses.

Opportunity Analysis - Lightweight and Recycled Glass Paired With Premium Dispensing Systems

Brands transitioning to lightweight or recycled glass containers combined with precision droppers and metered dispensing systems can achieve meaningful packaging value premiums. If even 10-15% of the 2026 market base migrates toward these higher-value formats at a moderate price uplift, this would represent a US$110-170 million incremental annual revenue opportunity by 2028. Container manufacturers that invest in recycled material certification and closure innovation are well-positioned to capture this premium segment.

Growth in Small-Format, Travel, and Sample Packaging

Containers with capacities of up to 5 ml represent the fastest-growing segment, supported by product sampling programs, subscription models, and travel-compliant packaging requirements. Brands are increasingly using micro-formats to drive trial, repeat purchases, and customer lifetime value. Suppliers offering integrated services such as filling, labeling, and quality control for sample kits can capture additional value beyond container manufacturing alone.

Category-wise Analysis

Material Insights

Glass is anticipated to account for approximately 63.7% of the global essential oil containers market in 2026, driven by its chemical inertness, impermeability, and strong alignment with pharmaceutical-grade and therapeutic applications. Amber and cobalt blue glass variants are widely adopted to protect volatile essential oils from UV radiation, oxidation, and contamination, directly supporting longer shelf life and product efficacy.

Major aromatherapy and wellness brands, including those supplying pharmaceutical distribution channels, continue to standardize glass packaging for premium and clinical formulations. Glass also supports advanced finishing techniques such as frosted coatings, embossing, and silk-screen printing, which enhance brand differentiation. Higher average selling prices (ASPs) and repeat procurement contracts reinforce revenue concentration among specialized glass manufacturers and secondary processing providers.

Aluminum is likely to be the fastest-growing material segment, supported by rising demand for lightweight, recyclable, and travel-friendly packaging formats. Aluminum containers are increasingly used in roll-on applicators, spray bottles, and cartridge-based systems for aromatherapy, personal care, and home-fragrance products. For example, portable essential oil blends and refillable fragrance systems increasingly adopt aluminum to reduce breakage risk and logistics costs.

Strong sustainability credentials, including high recycling rates and lower transportation emissions, further accelerate adoption among eco-conscious brands. Aluminum’s compatibility with modern minimalist aesthetics and matte finishes also supports its penetration into premium lifestyle product lines and direct-to-consumer channels.

Product Type Insights

Bottles are estimated to be the dominant product type, accounting for 51.6% of total container volumes, supported by their versatility, dosing precision, and compatibility with a wide range of closures. Dropper bottles, Euro-droppers, and Boston-round formats are widely used across personal care, aromatherapy, and therapeutic wellness segments. Their dominance is reinforced by standardized filling, labeling, and capping infrastructure used by contract manufacturers and small-batch producers alike.

Bottles also support multi-material configurations, such as glass bodies with aluminum or plastic closures, enabling cost optimization without compromising functionality. Broad SKU availability across capacities further strengthens their role as the industry’s primary packaging format.

Jars are emerging as the fastest-growing product type, driven by expanding use in blended oils, balms, infused waxes, and semi-solid wellness formulations. Growth is particularly strong in home-use and premium personal care categories, where wide-mouth access improves usability and product recovery. For example, essential-oil-infused balms and aromatherapy salves increasingly favor glass or aluminum jars for stability and presentation.

Decorative labeling, textured finishes, and reusable packaging concepts further enhance jar adoption in high-value product lines. As brands diversify beyond liquid-only formulations, jars are gaining strategic importance within differentiated product portfolios.

Regional Market Insights

North America Essential Oil Containers Market Trends - Regulation-Driven Premium Glass and Aluminum Adoption

North America is projected to represent the largest regional market, accounting for approximately 32.4% of global value, driven primarily by the strong consumer spending on wellness, aromatherapy, and premium personal care products in the U.S... The U.S. market benefits from a highly developed retail and e-commerce ecosystem, where essential oil brands leverage omnichannel distribution through specialty wellness stores, pharmacies, and direct-to-consumer platforms. Established aromatherapy and wellness brands, along with private-label suppliers serving large retailers, increasingly prioritize high-quality glass and aluminum containers to support premium positioning and regulatory compliance.

Regulatory oversight by agencies such as the U.S. Food and Drug Administration (FDA) and Health Canada reinforces demand for pharmaceutical-grade glass containers, particularly for therapeutic and ingestible oil applications. This regulatory environment has encouraged packaging suppliers to invest in traceability systems, compliance documentation, and high-barrier materials. Investment activity across the region is concentrated in automated filling lines, lightweight glass technologies, and sustainable packaging formats, with several North American packaging manufacturers expanding capabilities in recycled glass content and aluminum roll-on systems. These developments strengthen regional leadership in premium packaging innovation while raising barriers to entry for low-cost imports.

Europe Essential Oil Containers Market Trends - Compliance-Centric, Circular Packaging Leadership

Europe represents a high-value, regulation-driven market, supported by stringent product safety, labeling, and sustainability requirements under EU-wide frameworks such as REACH and the EU Packaging and Packaging Waste Directive. Germany, the U.K., France, and Spain anchor regional demand through well-established cosmetics, fragrance, and wellness industries that emphasize quality, consistency, and environmental responsibility. European essential oil brands and contract manufacturers strongly favor certified glass and aluminum containers, reflecting both regulatory requirements and consumer preferences for sustainability.

The region has seen growing adoption of refillable container systems, lightweight decorative glass, and circular economy-aligned packaging designs, particularly in France and Germany. Leading European packaging suppliers have expanded offerings in reusable glass bottles and mono-material aluminum solutions to align with brand sustainability targets. In the U.K. and France, premium aromatherapy and home-fragrance brands increasingly use customized jars and bottles with embossed branding and water-based coatings to support differentiation without compromising recyclability. Harmonized regulatory standards benefit large, certified suppliers while encouraging consolidation and long-term supplier partnerships across the value chain.

Asia Pacific Essential Oil Containers Market Trends - High-Growth Manufacturing Scale with Rising Wellness Demand

The Asia Pacific is likely to be the fastest-growing regional market, driven by rising disposable incomes, rapid urbanization, and the increasing adoption of wellness and personal care products across emerging economies. China plays a dual role as both a major consumption market and a global manufacturing hub for essential oil containers, benefiting from large-scale glass and aluminum production capacity. Chinese packaging suppliers are increasingly serving export-oriented brands by meeting international quality and compliance standards, thereby reinforcing the region’s manufacturing advantage.

Japan contributes through its focus on precision manufacturing, premium aesthetics, and functional innovation, particularly in small-capacity bottles and roll-on containers designed for personal use. India and ASEAN countries are experiencing rapid growth in direct-to-consumer wellness brands, driven by social commerce and online marketplaces. This shift has increased demand for cost-efficient, scalable, and sustainable container solutions, including lightweight glass bottles and aluminum formats optimized for shipping. Regional investments in automation and localized supply chains are improving quality consistency, enabling Asia Pacific suppliers to compete more effectively in both domestic and export markets.

Competitive Landscape

The global essential oil containers market exhibits a semi-consolidated structure at the premium end, dominated by global glass manufacturers and specialized closure providers, while remaining fragmented at the commodity level. Large players capture a disproportionate share of value through certified, high-margin products, while numerous regional suppliers compete on price and delivery speed.

Recent strategic activity includes expansions of cosmetic and dropper bottle production lines, launches of metered and eco-compatible dispensing systems, and the establishment of regional warehousing and fill-finish partnerships. These initiatives aim to reduce lead times, enhance sustainability credentials, and support fast-growing DTC brands.

Leading companies focus on premiumization, vertical integration, and sustainability leadership. Differentiation is achieved through technical certification, global distribution networks, and turnkey packaging solutions that integrate containers, closures, and filling services.

Key Industry Developments

- In May 2025, Valiant Packaging rolled out UV-protective caps and custom closure options for dropper bottles, screw caps, and spray pumps tailored for essential oil applications, driving a 38% revenue increase within the first six months of launch.

Companies Covered in Essential Oil Containers Market

- Gerresheimer AG

- AptarGroup, Inc.

- Berlin Packaging

- Amcor plc

- Berry Global Group, Inc.

- Piramal Glass Limited

- SGD Pharma

- Vetropack Group

- Ardagh Group

- Stoelzle Glass Group

- Quadpack Industries

- TricorBraun

- HCP Packaging

- Alpha Packaging

- Comar, LLC

- Bormioli Pharma

- Heinz-Glas Group

- Verescence

Frequently Asked Questions

The global essential oil containers market is estimated to be valued at US$5.7 billion in 2026.

By 2033, the essential oil containers market is projected to reach US$9.8 billion.

Key trends include increasing preference for glass containers due to chemical stability, rising adoption of lightweight and recyclable aluminum formats, growth of refillable and reusable packaging systems, and expanding demand for small-capacity containers aligned with travel, sampling, and e-commerce distribution.

Glass is the leading material segment, accounting for approximately 63.7% of the market, supported by its superior barrier properties, regulatory acceptance for therapeutic applications, and strong alignment with premium aromatherapy and pharmaceutical products.

The essential oil containers market is expected to grow at a CAGR of 8.0% between 2026 and 2033.

Major players include Gerresheimer AG, AptarGroup, Inc., Berlin Packaging, Amcor plc, Berry Global Group, Inc.