- Medical Devices

- Latin America Capnography Equipment Market

Latin America Capnography Equipment Market Size, Trends, Share, Growth, and Regional Forecast, 2026 to 2033

Latin America Capnography Equipment Market by Product (Mainstream Capnographs, Sidestream Capnographs, Microstream Capnographs, Capnography Disposables), Modality (Handheld Devices, Standalone Devices), End-user, and Regional Analysis from 2026 to 2033

Latin America Capnography Equipment Market Share and Trends Analysis

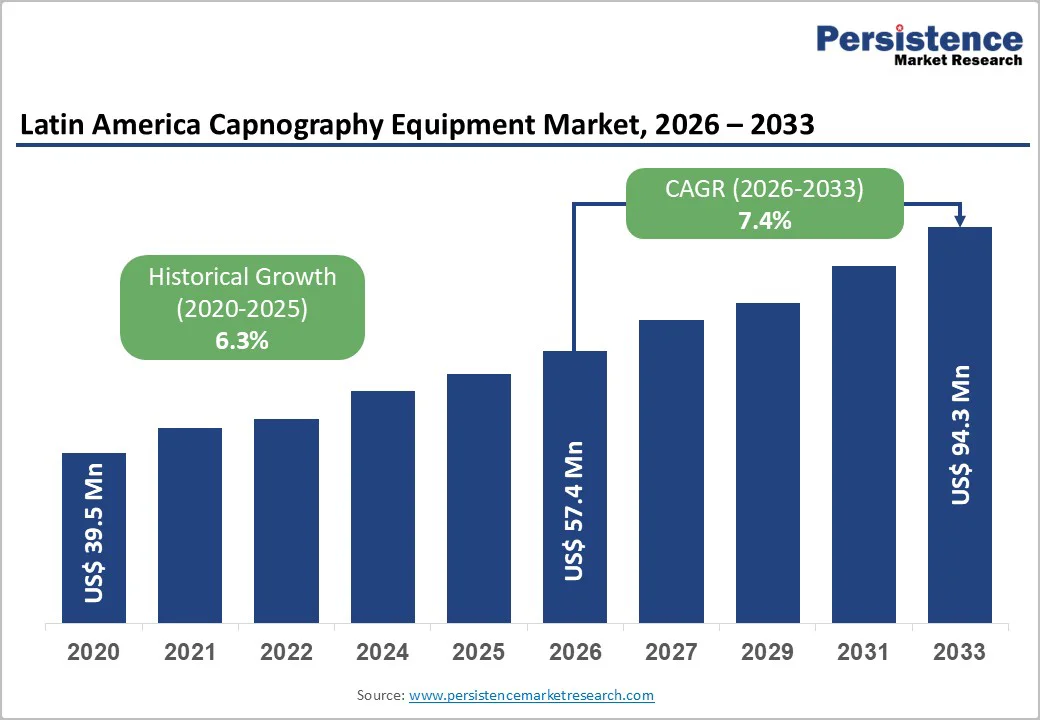

Latin America capnography equipment market size is estimated to reach US$ 57.4 Million in 2026 and is projected to reach US$ 94.3 Million by 2033, growing at a CAGR of 7.4% between 2026 and 2033.

As healthcare systems prioritize safer sedation practices, improved respiratory monitoring, and enhanced perioperative care, this has contributed to the growth. Rising cases of respiratory illnesses, growing surgical and emergency procedure volumes, and broader adoption of patient-safety protocols are strengthening demand for capnography across hospitals and ambulatory centers. Increasing uptake of minimally invasive and outpatient procedures also fuels the need for reliable CO2 monitoring, particularly in resource-diverse settings. Supported by gradual technology upgrades and expanding clinical awareness, the region continues to move toward wider integration of capnography as a standard-of-care monitoring tool.

Key Industry Highlights

- Leading Country: Brazil dominates the Latin America market with 42.8%, driven by rising plastic-surgery and medical-tourism demand, increased cardiac procedures, and high healthcare GDP spend in Brazil.

- Leading Product: Sidestream Capnographs lead with 44.1% share, supported by their ease-of-use, ability to monitor non-intubated patients, and broad availability from many local/regional manufacturers

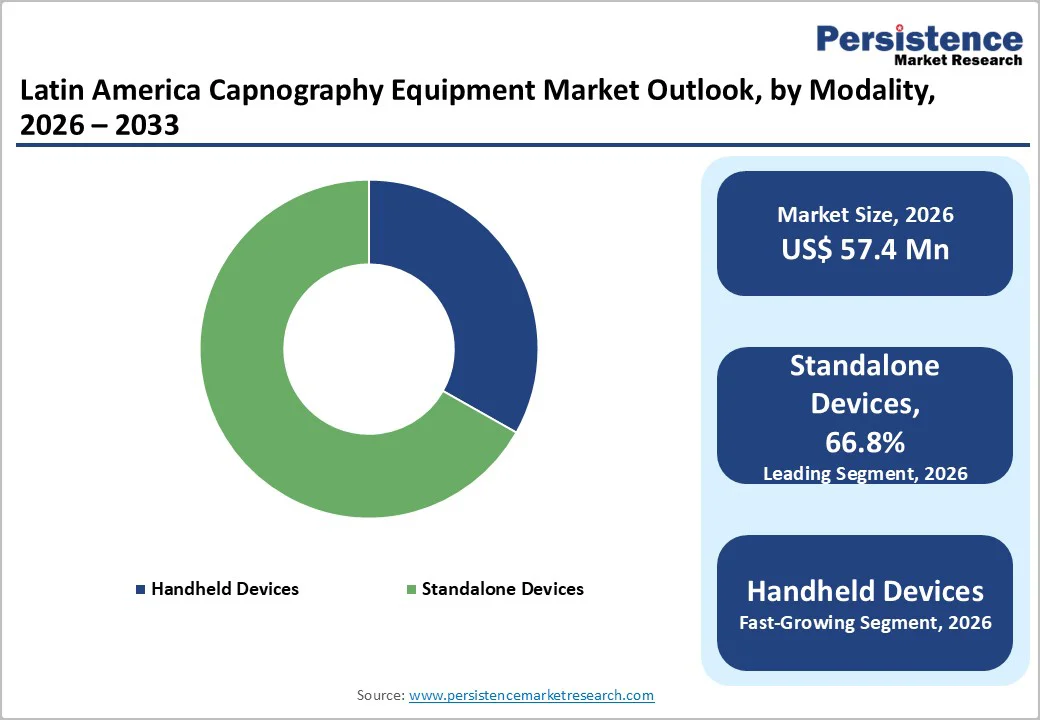

- Leading Modality: Standalone Devices dominate with 66.8%, driven by hospitals’ preference for independent capnographs for anaesthesia, sedation, and ICU use - offering flexibility without integration requirements

- Leading End-user: Hospitals lead with 52.5% share, due to high procedural volumes (surgery, sedation, ICU), regulatory recommendations for capnography in routine hospital settings, and hospitals’ capacity to invest in monitoring equipment.

| Key Insights | Details |

|---|---|

| Latin America Capnography Equipment Market Size (2026E) | US$ 57.4 Million |

| Market Value Forecast (2033F) | US$ 94.3 Million |

| Projected Growth (CAGR 2026 to 2033) | 7.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.3% |

Market Dynamics

Driver - Growing Respiratory Disease Burden and Higher Sedation Volumes Propel Capnography Adoption

The demand for capnography equipment in Latin America is steadily rising as respiratory disorders become a major public-health concern across the region. Conditions such as asthma and Chronic Obstructive Pulmonary Disease (COPD) with prevalence rate of 5%-20% (Asthma) & 8.9% (COPD) continue to affect a large share of the adult population, especially smokers and aging individuals, placing additional pressure on healthcare systems that already spent heavily on hospital admissions, emergency management, and long-term therapies. Growing emphasis on early detection of ventilation issues and accurate CO2 tracking is pushing hospitals and clinics to adopt capnography as part of routine monitoring.

At the same time, the region has witnessed a sharp increase in sedation-based procedures, including cosmetic and minimally invasive surgeries, which require continuous respiratory surveillance to avoid complications during moderate or deep sedation. This has strengthened the relevance of sidestream and mainstream capnography devices across surgical suites, emergency units, and ambulatory centers.

Supportive recommendations from anesthesiology societies and regional health authorities further reinforce the integration of capnography into standard practice, particularly for airway management, endotracheal tube verification, and prevention of hypoventilation-related events. As technology becomes more compact, reliable, and user-friendly, adoption is expected to accelerate across both large tertiary hospitals and smaller care facilities. Together, rising clinical need and expanding procedural intensity position capnography as a vital monitoring tool in Latin America’s evolving healthcare landscape.

Restraints - Budget Pressures and Limited Clinical Awareness Restrict Capnography Penetration

Despite its growing clinical importance, several structural and economic challenges continue to restrict widespread deployment of capnography systems across Latin America. Public hospitals, which manage a significant share of patient volume in the region, often operate under tight budgets that prioritize essential services over advanced monitoring technologies. As a result, procurement cycles are slow, and many facilities delay upgrades even when devices are clinically recommended.

In addition, smaller clinics and outpatient centers-particularly those in semi-urban and rural areas-lack adequate training or awareness regarding the benefits of capnography for sedation safety or respiratory evaluation. Limited exposure to updated clinical guidelines often leads practitioners to rely solely on pulse oximetry, underestimating the value of real-time CO2 monitoring. High operational costs associated with consumables, maintenance, and replacement parts can further discourage adoption among resource-constrained providers.

Fragmented reimbursement policies across countries also affect purchasing decisions, as not all monitoring equipment is covered by insurance programs or government funding. This combination of financial barriers and knowledge gaps results in uneven adoption across the region, with advanced facilities progressing faster than smaller institutions. Unless affordability improves and clinical awareness deepens, the market’s potential may remain only partially realized.

Opportunity - Growing Ambulatory Care, Private Investment, and Medical Tourism

Several emerging trends are opening new avenues of growth for capnography equipment suppliers in Latin America. The increasing shift toward ambulatory care, day-surgery centers, and office-based procedures has created strong interest in compact, portable, and handheld capnographs that can be used across non-hospital environments. These devices appeal to providers seeking versatility, lower upfront costs, and easier integration into fast-turnover surgical workflows.

Simultaneously, private healthcare investment is expanding across major markets such as Brazil, Mexico, Colombia, and Chile, driving modernization of diagnostic and monitoring infrastructure. Hospitals upgrading their anesthesia and critical-care units are actively exploring advanced CO2 monitoring technologies that support better clinical outcomes and align with global standards of care.

Additionally, Latin America’s growing reputation as a hub for cosmetic, dental, and specialty medical tourism is generating demand for high-quality sedation and procedural safety tools. Providers catering to international patients increasingly adopt capnography to match safety expectations common in North America and Europe.

With rising emphasis on patient safety, improved clinical training, and broader decentralization of surgical services, the opportunity for expansion is substantial. Overall, technological innovation and shifting care models create a favorable environment for accelerated capnography adoption across the region.

Category-wise Analysis

By Product Insights

Sidestream capnographs are expected to secure a 44.1% share of the Latin America market by 2026, largely because they support a wide range of clinical environments, including emergency care, procedural sedation, and general wards. Their ability to monitor both intubated and non-intubated patients makes them the preferred choice for hospitals facing diverse patient needs. Additionally, their compact design, lower maintenance requirements, and broader vendor availability accelerate adoption across mid-tier facilities. Collectively, these advantages position sidestream technology as the most practical and scalable option for regional care settings.

By Modality Insights

Standalone capnography devices are projected to hold nearly 66.8% of the market by 2026, supported by their adaptability across operating rooms, ICUs, emergency units, and ambulatory centers. Their independent functionality allows hospitals to use them without relying on integrated platforms, enabling faster deployment in time-critical scenarios. These devices also appeal to facilities with limited interoperability infrastructure, reducing dependence on centralized monitoring systems. As surgical and sedation-based procedures increase across Latin America, the demand for versatile standalone systems continues to strengthen, reinforcing their dominant role.

By End-user Insights

Hospitals are projected to account for 52.5% of the Latin America capnography market by 2026, driven by their high caseload of surgeries, emergency interventions, and ventilated patients requiring continuous CO2 monitoring. Increasing regulatory emphasis on patient-safety standards encourages hospitals to adopt capnography for anesthesia, airway management, and post-operative care. Their ability to invest in advanced monitoring solutions and integrate capnography into routine clinical pathways further strengthens uptake. The expanding burden of respiratory diseases across the region also ensures hospitals remain the primary adopters of capnography systems.

Regional Insights

Brazil Capnography Equipment Market Trends

Brazil is projected to capture 42.8% of the Latin America capnography equipment market by 2026. Brazil’s growing burden of respiratory illnesses and expanding surgical demand are creating a strong impetus for capnography adoption. Chronic respiratory diseases - including COPD and other lung conditions - remain among the leading causes of hospitalization and mortality in Brazil.

As hospital admissions for respiratory disease remain substantial, continuous monitoring of ventilation and CO2 becomes increasingly relevant to improve patient safety and outcomes. Concurrently, Brazil’s health-care infrastructure is transforming: the number of surgical interventions and anesthesia-requiring procedures is rising across both public and private sectors.

In such settings - where airway management, sedation, or critical care are routine - capnography becomes a vital monitoring tool to prevent hypoventilation, ensure appropriate ventilation, and detect respiratory events early. Moreover, demographic shifts - notably an ageing population and increasing prevalence of chronic non-communicable diseases - are driving demand for more complex medical and surgical care. As patient risk profiles rise, hospitals are more likely to invest in advanced monitoring equipment, including capnographs to enhance perioperative safety and respiratory care standards.

Together, rising respiratory disease burden, increased surgical/ICU demand, and changing patient demographics are converging to fuel a significant growth trajectory for capnography equipment in Brazil. Thus, capnography is increasingly becoming an indispensable component of Brazil’s evolving clinical and perioperative care landscape.

Mexico Capnography Equipment Market Trends

Mexico is projected to account for 23.7% of the Latin America capnography equipment market by 2026. Mexico’s rapidly expanding aesthetic and cosmetic surgery landscape is fueling demand for advanced monitoring tools, including capnography. The country’s cosmetic-surgery market - including procedures such as liposuction, facelifts, rhinoplasty, and body contouring - is forecast to grow sharply over the coming years, reflecting rising social acceptance of cosmetic enhancements and growing confidence in clinical infrastructure.

Additionally, a booming medical-tourism industry, drawing patients domestically and internationally (especially from North America), is contributing to a surge in surgical volume. Lower procedural costs, internationally trained plastic-surgeons, and accredited clinics make Mexico a hub for both elective and reconstructive surgeries.

As demand for both invasive and minimally invasive aesthetic procedures climbs, reliance on safe sedation, airway management, and ventilation monitoring becomes more critical - pushing clinics and hospitals toward capnography adoption to reduce respiratory risks during sedation. In summary, the interplay of rising cosmetic & reconstructive surgery volume, growing medical tourism, and increasing demand for procedural safety is propelling the Mexican capnography-equipment market upward.

Competitive Landscape

The Latin America capnography market features a competitive landscape shaped by global monitoring technology manufacturers and regional suppliers offering cost-effective devices. Competition centers on product reliability, portability, integration with anesthesia systems, and expanding hospital partnerships to strengthen clinical adoption across varied care settings.

Key Industry Developments:

- In April 2025, Masimo announced that CEO Joe Kiani delivered a keynote in Chile at the 6th Global Ministerial Summit on Patient Safety, highlighting how the company’s AI-driven monitoring technologies enhance early deterioration detection and strengthen patient-safety practices.

Companies Covered in Latin America Capnography Equipment Market

- Medtronic

- Drägerwerk AG & Co. KGaA

- Masimo

- Koninklijke Philips N.V.

- Infinium Medical

- Qinhuangdao Kapunuomaite Medical Equipment S & T Co.,Ltd.

- Nonin

- BPL Medical Technologies

Frequently Asked Questions

The Latin America capnography equipment market is projected to be valued at US$ 57.4 Million in 2026.

Growing respiratory disease burden and rising sedation-based procedures are driving increased adoption of capnography across clinical settings.

The market is poised to witness a CAGR of 7.4% between 2026 and 2033.

Expanding ambulatory care, portable device demand, and rising medical tourism create strong growth opportunities for capnography solutions.

Major players include Medtronic, Drägerwerk AG & Co. KGaA, Masimo, Koninklijke Philips N.V., Infinium Medical, and others.