- Food Packaging

- Food Storage Container Market

Food Storage Container Market Size, Share, and Growth Forecast, 2026 - 2033

Food Storage Container Market by Material (Plastic, Glass, Others), Product Type (Airtight, Rigid, Others), Application, and Regional Analysis for 2026 - 2033

Food Storage Container Market Size and Trends Analysis

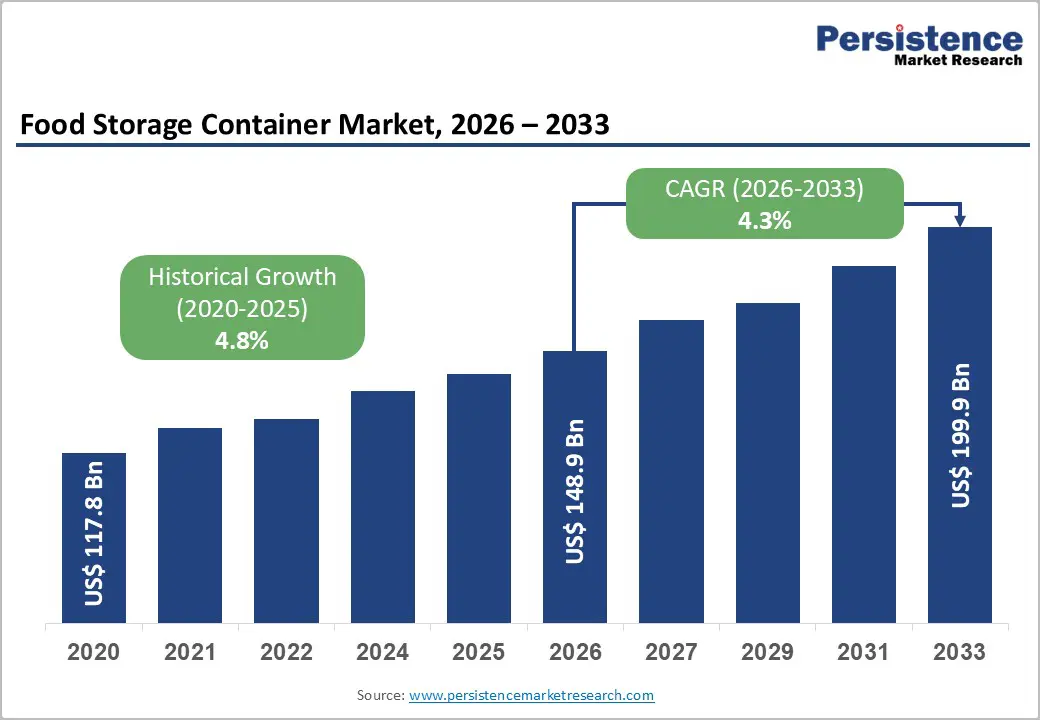

The global food storage container market size is likely to be valued at US$148.9 billion in 2026 and is expected to reach US$199.9 billion by 2033, growing at a CAGR of 4.3% between 2026 and 2033, driven by sustained growth in home meal preparation, increasing consumption of convenience foods, and rising adoption of reusable and sustainable storage solutions.

Product innovation in airtight, insulated, and hybrid-material containers continues to elevate replacement demand and average selling prices. Asia Pacific is witnessing the fastest adoption driven by urbanization and the expansion of organized retail, while manufacturers globally face margin pressure from raw-material price volatility and tightening plastic regulations.

Key Industry Highlights

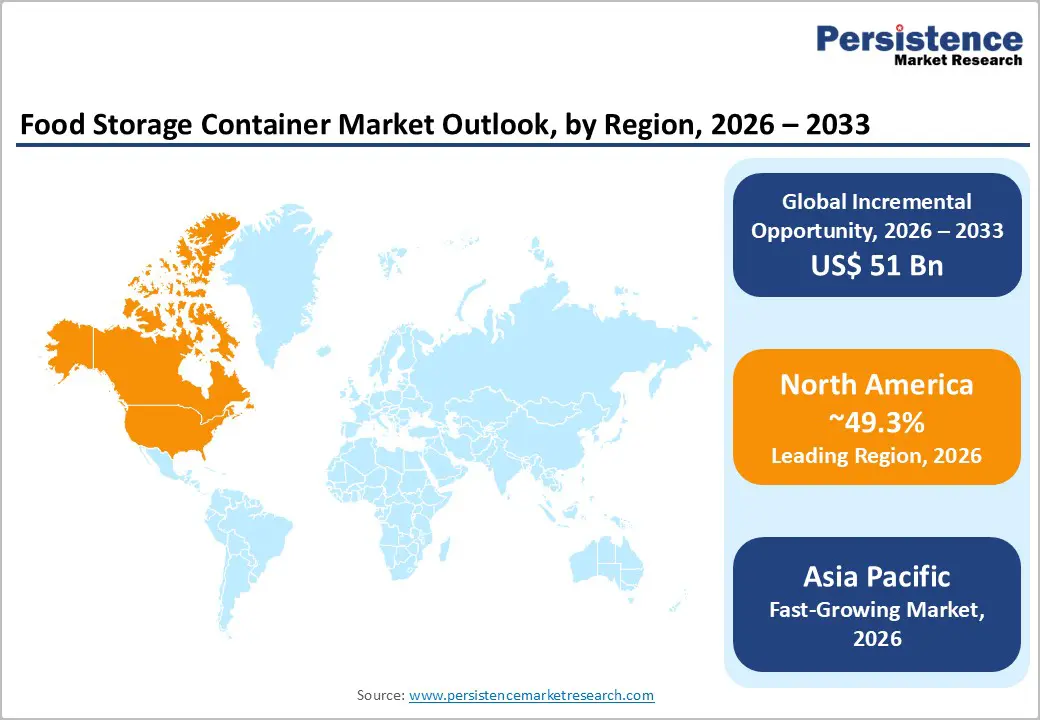

- Leading Region: North America is projected to account for approximately 49.3% of market share in 2026, supported by high per-capita kitchenware spending, strong omnichannel retail penetration, and sustained demand for premium airtight and glass storage containers.

- Fastest-growing Region: Asia Pacific, projected to record the highest regional growth rate through the forecast period, driven by rapid urbanization, expanding middle-class populations, and accelerating e-commerce adoption across China, India, and Southeast Asia.

- Investment Plans: Manufacturers are prioritizing direct-to-consumer platforms, advanced sealing technologies, and supply-chain resilience, with capital allocation increasingly focused on nearshoring in North America and capacity expansion in the Asia Pacific to support both domestic consumption and export demand.

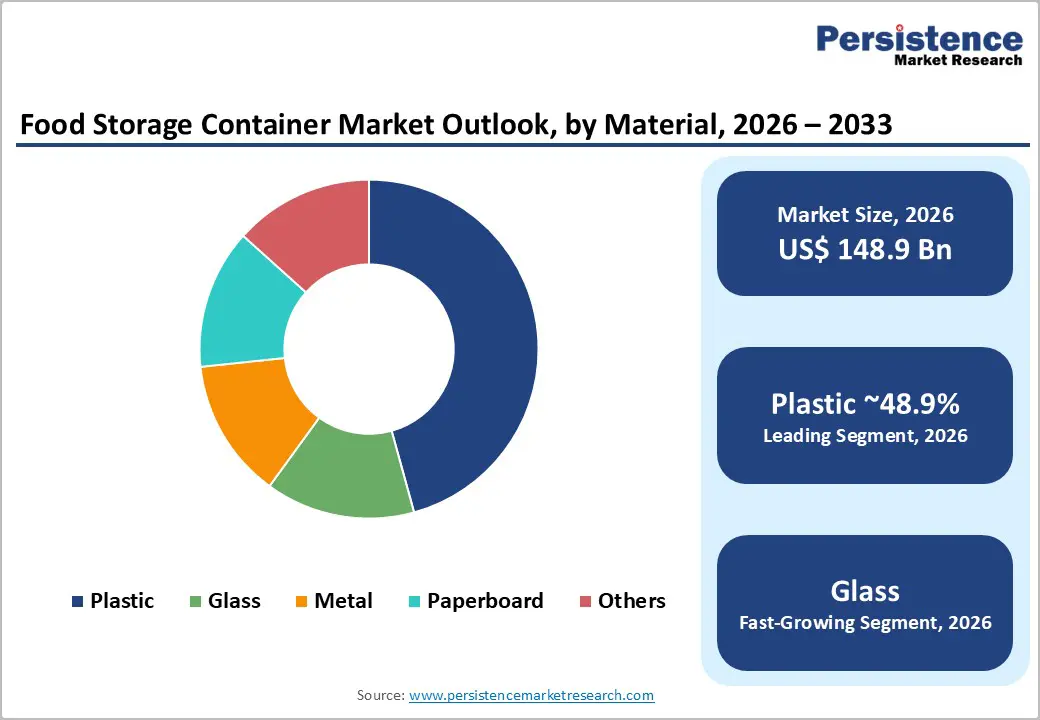

- Dominant Material: Plastic containers are estimated to hold a 48.9% market share due to their cost efficiency, lightweight nature, and broad applicability across mass retail and e-commerce channels.

- Leading Product Type: Airtight containers are expected to account for 43.8% of total market demand, driven by strong consumer preference for leakproof performance, modular compatibility, and long-term food preservation benefits.

| Key Insights | Details |

|---|---|

| Food Storage Container Market Size (2026E) | US$148.9 Bn |

| Market Value Forecast (2033F) | US$199.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Convenience and Changing Food Consumption Patterns

The growing preference for home meal preparation, portion control, and on-the-go consumption has significantly increased demand for airtight, microwave-safe, and freezer-compatible food storage containers. Urban consumers increasingly rely on reusable meal-prep sets and compartmentalized containers to manage busy lifestyles. While ready-to-eat and takeaway channels still rely heavily on single-use packaging, households are shifting toward durable, reusable solutions. This behavioral shift is expanding replacement cycles and encouraging premium purchases. As a result, multifunctional storage systems that support refrigeration, reheating, and transport are gaining traction across both household and commercial segments.

Sustainability and Material Substitution

Environmental concerns and regulatory pressure on single-use plastics are accelerating material substitution across the food storage container market. Consumers increasingly favor glass, metal, and recycled-content plastics due to perceived health, safety, and sustainability benefits. Brands that invest in recyclable materials and transparent lifecycle disclosures are gaining shelf visibility and institutional procurement approvals. Although plastic remains the dominant material by volume, glass and stainless-steel containers are growing faster as consumers accept higher price points for durability and circularity. Regulatory changes at the municipal and national levels are reinforcing this transition and reshaping long-term material demand.

Product Innovation and Functional Advancements

Ongoing innovation in sealing technologies, insulation, and material engineering is expanding the functional scope of food storage containers. Advanced silicone gaskets, multi-latch locking systems, vacuum insulation, and hybrid lids enable leak-proof transport, thermal retention, and multi-environment use. These features support premium pricing and attract consumers seeking versatility and durability. Partnerships between material suppliers and consumer brands have shortened development cycles for patented sealing solutions. Emerging smart features, such as freshness indicators, are also being explored, creating opportunities for accessory sales and post-purchase services.

Barrier Analysis - Raw-Material Price Volatility

Fluctuations in plastic resin and stainless-steel prices continue to challenge profitability, particularly for manufacturers operating in price-sensitive retail segments. Sudden increases in raw-material costs force companies to either absorb margin losses or pass costs to consumers, which can weaken competitiveness. Supply-chain disruptions, including logistics delays and production outages, further exacerbate cost pressures and affect product availability. Historically, volatility in key input materials has resulted in significant margin variability for commodity-focused container manufacturers.

Regulatory Fragmentation and Compliance Costs

Food-contact material regulations vary widely across regions, creating compliance complexity for manufacturers operating globally. Differences in testing, labeling, and material restrictions increase product development costs and extend time-to-market. Smaller manufacturers face disproportionate burdens when entering highly regulated markets, while larger players benefit from scale advantages. Noncompliance risks include product recalls and reputational damage. For regulated premium product lines, compliance requirements can add measurable unit costs, affecting pricing strategies.

Opportunity Analysis - Premium and Insulated Container Segments

Premium food storage containers, including insulated jars and high-performance airtight systems, represent a high-value growth opportunity. These products command average selling prices that are two to four times higher than those of standard plastic containers. Bundled offerings, such as accessory lids and seal replacement subscriptions, further enhance recurring revenue potential and customer lifetime value.

Emerging Markets and Organized Retail Expansion

Rapid urbanization and the expansion of organized retail in the Asia Pacific are creating substantial growth opportunities. Countries such as India and those in Southeast Asia are witnessing increased household spending on kitchen organization products. Entry strategies involving local manufacturing partnerships or joint ventures help reduce logistics costs and improve margins. Capturing even a small share of incremental household adoption in these markets can generate significant revenue for mid-sized manufacturers over the forecast period.

Circular and Service-Based Business Models

Circular business models, including product leasing, lid replacement programs, and take-back initiatives for recycling, are gaining acceptance among environmentally conscious consumers. These services reduce end-of-life friction while strengthening brand loyalty and repeat purchases. Pilot programs in developed markets indicate a willingness to pay for circular solutions when convenience is maintained. Integrating such services into retail and loyalty ecosystems presents a differentiated growth pathway.

Category-wise Analysis

Material Insights

Plastic food storage containers are anticipated to account for approximately 48.9% of market share in 2026, maintaining leadership due to their cost competitiveness, lightweight properties, and high design adaptability. These containers are extensively adopted across both household and commercial kitchens, particularly in price-sensitive and high-volume markets such as the Asia Pacific, Latin America, and parts of the Middle East. Leading manufacturers offer broad plastic portfolios ranging from entry-level polypropylene tubs to engineered airtight containers featuring snap-lock lids, stackable formats, and microwave-safe designs. Plastic’s low production and logistics costs support deep penetration across mass retail chains, grocery outlets, and e-commerce platforms, where affordability and durability drive purchasing decisions. Global brands such as LocknLock, Tupperware Brands, and Rubbermaid continue to rely on plastic as their core revenue material. Tightening single-use plastic regulations, extended producer responsibility (EPR) frameworks, and rising consumer awareness around recyclability are gradually moderating growth in mature markets, prompting manufacturers to increase recycled content and introduce BPA-free and bio-based plastic alternatives.

Glass containers are likely to be the fastest-growing material segment, driven by strong consumer preference for chemical inertness, reusability, and premium aesthetics. Growth is most pronounced in North America and Europe, where health-conscious consumers favor non-reactive materials for food storage, meal prep, and oven-to-table applications. Despite lower shipment volumes compared to plastic, higher average selling prices allow glass containers to contribute disproportionately to overall revenue growth. Manufacturers are investing in tempered, lightweight borosilicate glass paired with silicone-sealed or polymer lids to address traditional concerns around fragility and weight. Brands such as Pyrex, OXO, and Anchor Hocking have expanded their modular glass ranges to be compatible with freezing, reheating, and dishwashing. As sustainability considerations increasingly influence purchasing behavior, glass is gaining traction in premium retail channels and subscription-based kitchenware models, improving its competitiveness beyond niche segments.

Product Type Insights

Airtight containers are expected to account for approximately 43.8% of the market share in 2026, forming the backbone of the food storage container industry. These products are widely preferred for meal preparation, refrigeration, freezer storage, and spill prevention, where reliable sealing performance is critical. Consumer purchasing behavior indicates a strong willingness to pay premium prices for containers that offer leak resistance, odor control, and long-term durability. Airtight containers also serve as the primary platform for innovation, with manufacturers integrating features such as vacuum-sealing valves, modular stacking systems, and interchangeable lid ecosystems. Brands including Sistema, OXO, and IKEA emphasize airtight functionality as a core value proposition across both plastic and glass product lines. Their strong repeat-purchase rates and compatibility with bulk kitchen organization solutions support sustained margin expansion, reinforcing airtight containers as the market’s most commercially resilient product category.

Flexible containers, encompassing resealable pouches, collapsible silicone bowls, and foldable storage formats, are likely to emerge as the fastest-growing product segment. Demand is driven by their ability to address space efficiency, portability, and material reduction, aligning closely with urban lifestyles and sustainability goals. These solutions are increasingly adopted for portion control, on-the-go meals, travel storage, and specialized cooking applications, including sous vide preparation. Flexible containers benefit from lower shipping volumes and flat-pack logistics, making them well-suited to direct-to-consumer and e-commerce sales models. Companies such as Stasher and Lékué have gained traction by positioning flexible containers as reusable alternatives to disposable packaging. While per-unit pricing remains lower than premium rigid containers, accelerating adoption rates and expanding use cases are driving strong volume-led growth, particularly among younger, environmentally conscious consumers.

Regional Insights

North America Food Storage Container Market Trends - Retail Scale, Premiumization, and Regulatory-Driven Reusability

North America is projected to account for approximately 49.3% of market share, with the U.S. as the dominant contributor. High per-capita spending on kitchenware, widespread adoption of organized food storage habits, and a deeply entrenched big-box retail and omnichannel ecosystem underpin sustained demand. Large retailers such as Walmart, Target, Costco, and Amazon provide nationwide distribution for both mass-market and premium brands, enabling rapid product scaling and frequent portfolio refresh cycles. Consumers increasingly favor premium glass, insulated, and airtight containers, driving higher revenue per unit even as volume growth moderates in mature sub-segments.

Regulatory oversight in North America emphasizes food-contact safety, chemical compliance, and labeling transparency, with agencies such as the U.S. Food and Drug Administration (FDA) enforcing standards related to BPA-free plastics and material migration limits. At the state level, restrictions on certain single-use plastics in California, New York, and Washington are influencing product design choices and accelerating the shift toward reusable, durable storage formats rather than disposable alternatives. This regulatory environment has encouraged manufacturers to invest in recycled-content plastics and long-life glass systems. Leading brands, including Tupperware Brands, Rubbermaid (Newell Brands), OXO, and Pyrex, continue to shape market dynamics through innovation in sealing technology, modular storage systems, and freezer-to-microwave compatibility. Investment activity increasingly targets brands with direct-to-consumer capabilities, proprietary lid-locking mechanisms, and data-driven demand forecasting. Nearshoring initiatives in Mexico and the southern U.S. are strengthening supply-chain resilience, reducing lead times, and mitigating exposure to global logistics volatility, reinforcing North America’s position as both a demand and innovation hub.

Europe Food Storage Container Market Trends - Sustainability Regulation and Circular-Economy Product Design

Europe represents a mature yet innovation-driven market, strongly shaped by sustainability priorities, regulatory harmonization, and environmentally conscious consumer behavior. Western European countries, particularly Germany, the U.K., France, and the Nordics, anchor regional demand, supported by high household penetration of reusable food storage products and a strong preference for recyclable, repairable, and long-life materials. Glass, stainless steel, and premium airtight containers are especially prominent in urban households, where food waste reduction and portion planning are key drivers of consumption.

The regulatory environment plays a central role in shaping market structure. Extended Producer Responsibility (EPR) frameworks, packaging waste directives, and eco-design requirements under EU legislation are accelerating material innovation while raising compliance costs for smaller suppliers. These dynamics are contributing to supplier consolidation and favoring established manufacturers with strong compliance infrastructure. European players such as Bormioli Rocco, Luminarc (Arc Group), and EMSA have expanded their portfolios with recyclable glass and modular designs aligned with EU sustainability benchmarks.

Retailers and private-label brands also exert significant influence, with chains such as IKEA, Carrefour, and Tesco promoting reusable storage solutions as part of broader circular-economy commitments. Investment activity increasingly targets premium glass and stainless-steel containers, as well as service-enabled models, including refill, recycling, and take-back initiatives. These trends position Europe as a test bed for regulation-driven innovation, where product differentiation is increasingly defined by environmental performance rather than price competition alone.

Asia Pacific Food Storage Container Market Trends - Urbanization-Led Growth and Manufacturing-Driven Innovation

Asia Pacific is likely to be the fastest-growing regional market, driven by rapid urbanization, rising disposable incomes, changing dietary patterns, and the explosive expansion of e-commerce and quick-commerce platforms. China and India account for substantial volume growth, supported by expanding middle-class populations and increased adoption of organized kitchenware. Japan and South Korea also lead the region in product innovation, particularly in compact, insulated, and space-efficient storage designs suited to smaller urban living environments.

The region benefits from a robust manufacturing base and cost advantages, enabling both large-scale domestic consumption and export-oriented production. Chinese manufacturers supply a significant share of global plastic and glass containers, while Indian firms are expanding capacity to serve both domestic demand and private-label exports to Europe and North America. Brands such as LocknLock (South Korea) have successfully leveraged Asia Pacific as both a production and innovation hub, introducing airtight and vacuum-seal technologies that later scaled globally.

Regulatory standards across Asia Pacific are tightening, particularly in food safety, material traceability, and chemical compliance, driven by export requirements and rising domestic awareness. Governments in China, Japan, and Australia are increasing scrutiny of food-contact materials, favoring manufacturers that invest in certified materials and advanced sealing technologies. Investment momentum remains strong across localized brands, private-label manufacturing, and digitally native players aligned with online retail ecosystems, reinforcing Asia Pacific’s role as the primary engine of global market expansion.

Competitive Landscape

The global food storage container market is semi-consolidated, characterized by a mix of global brand owners and numerous regional manufacturers. Large companies dominate branded segments and major retail channels, while private-label products intensify price competition. Plastic containers lead in volume, whereas glass and metal formats capture higher value shares. Mergers and acquisitions focus on acquiring differentiated designs, premium brands, and regional manufacturing capacity.

Recent strategic activity includes expanded launches of airtight and insulated containers, consolidation within premium glass portfolios, and expansion of manufacturing capacity across Asia to support global supply chains. These developments reflect a focus on innovation, cost optimization, and geographic diversification.

Leading players prioritize product differentiation through sealing and insulation technology, cost leadership in plastic manufacturing, and market expansion via direct-to-consumer and emerging markets. Circular initiatives and accessory ecosystems are increasingly used to strengthen customer retention.

Key Industry Developments

- In April 2025, Caraway introduced a new line of Glass Airtight Storage Containers, focusing on healthier, space-efficient designs that enhance freshness while reducing exposure to microplastics in household kitchens.

- In March 2025, Tupperware launched a new eco-friendly polypropylene container line featuring enhanced airtight sealing optimized for microwave and freezer use, reinforcing sustainability and performance in its core product portfolio.

Companies Covered in Food Storage Container Market

- Tupperware Brands Corporation

- Newell Brands (Rubbermaid)

- LocknLock Co., Ltd.

- IKEA

- Helen of Troy (OXO)

- Sistema Plastics

- Maspion Group

- Glasslock

- World Kitchen LLC (Pyrex)

- Cello World Ltd.

- Hamilton Housewares Pvt. Ltd.

- Meyer Corporation

- Snapware (Pyrex Brand)

- Progressive International

- Inter IKEA Group

- Brabantia

- Joseph Joseph

- Thermos L.L.C.

Frequently Asked Questions

The global food storage container market is estimated to be valued at US$148.9 billion in 2026.

By 2033, the food storage container market is projected to reach US$199.9 billion.

Key trends include a shift toward glass and reusable materials, growing demand for airtight and modular containers, rising popularity of direct-to-consumer brands, and increasing innovation in lightweight, insulated, and space-efficient designs aligned with sustainability and convenience.

By material, plastic containers remain the leading segment with an anticipated 48.9% market share, supported by affordability, lightweight properties, and widespread use across mass retail and foodservice channels.

The food storage container market is expected to grow at a CAGR of 4.3% between 2026 and 2033.

Major companies include Newell Brands (Rubbermaid), Tupperware Brands Corporation, LocknLock Co., Ltd., OXO (Helen of Troy), and IKEA.