- Medical Devices

- Single Lead ECG Machines Market

Single Lead ECG Machines Market Size, Trends, Share, Growth, and Regional Forecast, 2026 to 2033

Single Lead ECG Machines Market by Product (Recording Based Single-lead ECG Monitors, Real-time Single-lead ECG Monitors), Application (Atrial Fibrillation, Bradycardia, Tachycardia, Conduction Disorders, Others), End-user, and Regional Analysis from 2026 to 2033

Single Lead ECG Machines Market Share and Trends Analysis

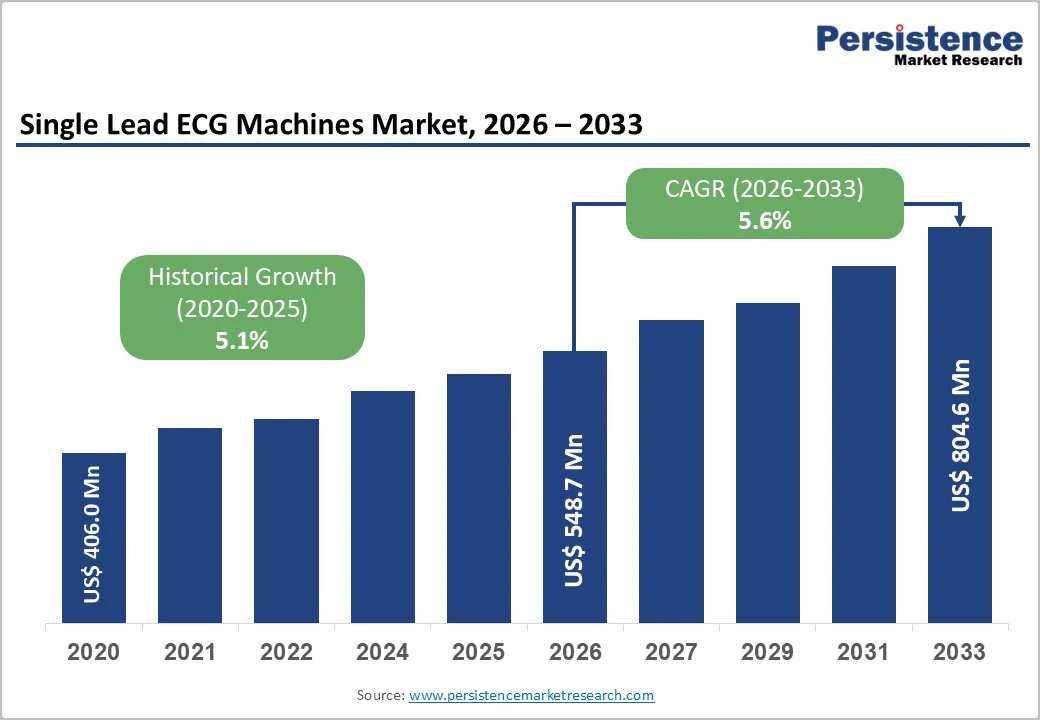

The global single lead ECG machines market size is estimated to reach US$ 548.7 million in 2026 and is projected to reach US$ 804.6 million by 2033, growing at a CAGR of 5.6% between 2026 and 2033. The global market is expanding steadily as healthcare systems adopt portable and cost-efficient cardiac monitoring solutions.

These devices record the heart’s electrical activity using a single lead and provide essential rhythm insights for rapid assessments and early detection of abnormalities. Their compact design, ease of use, and minimal training requirements have made them highly valuable in primary care, emergency settings, home monitoring, and remote diagnostics. As demand grows for accessible, point-of-care cardiac screening, single-lead ECG machines continue to play a vital role in widening preventive and frontline cardiovascular care.

Key Industry Highlights

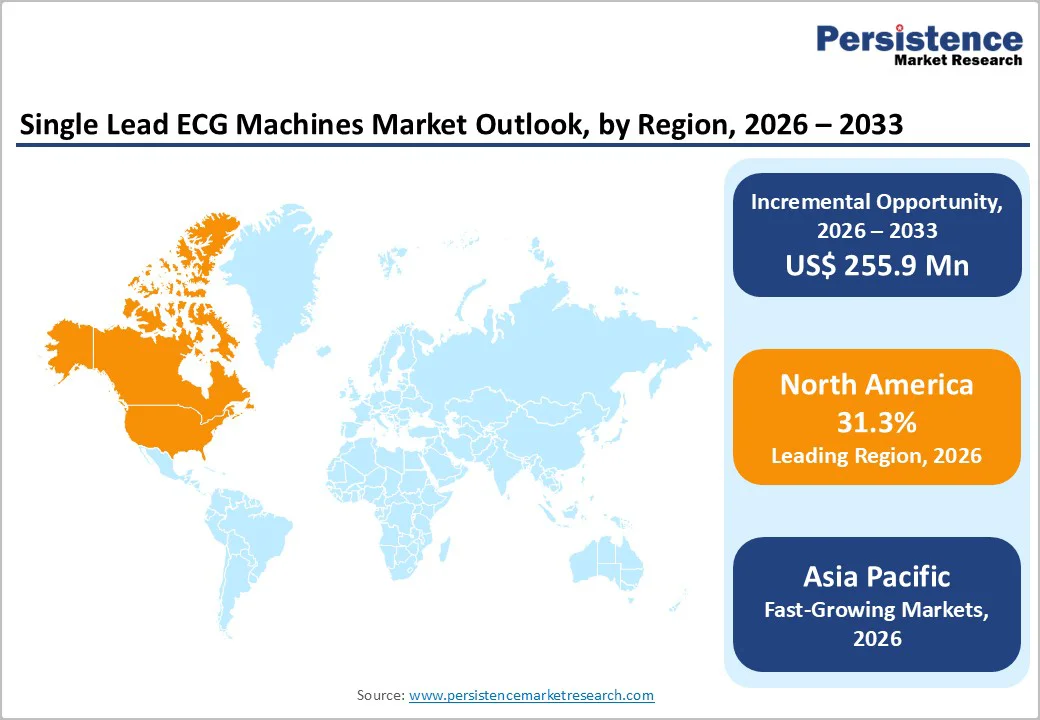

- Leading Region: North America dominates the global market, accounting for 31.3%, driven by strong adoption of advanced cardiac monitoring technologies, a high cardiovascular disease burden, mature reimbursement structures, and widespread availability of remote ECG diagnostic services.

- Fastest-Growing Region: The Asia Pacific market is expected to grow rapidly with a CAGR of 6.9% in the forecast period, fueled by expanding healthcare access, rising cardiac risk factors, a growing elderly population, and increasing penetration of low-cost wearable ECG devices across emerging economies.

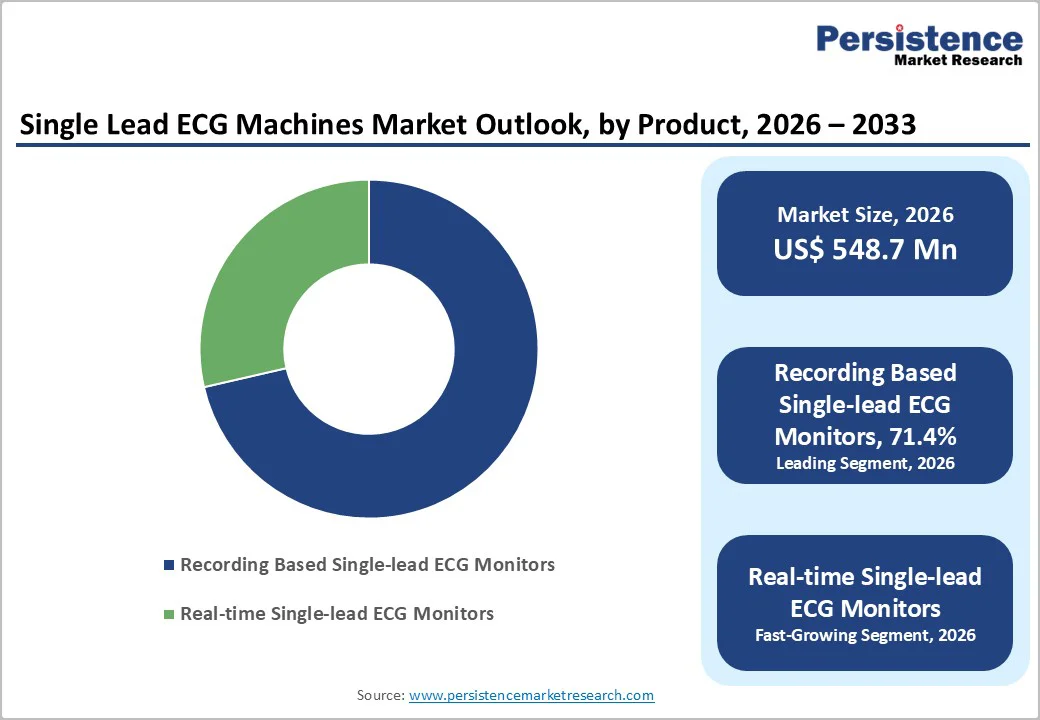

- Leading Product: Recording-Based Single-lead ECG Monitors, with a 71.4% share, supported by high demand for portable, continuous monitoring tools, lower cost compared to multi-lead systems, and growing use in home-based and ambulatory cardiac assessment.

- Leading Application: Atrial Fibrillation (AF) to remain dominant with 32.9%, driven by rising global AF burden, preference for long-term rhythm monitoring, increased screening programs, and early detection initiatives enabled by compact single-lead ECG technologies.

- Leading End-user: Hospitals lead with a 48.1% share, driven by high patient inflow for cardiac evaluation, greater diagnostic accuracy needs, integration of ECG data into hospital systems, and preference for clinically validated monitoring devices.

- Remote ECG monitoring usage is accelerating, driven by expanding telehealth, chronic disease management needs, wearable device penetration, and growing preference for continuous rhythm assessment outside clinical settings.

- Growing shift to homecare due to patient convenience, cost-effectiveness, reduced hospital visits, and increasing adoption of portable single-lead devices for chronic cardiovascular disease management.

- Expanding reimbursement coverage strengthens market demand, supported by insurance recognition of remote monitoring value, reduced patient cost burden, and inclusion of ECG services in chronic disease management packages.

| Key Insights | Details |

|---|---|

| Global Single Lead ECG Machines Market Size (2026E) | US$ 548.7 Million |

| Market Value Forecast (2033F) | US$ 804.6 Million |

| Projected Growth (CAGR 2026 to 2033) | 5.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.1% |

Market Dynamics

Driver - Global Cardiovascular Burden and Increasing Demand for Portable Cardiac Diagnostics Boost Single-lead ECG Adoption

Cardiovascular diseases (CVDs) remain the leading cause of death globally, claiming 18.6 million lives annually, with 126 million people affected by Coronary Artery Disease (CAD). This persistent disease burden has intensified the demand for scalable, accessible diagnostic tools capable of early rhythm screening and continuous monitoring across diverse care settings. Healthcare systems also face operational inefficiencies-nearly 60% of hospitals report challenges with duplicate ECGs, while 80-90% of ischemic episodes remain clinically silent, underscoring the value of rapid, point-of-care cardiac assessment.

Single lead ECG devices address these gaps effectively by offering portable, wearable, and highly usable monitoring solutions for ambulatory clinics, pre- and post-surgical recovery, and home-based cardiac-risk patients. Their rising acceptance is further supported by strong clinical evidence showing high concordance with multi-lead ECG parameters and accurate arrhythmia detection, even during exercise. Patients increasingly prefer these lightweight wearable devices due to improved comfort and adherence.

A key innovation milestone occurred in April 2025, when HeartBeam, Inc. announced a strategic collaboration with AccurKardia to integrate the FDA-cleared AccurECG™ analysis software into HeartBeam’s ambulatory devices. Such advancements enhance diagnostic precision and reinforce the growing shift toward continuous, remote, and patient-friendly cardiac monitoring-solidifying single-lead ECG machines as a critical driver in the global diagnostics market.

Restraints - Clinical limitations and insufficient multi-lead data restrict single-lead ECGs for comprehensive diagnosis

Despite their convenience, single-lead ECG machines face inherent diagnostic limitations compared to multi-lead systems. Because they record only one electrical axis of the heart, these devices may miss subtle conduction abnormalities, ischemic patterns, or complex arrhythmias that require multi-vector evaluation.

As a result, clinicians still rely heavily on multi-channel ECGs for comprehensive assessment, especially in acute care, advanced cardiology, exercise stress testing, and structural heart disease evaluation. This creates a ceiling on how widely single-lead devices can be used in frontline diagnostic decision-making.

In parallel, the rapid rise of artificial intelligence (AI) for ECG-based structural heart disease (SHD) detection presents another hurdle. While AI tools can identify patterns of SHD, most algorithms are trained on multi-lead ECG datasets. Scaling these models for widespread use in wearable or portable single-lead systems remains difficult due to the limited availability of well-labeled diagnostic data from such devices. This data scarcity slows model development, reduces clinical confidence, and restricts the integration of advanced diagnostic analytics into single-lead platforms.

Together, these constraints reduce the clinical depth and reliability of single-lead ECG interpretations, thereby restraining their uptake in high-acuity environments and narrowing their role to screening rather than full diagnostic replacement.

Opportunity - Digital Health Expansion and Wireless Monitoring Create Growth Potential for Single-lead ECG Technologies

The accelerating digital transformation in healthcare-driven by mobile connectivity, smartphone penetration, and algorithm-enabled monitoring-has created major opportunities for single-lead ECG devices. Although healthcare historically lagged in adopting digital tools, a new wave of wireless and biosensor-based cardiac monitoring solutions is now reshaping patient management. These systems leverage real-time data transmission, cloud analytics, and predictive algorithms to support individualized care, allowing clinicians to detect events before they escalate.

Ambulatory ECG monitoring, essential for capturing intermittent arrhythmias, has become significantly more patient-centric with newer single-lead devices. Their lightweight, waterproof designs, extended battery life, wireless synchronization, and app-based engagement offer substantial advantages over traditional Holter monitors. These features enhance comfort, prolong monitoring duration, and improve real-world adherence-creating opportunities for broader screening programs and long-term rhythm surveillance.

Innovation in consumables further expands the opportunity. For instance, companies like Dräger have introduced single-patient-use ECG lead systems, reducing nosocomial infection risks and supporting hospital hygiene protocols while lowering associated treatment costs. As health systems shift toward remote, preventive, and home-based cardiac diagnostics, the market is poised for accelerated adoption of next-generation single-lead ECG devices, enabling wider access and more proactive cardiovascular management.

Category-wise Analysis

By Product Insights

Recording-based single-lead ECG monitors are expected to capture a 71.4% share of the global market by 2026, driven by their ability to offer consistent, high-quality tracings ideal for routine cardiac assessments. Their compact, low-maintenance design makes them highly suitable for primary care centres, emergency rooms, and remote clinics with limited resources. These devices also enable rapid rhythm evaluation, supporting frontline clinicians in early detection of arrhythmias. Their affordability compared to multi-lead systems further encourages adoption, especially in cost-sensitive markets. Growing demand for point-of-care cardiac diagnostics strengthens their dominance.

By Application Insights

Atrial fibrillation is projected to hold nearly 32.9% of the global single lead ECG machines market in 2026, driven by its rising global prevalence and the increasing emphasis on timely rhythm detection in outpatient and remote-care settings. Single-lead ECG devices provide quick screening capabilities, enabling early identification of irregular rhythms and reducing dependency on full multi-lead tests for initial assessment. Their portability supports long-term monitoring, which is essential for detecting intermittent AF episodes. As AF-related stroke risk becomes a public-health priority, demand for accessible, low-cost screening tools continues to grow.

By End-user Insights

Hospitals are projected to account for nearly 48.1% of the global single lead ECG machines market in 2026, supported by their extensive patient throughput and the growing need for rapid cardiac triage. Emergency departments, outpatient wards, and general medicine units rely on single-lead ECGs for quick rhythm assessments before deciding on full diagnostic evaluations. Their portability enables bedside use, improving workflow efficiency and reducing delays in initial screening. Hospitals also increasingly deploy these devices for continuous monitoring in recovery units, strengthening their adoption. Budget-friendly pricing further supports large-scale procurement across hospital networks.

Regional Insights

North America Single Lead ECG Machines Market Trends

North America is projected to secure 31.3% of the global single lead ECG machines market by 2026, largely due to its strong focus on early detection of cardiac rhythm disorders. The region’s ageing population-where atrial fibrillation (AF) affects nearly 5% of individuals above 65 and 10% above 80-continues to fuel the need for rapid, accessible diagnostic tools.

Over the past few years, studies such as the AHS (Apple Heart Study) and the Fitbit Heart Study have helped validate the use of photoplethysmography (PPG) and single-lead ECG for AF screening, strengthening clinical confidence in these compact systems. Diagnostic momentum further accelerated with the April 2025 JAMA Cardiology publication demonstrating a noise-adapted AI model capable of predicting heart failure risk using single-lead ECGs across datasets from the Yale New Haven Health System, UK Biobank, and ELSA-Brasil.

These findings, combined with earlier innovations such as the 2022 University of Michigan AI model for hemodynamic instability prediction, highlight the region’s shift toward AI-enabled, portable cardiac diagnostics-supporting widespread adoption of single-lead ECG devices in clinics and home-based monitoring.

Europe Single Lead ECG Machines Market Trends

Europe is projected to account for 28.8% of the global single lead ECG machines market by 2026, supported by a rapidly strengthening emphasis on digital diagnostics, preventive cardiology, and structured screening programs across major economies. The region continues to face a growing burden of atrial fibrillation, heart failure, and age-associated arrhythmias, prompting healthcare systems to adopt more scalable, patient-friendly rhythm-monitoring tools.

Single-lead ECG devices-owing to their portability, low cost, and suitability for primary and community care-align closely with Europe’s shift toward decentralized diagnostic pathways. Several EU-funded initiatives advancing remote cardiac assessment, early AF detection, and home-based monitoring have accelerated clinical acceptance of single-channel devices. Increasing integration of AI-supported ECG interpretation across national digital-health frameworks also enhances diagnostic accuracy, especially in underserved or rural regions.

Additionally, Europe’s strong regulatory support for wearable and mobile cardiac technologies encourages continuous innovation. Together, these factors position single-lead ECG machines as essential tools for timely triage, long-term rhythm tracking, and cost-efficient cardiac screening across Europe’s ageing population.

Asia Pacific Single Lead ECG Machines Market Trends

The Asia Pacific market is expanding rapidly and is expected to grow at a 6.9% CAGR, driven by the region’s risein cardiovascular disease (CVD) burden and rising demand for accessible diagnostic tools. Countries such as India are witnessing disproportionately high CVD mortality-272 per 1 lakh compared with the global average of 235-making affordable rhythm-monitoring solutions critical. This need is reinforced by India’s projected US$2.17 trillion economic loss from CVD between 2012 and 2030.

Diagnostic adoption has accelerated through industry advances, including the January 2024 collaboration between India Medtronic Private Limited and Cardiac Design Labs, and the December 2025 launch of vCardio by vTitan Corporation-a fully India-designed single-lead wearable that integrates hardware with AI-based cloud analytics. Such innovations support early detection of arrhythmias, remote postoperative monitoring, and rural outreach where specialist access is limited.

Clinical validation is also growing; a 2023 ESIC Hospital study demonstrated strong patient comfort and reduced noise using a single-lead adhesive patch compared to traditional Holter systems. Collectively, these developments position single-lead ECG devices as essential diagnostic tools across Asia Pacific’s high-risk population.

Competitive Landscape

The global single lead ECG machines market is highly competitive, driven by rapid innovation in AI-powered diagnostic algorithms, wearable and portable device design, and growing demand for remote cardiac monitoring. Market participants focus on improving accuracy, reducing device size, and enhancing user-friendliness to capture broad adoption across hospitals, clinics, and home-care settings.

Key Industry Developments:

- In June 2024, Anumana and InfoBionic.Ai entered a research collaboration to integrate ECG-AI™ technology with the MoMe ARC® platform, aiming to advance remote cardiac monitoring, enable earlier disease detection, and improve patient outcomes in partnership with Mayo Clinic.

- In July 2025, Royal Philips partnered with Epic to integrate its cardiac ambulatory monitoring and diagnostic services with Epic’s Aura platform, enabling deeper interoperability, streamlining cardiac diagnostics, and supporting providers in improving clinical workflows and patient outcomes.

Companies Covered in Single Lead ECG Machines Market

- Viatom Technology Co., Ltd.

- iRhythm Inc.

- GE Healthcare

- Drägerwerk AG & Co. KGaA

- HOVERLABS

- Recorders & Medicare Systems P Ltd.

- AliveCor, Inc.

- Zimed Healthcare LLC

- BPL Medical Technologies

- Cardionica

- KORRIDA MEDICAL SYSTEMS

- MicroPort Scientific Corporation

Frequently Asked Questions

The global single lead ECG machines market is projected to be valued at US$ 548.7 Million in 2026.

Growing cardiovascular disease burden and rising demand for portable, real-time cardiac screening solutions drive market growth.

The global market is poised to witness a CAGR of 5.6% between 2026 and 2033.

Advancements in AI-enabled diagnostics and expanding adoption of wearable cardiac monitoring devices present major growth opportunities.

Major players in the global are GE Healthcare, Drägerwerk AG & Co. KGaA, Recorders & Medicare Systems P Ltd., AliveCor, Inc., and others.