- Plastics, Polymers & Resins

- Polymer Clay Market

Polymer Clay Market Size, Share, and Growth Forecast, 2025 - 2032

Polymer Clay Market By Product Form (Solid Polymer Clay, Liquid Polymer Clay, Others), Application (Jewelry and Arts & Sculpture, Toys & Novelty Crafts, Others), Distribution, and Regional Analysis for 2025 - 2032

Polymer Clay Market Size and Trends Analysis

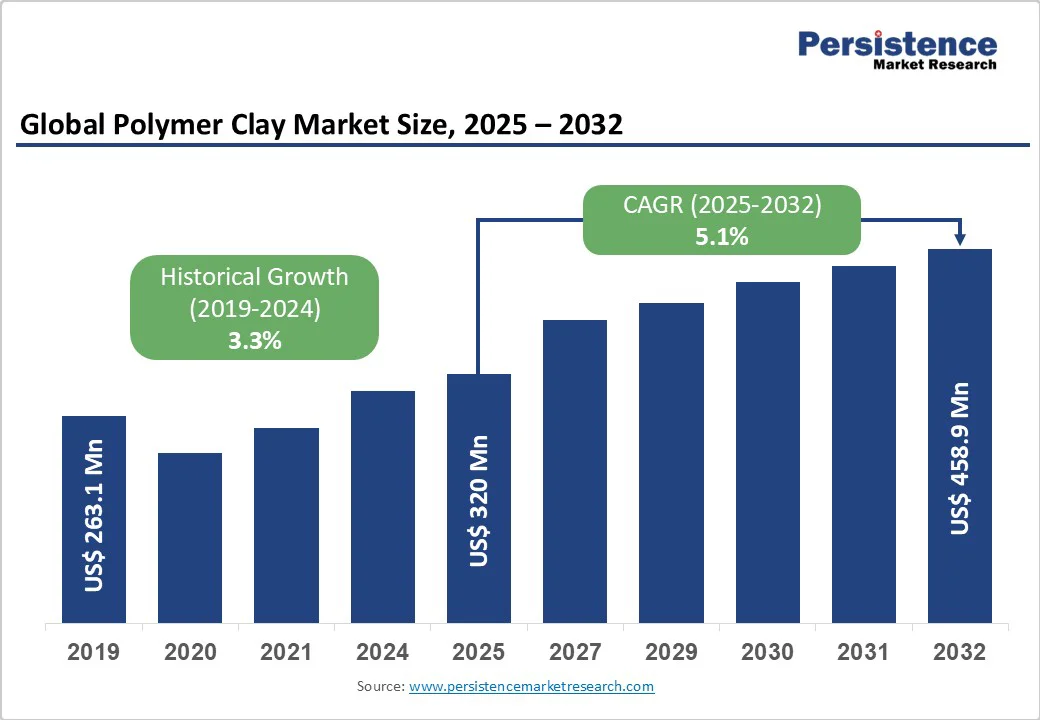

The global polymer clay market size is projected to be valued at approximately US$320 Million in 2025, and is expected to reach around US$458.9 Million by 2032, growing at a CAGR of 5.1% during the forecast period from 2025 to 2032, driven by the rising popularity of do-it-yourself (DIY) activities, educational craft programs, and the growing demand for handmade decorative products.

Consumer preference for cost-effective, oven-bake modeling materials has strengthened the adoption of polymer clay among hobbyists and artisans. E-commerce platforms have broadened accessibility, while product innovations such as effect finishes and non-toxic formulations continue to attract a wider customer base.

Key Industry Highlights

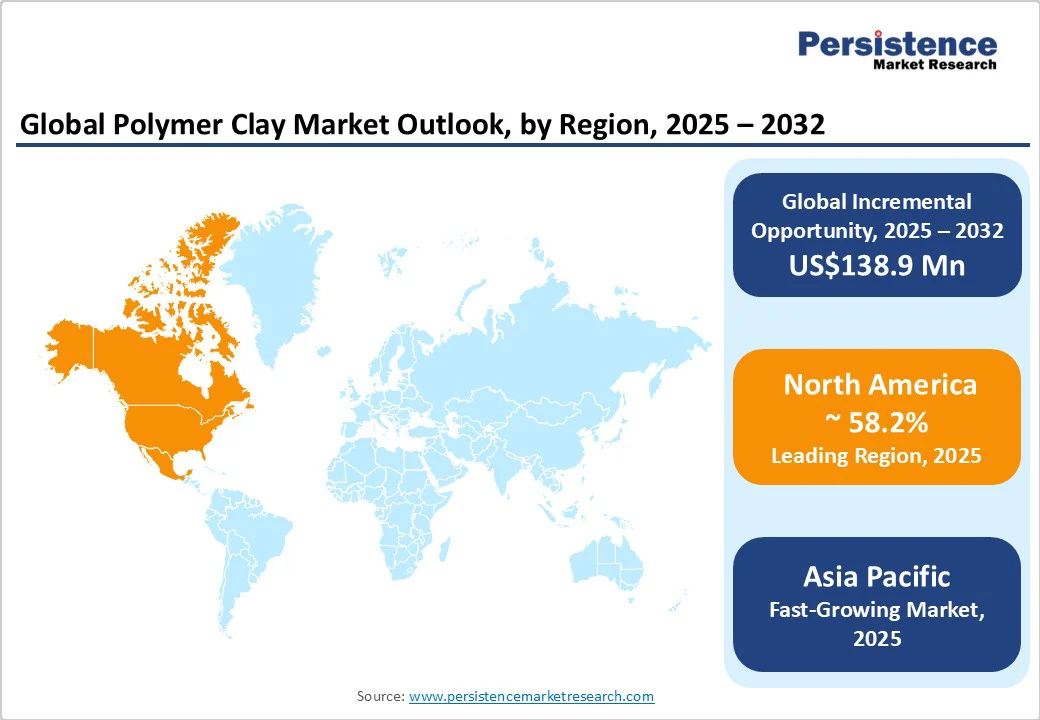

- Leading Region: North America holds 58.2% of the regional market share, driven by strong DIY culture, high per-capita craft spending, and established retail and e-commerce networks.

- Fastest-growing Region: Asia Pacific fueled by rising disposable incomes, educational adoption, and cost-competitive manufacturing.

- Investment Plans: Focus on premium formulations, educational and institutional kits, digital tutorials, and online subscription boxes to expand market reach and consumer engagement.

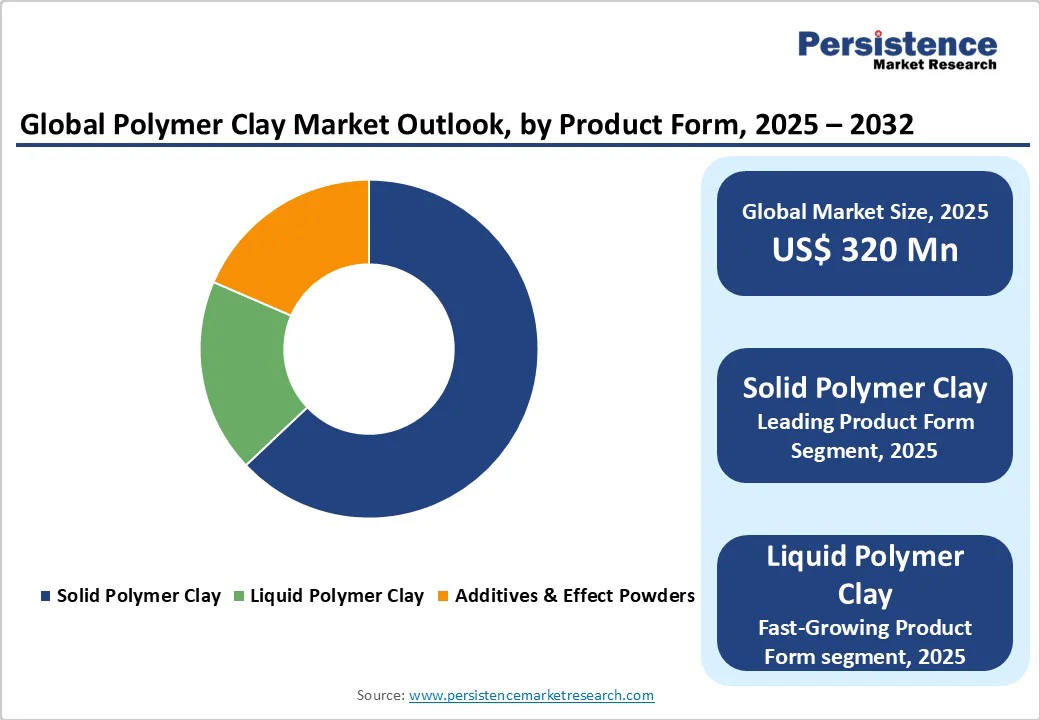

- Dominant Product Form: Solid Polymer Clay 68.5% of market share, favored for versatility, ease of handling, and availability in standard block formats.

- Leading Application: Jewelry and Arts & Sculpture 65.3% of application share, driven by social media trends, artisan adoption, and high aesthetic appeal of finished products.

| Key Insights | Details |

|---|---|

|

Polymer Clay Market Size (2025E) |

US$320 Mn |

|

Market Value Forecast (2032F) |

US$458.9 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

5.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Growth of the DIY and Hobbyist Economy

The polymer clay industry has experienced a resurgence driven by the global DIY and small-craft movement. Platforms such as Etsy, Pinterest, and Instagram have encouraged millions of individuals to launch small jewelry and decorative-item businesses using polymer clay as a primary material. The market benefits from low entry barriers, minimal capital requirements, and a strong online community that promotes creative sharing. The result has been an annual increase in retail unit sales, with hobbyists and micro-entrepreneurs collectively driving more than 40% of consumer-grade clay demand. This trend has also encouraged brands to introduce starter kits and themed assortments that appeal to beginners and small sellers alike.

Institutional and Educational Applications

Educational institutions have become a consistent demand driver. Schools and art academies increasingly adopt polymer clay for creative learning due to its safety, flexibility, and easy curing properties. Non-toxic formulations, combined with certification standards such as ASTM and EN-71, have made polymer clay suitable for children’s art and classroom activities. The institutional channel provides predictable year-round demand, reducing the seasonality that characterizes consumer craft sales. Manufacturers targeting this segment often design large-volume class packs and bundled tool kits, ensuring stable margins through bulk procurement contracts.

Product Innovation and Specialty Effects

Manufacturers continue to diversify their offerings with innovations such as metallic, glow-in-the-dark, granite, and translucent finishes. These effect clays allow consumers to create professional-grade results at home, stimulating repeat purchases. Eco-friendly trends are also reshaping product development; several producers have shifted towards phthalate-free and biodegradable additives to meet sustainability expectations. Continuous color and texture innovation enhances product differentiation, widens profit margins, and sustains consumer interest across seasonal cycles. These efforts collectively elevate polymer clay from a basic craft material to a specialized artistic medium.

Barrier Analysis - Price Sensitivity and Substitution Threats

The market faces pricing constraints due to competition from air-dry clays, silicone compounds, and other inexpensive modeling materials. Many consumers in emerging economies remain price-sensitive, preferring lower-cost or reusable alternatives. This limits manufacturers’ ability to raise prices despite rising raw-material and logistics costs. The resulting margin compression discourages new entrants and may restrain investment in research or product development over the forecast period.

Regulatory and Environmental Compliance

As polymer clay is a plastic-based material, regulatory scrutiny has intensified concerning microplastics and additive safety. Compliance with evolving standards, especially within the European Union and North America, requires costly testing, reformulation, and certification. Smaller manufacturers face significant financial strain in meeting these obligations. Furthermore, increasing consumer awareness regarding sustainability has led to growing demand for eco-friendly alternatives, compelling brands to allocate more resources toward material innovation.

Opportunity Analysis - Emergence of Premium and Sustainable Product Lines

The development of premium “effect” and eco-friendly polymer clays represents a lucrative growth opportunity. Metallic, stone-finish, and biodegradable glitter variants attract artists and professional crafters seeking high-performance materials. Premium SKUs already account for nearly 10% of global market value and are expected to rise further as sustainability becomes a purchasing criterion. Manufacturers introducing certified eco-safe and recyclable formulations are likely to achieve stronger brand differentiation and margin expansion.

Expansion into Educational and B2B Bulk Supply

Schools, creative academies, and art studios increasingly demand standardized kits that comply with safety norms. Bulk packaging solutions and curriculum-based craft kits can provide stable recurring revenue for suppliers. In high-population countries such as India and Indonesia, educational channels remain underpenetrated, offering considerable room for expansion. Establishing distribution partnerships with educational supply companies and leveraging digital procurement portals can significantly increase market reach.

E-commerce and Subscription Craft Kits

The rise of online craft marketplaces and subscription-box models presents scalable opportunities. Monthly art kits containing polymer clay projects encourage recurring purchases and brand loyalty. Direct-to-consumer fulfilment also improves profit margins by bypassing retail intermediaries. With the global e-commerce penetration rate in crafts exceeding 25%, this channel is expected to deliver the highest growth through 2032.

Category-wise Analysis

Product Form Insights

Solid polymer clay remains the dominant segment with a market share of 68.5% due to its broad versatility, user-friendly handling, and compatibility with standard home ovens. It is widely preferred by hobbyists, artists, and crafters for creating jewelry, figurines, decorative home items, and miniature sculptures. Major brands such as Sculpey and FIMO continue to focus on solid block formats, providing an extensive variety of colors, effects, and pre-packaged kits that cater to both beginners and professional users. In recent years, product developments have included pre-conditioned sets, themed project kits, and effect clays such as stone, metallic, and translucent finishes, which have enhanced the creative possibilities for consumers. These innovations have helped solid polymer clay maintain its strong market presence across retail stores and online platforms.

Liquid polymer clay is experiencing the fastest growth, largely due to its versatility in coatings, glazing, and detailed surface applications. It is increasingly used by jewelry designers, miniature artists, and professional crafters for creating glossy, polished finishes and fine detailing that cannot be achieved with solid clay alone. Recent developments in this segment include pre-mixed effect liquids, transparent and translucent variants, and hybrid formulas designed to combine with solid clay for complex layered designs. Companies have also introduced liquid clay pens and applicators for precision work, making it more accessible to both hobbyists and advanced users. The growing popularity of social media tutorials and DIY video content showcasing liquid clay techniques has further accelerated its adoption and encouraged creative experimentation.

Application Insights

The jewelry and arts & sculpture segment continues to lead the market with a share of 65.3% due to polymer clay’s strength, color diversity, and ability to retain fine details after baking. It is ideal for creating earrings, pendants, rings, small sculptures, and decorative figurines. Social media platforms such as Instagram and TikTok have played a crucial role in promoting jewelry-making and arts & craft projects, inspiring a surge in consumer interest. Recent product developments include themed jewelry kits, effect-based color palettes such as marble, metallic, and granite finishes, and ready-to-bake project packs that cater to both amateur hobbyists and professional designers. Educational kits for schools and workshops are driving growth by introducing polymer clay to new users and sustaining demand in the artistic segment.

The toys, miniatures, and novelty crafts segment is witnessing the highest growth rate within applications, driven by the rising popularity of DIY miniature kits, collectible figurines, and character-based craft sets. These products target younger audiences, hobby collectors, and enthusiasts who enjoy themed or seasonal projects. Recent developments include collaboration kits with popular animated characters, DIY subscription boxes for monthly projects, and interactive kits that combine polymer clay with other craft materials for mixed-media creations. Retailers and online marketplaces are increasingly promoting these products through social campaigns, tutorials, and influencer collaborations, which have significantly boosted adoption and engagement.

Regional Market Insights

North America Polymer Clay Market Trends - DIY Culture and E-Commerce Fuel Polymer Clay Innovation

North America continues to hold a significant share of the global polymer clay market, driven by a well-established consumer base that demonstrates strong interest in DIY projects, crafts, and creative hobbies. The U.S. dominates regional revenue, accounting for over 60% of North American sales, due to high per-capita spending on art supplies and the presence of a mature DIY ecosystem. Institutional demand is also substantial, supported by government and non-profit initiatives promoting arts education in schools and community programs. The regulatory landscape emphasizes product safety, with compliance required under ASTM and CPSIA standards, ensuring non-toxic and child-safe formulations.

Recent developments in North America include Sculpey’s launch of specialty effect clays in 2024, such as metallic and translucent variants targeted at professional crafters, and Makin’s USA introduction of educational classroom kits designed for large-scale institutional use. E-commerce continues to drive sales growth, with platforms such as Amazon and Etsy offering targeted DIY kits and subscription-based craft boxes. North American manufacturers are increasingly investing in premium formulations, digital tutorials, and online workshops, which not only enhance brand visibility but also educate consumers on advanced polymer clay techniques.

Europe Polymer Clay Market Trends-Premium Crafting and Sustainability Drive Market Demand

Europe represents a mature yet innovative market, distinguished by high product quality standards, structured retail networks, and a strong emphasis on design aesthetics. Countries such as Germany, the U.K., France, and Spain are key revenue contributors, reflecting the region’s established craft culture and high consumer engagement. European consumers demonstrate strong brand loyalty toward local manufacturers, notably Staedtler (FIMO), which has maintained a dominant position through continuous product innovation. Demand is supported by the popularity of artisanal crafts, home décor, and bespoke jewelry, with consumers increasingly seeking premium, eco-friendly, and child-safe products.

Regulatory frameworks such as REACH and EN-71 have prompted manufacturers to introduce phthalate-free clays and safer pigments, particularly for children’s craft applications. Recent developments include Staedtler’s launch of biodegradable glitter clays and seasonal effect palettes in 2024, designed to align with sustainability trends and consumer preferences for natural finishes.

Retailers in Europe also employ frequent product refreshes, offering limited-edition colors and textures to attract design-conscious buyers. The growth of online marketplaces and subscription-based DIY kits has enabled broader reach across the continent, enhancing accessibility while promoting creative engagement. Sustainability initiatives, such as locally sourced polymer resins and reduced packaging waste, are increasingly shaping manufacturer strategies and consumer choices.

Asia Pacific Polymer Clay Market Trends-Fast-Growing Market Backed by Arts Education and Exports

Asia Pacific is emerging as the fastest-growing regional market, driven by rising disposable incomes, increasing participation in DIY crafts, and the rapid expansion of art curricula in schools. China, Japan, India, and ASEAN countries collectively offer a vast consumer base that is becoming increasingly aware of global craft trends.

Competitive production costs, particularly the availability of PVC and polymer resins, provide regional manufacturers with an advantage, allowing them to serve both domestic markets and export opportunities. White-label production for Western brands is common, enabling local suppliers to integrate into global supply chains efficiently.

Recent developments include Shenzhen Polymer Crafts Co. expanding its production line for effect clays in 2024, targeting both domestic and export markets, and Craft Polymers Pvt. Ltd. launching DIY kits for schools in India, designed to support art education programs and nurture creative skills from a young age. E-commerce platforms such as Shopee, Flipkart, and Lazada have become critical channels, offering nationwide and international access for local brands. Government-backed initiatives promoting arts education in China, India, and Singapore have further bolstered institutional adoption. The development of localized packaging, bundled kits, and themed project sets has enhanced product accessibility, contributing to rising volumes.

Competitive Landscape

The global polymer clay market is moderately consolidated, with major international brands leading premium segments and regional players serving price-sensitive consumers. Developed markets remain brand-driven, while emerging economies show greater fragmentation due to private-label and contract manufacturing.

Competition centers on innovation, distribution reach, and regulatory compliance. Market leaders emphasize eco-friendly materials, safety certifications, and e-commerce expansion, while smaller firms focus on cost efficiency and partnerships. Growing demand for sustainable materials and educational uses is reshaping the industry’s strategic direction.

Companies Covered in Polymer Clay Market

- Polyform Products Company (Sculpey)

- Staedtler Mars GmbH & Co. KG (FIMO)

- Makin’s USA

- Laguna Clay Company

- Van Aken International

- Viva Decor GmbH

- American Art Clay Co. Inc. (AMACO)

- Macfarlane Group PLC

- The Clay and Paint Factory

- Craft Polymers Pvt. Ltd.

- Faber-Castell AG

- Linecross Ltd.

- Creative Industries Co.

- Shenzhen Polymer Crafts Co.

- Hobbycraft Group Ltd.

- Arteza Inc.

- Crayola LLC

- Pentel Co., Ltd.

- Daiso Industries Co., Ltd.

- Colorificio Monetti S.p.A.

Frequently Asked Questions

The market size is estimated to be US$320 Million.

The polymer clay market is projected to reach US$458.9 Million by 2032.

Key trends include the growing popularity of DIY and hobbyist crafts, the expansion of educational and institutional applications, product innovations with effect finishes, sustainability initiatives, and increasing sales through e-commerce and subscription-based craft kits.

The leading segment by product form is Solid Polymer Clay, preferred for its versatility, ease of handling, and availability in retail and online channels. By application, the jewelry and arts & sculpture segment dominates the market due to high consumer demand and social media-driven DIY trends.

The polymer clay market is expected to grow at a CAGR of 5.1% between 2025 and 2032.