ID: PMRREP19105| 198 Pages | 29 Nov 2025 | Format: PDF, Excel, PPT* | Industrial Automation

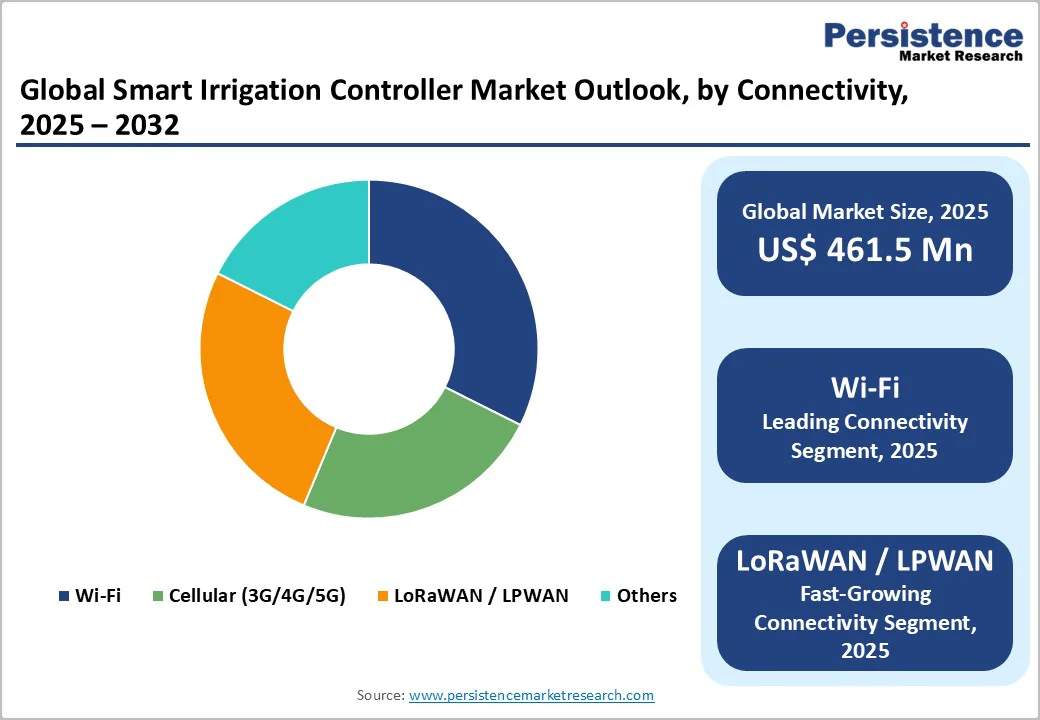

The global Smart Irrigation Controller Market size is valued at US$461.5 million in 2025 and is projected to reach US$1,205.3 million by 2032, growing at a CAGR of 14.7% between 2025 and 2032. This robust expansion is driven by escalating global water scarcity concerns, with over 40% of the global population facing water stress, and agriculture consuming approximately 70% of freshwater withdrawals. The market's growth trajectory reflects the urgent need for water-efficient technologies as agricultural water scarcity is expected to increase in more than 80% of the world's croplands by 2050. Government initiatives promoting water conservation, including rebate programs covering 50-100% of smart controller installation costs in water-stressed regions, coupled with rapid advancements in IoT connectivity and decreasing sensor costs, are accelerating adoption across agricultural and non-agricultural applications.

Drivers - Rise in Global Water Scarcity and Conservation Imperatives

Global water scarcity has emerged as the primary catalyst driving smart irrigation controller adoption, with agricultural irrigation accounting for approximately 70% of freshwater withdrawals worldwide. More than 25% of global agriculture is currently grown in areas experiencing high water stress, with this figure doubling for irrigated cropland, which produces 40% of the global food supply. The World Resources Institute reports that 60% of irrigated crops face high to extremely high water stress levels, creating unprecedented pressure to optimize water usage. Smart irrigation controllers address this critical challenge by automatically adjusting irrigation schedules based on real-time environmental data, achieving water consumption reductions of 15-30% compared to conventional systems and up to 50% when integrated with AI algorithms. By 2025, an estimated 1.8 billion people are expected to be living in regions with absolute water scarcity, making water-efficient irrigation technologies essential for agricultural sustainability and food security. The alignment of smart irrigation technology with global sustainable development goals, combined with growing public awareness of water conservation benefits, has created a favorable regulatory and social environment, accelerating market expansion across both developed and emerging markets.

Government Initiatives and Regulatory Mandates Promoting Water Efficiency

Government policies and financial incentives are significantly accelerating smart irrigation controller adoption worldwide, with municipalities and water districts implementing comprehensive rebate programs and regulatory mandates. California's permanent landscape budgeting rules and WaterSense programs mandate water-efficient system installation, with rebate programs offering $25-$60 per station for smart controllers and some programs covering up to 50-100% of installation costs. The San Diego County Water Authority's LEAVES program provides enhanced rebates of $60 per station alongside flow sensors ($120 each) and master valves ($500 each) as part of comprehensive water conservation initiatives. The U.S. Environmental Protection Agency is channeling $50 billion toward modern water infrastructure, including smart irrigation upgrades, while the European Union's Common Agricultural Policy for 2023-2027 allocates €387 billion with significant emphasis on sustainable water management and precision agriculture technologies. India's government plans to invest approximately $650 million for precision farming adoption using IoT, AI, and smart irrigation technologies, while China's Ministry of Agriculture champions sensor-based irrigation trials and digital agriculture initiatives under the 14th Five-Year Plan.

Restraints - High Initial Investment Costs and Economic Barriers

The high upfront costs of smart irrigation controller systems are the biggest barrier to adoption, especially for small and medium-sized farmers on limited budgets. Entry-level systems start around $530, with additional monthly fees, while medium-sized installations average about $10,000 in 2023. This significant initial investment, covering equipment and installation, poses a financial risk for farmers unsure of their return on investment. Economic barriers also include system integration, ongoing maintenance, and potential infrastructure upgrades. Many farmers, operating on thin profit margins, hesitate to invest due to perceived risks and uncertain financial returns, despite the long-term savings these systems offer. Access to financing options like grants or low-interest loans is uneven, further limiting adoption among resource-limited operations.

Connectivity Challenges and Technical Complexity in Rural Areas

Connectivity issues are a major barrier to smart irrigation adoption, as these systems depend on stable internet connections for IoT functionality and real-time data transmission. Rural areas often struggle with inadequate coverage, with around 19 million Americans lacking access to high-speed internet, according to the FCC. A South African study found that only 46% of smallholder farmers adopted climate-smart irrigation, largely due to limited internet access. Additionally, the technical complexity of setting up and operating these systems can be overwhelming for farmers used to manual irrigation, especially where training and support are scarce. Many farmers also worry about compatibility issues with traditional equipment, further discouraging adoption. This digital divide may worsen inequalities, leaving vulnerable populations without access to essential resilience-enhancing technologies.

Opportunities - Integration with Smart City Infrastructure and Municipal Water Management

The growing development of smart city initiatives worldwide presents substantial expansion opportunities for smart irrigation controller integration into municipal water management systems. Urban areas are increasingly adopting IoT-based infrastructure for public space management, including parks, sports fields, golf courses, and green spaces, creating significant demand for centralized irrigation control. Smart irrigation systems can integrate with city-wide water management platforms, enabling centralized monitoring and control of public irrigation needs across multiple facilities while responding dynamically to water restrictions. Germany's Smart Cities Pilot Projects, funded with 750 million Euros for urban digitization including water management systems, exemplify the substantial investment flowing into municipal smart infrastructure.

Emerging Technologies and Market Innovation Opportunities

Advanced technology integration, including artificial intelligence, machine learning, and LPWAN connectivity, represents significant market expansion opportunities with transformative potential. The LPWAN for the agriculture market is projected to reach $6.8 billion by 2032, driven by increasing adoption of smart agricultural practices demanding robust, cost-effective, and energy-efficient connectivity solutions for monitoring and automation across vast rural landscapes. LoRaWAN technology's long-range, low-power capabilities make it particularly suitable for agricultural applications, with devices transmitting data across substantial distances while operating for years on single batteries.

Product Type Insights

Weather-based Irrigation Controllers dominate the smart irrigation controller market with a commanding 54% market share in 2025, reflecting their widespread adoption across residential, commercial, and agricultural applications. These controllers utilize evapotranspiration data incorporating temperature, humidity, solar radiation, and weather forecasts to automatically adjust irrigation schedules, providing optimal water application without manual intervention.

Soil Moisture-based controllers represent the fastest-growing segment with a projected CAGR of 15.6%, fueled by their precision in monitoring soil moisture levels and plant water requirements, offering granular irrigation management. The soil moisture sensor-driven irrigation AI market is rapidly expanding due to the need for efficient water management and the rise of smart farming. These controllers offer real-time soil monitoring, allowing irrigation only when needed, which can reduce water use by 20-50% based on crop and conditions. Government programs, like the USDA's Environmental Quality Incentives Program, are incentivizing farmers to adopt these advanced technologies, particularly in precision agriculture.

Connectivity Insights

Wi-Fi connectivity leads the smart irrigation controller market with 32% market share in 2025, reflecting its widespread availability, ease of integration with existing home and commercial networks, and compatibility with smart home ecosystems, including Amazon Alexa and Google Home. Wi-Fi-enabled controllers provide reliable real-time data transmission, remote access capabilities, and seamless integration with cloud-based management platforms, making them the preferred choice for residential and commercial landscape applications. The technology's ubiquity in urban and suburban areas, coupled with user familiarity and established infrastructure, drives its market dominance despite connectivity limitations in some rural agricultural settings.

LoRaWAN/LPWAN connectivity emerges as the fastest-growing segment with an impressive CAGR of 17.7%, driven by its unique advantages for agricultural applications requiring long-range, low-power wireless communication across vast rural landscapes. LoRaWAN technology enables data transmission across substantial distances while consuming minimal battery power, with devices operating for years on single batteries, making it ideal for remote agricultural monitoring where frequent maintenance is challenging. This connectivity solution addresses critical rural coverage limitations while offering cost-effective deployment for large-scale farming operations, with governments and private technology companies partnering to build agricultural IoT ecosystems powered by LPWAN.

Power Source Insights

Solar-powered controllers dominate the power source segment with 43% share in 2025, reflecting growing emphasis on sustainable agriculture practices and renewable energy adoption, combined with decreasing solar panel costs, making these systems increasingly cost-effective. The solar-powered smart irrigation controller market is growing at a CAGR of 17%, driven by the convergence of sustainable energy adoption and increasing demand for precision agriculture solutions. These controllers eliminate dependence on traditional energy sources, reduce carbon emissions, and enable off-grid irrigation management, particularly valuable for remote farms where grid electricity access is limited or unreliable. Government initiatives promoting renewable energy adoption in agriculture, coupled with falling solar technology costs and advancements in pump efficiency, are making solar irrigation increasingly accessible to farmers worldwide.

Battery-powered controllers demonstrate robust growth with a considerable CAGR of 14.5%, driven by their flexibility, portability, and suitability for temporary or small-scale irrigation applications where permanent power infrastructure is impractical. Advanced battery-saving technologies enable DC controllers to remain offline while continuously managing field-based irrigation activities, maintaining logs, and generating water use reports without constant power consumption. The segment benefits from innovations in low-power consumption technologies and extended battery life, with LoRaWAN-enabled sensors offering years of operation on single batteries, making them increasingly attractive for cost-conscious users.

Application Insights

Non-Agricultural applications hold the largest market share at around 51% in 2025, driven by widespread adoption in residential landscapes, commercial facilities, and sports grounds. The non-agriculture segment dominated North America’s smart irrigation market with ~60% share in 2024, attributed to smart home technology proliferation and urban landscaping trends. Within non-agricultural applications, Residential Landscapes demonstrate rapid expansion as homeowners increasingly adopt smart irrigation for water bill savings and improved landscape quality, with smaller, more affordable systems and DIY installation kits lowering entry barriers.

Sports Grounds and Golf Courses show particularly strong growth, with precision irrigation adoption rates reaching around 67% for individual head control systems in United States golf courses, driven by the need to reduce water use while improving playability and turfgrass aesthetics. Smart irrigation systems for golf courses can reduce water consumption while maintaining excellent playing conditions, with automated controllers using real-time soil moisture and weather data for optimal turf management.

Agricultural Fields and Greenhouses represent the fastest-growing segment with a CAGR of 15.9% in 2025, driven by agriculture's position as the largest water consumer globally and the sector's urgent need for water-efficient technologies amid increasing scarcity. In 2024, the Asia Pacific agriculture application segment saw significant growth due to the region's dependence on agriculture for food security and rural livelihoods. Government-led micro-irrigation programs in India and China are widespread. Smart greenhouse systems with IoT technologies allow real-time monitoring and can reduce water usage by 30-50% compared to traditional methods. China's Ministry of Agriculture reports over 800,000 acres of farmland using AI-based irrigation platforms, while India’s agritech startups promote sensor-as-a-service models for smallholder farmers.

North America Smart Irrigation Controller Market Trends

North America holds a prominent market share of 26% in the global smart irrigation controller market, with the region growing at a CAGR of 15.6% through 2033. The United States dominates the regional market, accounting for a substantial portion of North American revenue, driven by stringent state-level water conservation laws, including California's Title 23 and permanent landscape budgeting rules mandating water-efficient system installation. The region's leadership stems from high adoption of IoT-enabled precision agriculture, broad integration with smart home ecosystems, including Amazon Alexa and Google Home, and significant funding from the USDA's Natural Resources Conservation Service (NRCS) for drip and smart irrigation systems. California's WaterSense program and municipal rebate programs offering $25-$60 per station create strong economic incentives, accelerating residential and commercial adoption.

The regional market benefits from technological innovation leadership, with U.S.-based manufacturers including The Toro Company, Rain Bird Corporation, and Hunter Industries driving product development and market penetration. Approximately 28 million homes across the United States have in-ground sprinkler systems, representing a substantial conversion opportunity for smart controller adoption. U.S. commercial farms and golf courses commonly deploy cloud-connected irrigation systems linked with satellite weather data and soil analytics, reducing water usage by over 30%. The prevalence of droughts in western states has accelerated adoption, with NOAA reporting prolonged dry spells between 2012 and 2021 creating urgent demand for water-efficient irrigation solutions.

Europe Smart Irrigation Controller Market Trends

Europe maintains a considerable market share of 23% in the global smart irrigation controller market and is experiencing robust growth at a CAGR of 11.3%, driven by stringent environmental regulations and government incentives promoting water conservation aligned with EU sustainability mandates. The European smart irrigation market growth is reflecting accelerated technology adoption across the continent. The EU's Water Framework Directive enforces efficient water use, spurring market expansion particularly in Mediterranean countries facing recurring droughts and acute water stress. Spain, Italy, France, and Greece have adopted smart irrigation extensively to combat water shortages in Mediterranean agriculture, with emphasis on soil health and biodiversity, aligning with the EU Green Deal.

Germany demonstrates strong market leadership within Europe, benefiting from engineering precision emphasis, sustainability focus, and substantial smart city investment. France's wine industry represents a key adoption segment, with viticulture increasingly incorporating subsurface drip irrigation and precision controllers to maintain quality while conserving water. The Greater Cambridge program in the UK aims for a 20% reduction in municipal water demand by 2038 through smart irrigation and urban water management. The EU's Common Agricultural Policy for 2023-2027 allocates €387 billion, focusing on sustainable water management and precision agriculture. Cross-border pilot programs involving academic institutions and agritech firms, especially in the Mediterranean corridor, are supporting regional growth, with Dutch greenhouse clusters enhancing sensor density for predictive crop steering.

Asia Pacific Smart Irrigation Controller Market Trends

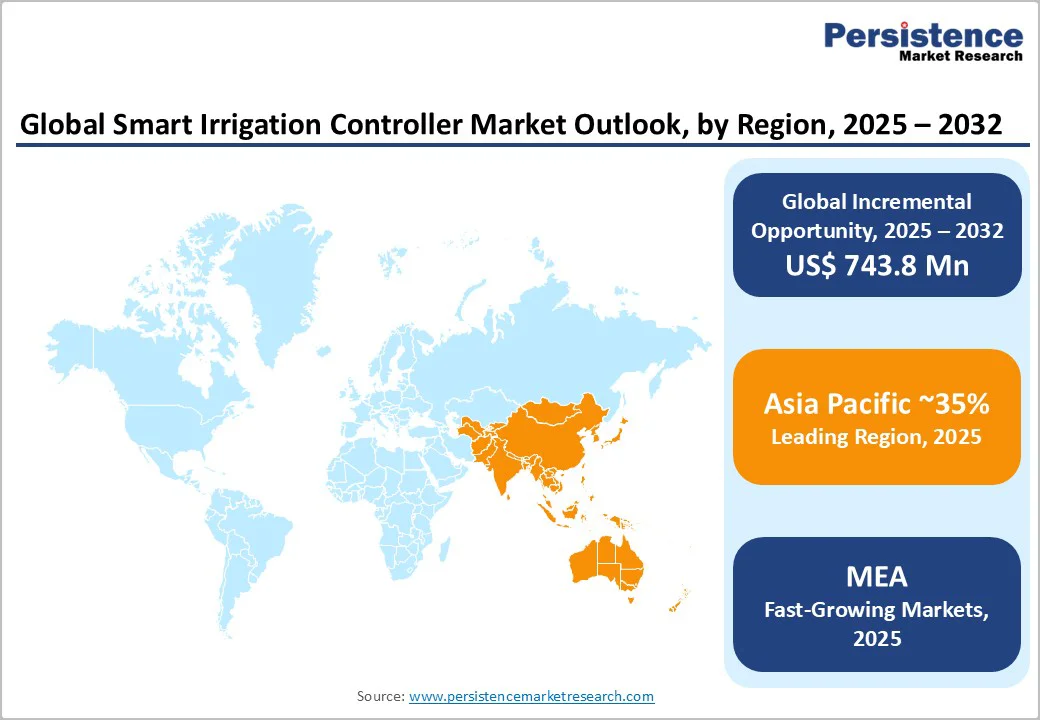

Asia Pacific represents the dominating region with the largest market share of 35% and demonstrates the highest growth rate with a CAGR of 17.8%, positioning it as the fastest-expanding regional market globally. The region's smart irrigation market growth driven by extensive agricultural lands, shifting climate patterns, government initiatives to reduce water waste, and high population density, combined with declining water levels. China maintains the leading position within Asia Pacific, driven by an aggressive push toward digital agriculture and large-scale mechanization under the 14th Five-Year Plan, prioritizing smart irrigation as part of its strategy to achieve food security and sustainable resource management. The Chinese government's "Digital Agriculture and Rural Areas Development Plan" integrates smart irrigation with drone-based crop monitoring and AI analytics to optimize resource use, with the Ministry of Agriculture reporting more than 800,000 acres monitored using wireless soil sensors integrated with AI platforms.

India holds an 18.4% regional market share in 2024, influenced by its vast agricultural base and strong policy backing for water-efficient technologies, with government plans to invest approximately $650 million for precision farming adoption using IoT, AI, and smart irrigation technologies. The growth of agritech startups is crucial for adoption, with funding in India reaching $350 million in 2023, over 40% of which is for sensor-based irrigation and monitoring. NABARD suggests that precision agriculture could boost Indian farmers' incomes by 15-20% while reducing water use by nearly 30%. In 2024, weather-based controllers dominated the Asia Pacific market with 42.5% of business value, while sensors accounted for 35.3%, essential for real-time monitoring of irrigation schedules.

The smart irrigation controller market remains moderately consolidated, led by established global manufacturers supported by extensive portfolios, mature distribution networks, and strong brand recognition. Netafim and other major players maintain leadership through advanced technologies, while diverse innovators such as Rachio, HydroPoint, Weathermatic, and Galcon strengthen the competitive landscape. New entrants and agritech startups increasingly differentiate through IoT-driven platforms, subscription models, and specialized applications across global and regional market environments.

The global smart irrigation controller market is valued at US$461.5 million in 2025 and is projected to reach US$1,205.3 billion by 2032.

The Smart Irrigation Controller Market is driven by increasing global water scarcity, as agriculture uses 70% of freshwater, along with government rebates for water-efficient technologies and advancements in IoT, sensors, and AI for precise water management.

The Smart Irrigation Controller Market is expected to grow at a CAGR of 14.7% between 2025 and 2032.

Key market opportunities include integration with smart city infrastructure, municipal water management systems, agricultural technology, and emerging technologies like LPWAN connectivity and solar-powered controllers for cost-effective off-grid irrigation, especially in developing markets.

The key players in the global Smart Irrigation Controller Market include Rain Bird Corporation, The Toro Company, Hunter Industries, Netafim, HydroPoint Data Systems, and Rachio Inc.

|

Report Attribute |

Details |

|

Historical Data/Actuals |

2019 – 2024 |

|

Forecast Period |

2025 – 2032 |

|

Market Analysis Units |

Value: US$ Mn, Volume: Tons |

|

Geographical Coverage |

|

|

Segmental Coverage |

|

|

Competitive Analysis |

|

|

Report Highlights |

|

By Product Type

By Connectivity

By Power Source

By Application

By Region

Delivery Timelines

For more information on this report and its delivery timelines please get in touch with our sales team.

About Author