- Sensors & Controls

- 3D Sensors Market

3D Sensors Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

3D Sensors Market by Product Type (Image Sensors, Position Sensors, Pressure Sensors, Temperature Sensors, Accelerometer Sensors, Gesture-Recognition Sensors, Others), Technology (Time of Flight (ToF), Structured Light, Stereo Vision, Ultrasound, Millimeter-Wave Radar), Application (Consumer Electronics, Automotive, Others) and Regional Analysis for 2025 - 2032

3D Sensors Market Share and Trends Analysis

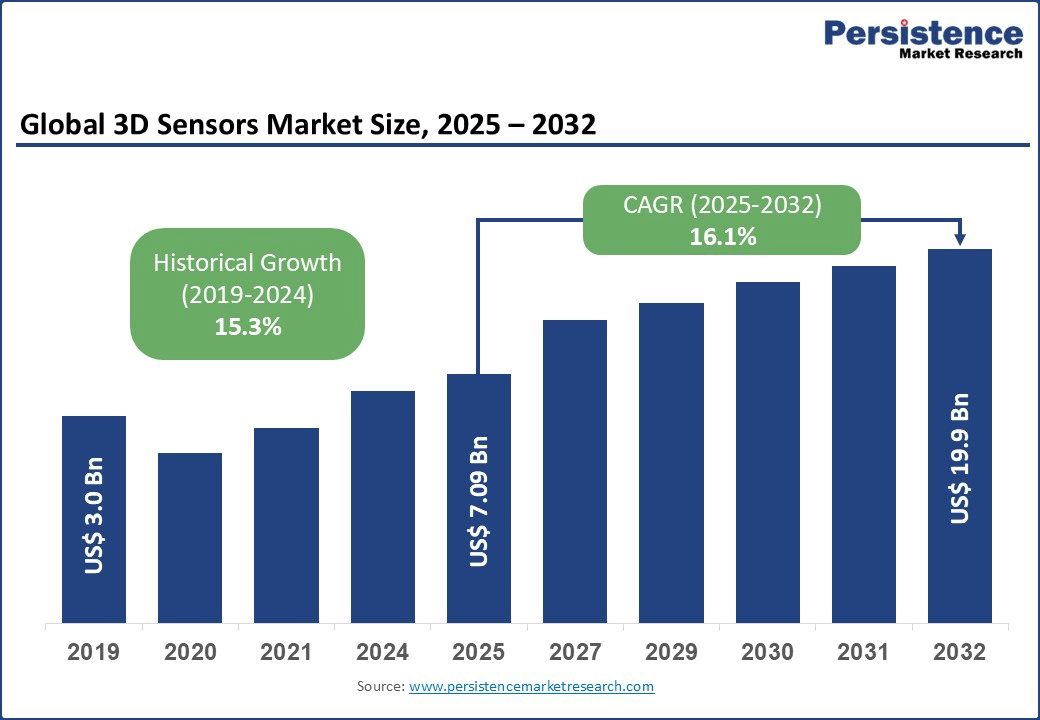

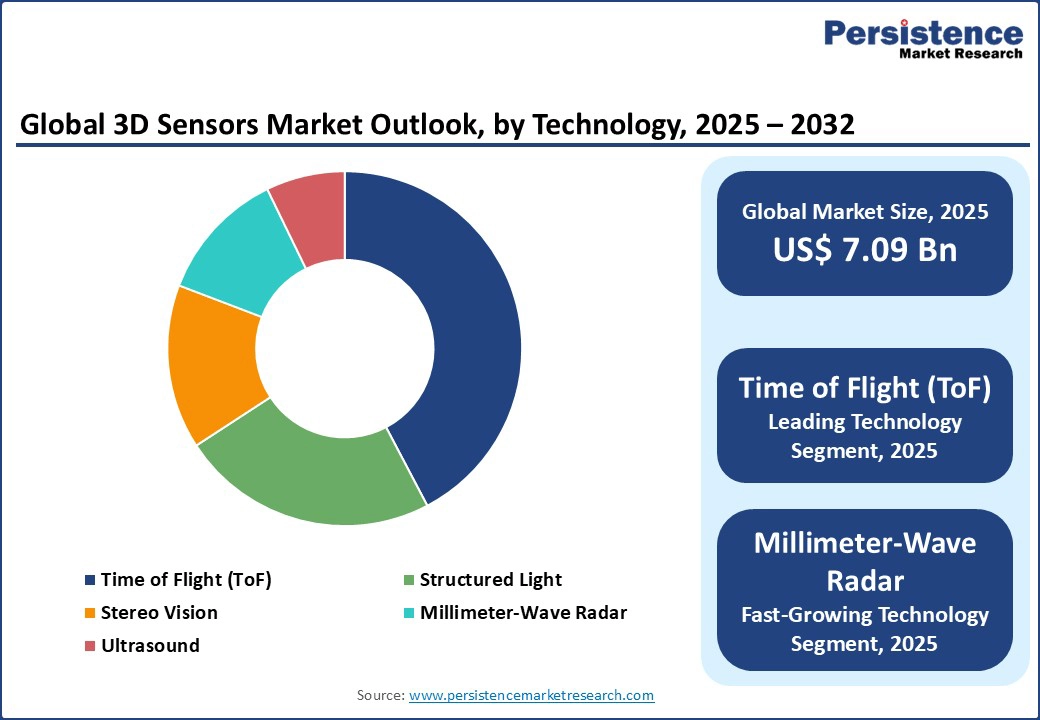

The global 3D sensors market size is likely to be valued at US$ 7.09 Bn in 2025, and is expected to reach US$ 19.9 Bn by 2032, growing at a CAGR of 16.1% during the forecast period 2025 - 2032.

Key Industry Highlights

- Leading Technology: Time of Flight sensors are set lead with about 42.3% market revenue share in 2025 due to their superior real-time 3D depth sensing capabilities and ease of integration in smartphones and autonomous vehicles.

- Fastest-growing Technology Segment: The millimeter-wave radar segment is projected to exhibit the highest CAGR of about 19.0% through 2032 owing to the unique capability of these radars for non-visual, long-range 3D sensing critical in autonomous vehicles and ADAS.

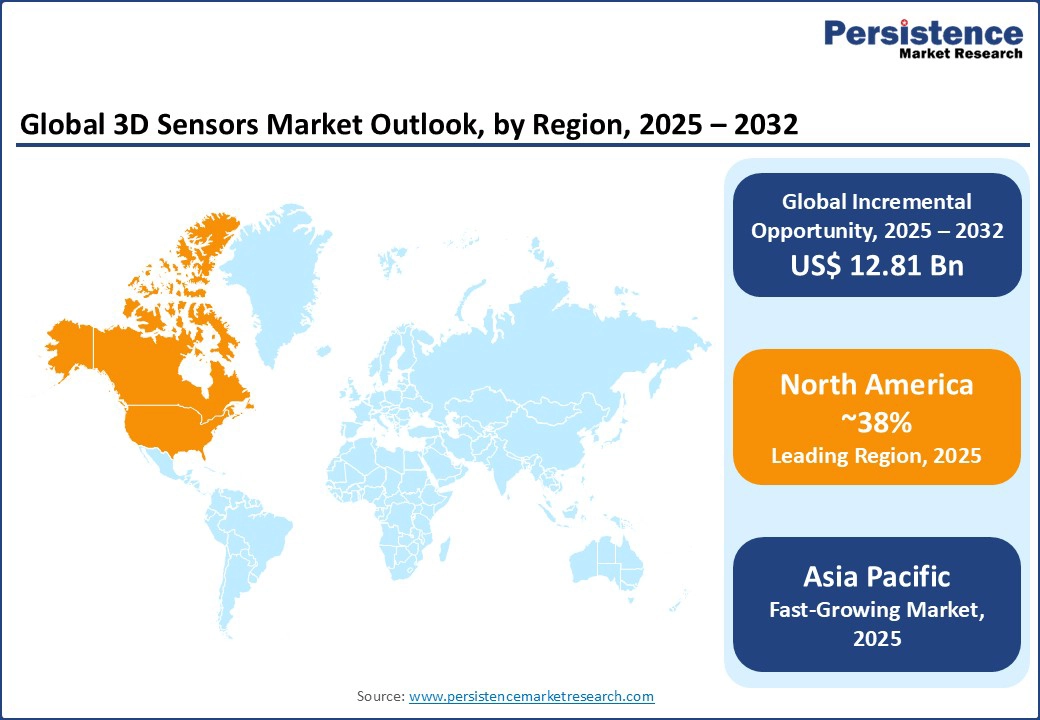

- Dominant Region: North America is expected to hold the largest market share at approximately 38.1% in 2025, fueled by pioneering R&D in and extensive adoption of cutting-edge 3D sensing technologies in aerospace, defense, and advanced automotive safety systems.

- Fastest-growing Regional Market: Asia Pacific is likely to be the fastest-growing regional market with a CAGR of nearly 17.0% from 2025 to 2032, spurred by China's dominance in the manufacturing of consumer electronics and electric vehicles (EVs), with support from increasing smart city initiatives.

- Notable Development: In July 2025, Infineon Technologies launched the third generation of its XENSIV™ 3D magnetic Hall-effect sensor family, designed under ISO 26262 with integrated diagnostics for ASIL-B functional safety, ideal for automotive, industrial, and consumer uses.

| Global Market Attribute | Key Insights |

|---|---|

| 3D Sensors Market Size (2025E) | US$ 7.09 Bn |

| Market Value Forecast (2032F) | US$ 19.9 Bn |

| Projected Growth (CAGR 2025 to 2032) | 16.1% |

| Historical Market Growth (CAGR 2019 to 2024) | 15.3% |

The convergence of artificial intelligence (AI) and Internet of Things (IoT) opens up numerous application areas for 3D imaging sensors across a wide spectrum of industries spanning healthcare, autonomous vehicles, logistics, and consumer electronics, among others, fueling the market over the next several years.

Market Dynamics

Driver - Emergence of Autonomous Mobility and Evolving Vehicle Safety Regulations to Catalyze Market Development

Spearheading the progress of the 3D sensors market is the increasing incorporation of ADAS by automakers and the corresponding intensification of stringent vehicle safety regulations worldwide, which collectively necessitate high-precision spatial sensing technologies.

With governments around the globe enforcing rigorous safety mandates, such as the General Safety Regulation of the European Union (EU) requiring autonomous emergency braking and pedestrian detection in all new vehicles by 2025, the integration of sophisticated 3D sensors such as stereo vision, has become indispensable. Such mandates are pushing auto companies and vehicle security specialists to develop and introduce novel products into the market.

For instance, in June 2025, the German sensor and safety expert SICK launched the multiScan100-S, the industry’s first component-level safety-certified 3D LiDAR sensor tailored for rugged outdoor environments, such as container terminals, offering a 360-degree scanning field up to 62 meters and an IP69K enclosure for harsh conditions.

As is evident, the combined pressures of strict regulations and a growing inclination toward autonomous mobility are accelerating advancements in miniaturized, AI-powered 3D sensor modules optimized for diverse, real-world applications.

Restraint - Lack of Industry Standardization to be a Major Hindrance

The lack of unified industry standards governing hardware specifications, communication protocols, and data formats challenges industry growth. The absence of standardization creates integration complexities and interoperability challenges across different sensor technologies such as ToF and structured light, thereby delaying widespread adoption of these sensors.

Manufacturers face significant hurdles in developing components compatible with diverse application ecosystems, ranging from automotive ADAS suites to consumer electronics and industrial automation, leading to increased costs and prolonged product development cycles.

For example, the coexistence of multiple competing standards, such as VCSEL, SPAD, and CMOS means that companies must invest heavily in adapting their sensor designs to fit various platforms, limiting economies of scale and slowing innovation diffusion. For system integrators, the struggle lies in the seamless data fusion from multi-vendor sensors, which is critical for applications such as smart manufacturing, where real-time precise 3D environmental mapping is essential.

Fusion of Sensor Technologies with AI to Unlock Untapped Frontiers

A compelling opportunity that 3D sensors market players can tap into is the arming of sensor technologies with the power of AI, which promises to revolutionize data accuracy, contextual awareness, and application versatility across industries. By combining inputs from multiple 3D sensor modalities with advanced machine learning algorithms, companies can deliver unprecedented precision in depth mapping, object recognition, and environmental modeling.

For example, in autonomous vehicles, AI-enhanced sensor fusion synergizes LiDAR data with ToF and stereo vision inputs to produce highly reliable 3D environmental reconstructions indispensable for real-time navigation and safety-critical decision-making. This convergence facilitates diversification into niche but rapidly growing sectors, including industrial automation robotics, smart healthcare diagnostics, and augmented reality-based retail experiences.

In June 2025, Caltech engineers developed PillTrek, a miniature ingestible smart capsule equipped with a wireless electrochemical workstation and powered by inexpensive, low-power sensors that continuously monitor gut health in real-time by measuring pH, temperature, and biomarkers such as glucose, serotonin, metabolites, and ions. Newer applications in smart city infrastructure, such as intelligent traffic monitoring and precision agriculture using 3D spatial analytics, also highlight the limitless possibilities of AI-powered 3D sensing.

Category-wise Analysis

Technology Insights

Within the technology category, the dominant segment is time of flight, which is expected to hold approximately 42.3% of the 3D sensors market revenue share, due to its ability to deliver fast, accurate depth sensing across consumer electronics and automotive applications.

ToF sensors are prized for their compact design and real-time 3D data capture, enabling applications such as facial recognition, gesture control, and augmented reality in smartphones and gaming devices. The primary factor bolstering the dominance is the ability of ToF for efficient range detection in both indoor and outdoor environments.

Major players such as STMicroelectronics and Infineon Technologies are leading innovation in compact ToF modules for emerging AR glasses and autonomous robotics, driving industry momentum. For example, in February 2025, Infineon supplied a ToF sensor that enables Roborock's Saros Z70 to become the first vacuum cleaner equipped with a robotic cleaning arm, bringing advanced object recognition and manipulation to autonomous home cleaning devices.

The millimeter-wave radar segment, in contrast, is projected to exhibit a strong CAGR of about 19.0% through 2032. This technology is gaining unprecedented traction owing to its unique capability for non-visual, long-range 3D sensing critical in autonomous vehicles and ADAS. Regulatory frameworks mandating advanced safety features, alongside its robustness in adverse weather and lighting conditions where optical sensors may falter, are the main growth stimulants for millimeter-wave radars.

Product Type Insights

Image sensors are likely to lead this market in 2025 with an estimated 38.6% revenue share. The apex position of this segment is majorly attributable to the widespread adoption of advanced image sensors that are capable of capturing depth and spatial data alongside traditional 2D images, facilitating critical functionalities such as facial recognition, gesture control, and AR for diverse applications.

Recent improvements in pixel density and light sensitivity have enabled imaging sensors to perform reliably in low-light and dynamic environments, boosting their adoption across consumer electronics, automotive, and industrial automation sectors.

The miniaturization of these sensors, coupled with enhanced computational imaging techniques, has set a foundation for immersive digital experiences, boosting market growth. High-profile products incorporating back-illuminated stacked CMOS architectures, such as the April 2025 launch of the OV50X ultra-high dynamic range image sensor for smartphones by OmniVision, underscore the focus on expanding dynamic range and reducing power consumption, solidifying image sensors as the backbone of most 3D sensing systems.

Gesture-recognition sensors are predicted to showcase a staggering 26.2% CAGR during 2025 - 2032 on account of the increasing demand in public and private spaces to minimize direct physical contact, a trend augmented by post-pandemic hygiene awareness. Gesture-recognition sensors leverage 3D sensing to enable intuitive, contactless user interfaces across retail, healthcare, automotive infotainment, and smart home applications.

Advancements in AI-driven pattern recognition and machine learning algorithms have elevated their accuracy, contextual understanding, and adaptability, enabling seamless human-machine interaction. The expansion of smart cities and IoT ecosystems is also propelling this segment as gesture control becomes integral to user experience design in public kiosks, smart appliances, and augmented reality systems.

Regional Insights

North America 3D Sensors Market Trends

North America holds around 38.1% of the 3D sensors market share as of 2025, the largest among regions, primarily boosted by the widespread adoption of advanced sensor technologies across automotive, aerospace & defense, healthcare, and industrial automation sectors.

Bolstering the leadership of the region are the pioneering R&D investments and a robust venture capital ecosystem, especially in LiDAR and ToF sensor technologies crucial for ADAS and autonomous vehicles. Notably, tier 1 automotive suppliers in the U.S. are advancing chip-scale beam steering and multisensor fusion, positioning North America at the forefront of next-gen 3D perception technologies.

For example, in January 2025, Sony Honda Mobility unveiled the AFEELA 1 at CES 2025, offering advanced software-driven features such as ADAS, OTA upgrades, personalized in-cabin entertainment, and a natural-voice “Personal Agent” to redefine intelligent mobility. The ongoing emphasis on high-precision spatial sensing for defense applications and healthcare imaging is set to further fuel the demand for 3D sensors in the region.

Asia Pacific 3D Sensors Market Trends

Asia Pacific is the fastest-growing regional market for 3D sensors from 2025 to 2032, slated to enjoy a CAGR of approximately 17.0% fueled by rapid industrial digitization, growing adoption of smart technologies, and booming consumer electronics manufacturing.

China dominates within APAC, buoyed by strong penetration in smartphone facial recognition and AR-enabled devices. South Korea and Japan are also playing an instrumental role on the back of their advanced semiconductor fabs and robotics industries, aiding cutting-edge sensor manufacturing and integration into automated industrial systems.

Government initiatives to promote smart cities, Industry 4.0, and digital infrastructure are also likely to amplify 3D sensor adoption across a range of sectors such as healthcare, smart retail, and logistics. Cost-competitive production coupled with increasing local R&D investments and soaring EV sales in the region has built a robust foundation for the diffusion of next-gen innovations.

Europe 3D Sensors Market Trends

The market in Europe is projected to make significant gains over the forecast period 2025 - 2032 owing to the massive demand for automotive safety technologies and expanding industrial automation.

The adoption of ADAS, mandated across the EU bloc, is fueling the growth of ToF and millimeter-wave radar sensors in passenger vehicles to enhance pedestrian detection and collision avoidance. In parallel, European automotive original equipment manufacturers (OEMs) and component suppliers are investing heavily in embedded 3D sensing to meet rigorous EU safety regulations.

Industrial robotics and factory automation are also key verticals, leveraging 3D sensors for precise object detection and machine vision. Sustainability trends and smart manufacturing initiatives under the Industry 5.0 framework will provide unparalleled support for the deployment of advanced sensors for energy efficiency and quality control.

Competitive Landscape

Chief among the factors shaping the global 3D sensors market landscape revolves around unrelenting technological innovation, strategic partnerships, and dynamic expansion across diverse end-use sectors. Leading players are fiercely investing in R&D to pioneer miniaturized, AI-powered, and energy-efficient 3D sensing solutions that integrate Time of Flight, structured light, and LiDAR technologies, spurred by and growing demand in automotive ADAS, consumer electronics, healthcare diagnostics, and industrial automation.

The surge in autonomous vehicles and smart manufacturing initiatives has fostered an intense competition for sensor accuracy, resolution, and real-time processing capabilities. Consolidation through mergers & acquisitions, as illustrated by Qualcomm's acquisition of Veoneer’s LiDAR business in 2022 to strengthen its 3D perception capabilities, and ecosystem collaboration, such as joint ventures between sensor manufacturers and AI firms to integrate edge computing, are becoming major industry trends.

Key Industry Developments:

- In July 2025, VoxelSensors teamed up with Qualcomm to integrate its innovative single-photon active event sensor (SPAES™) into Snapdragon XR platforms, delivering dramatically improved depth sensing for robotics and XR, with up to tenfold power savings, lower latency, and strong performance in challenging lighting. This collaboration aims to enable more efficient, user-centric “Physical AI” experiences and pave the way for lightweight, all-day wearable AR devices.

- In July 2025, Sparsh CCTV, Innoviz Technologies, and Cron AI entered into a strategic partnership to deliver a unified LiDAR-camera-vision perception platform, designed for edge-native deployment across India's intelligent transportation systems, perimeter security, railways, and critical infrastructure, leveraging real-time, on-device processing without cloud dependency. Backed by strong local reach, this collaboration targets a combined addressable market exceeding US$1 Bn across rapidly growing ITS and perimeter-security sectors.

- In June 2025, STMicroelectronics rolled out its fifth-generation Human Presence Detection (HPD) solution, integrating a FlightSense ToF sensor with embedded AI algorithms. The solution delivers features such as adaptive screen dimming, hands-free Windows Hello login, multi-person detection, head orientation tracking, and gesture/hand posture recognition while reducing daily power consumption by over 20% and preserving user privacy by avoiding image capture.

Companies Covered in 3D Sensors Market

- Infineon Technologies AG

- Texas Instruments Incorporated

- Qualcomm Technologies, Inc.

- STMicroelectronics N.V.

- OmniVision Technologies, Inc.

- LMI Technologies Inc.

- ifm electronic GmbH

- Keyence Corporation

- Cognex Corporation

- Microchip Technology Inc.

Frequently Asked Questions

The global 3D sensors market is projected to reach US$ 7.09 Bn in 2025.

The increasing incorporation of ADAS by automakers and the corresponding intensification of stringent vehicle safety regulations worldwide are driving the market.

The market is poised to witness a CAGR of 16.1% from 2025 to 2032.

The integration of sensor technologies with AI and machine learning and the growing applicability of 3D sensors in smart city infrastructure are key market opportunities.

Infineon Technologies AG, Texas Instruments Incorporated, and Qualcomm Technologies, Inc. are some of the key players.