- Specialty & Fine Chemicals

- Polymerization Inhibitor Market

Polymerization Inhibitor Market Size, Share, and Growth Forecast, 2025 - 2032

Polymerization Inhibitor Market by Product Type (Phenolic Inhibitors, Amines, Nitroxides, Quinones, Others), Application (Petrochemicals, Plastics, Pharmaceuticals, Paints and Coatings, Others), End-use (Chemical, Automotive, Healthcare, Construction, Others), and Regional Analysis for 2025 - 2032

Polymerization Inhibitor Market Size and Trend Analysis

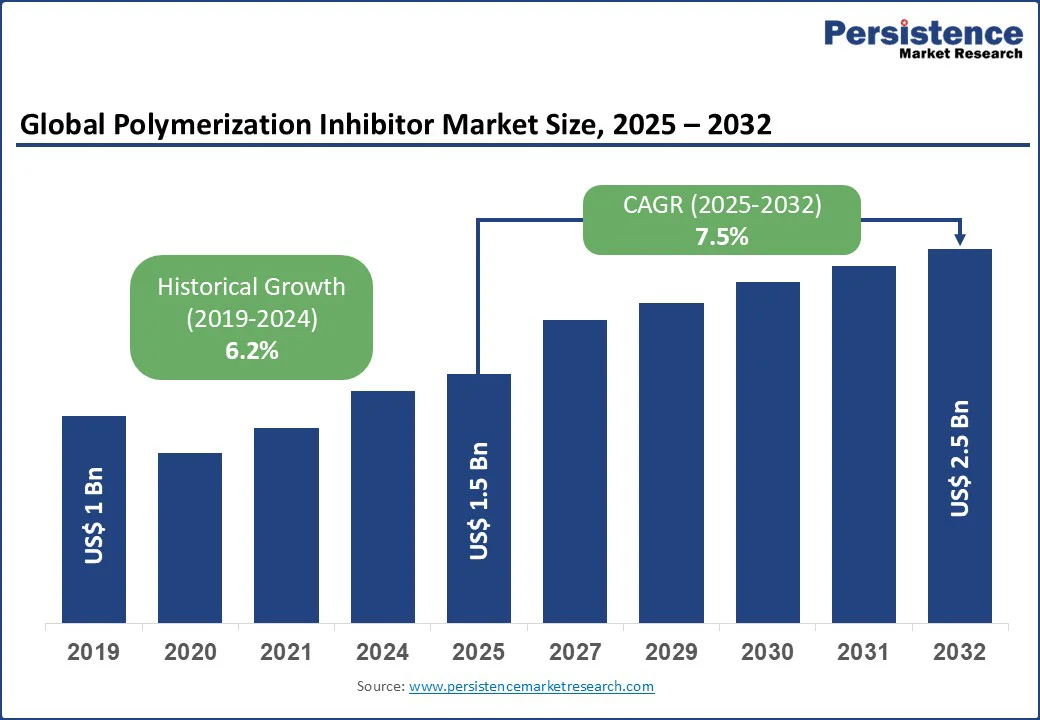

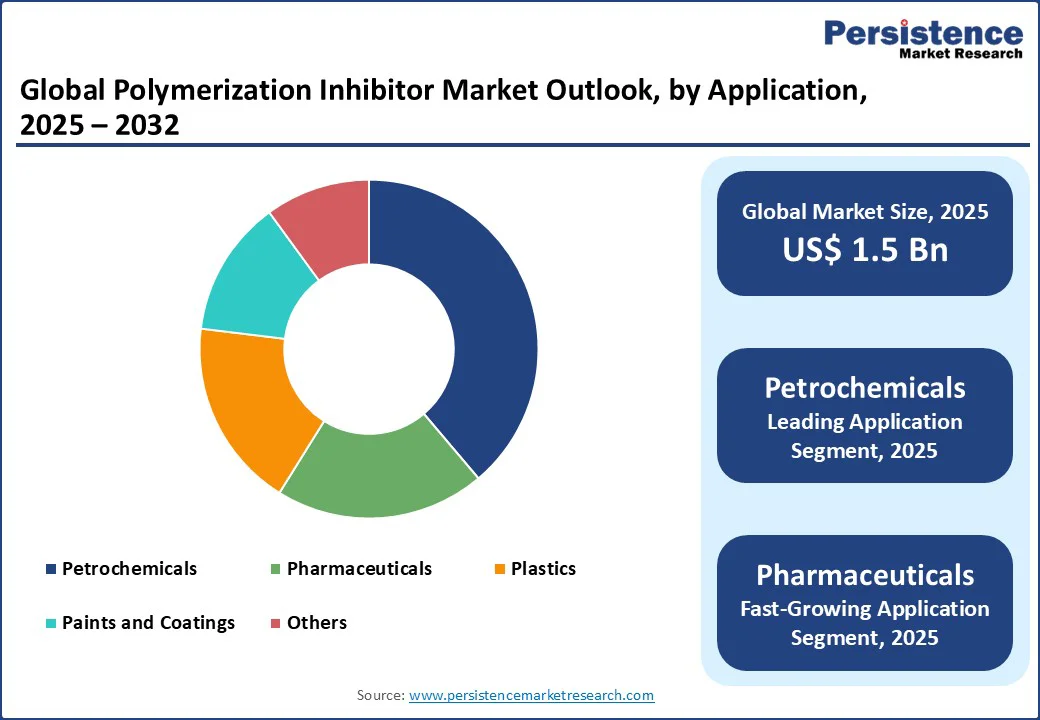

The global polymerization inhibitor market size is likely to value US$1.5 Bn in 2025 and reach US$2.5 Bn by 2032, growing at a CAGR of 7.5% during the forecast period from 2025 to 2032.

Key Industry Highlights:

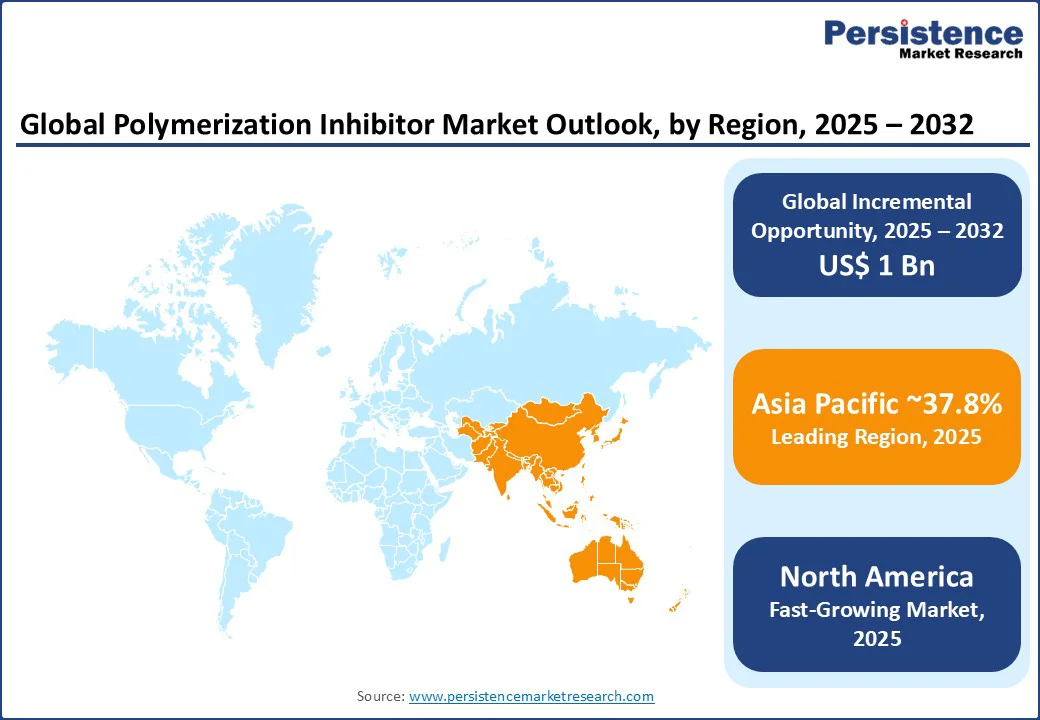

- Leading Region: Asia Pacific holds a 37.8% share in 2025 of the polymerization inhibitor market, driven by rapid industrialization, high chemical production, and expanding pharmaceutical sectors in China and India.

- Fastest-growing Region: North America is the fastest-growing region, fueled by robust demand from the petrochemical and healthcare industries in the U.S. and Canada.

- Investment Plans: China’s 14th Five-Year Plan (2021-2025) emphasizes chemical industry growth, boosting demand for polymerization inhibitors in petrochemical applications. Goals include extending the petrochemical industry chain and achieving bulk chemical products utilization rates exceeding 80%, with 30 smart manufacturing demonstration plants and 50 smart chemical demonstration parks by 2025.

- Dominant Product Type: Phenolic inhibitors account for nearly 40.4% market share of the polymerization inhibitor market, due to their effectiveness in stabilizing monomers in petrochemical and plastics applications.

- Leading Application: Petrochemicals contribute over 38.7% of market revenue, driven by global demand for stable monomers in fuel and chemical production.

| Global Market Attribute | Key Insights |

|---|---|

| Polymerization Inhibitor Market Size (2025E) | US$ 1.5Bn |

| Market Value Forecast (2032F) | US$ 2.5Bn |

| Projected Growth (CAGR 2025 to 2032) | 7.5% |

| Historical Market Growth (CAGR 2019 to 2024) | 6.2% |

The polymerization inhibitor market is experiencing robust growth, driven by increasing demand from key industries such as petrochemicals, plastics, and pharmaceuticals, where prevention of unwanted polymerization is critical for product stability and safety.

Market Dynamics

Driver: Growing Demand in Petrochemical and Pharmaceutical Industries Fuels Market Expansion

The global polymerization inhibitor market is experiencing significant growth due to surging demand from the petrochemical and pharmaceutical industries. Polymerization inhibitors are critical for preventing unwanted polymerization of reactive monomers, ensuring product stability during storage and transportation.

In petrochemicals, inhibitors such as phenolic compounds and nitroxides are used to stabilize monomers such as styrene and butadiene, which are essential for producing fuels and chemicals. According to the IEA’s report “The Future of Petrochemicals”, petrochemicals are projected to account for more than a third of the growth in global oil demand by 2030, and nearly half of the growth by 2050, adding roughly 7 million barrels of oil per day, driving demand for inhibitors.

In pharmaceuticals, inhibitors ensure the stability of active ingredients, supporting drug safety and efficacy. The global pharmaceutical market, valued at $1.5 trillion in 2023 per WorldMetrics.org, relies on inhibitors for quality control.

Companies such as BASF SE and Solvay report increased sales of inhibitors for these applications in 2024. Rising industrialization and stringent safety regulations ensure sustained demand, positioning petrochemicals and pharmaceuticals as key drivers for market growth through 2032.

Restraint: High Costs and Environmental Concerns Limit Adoption

The polymerization inhibitor market faces challenges due to the high costs of advanced inhibitors and growing environmental concerns. Developing eco-friendly and high-performance inhibitors, such as nitroxides and bio-based compounds, involves significant R&D and production costs, increasing prices for end-users. In 2023, the cost of advanced inhibitors rose, impacting adoption in cost-sensitive markets.

Additionally, some traditional inhibitors, such as DNBP, pose environmental and health risks due to their toxicity, leading to stricter regulations in regions such as Europe. The European Chemicals Agency (ECHA) has flagged certain inhibitors for potential restrictions, pushing manufacturers toward sustainable alternatives.

Competition from alternative stabilization methods, such as physical process controls, further hinders market growth. These factors create pricing pressures and limit adoption, particularly in emerging economies, restraining overall market expansion.

Opportunity: Rising Demand for Eco-Friendly and Bio-Based Inhibitors

The increasing focus on sustainability and environmental regulations presents significant opportunities for the polymerization inhibitor market. Industries are shifting toward eco-friendly and bio-based inhibitors to comply with stringent regulations and reduce environmental impact. The global push for green chemistry, supported by initiatives such as the EU’s Green Deal, drives demand for biodegradable inhibitors in petrochemicals and plastics.

Companies such as Arkema Group and Clariant AG are innovating with bio-based phenolic and amine inhibitors for pharmaceutical and coating applications. The pharmaceutical sector, with a growing focus on sustainable production, is adopting these inhibitors to meet regulatory standards.

Government incentives, such as tax breaks for green technologies in North America, further encourage investments. These trends create opportunities for manufacturers to develop advanced, eco-friendly inhibitors to meet evolving industry needs through 2032.

Category-wise Insights

By Product Type

- Phenolic inhibitors hold the largest market share in the polymerization inhibitor market, approximately 40.4% in 2025, due to their high effectiveness in stabilizing monomers in petrochemical and plastics applications. Widely used for monomers such as styrene, phenolic inhibitors, offered by companies such as BASF SE and Eastman Chemical, ensure product stability during storage and transportation. Their versatility and compatibility with various industrial processes make them a preferred choice across the chemical and automotive sectors.

- Nitroxides are the fastest-growing product type, driven by their high efficiency in preventing free-radical polymerization in high-temperature environments. Their use in pharmaceuticals and plastics, where precise control is critical, is expanding rapidly. Companies such as Evonik Industries and Adeka Corporation are innovating with nitroxide-based solutions, catering to demand in North America and the Asia Pacific, supported by advancements in formulation technologies.

By Application

- The petrochemical sector accounts for over 38.7% polymerization inhibitor market in 2025, driven by the global demand for stable monomers in fuel and chemical production. Polymerization inhibitors are critical for preventing unwanted reactions in monomers such as styrene and butadiene, used in refineries. Major players such as Solvay and LANXESS AG supply inhibitors for petrochemical applications, with strong demand in the Asia Pacific and the Middle East.

- The pharmaceutical sector is the fastest-growing application, propelled by the need for inhibitors to ensure the stability of active ingredients in drug production. The global pharmaceutical industry’s expansion, particularly in emerging markets, drives demand for high-performance inhibitors. Companies such as Clariant AG and Innospec Inc. are developing specialized solutions for pharmaceutical applications, supporting growth in North America and Europe.

By End-use

- The chemical industry holds the largest market share of approximately 36.8% in 2025, driven by its extensive use of polymerization inhibitors in monomer stabilization and chemical processing. Inhibitors ensure product quality in the production of plastics, resins, and intermediates. Companies such as BASF SE and Arkema Group lead with comprehensive portfolios, catering to demand in the Asia Pacific and North America.

- The healthcare sector is the fastest-growing end-use, fueled by the increasing demand for inhibitors in pharmaceutical manufacturing to ensure drug stability and safety. The global rise in healthcare investments, particularly in the U.S. and India, supports this segment’s growth. Companies such as Solvay and Croda International are innovating with eco-friendly inhibitors, aligning with regulatory trends in healthcare applications.

Regional Insights

Asia Pacific Polymerization Inhibitor Market Trends

Asia Pacific is poised to dominate the global polymerization inhibitor market, capturing an estimated 37.8% share by 2025, fueled by rapid industrialization and high chemical output. China, recognized as a global chemical manufacturing powerhouse, significantly drives demand for polymerization inhibitors, as noted by the China Petroleum and Chemical Industry Federation. Simultaneously, India’s growing pharmaceutical sector, valued at $50 billion in 2023 according to the India Brand Equity Foundation, amplifies inhibitor usage in drug synthesis and formulation.

The robust expansion of the region’s petrochemical and plastics industries further accelerates market growth, with key players such as Dorf Ketal and Adeka Corporation increasing regional investments. Moreover, government policies, notably China’s 14th Five-Year Plan, prioritize high-quality industrial development, fostering innovation and sustainability in chemical processes. Collectively, these factors ensure that the Asia Pacific will maintain its market leadership and experience sustained growth in polymerization inhibitor demand through 2032.

North America Polymerization Inhibitor Market Trends

North America is emerging as the fastest-growing region in the global polymerization inhibitor market, driven by strong demand from the petrochemical and healthcare industries in both the U.S. and Canada. In the U.S., the expansive petrochemical sector relies heavily on polymerization inhibitors to ensure monomer stability during processing, particularly in large-scale plastic and resin production.

Meanwhile, Canada’s pharmaceutical industry, supported by advanced manufacturing capabilities and a focus on innovation, contributes to growing demand for high-performance inhibitors in drug formulation and chemical synthesis.

Leading market players such as Eastman Chemical Company and Innospec Inc. maintain a dominant presence, offering broad product portfolios and well-established distribution networks that cater to industrial, healthcare, and consumer applications.

Furthermore, rising consumer preference for sustainable and low-toxicity inhibitors, along with stringent safety and environmental regulations, is pushing innovation and adoption of next-generation formulations. These combined factors position North America for sustained, rapid market growth through 2032.

Europe Polymerization Inhibitor Market Trends

Europe stands as the second fastest-growing region, propelled by stringent regulatory frameworks and increasing demand across pharmaceuticals and petrochemicals. Key countries such as Germany and France lead this growth, with Germany’s robust chemical industry heavily relying on phenolic inhibitors to ensure product stability and quality. Industry giants such as BASF SE and Clariant AG play pivotal roles in supplying advanced inhibitor solutions tailored to stringent market needs.

The European Union’s Green Deal further accelerates this expansion by encouraging sustainable and eco-friendly chemical processes, driving demand for greener polymerization inhibitors in the petrochemical, coating, and plastics sectors.

Europe’s commitment to high-quality standards and regulatory compliance ensures continuous innovation, as companies focus on safer, more efficient inhibitor technologies. These factors combined solidify Europe’s position as a dynamic market, set to witness steady growth through 2032, balancing environmental goals with industrial advancement.

Competitive Landscape

The global polymerization inhibitor market is highly competitive, characterized by a fragmented landscape with numerous domestic and international players. Leading companies such as BASF SE, Arkema Group, Solvay S.A., and Evonik Industries dominate through extensive product portfolios and global distribution networks.

Regional players such as Dorf Ketal Chemicals, focus on localized offerings in the Asia Pacific. Companies are investing in R&D to develop eco-friendly and high-performance inhibitors, driven by demand in petrochemicals and pharmaceuticals. Strategic collaborations and partnerships are prevalent, enabling firms to expand their market presence and cater to evolving industry needs.

Key Industry Developments:

- January 2024: Nouryon completed a significant expansion of its production capacity for Levasil colloidal silica products at its Green Bay, Wisconsin facility. This nearly 50% increase in capacity was undertaken to address the rising global demand for colloidal silica, a vital material used across diverse industries. Levasil colloidal silica serves as a critical additive in polymerization processes, enhancing the stability, durability, and overall performance of polymers.

- December 2023: Arkema finalized its acquisition of Dow's flexible packaging laminating adhesives business for $150 million, making Arkema a leading player in this market and expanding its offerings in adhesives and functional materials. The acquisition includes advanced technologies, global facilities, and a strong revenue base, which will allow Arkema to offer a more complete range of solutions to customers in the growing flexible packaging segment, aligning with the company's strategy to expand in high-technology markets.

Companies Covered in Polymerization Inhibitor Market

- BASF SE

- Arkema Group

- Solvay S.A

- Evonik Industries AG

- Clariant AG

- LANXESS AG

- Albemarle Corporation

- Eastman Chemical Company

- Dorf Ketal Chemicals India Private Limited

- Innospec Inc.

- Croda International Plc

- Adeka Corporation

- Others

Frequently Asked Questions

The Polymerization Inhibitor market is projected to reach US$1.5 Bn in 2025.

Growing demand in the petrochemical and pharmaceutical industries, and advancements in eco-friendly inhibitors are the key market drivers.

The Polymerization Inhibitor market is poised to witness a CAGR of 7.5% from 2025 to 2032.

The rising demand for eco-friendly and bio-based inhibitors is the key market opportunity.

BASF SE, Arkema Group, Solvay S.A., and Evonik Industries AG are key market players.