- Animal Feed & Additives

- High Fiber Feed Market

High Fiber Feed Market Size, Share, and Growth Forecast 2026 - 2033

High Fiber Feed Market by Livestock (Ruminants, Poultry, Equines, Swine, Aquatic Animals, Pets), by Source (Soybean, Wheat, Corn, Sugar Beet, Others), by Sales Channel (Direct sales, Indirect sales), and by Regional Analysis, 2026-2033

High Fiber Feed Market Size and Trend Analysis

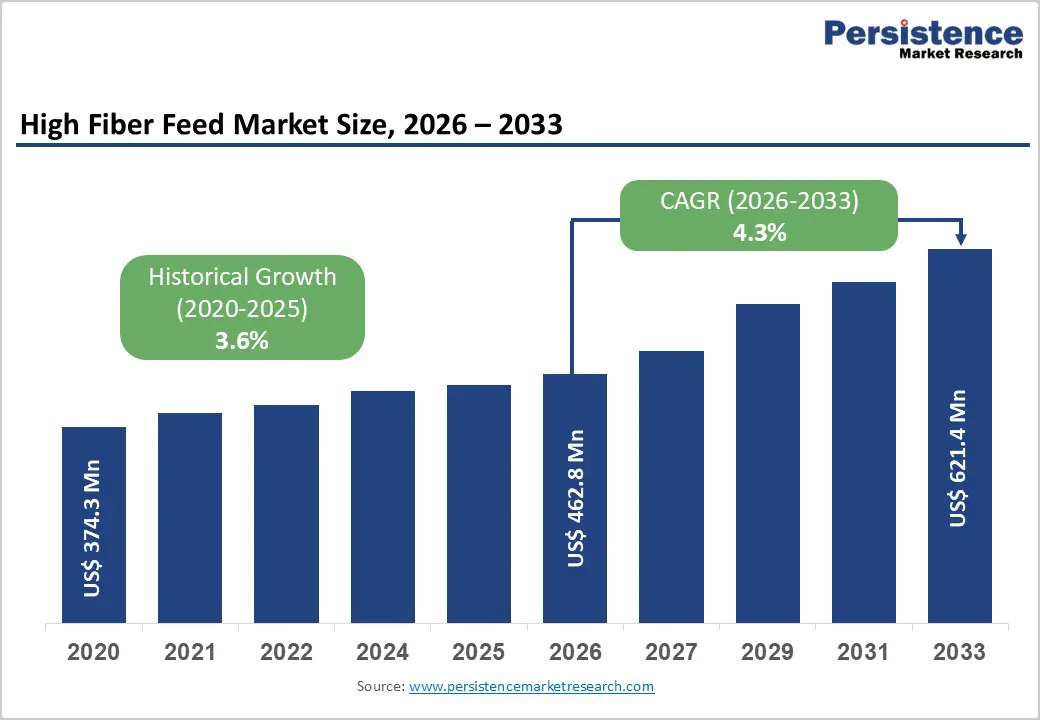

The global High Fiber Feed Market size is expected to be valued at US$ 462.8 million in 2026 and projected to reach US$ 621.4 million by 2033, growing at a CAGR of 4.3% between 2026 and 2033

The expansion of the global high fiber feed market is primarily anchored in the fundamental shift within the livestock industry toward gut health optimization and sustainable nutritional regimes. As commercial livestock producers prioritize metabolic efficiency and immune resilience, high-fiber dietary formulations have transitioned from being supplemental roughage to essential core components of balanced rations. This transition is further accelerated by the rising global demand for animal protein, necessitating higher productivity per animal, which in turn demands a specialized diet to prevent gastrointestinal disorders such as acidosis in Ruminants. Additionally, the rapid humanization of pets has created a significant niche for premium, fiber-enriched companion animal foods aimed at weight management and digestive wellness.

Key Industry Highlights

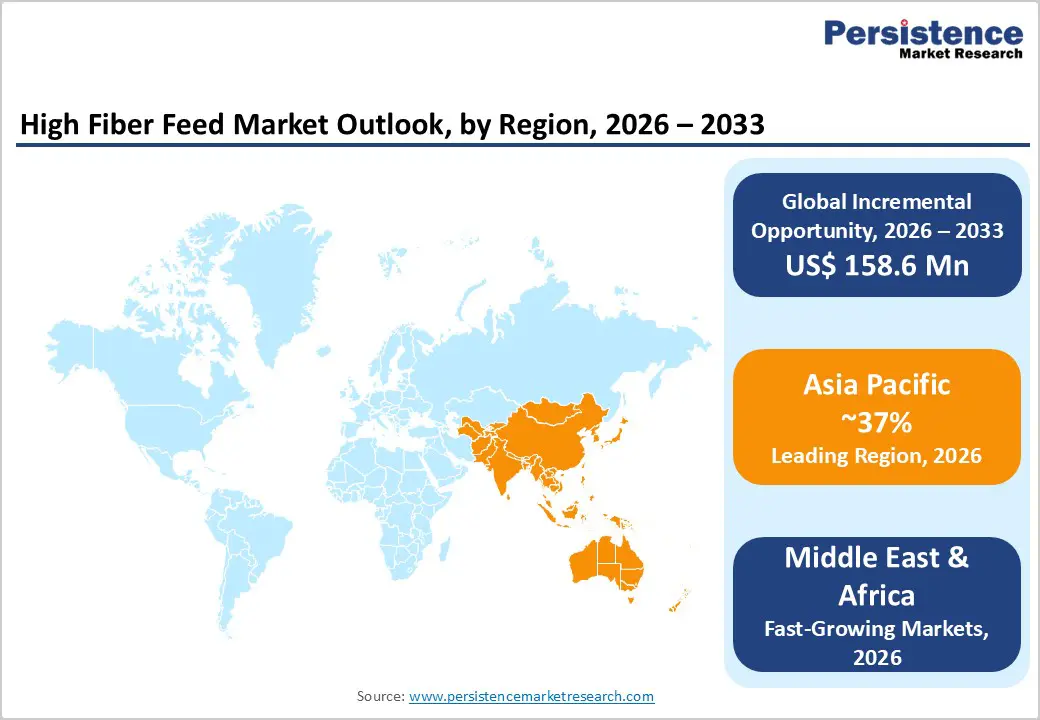

- Leading Region: Asia Pacific, accounting for around 37% market share, supported by large-scale livestock populations, rapid farm intensification in China and India, and strong availability of cereal by-products enabling cost-effective high-fiber feed production.

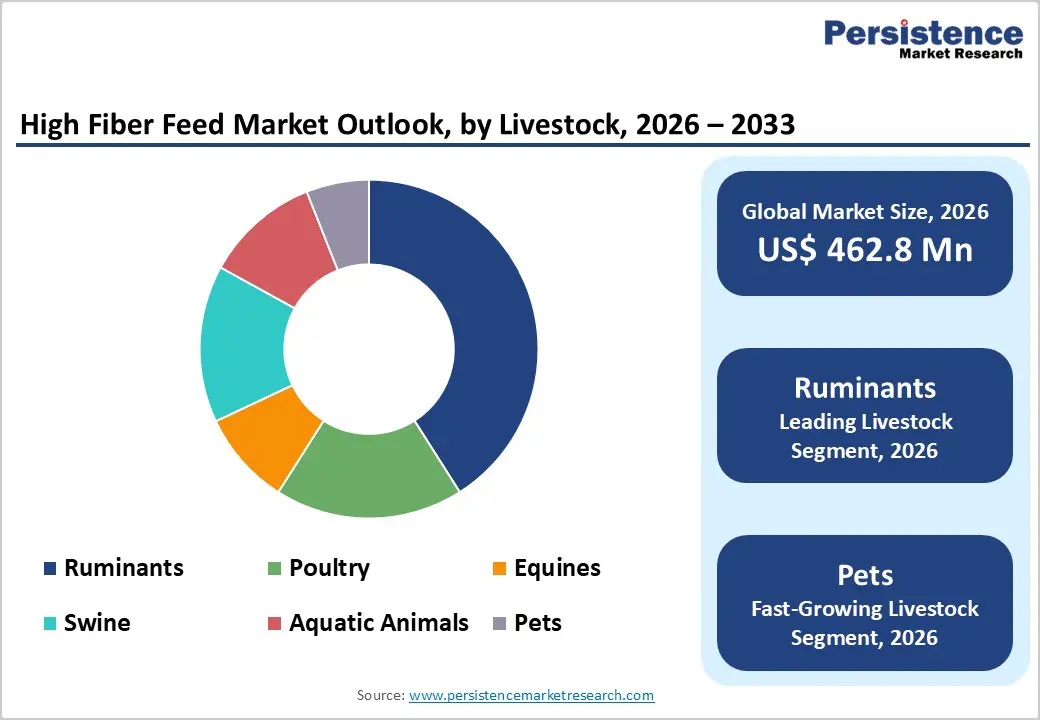

- Dominant Livestock Segment: Ruminants, holding approximately 41% market share due to physiological dependence on fiber for rumen function, milk fat maintenance, and prevention of metabolic disorders in dairy and beef production systems.

- Fastest-Growing Livestock Segment: Pets, fueled by pet humanization, preventive healthcare spending, and rising demand for weight management and digestive health-focused premium pet diets.

- Market Drivers: Growing awareness of gut health, reduced antibiotic usage, and stricter animal welfare standards are accelerating adoption of fiber-rich feeds as natural performance enhancers across livestock categories.

- Opportunities: Premiumization of pet nutrition, functional fiber innovation, and diversification into alternative fiber sources such as sugar beet pulp, citrus pulp, and specialty cellulose offer high-margin growth avenues.

- Key Developments: In September 2025, ADM launched Digest Carb for dairy cows at SPACE 2025 in France. In August 2025, Cargill opened a new retail feed facility in Washington. In June 2025, Triple Crown Nutrition and Standlee introduced the Diamond Line for advanced equine nutrition.

| Global Market Attributes | Key Insights |

|---|---|

| Global High Fiber Feed Market Size (2026E) | US$ 462.8 Mn |

| Market Value Forecast (2033F) | US$ 621.4 Mn |

| Projected Growth (CAGR 2026 to 2033) | 4.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.6% |

Market Dynamics

Driver – Growing Awareness of Gut Health and Animal Welfare Standards

A pivotal driver propelling the High Fiber Feed Market is the burgeoning recognition of the intrinsic link between dietary fiber and the functional integrity of the animal gastrointestinal tract. Modern animal science has increasingly highlighted that dietary fiber is not merely a "filler" but a critical prebiotic that fosters a healthy microbiome, particularly in monogastric animals like Swine and Poultry, and essential for the mechanical and chemical digestive processes in Ruminants. Organizations such as the European Food Safety Authority (EFSA) and the U.S. Food and Drug Administration (FDA) have championed guidelines that emphasize the reduction of antibiotic growth promoters, leading producers to seek natural alternatives. Fiber-rich ingredients like Sugar Beet pulp and Soybean hulls are now extensively utilized to improve stool consistency, mitigate heat stress, and enhance the overall immune response of livestock, ensuring compliance with global animal welfare protocols while simultaneously boosting producer profitability through reduced veterinary costs.

Restraints – Volatility in Raw Material Prices and Supply Chain Instabilities

One of the primary barriers hindering the High Fiber Feed Market is the significant price volatility associated with the agricultural commodities that serve as primary fiber sources. Inputs such as Wheat bran, Corn gluten feed, and Soybean hulls are often secondary by-products of the food and biofuel industries, making their availability and cost highly dependent on the dynamics of those primary markets. For instance, a poor harvest season for cereal grains in major exporting regions like the Black Sea or the United States can cause a sharp spike in feed costs, which typically account for 60% to 70% of total livestock production expenses. Furthermore, global supply chain disruptions, similar to those experienced in 2024, have highlighted the vulnerability of feed logistics to geopolitical tensions and energy price fluctuations, often resulting in localized shortages and reduced profit margins for small-to-medium-scale livestock operations.

Opportunity – Expansion into the Premium Pet Nutrition and Wellness Segment

The humanization of pets has emerged as a goldmine of opportunity for the High Fiber Feed Market, as companion animal owners increasingly seek "human-grade" nutritional solutions for their dogs, cats, and small mammals. There is a skyrocketing demand for specialized pet foods that address obesity, a condition affecting approximately 50% of pets in developed markets like North America and Europe. High-fiber formulations utilizing Sugar Beet pulp, cellulose, and fruit fibers are being marketed as effective tools for weight management and "indoor" lifestyles. Innovations in "functional fibers" that serve as prebiotics to improve coat quality and reduce fecal odor are particularly attractive to urban pet owners. As the pet population grows globally, particularly in the Asia Pacific region, manufacturers have a significant opportunity to capture high-margin revenue through premium, clinically backed, fiber-fortified pet nutrition products.

Category-wise Analysis

Livestock Analysis

The Ruminants segment stands as the preeminent category in the High Fiber Feed Market, commanding a substantial 41% market share in 2025. This dominance is naturally dictated by the complex multi-compartmental stomach of cattle, sheep, and goats, which requires significant quantities of physical fiber to stimulate rumination, maintain optimal pH levels, and support the microbial fermentation necessary for the synthesis of volatile fatty acids (VFAs). High-fiber feed is indispensable in the dairy industry to prevent metabolic disorders like displaced abomasum and to maintain milk fat percentages. However, the Pets segment is identified as the fastest-growing livestock category during the forecast period. This growth is fueled by a profound shift in consumer spending toward preventative pet healthcare and the rising prevalence of sedentary lifestyles among companion animals, which necessitates fiber-rich diets to prevent constipation and manage caloric intake.

Source Analysis

Within the source category, Corn-derived and Soybean-derived fibers currently represent the most widely utilized segments due to their ubiquitous availability as co-products of the global grain processing industry. Soybean hulls, in particular, are highly valued for their digestible fiber content and are frequently used to replace starch-heavy grains in the diets of beef and dairy cattle. Corn gluten feed also holds a significant share, providing a reliable source of both protein and fiber for various livestock species. Conversely, Sugar Beet pulp is emerging as a high-potential source, prized for its exceptional palatability and water-holding capacity, making it a "gold standard" for equine and senior pet nutrition. The "Others" segment, which includes innovative sources such as citrus pulp, sunflower hulls, and specialized wood-derived cellulose, is also seeing increased traction as manufacturers seek to diversify their raw material portfolios and improve feed sustainability.

Region-wise Insights

Asia Pacific High Fiber Feed Market Trends and Insights

The Asia Pacific region stands as the dominant force in the global landscape, commanding a 37% market share in 2025. This leadership is propelled by the massive and rapidly industrializing livestock sectors in China, India, and ASEAN countries. China's aggressive efforts to modernize its swine and dairy industries have led to a skyrocketing demand for standardized high-fiber feed to manage animal health in high-density intensive farming systems. Similarly, India's status as the world's largest milk producer creates a perennial and growing requirement for high-quality ruminant nutrition to boost average animal productivity.

The region's growth dynamics are further characterized by a significant manufacturing advantage, with a vast agricultural base providing a steady supply of cereal by-products. Japan and South Korea are also witnessing a sharp increase in the premium pet food segment, paralleling Western trends of pet humanization. Furthermore, the expansion of the aquaculture sector in Southeast Asia is creating a specialized demand for fiber-enriched aquatic feeds to improve gut health in farmed shrimp and fish. As disposable incomes rise and dietary preferences shift toward high-quality animal protein, the Asia Pacific region is expected to remain the primary engine of volume growth for the global market, supported by ongoing government investments in agricultural infrastructure and food security.

Middle East & Africa High Fiber Feed Market Trends and Insights

Middle East & Africa High Fiber Feed Market is expected to grow at a CAGR of 7.6%, driven by structural changes in livestock production and rising pressure to improve feed efficiency under arid conditions. In the GCC, water scarcity and high import dependence are accelerating the use of fiber-rich by-products such as beet pulp, wheat bran, and date residues to optimize rumen health and reduce reliance on expensive concentrates. Dairy operations increasingly prioritize fiber functionality to stabilize milk yields amid heat stress.

In Egypt, expanding commercial dairy farms are adopting balanced high-fiber formulations to support higher-producing cattle while managing volatile grain prices. Across Sub-Saharan Africa, growth is fueled by smallholder intensification, with governments promoting crop residue utilization and locally sourced fibrous feeds to improve livestock productivity. The region is steadily shifting from volume-driven feeding toward performance-oriented nutrition strategies.

Market Competitive Landscape

The High Fiber Feed Market exhibits a moderately consolidated structure, where a small number of global agricultural giants, such as Cargill, Incorporated, ADM, and Bunge Limited, control a significant portion of the primary processing and global distribution of fiber sources. These market leaders maintain their dominance through extensive vertical integration controlling the supply chain from the procurement of raw grains to the manufacturing of finished feed products. Their strategies for expansion often involve significant R&D investments to develop proprietary enzymatic blends that enhance fiber digestibility. Simultaneously, the market remains fragmented at the regional level, with numerous smaller players like ForFarmers Group and MBRF catering to niche segments or localized livestock needs. Emerging business model trends show an increasing shift toward "nutritional consultancy" services, where feed companies provide data-driven advice to farmers to optimize herd performance. Key differentiators include the ability to provide certified sustainable, non-GMO, and traceable feed ingredients.

Key Developments:

- In September 2025, ADM unveiled Digest Carb, a new dairy cow feed solution at SPACE 2025 in western France, aimed at boosting milk yield, improving feed efficiency, and lowering overall feeding costs for European dairy farmers.

- In August 2025, Cargill’s Animal Nutrition and Health business opened a new retail feed facility in Granger, Washington, strengthening its regional distribution footprint and closer-to-farm service capabilities.

- In June 2025, Triple Crown Nutrition, in collaboration with Standlee Premium Products, launched the Triple Crown Diamond Line, marking a significant advancement in premium equine nutrition offerings.

Companies Covered in High Fiber Feed Market

- Cargill, Incorporated

- ADM

- Bunge Limited

- Wilmar International Limited

- Nutreco N.V.

- Charoen Pokphand Foods PCL

- ForFarmers Group

- MBRF

- Alltech Inc.

- Gulshan Polyols Ltd

- De Heus Animal Nutrition

Frequently Asked Questions

The global High Fiber Feed Market is expected to reach a value of US$ 462.8 million in 2026, growing steadily at a CAGR of 4.3% during the forecast period.

Growth is primarily driven by the increasing awareness of gut health, rising global demand for high-quality animal protein, and stringent animal welfare standards discouraging the use of antibiotic growth promoters.

The Asia Pacific region is the leading segment, holding a 37% market share in 2025, primarily due to the massive dairy and livestock modernization programs in China and India.

Significant opportunities lie in the Premium Pet Nutrition segment, focusing on weight management and digestive wellness, as well as the integration of AI-driven Precision Nutrition technologies.

Key players include Cargill, Incorporated, ADM, Bunge Limited, Wilmar International Limited, Nutreco N.V., Charoen Pokphand Foods PCL, MBRF, Alltech Inc., and others