- Nutraceuticals & Functional Foods

- Sports Nutrition Ingredients Market

Sports Nutrition Ingredients Market Size, Share, and Growth Forecast, 2025 - 2032

Sports Nutrition Ingredients Market By Ingredient Type (Protein, Probiotics, Specialty Amino Acids), Product Type (Dietary Supplements, Functional Sports & Hydration Beverages), Application, and Regional Analysis for 2025 - 2032

Sports Nutrition Ingredients Market Size and Trends Analysis

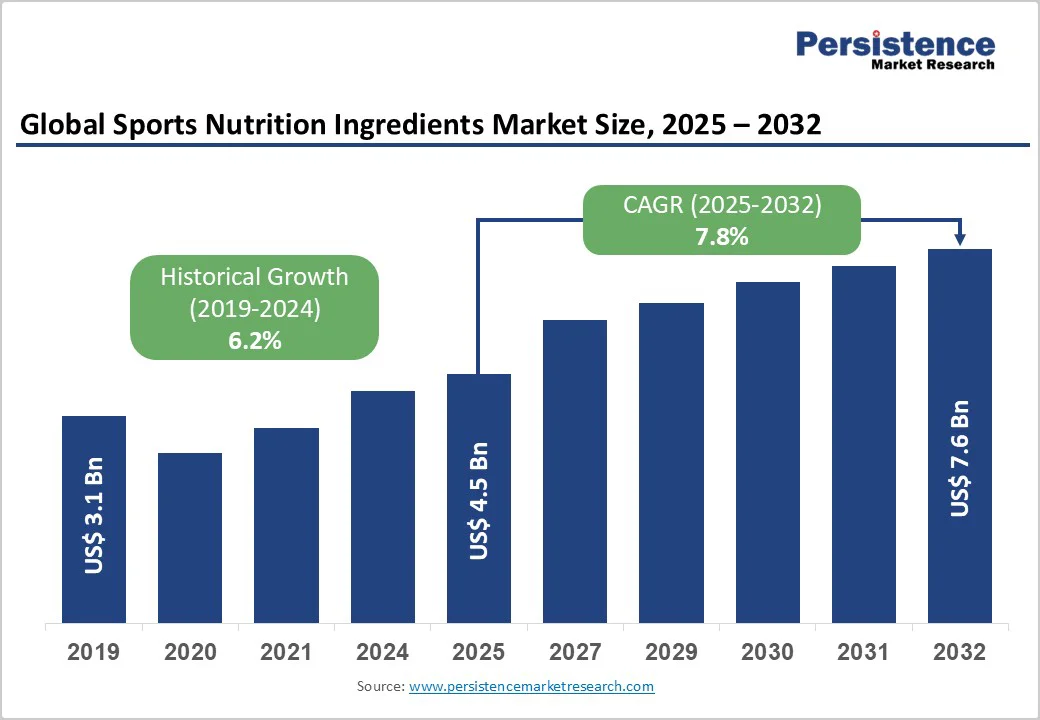

The global sports nutrition ingredients market size is likely to be valued at US$4.5 Billion in 2025 and is expected to reach US$7.6 Billion by 2032, growing at a CAGR of 7.8% during the forecast period from 2025 to 2032, driven by rising participation in fitness and active lifestyles, increasing consumer demand for protein and functional ingredients, and expanded e-commerce and retail distribution channels.

Clean-label and plant-based proteins, probiotic and recovery-focused formulations, and fortified hydration ingredients are key trends shaping demand, while innovations and emerging markets provide significant growth opportunities.

Key Industry Highlights

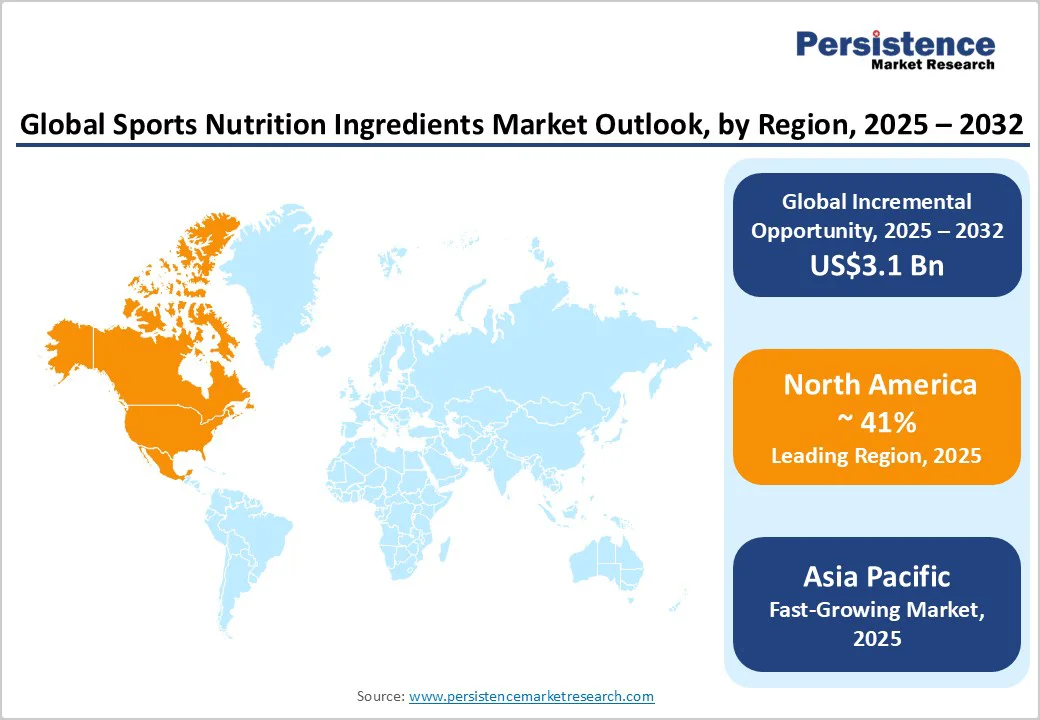

- Leading Region: North America accounts for approximately 41% of the revenue share in 2025, driven by high per-capita spend, mature retail and e-commerce channels, and strong R&D infrastructure in the U.S.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, with a double-digit CAGR projected through 2032, supported by rising disposable incomes, an urban fitness culture, and the increasing adoption of functional beverages and protein supplements in China, India, Japan, and ASEAN markets.

- Investment Plans: Key industry investments include the expansion of plant-based protein production, whey protein processing capacity, and co-development partnerships. Companies are investing in local manufacturing, functional beverage innovation, and premium plant-based formulations to meet regional demand and accelerate go-to-market timelines.

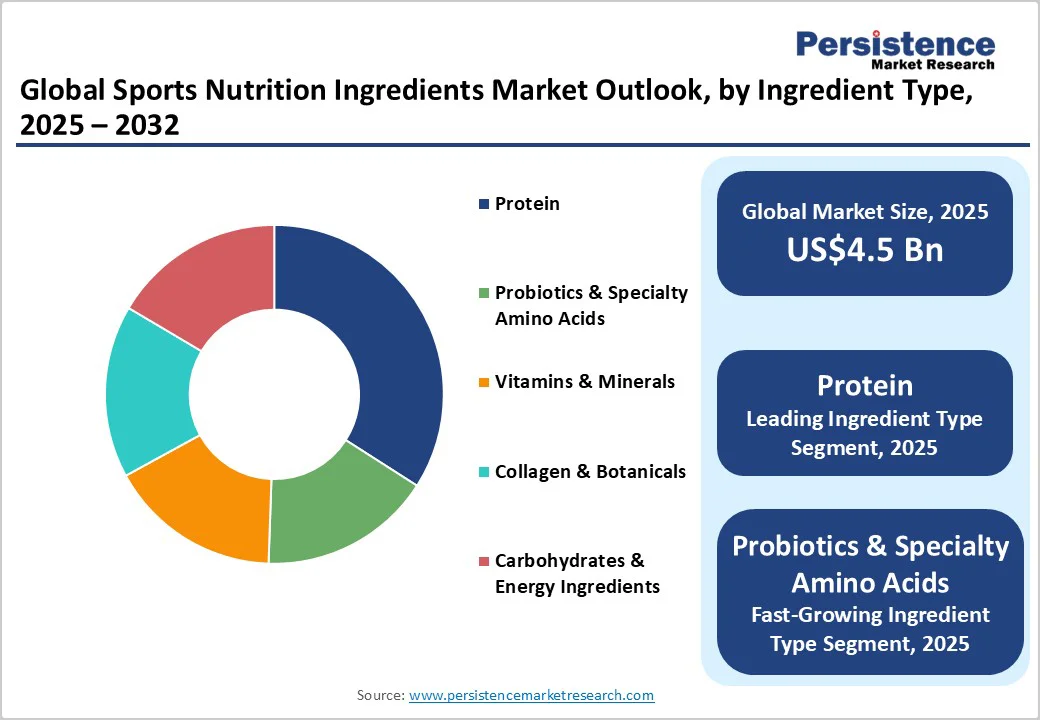

- Dominant Ingredient Type: Protein remains the largest ingredient segment, contributing approximately 31% of ingredient revenue in 2025, primarily through whey, casein, and plant isolates used in powders, RTDs, and bars.

- Leading Product Type: Dietary Supplements dominate in revenue, including powders, capsules, and tablets, supported by mature retail penetration and high-value formulations such as protein concentrates and amino acid blends.

| Key Insights | Details |

|---|---|

| Sports Nutrition Ingredients Market Size (2025E) | US$4.5 Bn |

| Market Value Forecast (2032F) | US$7.6 Bn |

| Projected Growth (CAGR 2025 to 2032) | 7.8% |

| Historical Market Growth (CAGR 2019 to 2024) | 6.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Mainstreaming of Active Lifestyles and Demographic Expansion

Demand for sports nutrition ingredients is expanding beyond professional athletes to everyday fitness enthusiasts and older adults focused on functional wellness. The sector’s CAGR of approximately 7.8% reflects adoption into mass retail and online channels.

This broadening consumer base increases volume for core ingredients such as whey, plant proteins, and amino acids, while supporting premium offerings such as hydrolysates and bioactive peptides, which command higher prices.

Ingredient Innovation in Plant Proteins, Biotech Peptides, and Microbiome-Targeted Ingredients

Research and development have introduced plant-based protein isolates, specialty amino acids, peptides identified via computational methods, and probiotic strains that enhance recovery and gut health. Protein remains the largest revenue contributor at 28% of ingredient sales, while probiotics and functional amino acids are growing at approximately 8% CAGR. Innovation drives higher margins and expands use across powders, beverages, and bars.

Expanding Channels and Direct-to-Consumer Strategies

Digital platforms have accelerated product discovery and adoption of specialty ingredients. E-commerce enables younger consumers to access niche products, increasing average order values for protein powders and recovery stacks. Subscription models and online sales also enhance customer lifetime value. Brands benefit from faster time-to-market for new formulations and rapid scaling of successful SKUs.

Barrier Analysis - Regulatory Complexity around Claims and Labeling

Health claims are closely monitored in major markets. In the U.S., structure/function claims require substantiation and FDA notification, while Europe mandates EFSA authorization. Compliance increases time-to-market and costs for clinical substantiation, especially for recovery and immune-support claims. Regulatory requirements can add 0.5-2% to launch budgets and delay commercialization by months or longer.

Supply Chain and Raw-Material Volatility

Specialty proteins, marine omega-3s, and botanicals face price and availability risks due to agricultural yields, logistics costs, and trade fluctuations. Supply constraints increase inventory costs and may force formulation adjustments. Price swings of 10-30% during supply disruptions directly affect margins, particularly for premium, traceable ingredients.

Opportunity Analysis - Emerging Markets and Targeted Segments

Asia Pacific markets, including India, China, and ASEAN nations, are expected to outpace mature regions, driven by rising disposable incomes and gym culture. There is a notable opportunity in products formulated for women and older adults, including micronutrient-fortified recovery blends and collagen-rich formulas. Early estimates indicate a multi-hundred-million-dollar growth potential in APAC by 2030.

Clean-Label, Plant-Based Proteins, and Sustainable Sourcing

Consumers increasingly prefer clean-label and sustainably sourced ingredients. Plant proteins and traceable supply chains improve revenue share and margins. High-bioavailability plant proteins, such as pea and fava, can command 25-35% premium pricing over commodity blends, offering significant profit opportunities for ingredient suppliers and formulators who invest in sustainability and transparency.

Category-wise Analysis

Ingredient Type insights

Protein ingredients, including whey, casein, soy, and emerging plant isolates such as pea, fava, and rice protein, account for approximately 31% of ingredient revenue in 2025. Whey proteins remain dominant due to their high biological value and efficacy in muscle recovery and body composition.

Protein ingredients are heavily utilized in powders, ready-to-drink beverages, and nutrition bars. Premium protein offerings, such as hydrolyzed whey and native whey, are increasingly adopted in clinical and professional sports applications. Rising demand for plant-based proteins is reshaping the category, with vegan and allergen-free formulations gaining traction among lifestyle users and younger demographics.

Probiotics, prebiotics, and targeted amino acids such as HMB, leucine, and glutamine are projected to grow at a CAGR of 8-8.5% through 2032. Growth is driven by research highlighting gut-health modulation, recovery optimization, and immune support benefits.

Cross-category fortification, adding probiotics and amino acids to RTDs, bars, and protein shakes, is accelerating adoption. Ingredient suppliers are increasingly developing strain-specific probiotics for recovery, cognitive support, and anti-fatigue benefits, opening new revenue streams in functional beverages and ready-to-eat nutrition products.

Product Type Insights

Dietary supplements, including powders, capsules, and tablets, continue to hold the largest share in the market. Mature retail penetration and established brand loyalty contribute to high-value formulations. Protein concentrates and amino acids remain the primary demand drivers.

Recent trends include sugar-reduced formulations, flavor innovation, and multi-functional blends that combine performance, recovery, and wellness benefits. Specialty formulations targeting women, older adults, and endurance athletes are also expanding the supplement portfolio. Retail channels and online subscription models further enhance visibility and repeat purchases.

Ready-to-drink (RTD) performance beverages and fortified hydration products are experiencing the fastest growth due to convenience and formulation innovation. Innovations such as enhanced solubility, shelf-stable proteins, electrolytes, and low-calorie formulations appeal to time-conscious consumers.

Functional beverages targeting energy, focus, and immune support are increasingly incorporated into lifestyle routines. E-commerce and convenience store channels are driving impulse and trial purchases. Collaborations between ingredient suppliers and beverage manufacturers for co-formulation are also accelerating product launches globally.

Application Insights

Professional and semi-professional athletes continue to be the largest revenue contributors, consuming high-protein and clinically dosed supplements to support muscle hypertrophy, recovery, and endurance. Institutional channels such as sports teams, gyms, and specialty retailers are key distribution points.

Product innovation focuses on efficacy-backed formulations, high-quality protein sources, and performance-focused blends. Competitive athletes often prefer formulations with verified bioavailability and minimal additives, ensuring maximum efficacy and compliance with anti-doping regulations.

Recreational fitness enthusiasts and lifestyle consumers represent the fastest-growing segment. These consumers adopt lower-cost, convenient formats such as RTDs, nutrition bars, and blended powders. Growth is primarily volume-driven, while margins are slightly lower per unit.

Brands are increasingly focusing on multi-functional formulations, combining protein, amino acids, vitamins, and botanicals, to appeal to wellness-conscious users. Social media influence, mobile fitness apps, and influencer-driven marketing campaigns are key drivers of adoption in this segment.

Regional Insights

North America Sports Nutrition Ingredients Market Trends

North America remains the largest regional market, accounting for approximately 41% of the market share for the sports nutrition ingredients market. The U.S. is the dominant contributor, supported by its mature retail infrastructure, strong e-commerce penetration, and high consumer awareness of fitness and wellness trends.

In 2025, North America is projected to account for nearly 40 percent of the global sports nutrition ingredient revenue, reflecting widespread institutional adoption as well as growing lifestyle consumption.

Key growth drivers in the region include aging populations focused on muscle retention, the rise of functional wellness trends, increasing gym memberships, and heightened engagement with digital fitness platforms. Ready-to-drink products and ready-to-eat supplements have surged in popularity, bolstered by the expansion of e-commerce channels and subscription-based purchasing models.

From a regulatory perspective, the U.S. Food and Drug Administration requires substantiation for structure and function claims. Although this increases compliance costs, it provides predictable regulatory pathways for product development. Recent updates to labeling standards have emphasized greater transparency in allergen disclosure, nutrient content, and ingredient traceability to enhance consumer confidence.

Recent developments include Nestlé Health Science launching a plant-based protein ready-to-drink line in 2024 aimed at active lifestyle consumers. In 2025, Arla Foods Ingredients expanded its whey protein production capacity in the U.S. to meet rising demand for premium dairy-based ingredients. DuPont introduced a new line of clinically backed probiotics designed for recovery-focused beverages targeting the mass-market fitness segment.

Europe Sports Nutrition Ingredients Market Trends

Europe demonstrates steady growth in the sports nutrition ingredient market, with Germany, the U.K., France, and Spain leading the regional demand. European consumers prioritize clean-label, natural, and sustainably sourced ingredients, with dietary supplements currently dominating the market. Functional beverages, driven by urban lifestyle trends and convenience-driven consumption, are emerging rapidly.

Growth is fueled by rising gym memberships, a growing health-conscious urban population, an aging demographic, and increased awareness of the benefits of sports nutrition beyond professional athletes. Functional hydration and recovery formulations are gaining traction, particularly among recreational fitness users.

The regulatory environment is governed by the European Food Safety Authority, which requires scientific substantiation and approval for health and nutrition claims. While this framework ensures consumer trust, it can slow the introduction of claim-specific products. To address this, brands are investing in clinical trials to secure pan-European approvals for claims related to performance, recovery, and gut health.

Recent developments in 2024 include BASF launching plant-based protein solutions across Europe with a focus on clean-label formulations for ready-to-drink products and bars. ADM strengthened its European plant-based protein portfolio through the acquisition of a specialty pea protein supplier in Germany. In 2025, DSM expanded vitamin and amino acid premix production in the U.K. to support the growing sports nutrition segment.

Asia Pacific Sports Nutrition Ingredients Market Trends

Asia Pacific is the fastest-growing region globally in the sports nutrition ingredients market, led by China, India, Japan, and ASEAN countries. Growth is driven by rising disposable incomes, an expanding urban fitness culture, and the emergence of local brands. In 2025, Asia Pacific is expected to account for nearly 30 percent of the global ingredient demand, with China and India experiencing double-digit compound annual growth rates.

Key growth drivers include rapid urbanization, increasing health awareness, higher gym penetration, and government campaigns promoting physical fitness. Protein powders, functional ready-to-drink beverages, and recovery-focused supplements are rapidly gaining popularity among both younger and middle-aged populations.

Regulatory frameworks vary significantly across the region. China mandates ingredient approvals for functional health foods, India is evolving its standards for nutraceuticals and dietary supplements, and Japan has a well-established Foods for Specified Health Uses program governing health claims. Companies must tailor their labeling, formulation, and clinical substantiation to meet the requirements of each market.

Recent developments include Cargill expanding pea protein production in China in 2024 to meet growing local demand for plant-based sports nutrition products. Ingredion launched plant-based protein blends in India in 2025, targeting the functional beverage and supplement segments. In 2025, Arla Foods Ingredients partnered with an ASEAN beverage manufacturer to supply whey proteins for ready-to-drink products and bars, improving regional supply chain efficiency.

Competitive Landscape

The global sports nutrition ingredients market is moderately consolidated, led by major players such as BASF, DuPont/IFS, Cargill, ADM, Arla Foods Ingredients, and DSM, leveraging scale, R&D, and global networks. Mid-tier and regional firms compete through niche innovation, clean-label, and plant-based offerings.

Mergers, acquisitions, and partnerships expand geographic presence and technological capabilities, as seen with Arla Foods Ingredients and ADM targeting protein isolates and plant-based formulations. Collaboration with beverage brands drives premium product development. Key differentiators include science-backed claims, sustainability focus, and co-creation with brands, while emerging trends highlight direct-to-consumer strategies and the rise of premium plant-based products.

Key Industry Developments

- In May 2025, IMCD acquired TECOM Ingredients by completing the purchase of the specialty ingredients distributor. The move expanded IMCD’s formulary reach in health and food ingredients and strengthened its distribution channel for sports nutrition component suppliers, enabling faster market access for novel ingredients.

- In March 2025, DuPont launched a clinically backed probiotic strain line targeted at recovery-focused products for active lifestyle consumers. The launch emphasized immune and gut health benefits, diversifying DuPont’s offerings beyond traditional protein and amino acid ingredients while tapping into the fast-growing probiotic and multifunctional segment.

Companies Covered in Sports Nutrition Ingredients Market

- Glanbia plc

- Kerry Group plc

- Arla Foods Ingredients Group P/S

- DSM-Firmenich AG

- ADM (Archer Daniels Midland Company)

- Cargill, Incorporated

- FrieslandCampina Ingredients

- BASF SE

- Lonza Group AG

- Nestlé Health Science

- Tate & Lyle PLC

- IFF (International Flavors & Fragrances Inc.)

- Hilmar Ingredients

- Saputo Inc.

- Fonterra Co-operative Group Limited

- Essentia Protein Solutions

- Ingredion Incorporated

- Carbery Group

- Lactalis Ingredients

- Novozymes A/S

Frequently Asked Questions

The sports nutrition ingredients market size is estimated at US$4.5 Billion in 2025.

The market is projected to reach US$7.6 Billion by 2032, driven by expanding consumer adoption of functional proteins, probiotics, and fortified beverages.

Key trends include the rise of plant-based proteins, growth of functional hydration and RTDs, increasing focus on gut health via probiotics and prebiotics, and sustainability-driven sourcing across Europe and North America.

By ingredient type, protein (whey, casein, soy, and pea) remains the leading segment, holding around 31% of ingredient revenue in 2025.

The sports nutrition ingredients market is expected to expand at a CAGR of 7.8% between 2025 and 2032.

Major companies in the sports nutrition ingredients market include Arla Foods Ingredients, Glanbia Nutritionals, ADM, Kerry Group, and FrieslandCampina Ingredients.