- Technology

- Direct-to-Garment (DTG) Printing Market

Direct-to-Garment (DTG) Printing Market Size, Trends, Share, and Growth Forecast, 2025 - 2032

Direct-to-Garment (DTG) Printing Market by Printing Mode (Single Pass Printing, Multi-Pass Printing), Ink Type (Water-Based Inks, Pigment Inks, Solvent-Based Inks, UV Inks, Dye-Based Inks.), Technology (Inkjet Printing Technology, Laser Technology.), Application, and Regional Analysis for 2025 - 2032

Direct-to-Garment (DTG) Printing Market Size and Trends Analysis

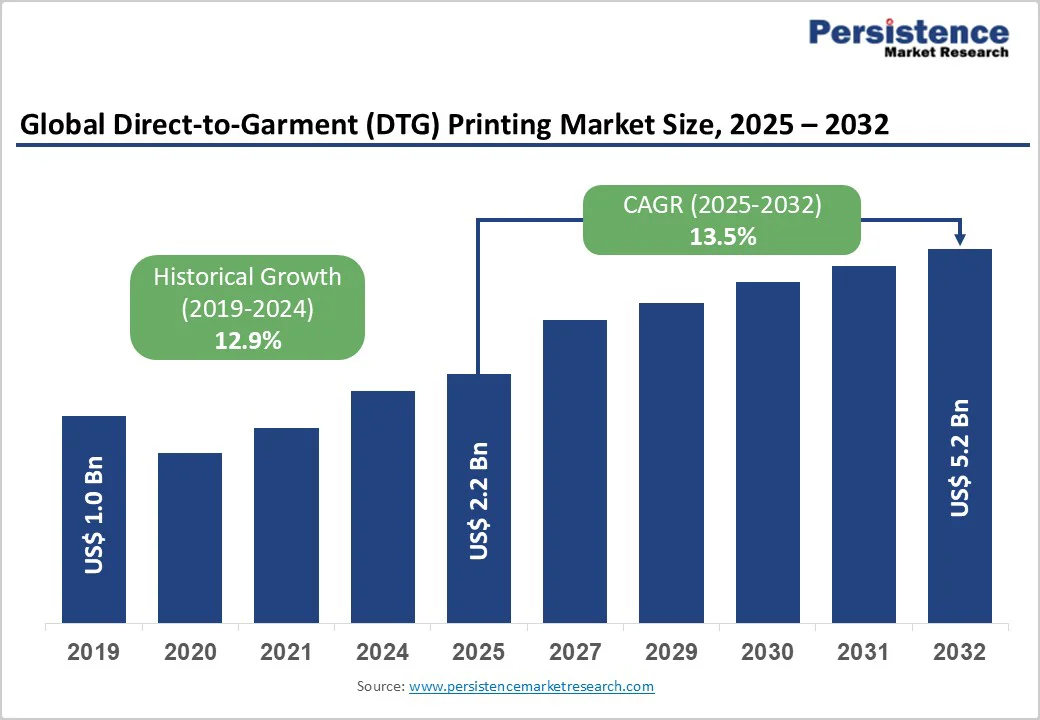

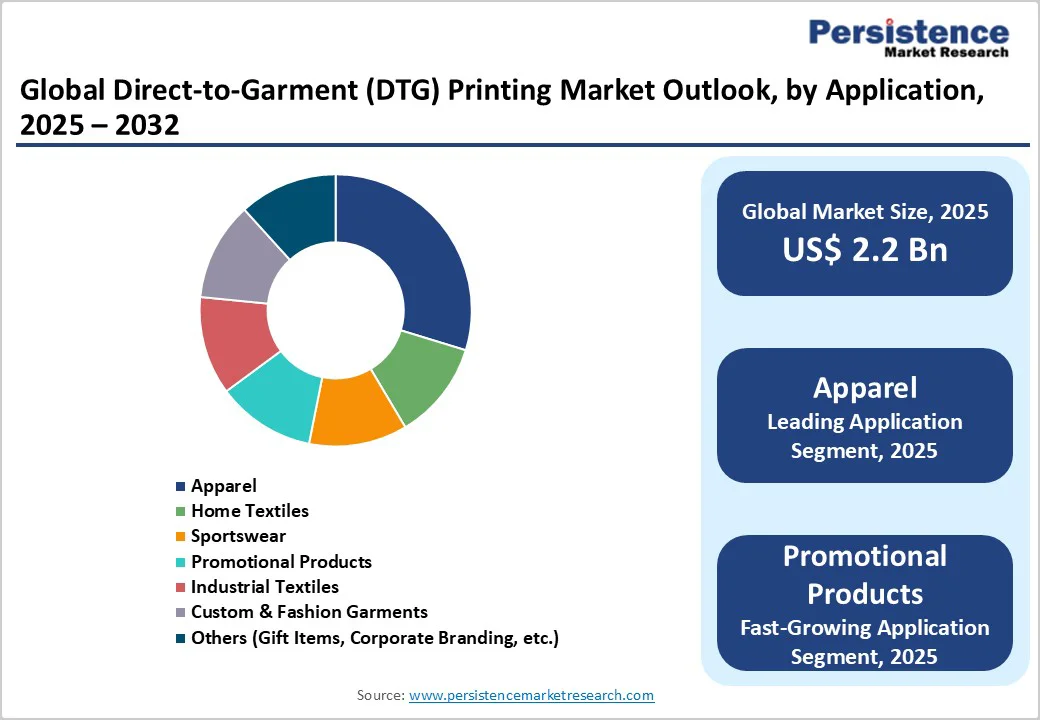

The global direct-to-garment (DTG) printing market size is valued at US$2.2 billion in 2025 and is projected to reach US$5.2 billion, growing at a CAGR of 13.5% between 2025 and 2032.

This expansion reflects the market's transformation from a niche customisation tool to mainstream production technology. The direct-to-garment (DTG) printing market growth is primarily driven by accelerating consumer demand for personalised apparel, the proliferation of e-commerce platforms enabling direct-to-consumer models, and advancements in sustainable ink formulations that align with regulatory requirements.

Key Industry Highlights:

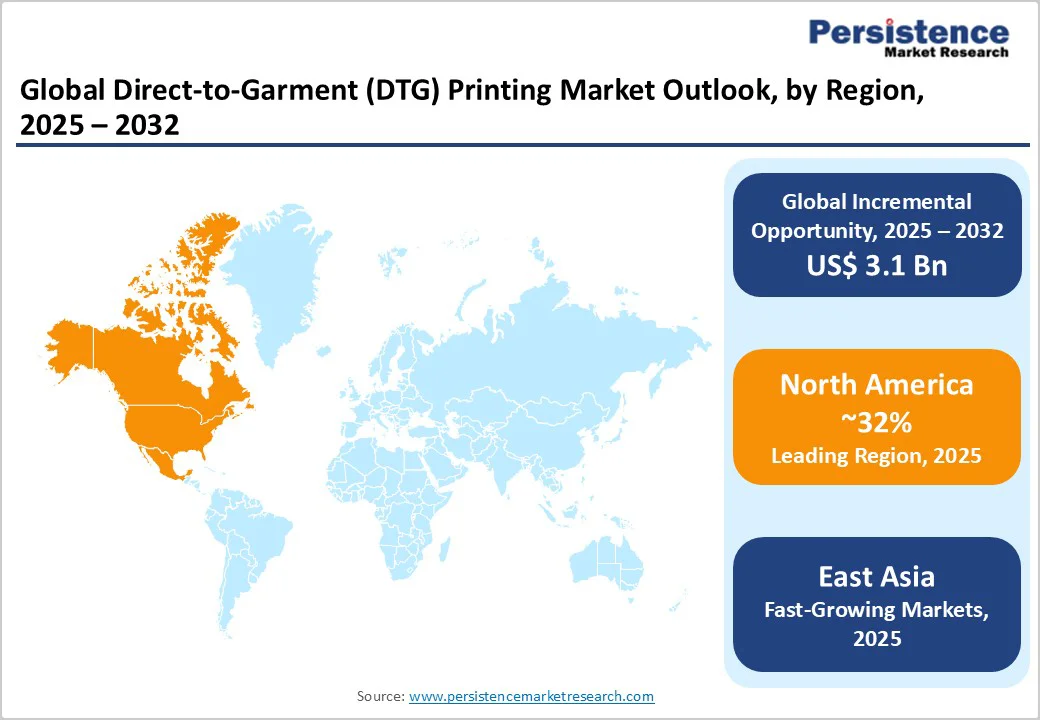

- North America leads the global DTG Printing Market with approximately 32% share, driven by strong consumer demand for personalised apparel and advanced digital printing infrastructure.

- Europe accounts for nearly 28% of global revenue, supported by stringent sustainability regulations, circular economy goals, and accelerated adoption of water-based inks.

- Asia-Pacific emerges as the fastest-growing regional market, propelled by China’s large-scale textile base, India’s expanding apparel sector, and Southeast Asia’s digital commerce boom.

- Apparel dominates with about 40% market share, maintaining its position as the core application segment for custom t-shirts, fashionwear, and merchandise printing.

- Water-based inks hold a leading 42% market share, reflecting rising environmental compliance and consumer preference for sustainable textile printing solutions.

- Single-pass printing technology commands around 55% market share, driven by its superior speed, throughput efficiency, and suitability for high-volume apparel production.

| Key Insights | Details |

|---|---|

| Direct-to-Garment (DTG) Printing Market Size (2025E) | US$2.2 Bn |

| Market Value Forecast (2032F) | US$5.2 Bn |

| Projected Growth (CAGR 2025 to 2032) | 13.5% |

| Historical Market Growth (CAGR 2019 to 2024) | 12.9% |

Market Dynamics

Drivers - Consumer Personalisation and E-Commerce Synergy

The direct-to-garment (DTG) printing market has experienced substantial momentum due to the convergence of consumer personalisation preferences and the expansion of digital commerce. Approximately 36% of consumers express interest in purchasing personalised products, with apparel being the dominant category.

In the second quarter of 2025, the U.S. Census Bureau reported e-commerce sales of $304.2 billion, accounting for 16.3% of total retail sales, marking a 5.3% year-on-year increase, notably outpacing the 3.9% growth in total retail sales during the same period. Women’s and girls’ apparel commanded significantly higher household expenditures than men’s and boys’, underscoring entrenched demand for personalised and fashion-forward clothing.

The shift toward e-commerce as a primary shopping destination, especially for apparel and footwear, reflects broader consumer behaviour favouring customisation, rapid fulfilment, and inventory-light business models, key advantages facilitated by DTG technology.

Online design platforms, such as those integrated with Shopify and Etsy, have empowered small businesses and independent creators to monetise custom designs without substantial investment. This has lowered market entry barriers and amplified demand for printing systems that support rapid customisation and small-batch production workflows.

Technological Advancement in Automation and Production Efficiency

The direct-to-garment (DTG) printing market is fundamentally driven by the global shift toward convenience consumption and the need to preserve product freshness across extended distribution networks.

According to the U.S. Department of Commerce, the U.S. food and beverage manufacturing sector accounted for 16.8% of total manufacturing sales in 2021 and employed approximately 1.7 million workers. In this context, high-barrier packaging films enable manufacturers to extend shelf life, reduce food waste, and meet retailer stocking requirements across increasingly complex supply chains.

The U.S. flexible packaging industry alone generated $41.5 billion in sales in 2022, with food packaging contributing nearly 50% of total shipments. Modified atmosphere packaging (MAP) technology, vacuum sealing, and multilayer barrier structures utilizing materials such as ethylene vinyl alcohol (EVOH) and polyamide (PA) have become standard practice in meat processing, dairy products, and ready-to-eat meal categories.

Regulatory Framework Advancement and Sustainable Ink Adoption

Environmental regulations have become a primary growth catalyst for the direct-to-garment (DTG) printing market, particularly in North America and Europe. Regulatory authorities now require up to 60% fewer hazardous air pollutants in textile print facilities, an EPA directive that directly aligns with DTG's water-based chemistry formulations. Water-based inks currently hold approximately 42% market share in the DTG sector as of 2025, reflecting both regulatory compliance requirements and consumer preference for eco-friendly printing solutions.

The European Union's Corporate Sustainability Reporting Directive (CSRD), Corporate Sustainability Due Diligence Directive (CSDDD), and the newly revised EU Taxonomy Regulation create compliance obligations that compel organisations across multiple sectors, including printing, to transition toward environmentally responsible practices.

In 2025, DTG became significantly greener, with innovations including eco-friendly inks, reduced water use, and localised, on-demand production models that collectively lower carbon footprints and minimise waste. These regulatory developments position water-based and pigment-based ink technologies as market differentiators, as manufacturers increasingly market their products' environmental credentials to justify premium pricing and capture market share from traditional screen-printing alternatives.

Restraints: High Initial Capital Investment and Operational Cost Barriers.

The Direct-to-Garment (DTG) Printing Market faces structural constraints, including equipment acquisition costs and specialised operational expenses, that limit market penetration among small and emerging businesses. DTG printer acquisition costs represent a significant barrier to entry for entrepreneurs and small print shops, with machines commanding premium pricing compared to traditional screen-printing equipment due to their technological sophistication and proprietary ink systems.

Specialized ink formulations command relatively high costs compared to conventional printing methods, creating ongoing operational expense pressures that impact profit margins, particularly for businesses with low monthly or yearly production volumes.

Pre-treatment requirements for certain fabric types, especially dark garments requiring specialized pretreatment processes, introduce additional operational complexity and costs that inexperienced operators may find challenging to manage consistently. Technical expertise requirements for operating and maintaining DTG systems remain a market restraint, as specialized training and support services increase the total cost of ownership and create dependency on manufacturer-provided technical resources.

Opportunity - Emerging Applications in Home Textiles and Technical Textile Segments

Home textiles represent a significant growth opportunity for the Direct-to-Garment (DTG) Printing Market, with applications extending beyond conventional apparel to include personalised home décor products, bedding, linens, and decorative textiles. Home textiles have emerged as the fastest-growing segment in the DTG market, driven by rising consumer demand for customised home furnishings and interior décor products that reflect individual aesthetic preferences.

The on-demand production model enabled by DTG technology aligns exceptionally well with this segment, as consumers increasingly seek unique, personalised items for personal use and gift-giving without committing to mass-production volumes.

Technical textiles, including automotive interiors, safety vests, medical wraps, and industrial applications requiring variable data printing for traceability codes and regulatory markings, represent an emerging opportunity for DTG manufacturers aiming to expand addressable markets beyond apparel decoration. These niche applications show strong growth potential as industrial and medical sectors increasingly adopt digital printing technologies to enhance product differentiation and compliance capabilities.

Geographic Expansion Opportunities in Asia-Pacific and Emerging Markets

Asia-Pacific markets offer substantial untapped opportunities for the Direct-to-Garment (DTG) Printing Market due to rapid industrialisation, urbanisation, and dynamic growth of the middle class.

China remains the world’s largest global textile and clothing producer, underpinned by a labour force exceeding 800 million and robust annual consumer expenditure on fashion.

Nearly 6.4 million people are employed directly in China’s garment and textile sector, reflecting a strong domestic base and ongoing export leadership despite shifts in global sourcing strategies. China accounted for 31.6% of global apparel exports in 2023 and hosts more than 44,000 manufacturing enterprises in textiles, apparel, and footwear, bolstered by continued government incentives supporting intelligent manufacturing systems and compliance with sustainability standards.

India’s apparel market is undergoing a transformative phase, valued at US$102.8 billion in 2022 and projected to reach US$146.3 billion by 2032, fueled by expanding middle-class populations, rising disposable incomes, and robust cultural diversity.

According to the India Brand Equity Foundation, e-commerce in India is valued at US$125 billion in 2024, with projections of US$345 billion by 2030 and over 270 million online shoppers, positioning the country as the world’s second-largest e-retail market. Major government initiatives such as “Make in India” and targeted skill development programs foster innovation, local manufacturing, and improvements in digital infrastructure, which support the DTG market’s penetration into Tier-II and Tier-III cities.

Category-wise Analysis

Printing Mode Insights

Single-pass printing technology dominates the direct-to-garment (DTG) printing market, commanding 55% market share in 2025, reflecting its efficiency advantages in high-volume production environments.

Single-pass systems use advanced carriage-mounted printheads that traverse the fabric width in a single pass, significantly reducing production cycle times compared to multi-pass alternatives and enabling substantially higher throughput per operational hour.

Single-pass digital textile printing machines are demonstrating strong commercial adoption among commercial print service providers and apparel manufacturers, prioritizing production speed and cost efficiency. These systems are particularly suited to production facilities with established high-volume orders, where amortizing premium equipment costs across substantial production runs creates economic advantages over lower-cost, lower-speed alternatives.

Multi-pass printing technology represents the fastest-growing segment within the Direct-to-Garment (DTG) Printing Market, despite commanding a smaller current market share, as it addresses specific production and economic requirements for businesses with variable or lower-volume production schedules.

Ink Type Insights

Water-based inks hold the dominant market position within the Direct-to-Garment (DTG) Printing Market, accounting for 42% market share in 2025, reflecting both regulatory compliance drivers and consumer sustainability preferences.

These non-toxic, biodegradable inks reduce environmental impact and appeal to eco-conscious consumers and businesses, aligning with current market demands for sustainable production practices and corporate commitments to ecological responsibility.

Water-based formulations demonstrate inherent suitability for fabric applications, with chemistry enabling efficient ink penetration into fabric fibers, producing soft-hand feel prints with vibrant, durable characteristics that meet premium consumer expectations for custom apparel.

Stringent environmental regulations favoring water-based pigment inks across North American and European markets have established baseline compliance requirements that effectively mandate the adoption of water-based chemistry for manufacturers seeking unrestricted market access in developed economies.

Pigment inks represent the fastest-growing segment within the Direct-to-Garment (DTG) Printing Market, driven by superior performance in durability, color vibrancy, and environmental sustainability.

Pigment inks command approximately 65% of the broader digital printing inks market, owing to their superior color vibrancy, lightfastness, and durability characteristics that make them ideal for applications requiring long-lasting prints, including textiles and specialty apparel products.

Application Insights

Apparel dominates the Direct-to-Garment (DTG) Printing Market application landscape, commanding 40% market share in 2025, reflecting the technology's foundational emergence within custom t-shirt printing and its evolution as the industry standard for personalized garment production.

Clothing and apparel still command around 60% of the Direct-to-Garment printing market revenue, pooling demand from fashion labels, merchandise resellers, influencer storefronts, and independent designers seeking high-quality, on-demand production capabilities.

DTG printing is widely used in apparel for its ability to produce high-resolution, full-colour designs on demand, meeting diverse aesthetic and functional requirements that traditional manufacturing methods cannot economically serve customised, short-run production scenarios.

Promotional products represent the fastest-growing application segment within the Direct-to-Garment (DTG) Printing Market, capitalising on corporate branding initiatives, event merchandise, and gift customisation opportunities that drive substantial demand for personalised product decoration.

Regional Insights and Trends

North America Direct-to-Garment (DTG) Printing Market Trends

North America maintains the dominant global position within the Direct-to-Garment (DTG) Printing Market, commanding approximately 32% of the global market within the provided data framework, with the United States generating substantial revenue contribution to regional and global market performance.

Federal chemical regulations remain lighter than Europe's, easing the adoption of new ink formulations and competing technology platforms, though corporate ESG pledges are accelerating the transition toward water-based ink systems among major brands and print service providers.

North America's market leadership reflects established infrastructure supporting digital printing technology adoption, the presence of major industry players including Kornit Digital, Epson, and Brother International, and consumer market characteristics emphasising personalisation and on-demand product availability, which position DTG technology as an optimal production method for regional apparel customisation and promotional product markets.

East Asia Direct-to-Garment (DTG) Printing Market Trends

East Asia is a key growth region for the Direct-to-Garment (DTG) Printing Market, with China poised to lead the Asia-Pacific digital textile printing sector. Supported by a massive labor force of over 800 million and extensive manufacturing infrastructure, China remains the world’s largest apparel producer and exporter.

Environmental regulations and government initiatives like “Made in China 2025” are accelerating the adoption of cleaner, more efficient DTG technologies, especially in textile clusters like Zhejiang and Guangdong.

Improvements in digital infrastructure, digital payments, and government schemes enhance business models focused on quick commerce and direct-to-consumer sales. Southeast Asian countries are also advancing digital textile printing adoption, collectively positioning East Asia as a strategic hub for DTG market expansion centred on sustainability, localised production, and personalised apparel demand.

Europe Direct-to-Garment (DTG) Printing Market Trends

Europe accounts for approximately 28% of the global Direct-to-Garment (DTG) Printing Market, with strong performance concentrated in Germany, the United Kingdom, and France, driven by regulatory compliance, sustainability initiatives, and consumer transition toward ethical fashion consumption.

The regional market’s expansion is underpinned by stringent European ESG frameworks, including the Corporate Sustainability Reporting Directive (CSRD), the Corporate Sustainability Due Diligence Directive (CSDDD), and revisions to the EU Taxonomy Regulation, which collectively compel textile and apparel producers to adopt sustainable production technologies such as DTG printing.

The Ecodesign for Sustainable Products Regulation (ESPR), effective from July 2024, extends design requirements to textiles, mandating durability, reparability, and recyclability characteristics naturally aligned with DTG technology’s waste-reducing and on-demand production capabilities.

Competitive Landscape

The global direct-to-garment (DTG) printing market is fragmented, with a wide range of companies offering diverse printing technologies and solutions. While some companies dominate the high-end industrial printing segment, the market remains competitive with many players catering to different niches, including small-scale businesses and large manufacturers.

Leading companies such as Kornit Digital Ltd., Brother International Corporation, Mimaki Engineering Co., Ltd., Ricoh Company, Ltd., and Durst Group hold significant market shares, driving innovation and technological advancements in DTG printing. Despite these leaders, the market includes several regional and smaller players, contributing to its fragmented nature and offering opportunities for new entrants to grow.

Key Industry Developments:

- In April 2024, Stratasys Ltd. introduced its Direct-to-Garment (D2G) solution for the J850 TechStyle™ printer, marking a breakthrough in the DTG printing market. The technology enables full-color, multi-material 3D printing directly on fully assembled garments across fabrics like denim, cotton, polyester, and linen. This innovation enhances personalization, sustainability, and design flexibility, empowering fashion brands to produce bespoke, waste-reducing apparel that supports sustainable manufacturing practices.

- In September 2025, Epson launched the SureColor® F1070 Business Edition, a hybrid Direct-to-Garment (DTG) and Direct-to-Film (DTFilm) printer designed for small businesses and creative entrepreneurs. The compact, all-in-one system enables on-demand, high-quality garment printing across diverse fabrics, enhancing accessibility for startups and artisans. Featuring PrecisionCore® Micro TFP® printhead and UltraChrome® DG2 inks, the model supports sustainable, OEKO-TEX®-certified printing while expanding customization and revenue opportunities in the global DTG printing market.

Companies Covered in Direct-to-Garment (DTG) Printing Market

- Kornit Digital Ltd.

- Brother International Corporation

- Mimaki Engineering Co., Ltd.

- Ricoh Company, Ltd.

- aeoon Technologies GmbH

- Durst Group

- KONICA MINOLTA

- ROLAND DG

- ROQ International

- Sawgrass Technologies Inc.

- Seiko Epson Corporation

- The M&R Companies.

Frequently Asked Questions

The global Direct-to-Garment (DTG) Printing market is projected to be valued at US$ 2.2 Bn in 2025.

The Single Pass Printing segment is expected to hold around 55% market share by Printing Mode in 2025 in the Global Direct-to-Garment (DTG) Printing Market.

The market is expected to witness a CAGR of 13.5% from 2025 to 2032.

The Direct-to-Garment (DTG) Printing market growth is driven by rising consumer demand for personalized apparel combined with expanding e-commerce platforms facilitating on-demand production and customisation.

Key market opportunities include expanding DTG adoption in emerging Asia-Pacific markets fueled by robust e-commerce growth, government initiatives supporting digital manufacturing, and increasing demand for sustainable, localized production models.

The leading global players in the Direct-to-Garment (DTG) Printing market include Kornit Digital, Brother International Corporation, Epson, Ricoh, ROQ International, Aeoon Technologies, and Omniprint.