- Inks, Coatings, Adhesives & Sealants (ICAS)

- Printing Inks Market

Printing Inks Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Printing Inks Market by Ink Type (Water-Based Inks, Solvent-Based Inks, UV-Cured Inks, Oil-Based Inks, LED-Curable Inks), Printing Process (Lithographic, Gravure, Flexographic, Digital, Screen), Application (Packaging & Labels, Commercial & Publication Printing, Textile Printing, Industrial & Decorative Printing, Misc.) and Regional Analysis for 2026 - 2033

Printing Inks Market Share and Trends Analysis

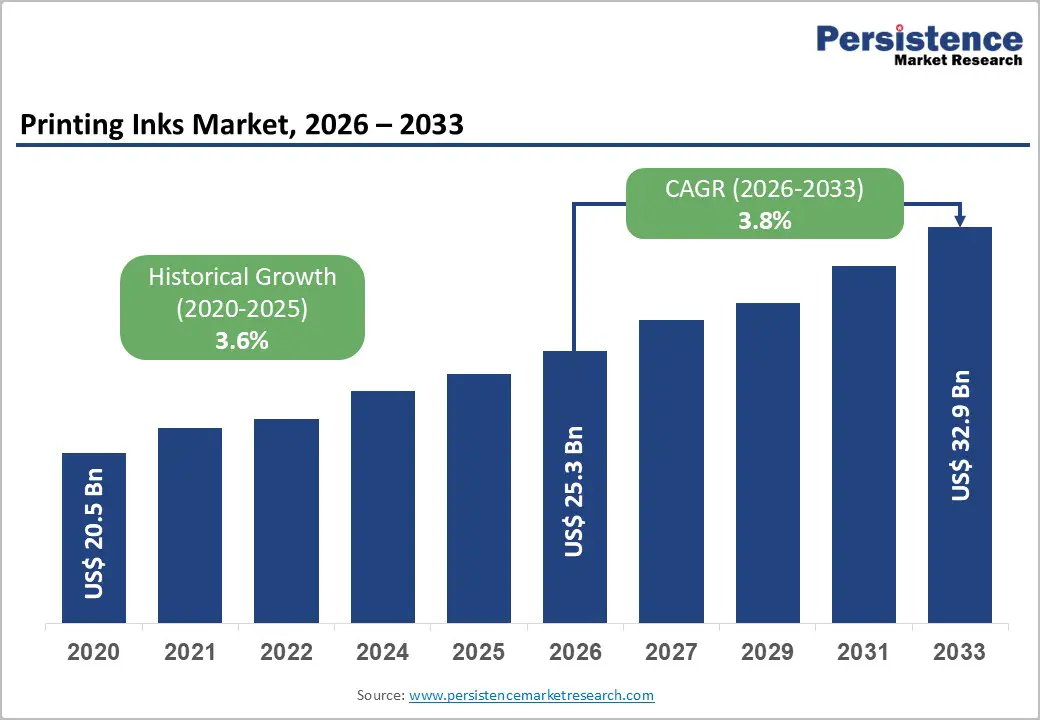

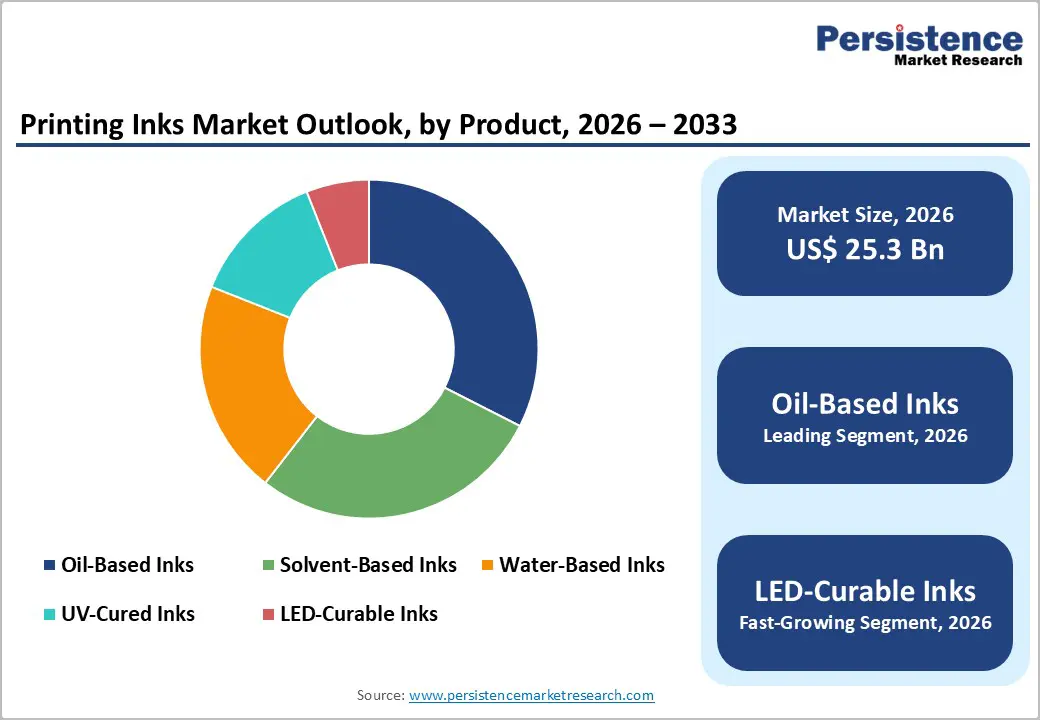

The global printing inks market size is projected at US$25.3 billion in 2026 and is projected to reach US$32.9 billion by 2033, growing at a CAGR of 3.8% between 2026 and 2033.

Growth is underpinned by rising packaging & labels demand in FMCG, e?commerce, and food sectors, alongside expansion in flexible packaging and corrugated formats. Regulatory pressure on VOC emissions accelerates adoption of water-based, UV and LED-curable chemistries, while digital printing penetration in short-run, customized applications further sustains ink consumption despite structural decline in publication print.

Key Industry Highlights:

- Oil-based inks lead ink types with ~33% share, while LED?curable inks grow fastest at about 7.9% CAGR on energy and sustainability benefits.

- Flexographic printing holds ~35% share of process demand, whereas digital printing expands near 7.8% CAGR, driven by short?run and variable data needs.

- Packaging & labels command ~55% application share, and textile printing is the fastest?growing segment at roughly 5.9% CAGR through 2033.

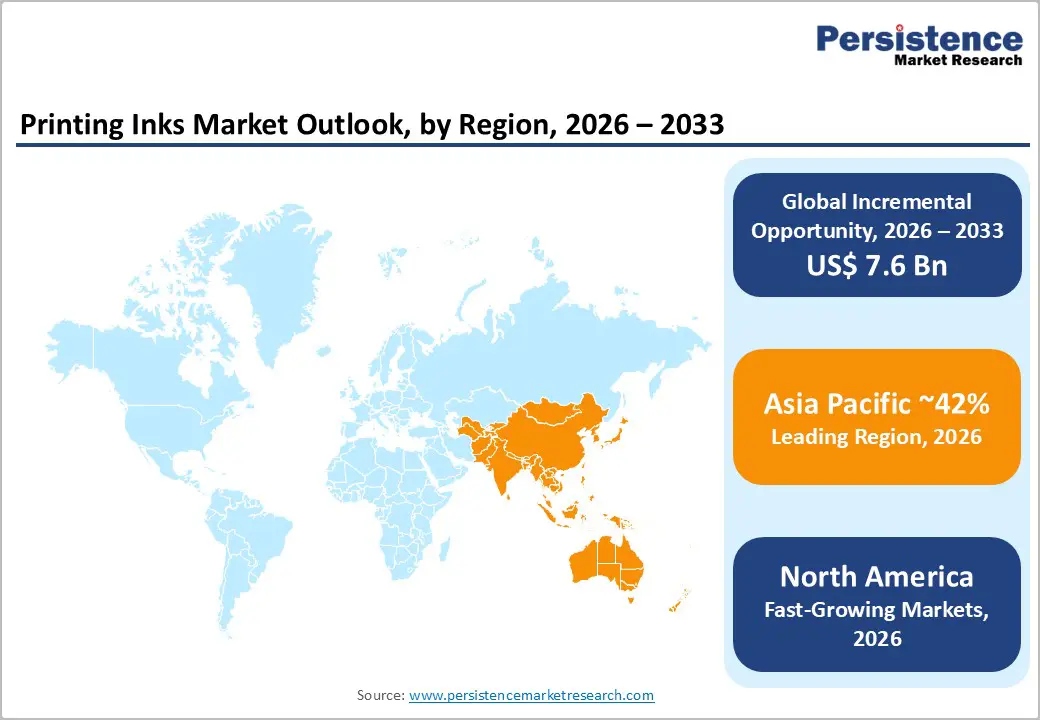

- Asia Pacific leads with about 42% global share and the highest regional growth, while Europe maintains ~27% share with strong regulatory influence.

- Post?2023 developments show multiple investments in UV/LED, sustainable and digital ink technologies, signaling strategic focus on high?value, low?VOC segments.

| Key Insights | Details |

|---|---|

| Printing Inks Market Size (2026E) | US$ 25.3 Billion |

| Market Value Forecast (2033F) | US$ 32.9 Billion |

| Projected Growth CAGR (2026 - 2033) | 3.8% |

| Historical Market Growth (2020 - 2025) | 3.6% |

Market Dynamics Analysis

Drivers - Rising demand from packaging and labels

Packaging and labels remain the core volume driver, accounting for roughly 48-55% of global printing ink consumption by volume as of 2020, reflecting their central role in food, beverage, personal care, and household product supply chains. The acceleration of e?commerce has heightened requirements for corrugated boxes, flexible packaging and shipping labels, directly lifting flexographic and digital ink usage. For example, several estimates indicate packaging inks alone are adding more than 2-3 percentage points to overall ink demand annually, offsetting declines in publication printing and stabilizing total market growth around the mid?single?digit range.

Shift toward low-VOC and energy?efficient chemistries

Tightening environmental regulations in North America, Europe and parts of Asia are constraining conventional solvent-based systems and boosting demand for water-based, UV?cured and LED?curable inks. In the EU, food-contact and recyclability rules have driven a material shift toward low?migration and de?inkable formulations, helping water-based inks capture more than 30% share in some packaging segments by the mid?2020s. UV?cured printing inks, valued at about USD 1.88 billion in 2026, are growing above 7% CAGR through 2031, with LED-technology capturing more than 56% of UV?cured share, illustrating rapid adoption of instant?curing, energy?saving solutions.

Restraints - Decline in commercial and publication printing

The long-term shift toward digital media continues to erode demand for newsprint, magazines and some commercial print applications, structurally reducing volumes for traditional offset and gravure inks. Publishers in mature markets report steady single?digit annual volume declines, which directly impacts lithographic ink consumption. Although packaging partly compensates, this segment’s contraction caps overall market growth and pressures margins for suppliers heavily exposed to legacy publication portfolios, especially in Europe and North America.

Volatility in raw material prices and supply disruptions

Printing inks rely on petrochemical?derived resins, solvents, and pigments, including carbon black and titanium dioxide, which are subject to price volatility and periodic shortages. Episodes of logistics disruption and energy price spikes since 2020 have raised manufacturing costs and complicated inventory management. Smaller converters struggle to pass on sharp price increases to end customers rapidly, compressing margins and sometimes delaying ink system upgrades, thereby moderating adoption of newer premium chemistries in cost?sensitive regions.

Opportunities - Adoption of UV-LED and specialty functional inks

The UV?cured printing inks market, projected to grow from USD 1.9 billion in 2026 to about USD 2.6 billion by 2033, demonstrates strong demand for high?performance, low?VOC solutions. Within this, UV?LED systems are forecast to expand above 9% CAGR, creating attractive niches in labels, folding cartons and industrial decorating. Functional inks such as barrier coatings, low?migration food packaging inks, and security or conductive inks enable premium pricing and differentiation, opening multi?hundred?million?dollar addressable sub?segments over the next decade as regulations and brand owner specifications tighten.

Growth of digital and on?demand printing applications

Digital printing’s projected CAGRs around 7-8% through 2033 reflect its role in short?run packaging, personalized labels, and on?demand commercial print, where conventional processes are uneconomical. This expansion translates into robust growth for inkjet and toner-based inks, especially UV and water?based inkjet formulations compatible with paper, films and textiles. As brands intensify use of variable data, versioning, and late?stage customization, digital inks could represent an incrementally growing share of the market, adding billions of dollars in revenue potential over the forecast horizon.

Category-wise Analysis

Ink Type Insights

Oil-based inks currently lead the ink type segment with an estimated ~33% share of the global printing inks market, reflecting their entrenched use in lithographic and some publication applications. Their cost efficiency, compatibility with diverse paper substrates, and established press infrastructure support this position despite environmental pressures. However, water-based inks already command more than 30% share in selected packaging applications, and UV/LED?curable systems together represent a fast?rising minority share as converters retrofit presses for energy?efficient curing and low?migration performance.

LED?curable inks represent the fastest-growing ink type, expanding at an estimated ~7.9% CAGR from 2026 to 2033, slightly ahead of broader UV?cured ink market growth near 7.2%. Growth is driven by lower energy consumption, instant curing, and improved substrate versatility in labels, narrow?web packaging and some commercial print. As LED units become more affordable and regulations tighten around VOC and mercury lamps, LED?curable ink penetration is expected to accelerate, particularly in Europe, North America, and higher?end Asia Pacific applications.

Printing Process Insights

Flexographic printing is the leading process segment with an estimated ~35% share of global printing inks demand, reflecting its dominance in flexible packaging, labels, corrugated and certain folding carton applications. Flexo inks both water-based and solvent-based, benefit from the process’s ability to print on non?absorbent substrates at high speeds with relatively low plate costs, aligning with large-volume packaging converters. Lithographic printing remains important in commercial print and some packaging, while gravure retains niches in high?volume décor and premium packaging, though both face structural pressure from digital and flexo advances.

Digital printing is the fastest-growing process, registering an estimated ~7.8% CAGR over 2026-2033, underpinned by inkjet and electrophotographic technologies. Key drivers include demand for short runs, rapid design changes, personalization, and late?stage customization in packaging and labels. Digital also grows quickly in textiles and industrial décor, where design flexibility and reduced waste matter. As press speeds improve and ink costs moderate, digital penetration in packaging and commercial segments is likely to deepen, further boosting high?value digital ink revenues.

Application Analysis

Packaging & labels is the leading application segment, accounting for an estimated ~55% share of the global printing inks market by the mid?2020s in value terms, and close to 48% by volume in some assessments. This reflects strong demand across food, beverage, personal care, pharmaceuticals and e?commerce logistics. Flexographic, gravure and digital printing processes, combined with water-based, solvent-based and UV?curable inks, support a wide range of substrates from paper and board to flexible films, making packaging & labels the principal growth engine and an anchor segment for strategic investment in sustainable ink technologies.

Textile printing is the fastest-growing application, expected to progress at around ~5.9% CAGR through 2033 as fashion, sportswear and home textiles shift towards shorter cycles and on?demand production. Digital textile printing, particularly using pigment and reactive inks, grows quickly due to advantages in design flexibility, reduced water usage and localized production. Asia Pacific hubs in China, India and Southeast Asia capture much of this incremental demand, encouraging ink manufacturers to localize formulations and invest in application support tailored to regional fiber and process mixes.

Regional Market Insights

North America Printing Inks Market Share and Trends Analysis

North America is a mature but steadily expanding market, anticipated to grow at a prominent 3.5% CAGR between 2026 and 2033, underpinned by high per?capita packaging consumption and strong brand investment in premium labels and corrugated formats. The United States dominates regional demand, with robust adoption of digital and UV/LED?curable inks for labels, folding cartons and industrial printing. Regulatory scrutiny on VOC emissions and food-contact safety supports migration towards water-based and low?migration systems, while a sophisticated converter base continues to invest in automation and color?management technologies that favor higher?value ink solutions.

Growth is reinforced by innovation ecosystems concentrated around packaging, specialty chemicals and print technology clusters, where collaboration between ink makers, press OEMs, and brand owners accelerates development of sustainable and functional formulations. Capital expenditure flows into narrow?web, digital and hybrid presses, encouraging trials of novel LED?curable and low?migration inks. While competition remains intense, suppliers with strong technical service and regulatory compliance capabilities are positioned to capture incremental share in food, beverage and healthcare packaging applications.

Europe Printing Inks Market Share and Trends Analysis

Europe commands roughly ~27% of the global printing inks market value, benefiting from high packaging sophistication, strong export-oriented FMCG industries, and stringent environmental regulation that guide technology choices. Germany, the U.K., France and Spain collectively form the core demand base, with Germany’s industrial packaging and specialty print sectors particularly influential. EU Green Deal initiatives and harmonized chemicals regulations (including REACH and food-contact frameworks) accelerate transition to low?VOC, water-based and de?inkable systems, creating both compliance obligations and innovation opportunities for suppliers.

The region is expected to grow at low?to?mid single?digit CAGRs through 2033, but offers attractive margins in sustainable and specialty inks, such as low?migration packaging, security and functional coatings. Cross?border consolidation among printers and packaging converters, along with pan?European brand specifications, favor larger ink manufacturers with broad portfolios and technical support networks. Investment continues in UV?LED retrofits and advanced color control, reinforcing demand for premium inks that ensure regulatory conformity and high print performance.

Asia Pacific Printing Inks Market Share and Trends Analysis

Asia Pacific is the leading region, accounting for around ~42% of global printing inks demand and simultaneously representing the fastest-growing regional market. China, Japan, India, and ASEAN economies offer powerful demand drivers: rising middle?class consumption, rapid growth in packaged foods and beverages, and expanding export?oriented manufacturing requiring high?quality packaging and labeling. Flexographic and gravure processes remain prevalent in flexible packaging, while digital and UV?curable inks gain ground in labels, commercial print and specialized industrial applications.

Regional growth rates often exceed 4% annually, with packaging and textiles delivering particularly strong volume gains for both conventional and advanced ink chemistries. Many global ink producers expand local manufacturing and R&D to serve Asia Pacific, leveraging lower production costs and proximity to large customer bases. Governments increasingly promote environmental compliance, gradually shifting demand toward water-based and low?VOC solutions, creating an attractive landscape for sustainable ink technologies and partnerships with regional converters and brand owners.

Competitive Landscape

Leading printing ink suppliers emphasize innovation-led portfolios in sustainable, low?migration and energy?efficient chemistries, combined with cost?effective global manufacturing footprints and targeted market expansion in Asia Pacific and high?value packaging segments. Key differentiators include regulatory expertise, application?specific technical service, and capabilities in UV/LED and digital inks. Emerging business models center on collaborative development with converters and brand owners, integrated color?management services, and lifecycle approaches aligned with circular economy and decarbonization objectives.

Strategic Developments:

- In 2024, DIC Corporation and its subsidiary Sun Chemical expanded investments in sustainable packaging ink technologies, advancing bio-renewable, low-migration and recyclable ink systems for flexible packaging and labels to support brand owners’ circular-economy and regulatory compliance objectives.

- In October 2021, Hubergroup advanced its sustainable ink portfolio by securing Cradle-to-Cradle Certified® Bronze status for the Gecko Green Line Premium flexographic and gravure ink series, reinforcing circular-economy principles such as material health, recyclability, renewable energy use, and responsible water management for packaging applications.

Companies Covered in Printing Inks Market

- DIC Corporation

- Flint Group

- Sakata INX Corporation

- Siegwerk Druckfarben AG & Co. KGaA

- Hubergroup

- Toyo Ink SC Holdings Co., Ltd.

- Sun Chemical

- T&K Toka Co., Ltd.

- Fujifilm Corporation

- Altana AG

- Epple Druckfarben AG

- Nazdar Ink Technologies

- Wikoff Color Corporation

- Yip's Chemical Holdings Limited

- Royal Dutch Van Son

Frequently Asked Questions

The global Printing Inks Market is expected to be about US$25.3 billion in 2026, reaching approximately US$32.9 billion by 2033 across packaging, publication, textile and industrial applications.

Growth is primarily driven by expanding packaging & labels demand, regulatory push toward low‑VOC and energy‑efficient chemistries, and technological advances in flexographic, UV/LED and digital printing processes that enable shorter runs and customization.

Between 2026 and 2033, the market is projected to grow at a 3.8% CAGR, broadly consistent with historical expansion around 3.6% supported by resilient packaging demand offsetting publication declines.

Key opportunities include Asia Pacific packaging and textile growth, rapid adoption of UV‑LED and low‑migration inks, and expansion of high‑margin digital, functional and sustainable ink solutions aligned with circular economy and decarbonization goals.

Major players include DIC Corporation, Sun Chemical, Flint Group, Sakata INX, Siegwerk, hubergroup, Toyo Ink, T&K Toka, Fujifilm, ACTEGA, Epple, Nazdar, Wikoff Color and regional specialists in Asia, Europe and North America.