- Medical Devices

- Medical X-Ray Detectors Market

Medical X-Ray Detectors Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Medical X-Ray Detectors Market by Product Type (Indirect Flat-Panel Detectors, Direct Flat-Panel Detectors, Computed Radiography (CR) Detectors), Panel Size (Large-Area Flat-Panel Detectors, Small-Area Flat-Panel Detectors), Modality (Portable Detectors, Fixed Detectors), End-user, Regional Analysis, from 2026 - 2033

Medical X-ray Detectors Market Share and Trends Analysis

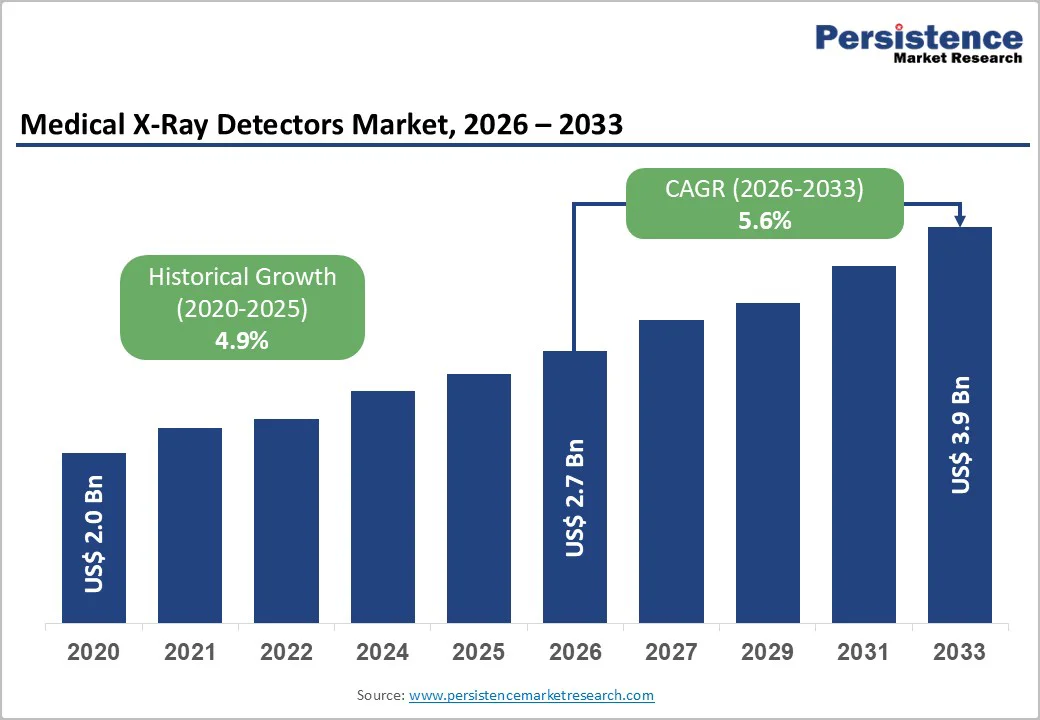

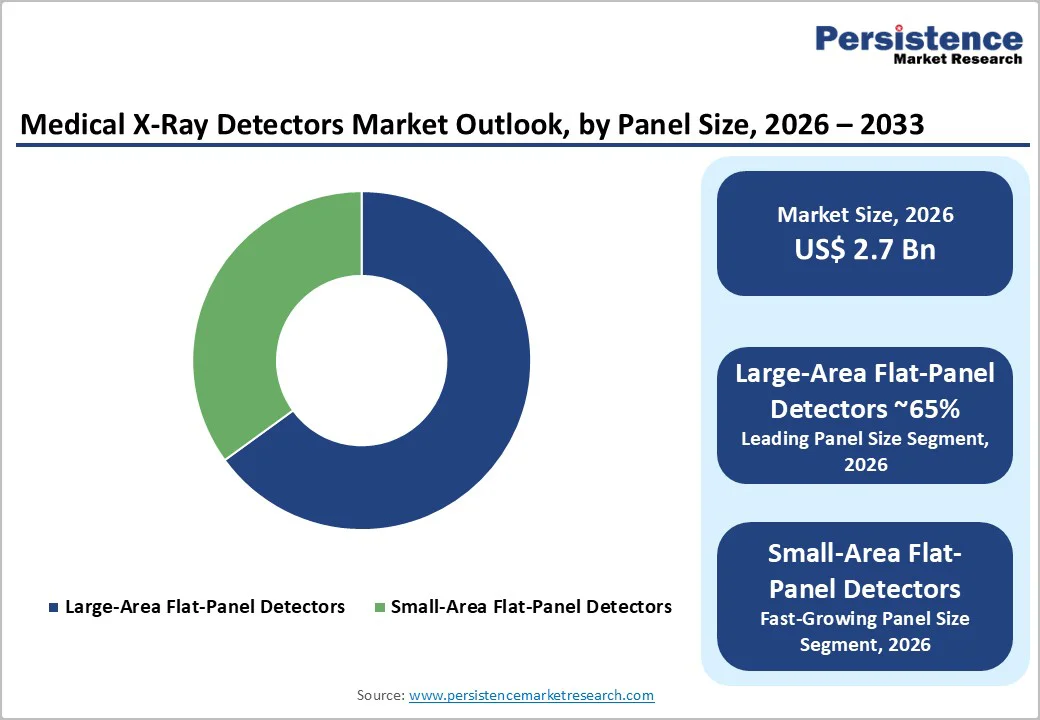

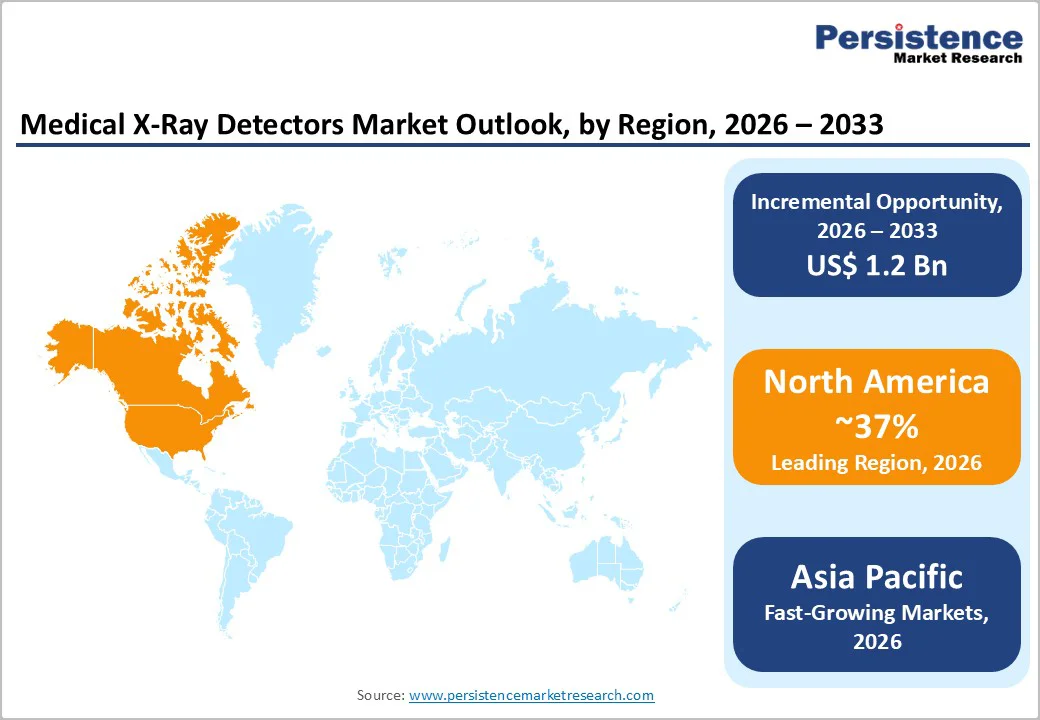

The global medical X-ray detectors market size is estimated to grow from US$ 2.7 billion in 2026 to US$ 3.9 billion by 2033, growing at a CAGR of 5.6% during the forecast period from 2026 to 2033. The global market is witnessing accelerated growth driven by hospital digitalization, increased procedural volumes, and a shift from analog and computed radiography systems to flat-panel detectors.

Rising chronic disease burden, trauma cases, and aging demographics strengthen the need for high-resolution imaging in routine and advanced diagnostics. Large-area, wireless, and low-dose detectors are gaining prominence due to faster workflow, sharper image quality, and integration with PACS and AI-supported platforms. Replacement cycles, regulatory push for dose compliance, and investments in enterprise radiology infrastructure further elevate adoption across hospitals, ambulatory centers, and diagnostic networks, reinforcing sustained market expansion.

Key Industry Highlights:

- Leading Region: North America leads the medical X-ray detectors market, supported by advanced diagnostic infrastructure, rapid CR-to-DR replacement, and favorable reimbursement for digital imaging upgrades.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, driven by large patient volumes, public hospital modernization, and government-supported digital health initiatives replacing analog systems.

- Dominant Segment: Large-area flat-panel detectors remain dominant due to wide coverage in chest, spine, trauma, and general radiography, enabling faster turnaround and higher throughput.

- Fastest Growing Segment: Small-area flat-panel detectors are the fastest-growing segment, driven by rising portable system deployments, ER/ICU mobility needs, and their suitability for extremity and bedside imaging.

| Key Insights | Details |

|---|---|

|

Medical X-Ray Detectors Market Size (2026E) |

US$ 2.7 Bn |

|

Market Value Forecast (2033F) |

US$ 3.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.9% |

Market Dynamics

Driver - Rise in Diagnostic Imaging Volumes for Chronic Conditions

The growing prevalence of chronic conditions such as cardiovascular diseases, cancer, orthopedic injuries, and respiratory ailments is driving a significant increase in demand for high-performance medical X-ray detectors. These detectors are critical for timely and accurate diagnosis, enabling clinicians to detect diseases early and improve patient outcomes. According to WHO data, diagnostic imaging procedures, including X-rays, account for over 70% of radiology exams in high-volume healthcare settings. Chest and musculoskeletal imaging dominate due to aging populations, trauma incidence, and the increasing burden of chronic diseases. This surge in diagnostic requirements has prompted hospitals and imaging centers to invest in modern X-ray detectors capable of handling higher patient throughput without compromising image quality.

Flat-panel detectors, compared to legacy systems, offer faster image acquisition and enhanced spatial resolution, which is essential in busy radiology departments. Their efficiency supports higher workflow capacity, reducing patient waiting times and enabling rapid clinical decision-making. Reports from the International Atomic Energy Agency (IAEA) highlight growing adoption in emerging markets, where procedural volumes are expanding. This combination of rising disease prevalence and procedural demand creates sustained opportunities for investments in advanced X-ray detector technologies, aligning with global public health initiatives focused on early detection and efficient diagnostic care.

Restraints - Stringent Regulatory Approvals and Compliance Burdens

Medical X-ray detector manufacturers face significant challenges in navigating complex regulatory frameworks that can slow product launches and increase development costs. Securing FDA 510(k) clearance, EU MDR certification, and adhering to IAEA dosimetry standards requires substantial time and resources, particularly for new technologies or portable modalities. Compliance demands extend to evolving requirements such as unique device identification (UDI) and comprehensive post-market surveillance, which complicate global supply chains and affect manufacturers’ operational efficiency.

Variability in national regulatory guidelines further hampers seamless market entry, making it difficult for new entrants or smaller players to compete effectively. Companies must invest in dedicated regulatory teams and compliance infrastructure to meet these diverse standards. This complexity often favors established players with experience and resources to navigate international requirements, while smaller or emerging manufacturers may delay innovation or avoid certain markets altogether. Consequently, regulatory hurdles act as a significant restraint, slowing technology adoption, limiting product availability in some regions, and increasing overall costs for both manufacturers and healthcare providers.

Opportunity - AI-integrated Large-Area Detectors for High-Volume Applications

Large-area flat-panel detectors represent a key growth opportunity in the medical X-ray market. These detectors provide full-field imaging capabilities that are particularly suitable for high-volume applications, including chest, spine, trauma, oncology, and cardiology imaging. Their superior signal-to-noise ratios (SNR) and high spatial resolution enable faster and more accurate diagnostics, which is critical in busy hospital environments. Integration with AI technologies offers additional advantages, such as automated lesion detection, workflow optimization, and dose management, enhancing clinical efficiency and patient safety.

Hybrid platforms, such as Canon’s combination of radiography and fluoroscopy, demonstrate the convergence of imaging modalities into space-efficient systems, enabling healthcare facilities to upgrade existing infrastructure without requiring extensive remodeling. Furthermore, government initiatives in regions like the Asia Pacific to enhance digital health infrastructure, coupled with IAEA endorsements for pediatric dose reference levels (DRLs), create favorable conditions for adoption. As older computed radiography (CR) systems are retired, these AI-enhanced large-area detectors are poised to capture a significant share of procedural volumes. The growing focus on high-throughput imaging, early detection, and workflow efficiency positions this segment as a strategic opportunity for manufacturers to expand market penetration and deliver advanced diagnostic solutions in both mature and emerging healthcare markets.

Category-wise Analysis

By Product Type Insights

Direct flat-panel detectors account for nearly 41% share in 2025, maintaining leadership due to clarity, speed, and dose efficiency. Their direct conversion technology, typically using amorphous selenium, eliminates intermediary scintillation layers, thereby reducing scatter and preserving anatomical boundaries with high modulation transfer performance. These attributes make them ideal for precise visualization in mammography, orthopedic load-bearing joints, and fine-contrast fluoroscopic assessments. Many FDA-cleared systems demonstrate notable equivalence in dose, signal quality, and workflow metrics, further driving hospital preference. Direct panels streamline connectivity with PACS, RIS, and integrated radiography consoles, supporting rapid reading cycles and structured reporting. In high-volume hospitals, faster capture-to-review intervals translate into improved room utilization and lower patient waiting times, strengthening their favorable economics. Additionally, lifecycle cost savings from reduced retakes and improved first-image accuracy drive replacement of older indirect panels and CR systems, reinforcing their adoption across tertiary care facilities and advanced radiology sites.

By Panel Size Insights

Large-area flat-panel detectors lead with approximately 65% share in 2025 due to their suitability for full-body and multi-region imaging. Their wider coverage supports routine chest, abdomen, spine, and emergency views without repositioning, reducing exposure cycles and improving patient comfort. They deliver strong signal-to-noise ratios through low-noise electronics and high-efficiency conversion layers, ensuring sharper contrast in both soft-tissue and bone examinations. Healthcare providers favor these detectors for standardized protocols, especially in trauma units, pre-operative assessments, and intensive-care workflows requiring quick bedside turnaround. Regulatory frameworks encourage their use because distribution remains uniform across larger fields, aiding compliance with pediatric and adult exposure reference values. Hospitals benefit from simplified equipment upgrading since standardized formats facilitate retrofitting into existing rooms. Their contribution to higher throughput, minimal motion artifacts, faster digital processing, and fewer retakes positions large-area detectors as preferred replacements for small-area panels in centralized radiology departments and multi-modality diagnostic units.

Region-wise Insights

North America Medical X-Ray Detectors Market Trends

North America remains at the forefront of medical X-ray detector adoption, driven by structured reimbursement, rapid digitalization, and hospitals replacing legacy analog systems. The U.S. maintains leadership supported by strong regulatory pathways that expedite product upgrades through standardized FDA 510(k) clearances. Continuous product enhancements in wireless and hybrid detector configurations have strengthened adoption across emergency, ICU, orthopedic, and mammography environments.

Facilities focus on platforms that deliver lower dose exposure, faster image turnaround, and cloud-based reporting, improving diagnostic workflows and compliance with safety metrics. Medicare-linked pressure to retire analog and CR systems further incentivizes the procurement of flat-panel detectors with automatic exposure optimization. Major suppliers expand U.S. manufacturing, licensing, and integrated service models, ensuring maintenance continuity in multisite networks. High disease burden in oncology, osteoporosis, and metabolic disorders sustains usage for routine monitoring. Furthermore, integration with enterprise imaging platforms, enhanced mobile carts, and interoperable radiography systems ensures continued market dominance within North America.

Asia Pacific Medical X-Ray Detectors Market Trends

Asia Pacific shows accelerated expansion led by infrastructure scale-up and direct government focus on digital imaging procurement. China remains the manufacturing and export hub, supplying cost-efficient large-area detectors to local and regional hospitals undergoing modernization programs. Public health reimbursements in China and provincial grants in Tier II–III cities support the swift replacement of CR systems in high-volume diagnostic centers. Japan advances specialized precision detectors suited for women’s health and oncology screening, driven by strong clinical standards and aging demographics. India shows rising consumption tied to hospital capacity growth, radiology outsourcing, and stronger medical tourism volumes, especially for orthopedic, cardiac, and trauma imaging. ASEAN markets benefit from foreign investments that prioritize wireless detectors to serve mobile radiography fleets. Local service partnerships, rapid installation cycles, and fleet-based maintenance models support adoption in mid-tier facilities. Digital health mandates and standardized PACS connectivity strengthen uptake of flat-panel detectors, positioning the Asia Pacific as the fastest-growing regional market.

Competitive Landscape

The global medical X-ray detectors market is moderately consolidated, dominated by key players such as Agfa-Gevaert, Fujifilm, Canon, Rayence, and Hamamatsu. These companies prioritize research and development to enhance wireless functionality, image quality, and panel efficiency. Strategies focus on obtaining regulatory approvals, forming OEM partnerships, and ensuring supply chain security through vertical integration. Market differentiation is driven by superior dose efficiency, high detector quantum efficiency (DQE), and modular designs. Additionally, subscription-based models for system upgrades and cloud-based analytics are emerging, supporting hospitals and imaging centers in managing replacement cycles and optimizing operational efficiency.

Key Industry Developments:

- In November 2024, Detection Technology, a global X-ray detector solutions leader, showcased its complete range of flat-panel X-ray detectors at RSNA 2024, aiming to enhance medical imaging capabilities.

- In 2021, Fujifilm launched the FDR Xair, an ultra-light portable X-ray unit designed with advanced digital imaging capabilities to support improved patient care across diverse clinical environments.

Companies Covered in Medical X-Ray Detectors Market

- Agfa-Gevaert N.V.

- Onex Corporation

- FUJIFILM Holdings Corporation

- Analogic Corporation

- Canon Inc

- DRTECH Corporation

- Hamamatsu Photonics k.k

- Konica Minolta, Inc.

- Rayence Co., Ltd.

- Teledyne Technologies Incorporated

- Others

Frequently Asked Questions

The global medical x-ray detectors market is projected to be valued at US$ 2.7 Bn in 2026.

Growing imaging volumes, chronic disease burden, hospital digital upgrades, faster diagnosis needs, workflow efficiency, and advanced flat-panel system adoption.

The global medical x-ray detectors market is poised to witness a CAGR of 5.6% between 2026 and 2033.

AI-enabled large-area panels, detector replacement cycles, hybrid fluoroscopy platforms, pediatric dose optimization, and expanding imaging centers in emerging economies.

Key companies include Agfa-Gevaert N.V., Onex Corporation, FUJIFILM Holdings Corporation, and Analogic Corporation.