- Automotive Components & Materials

- Automotive Seat Belt Market

Automotive Seat Belt Market Size, Share, and Growth Forecast, 2025 - 2032

Automotive Seat Belt Market By Product Type (2-Point, 3-Point Seat Belts), Vehicle (Passenger Cars, LCVs, HCVs), Component (Webbing Strap, Retractors, Buckles), Distribution Channel (OEM, Aftermarket), and Regional Analysis for 2025 - 2032

Automotive Seat Belt Market Size and Trends Analysis

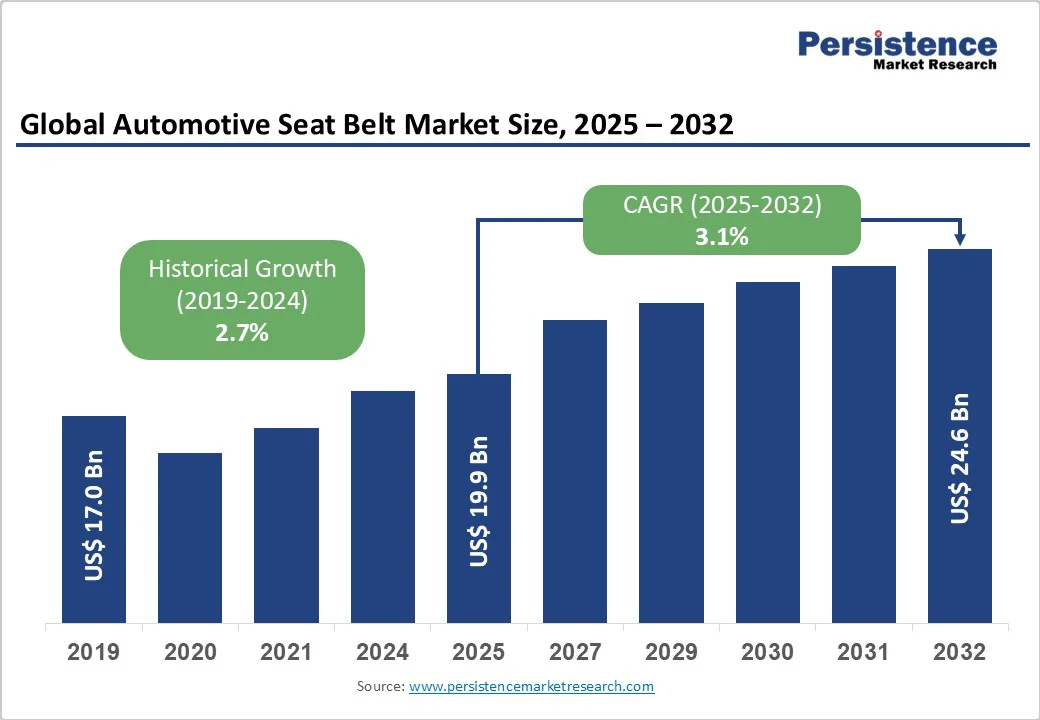

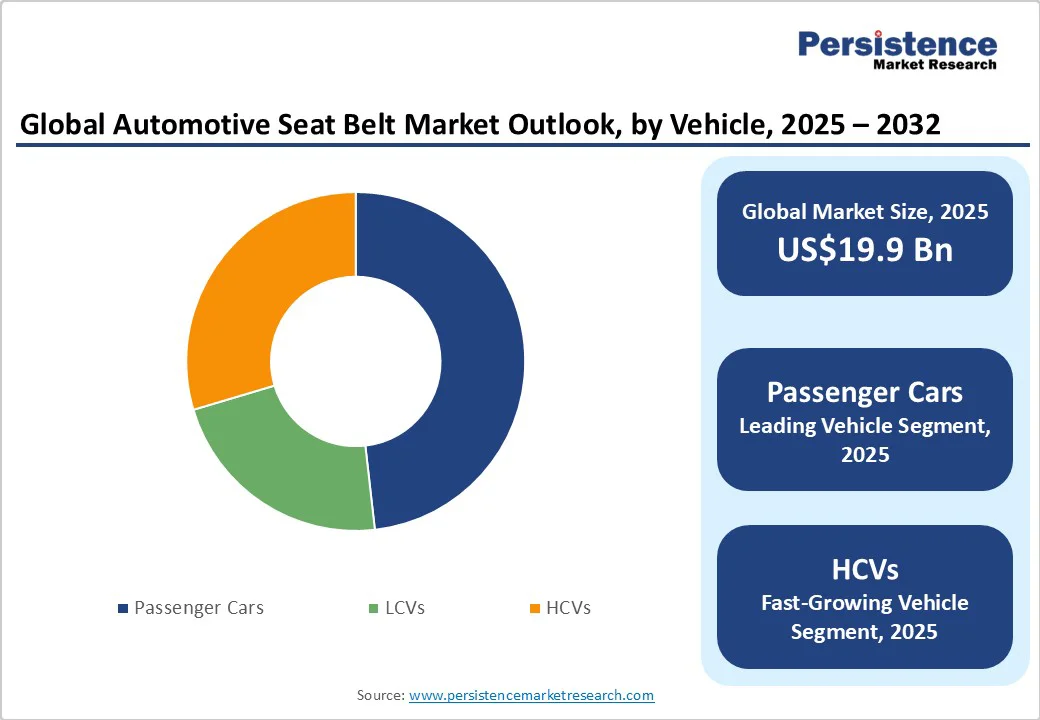

The global automotive seat belt market size is likely to be valued at US$19.9 Billion in 2025 and is estimated to reach US$24.6 Billion in 2032, growing at a CAGR of 3.1% during the forecast period 2025-2032, driven by increasing emphasis on road safety, driver-specific belt developments, and integrated safety systems. Modern driver seat belts also work in tandem with airbags to minimize injuries.

Key Industry Highlights

- Government Norm: Starting in September of 2027, all new passenger vehicles in the U.S. will have to sound a warning if rear-seat passengers don't buckle up. The National Highway Traffic Safety Administration finalized the rule, which requires improved warnings when front seat belts are not fastened.

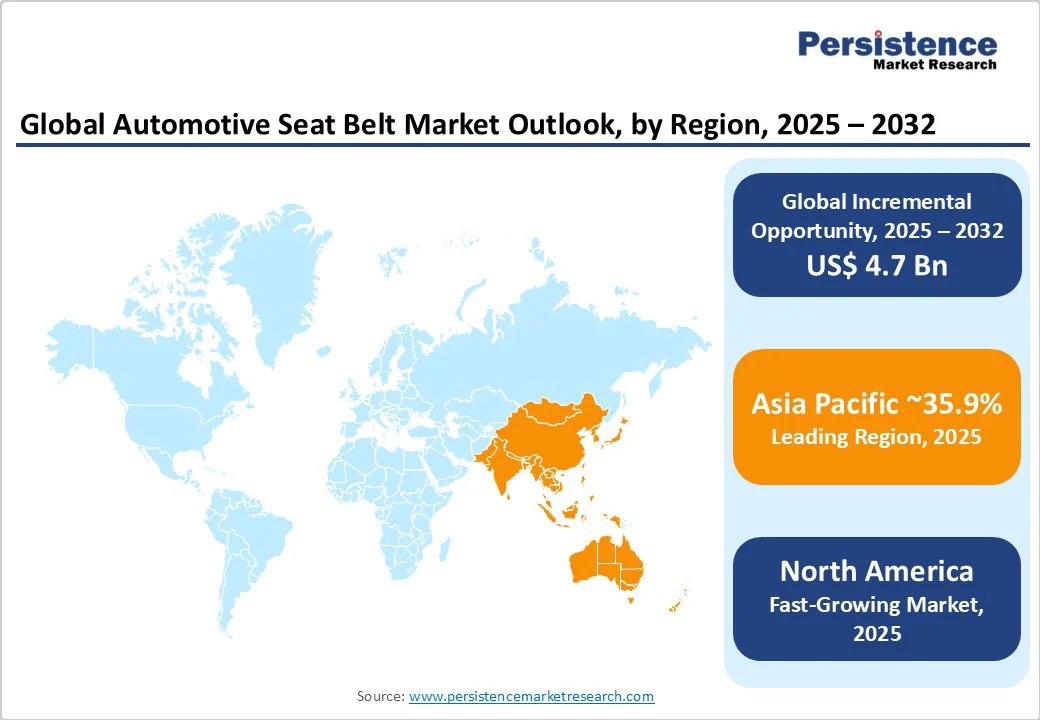

- Leading Region: Asia Pacific, with about 35.9% share in 2025, due to rising road safety regulations and ongoing vehicle production.

- Fastest-growing Region: North America, backed by high compliance rates and continuous integration of smart restraint technologies.

- Leading Product Type: 3-point seat belts hold nearly 66.4% share in 2025, as they provide superior upper and lower body protection.

- Dominant Vehicle: Passenger cars, approximately 48.2% of the automotive seat belt market share in 2025, spurred by demand for improved occupant protection.

- Key Component: Retractors recorded about 26.5% share in 2025, as they help improve comfort and safety by automatically managing slack and tightening belts during sudden braking or collisions.

| Key Insights | Details |

|---|---|

|

Automotive Seat Belt Market Size (2025E) |

US$19.9 Bn |

|

Market Value Forecast (2032F) |

US$ 24.6 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

3.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

2.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Tightening Safety Regulations Fuel Seat Belt Use

The tightening enforcement of road safety laws worldwide has become a key driver for the market. Governments are not only mandating seat belt use but also setting strict standards for belt performance, durability, and integration with other restraint systems. For instance, the European New Car Assessment Program (Euro NCAP) now includes seat belt reminders for all seating positions in its rating criteria, pushing automakers to adopt new solutions.

India’s Bharat NCAP, launched in 2023, has made front and rear seat belts mandatory in all new models. These evolving standards encourage manufacturers to innovate with load limiters, pretensioners, and seat-integrated belt designs, ensuring compliance while improving passenger protection.

Increasing Demand for Autonomous Vehicles

The shift toward semi-autonomous and fully autonomous vehicles is opening new design possibilities for seat belt manufacturers. As interior layouts evolve to allow swiveling or reclining seats, traditional belt geometries no longer suffice. This has led to the development of adaptive and motorized restraint systems capable of adjusting to different occupant positions.

ZF’s Active Control Retractor and Autoliv’s adaptive seat belt prototypes are prime examples, designed to work smoothly with vehicle sensors and ADAS systems. These developments ensure that passengers remain secure even when the car, rather than the driver, controls acceleration or braking. The increasing integration of AI-based safety technologies makes seat belts a key component of next-generation vehicle safety ecosystems.

Barrier Analysis - Challenges in Retrofitting Aging Vehicles

One key restraint for the automotive seat belt market is the difficulty of integrating modern seat belt systems into aging vehicles. Several vehicles, especially in developing regions, lack the structural compatibility to accommodate novel seat belt mechanisms such as pretensioners or load limiters. Retrofitting these technologies often requires modifications to the vehicle frame, which increases installation costs and deters owners from upgrading.

Regulations in several countries only mandate seat belts for new vehicles, limiting aftersales demand. For instance, India and parts of Africa still have large fleets of aging vehicles without standard three-point belts, which constrains the penetration of modern restraint systems despite rising road safety campaigns.

Impact of Global Economic Instability

Economic uncertainty directly affects automobile production and sales, which in turn influences the demand for seat belts. Periods of inflation, currency fluctuations, or supply chain disruptions, including those witnessed during the 2023 to 2024 semiconductor shortage and raw material price spikes, have pushed automakers to delay vehicle launches and reduce procurement volumes.

Cost pressures often compel OEMs to prioritize essential components over unique seat belt technologies, slowing development cycles. The volatility in global trade policies and rising transportation costs have also disrupted the flow of key materials such as nylon and polyester webbing, making it challenging for suppliers to maintain stable production and pricing levels across regions.

Opportunity Analysis - Collaborations between Automakers and Seat Belt Manufacturers

Strategic partnerships between automakers and seat belt suppliers are creating growth opportunities in the market. As vehicle safety becomes more data-driven, OEMs collaborate with safety system specialists to co-develop integrated restraint solutions. For example, Autoliv and Volvo have partnered to design next-generation seat belt systems that synchronize with airbag deployment and crash sensors for enhanced occupant protection.

ZF has also been working with electric vehicle manufacturers to develop lightweight seat belt assemblies personalized for EV interiors. Such collaborations not only accelerate development but also shorten development cycles, allowing both parties to meet evolving safety standards quickly. These alliances are helping seat belt makers move up the value chain by becoming long-term technology partners rather than just component suppliers.

Increasing Potential in the Automotive Aftermarket

The aftermarket segment presents new opportunities for seat belt manufacturers, especially in regions with large numbers of aging vehicles and weak OEM servicing networks. As road safety awareness rises, vehicle owners are now replacing worn-out or outdated seat belts with unique models featuring pretensioners and adjustable webbing.

For instance, governments in Latin America and Southeast Asia have started incentivizing retrofitting programs for aging taxis and commercial vehicles to comply with new safety mandates. Also, the booming e-commerce industry has made it convenient for consumers to access certified replacement belts directly from brands. This shift toward digital aftermarket sales and safety upgrades is creating a steady revenue stream beyond original equipment supply contracts.

Category-wise Analysis

Product Type Insights

3-point seat belts are predicted to capture around 66.4% of the market share in 2025, as they provide superior protection by restraining both the upper and lower body during a collision. Unlike 2-point lap belts, they significantly reduce the risk of chest and abdominal injuries by distributing impact forces across the shoulder and pelvis. Automakers are also adopting unique versions of 3-point systems equipped with pretensioners and load limiters, improving comfort and safety simultaneously.

2-point seat belts are predicted to see steady growth owing to their cost-effectiveness and easy installation in applications where minimal restraint is sufficient. They are commonly fitted in buses, forklifts, tractors, and construction machinery, where mobility and operator comfort are prioritized over full-body restraint. For instance, manufacturers such as AmSafe have introduced heavy-duty two-point belts that comply with international safety standards for industrial vehicles.

Vehicle Insights

Passenger cars are expected to hold a share of approximately 48.2% in 2025, spurred by the rising focus on occupant safety and the continuous tightening of safety standards across global markets. Modern car models increasingly integrate novel restraint technologies such as seat belt reminders, adaptive load limiters, and tension control systems that work in sync with airbags and ADAS features. For instance, Hyundai and Mercedes-Benz have recently incorporated seat belt load sensors that communicate with onboard control units to optimize crash protection.

HCVs are poised to be the fastest-growing vehicle type through 2032 as governments enforce strict safety norms for professional drivers and fleet operators. The rising number of road accidents involving trucks and buses has prompted regulatory bodies to make driver and co-driver seat belts mandatory in regions such as Europe, China, and India. For example, India’s 2023 amendment to the Central Motor Vehicle Rules requires factory-fitted seat belts for all seats in long-distance buses and goods carriers.

Component Insights

Retractors are anticipated to account for approximately 26.5% in 2025, as they automatically manage seat belt slack, ensuring both comfort and safety. These mechanisms allow free movement during normal driving but instantly lock the belt during sudden deceleration or collision, delivering a balance of convenience and protection. Novel versions now feature pyrotechnic and motorized retractors, which tighten the belt preemptively when sensors detect potential impact or emergency braking.

Pillar loops are estimated to witness a considerable CAGR in the foreseeable future due to their important role in optimizing seat belt geometry and occupant comfort. They guide the shoulder belt at the correct angle, reducing neck strain and improving the fit, which encourages regular seat belt use among passengers. Recent designs now include adjustable and motorized pillar loops, allowing users to customize height automatically based on seat position and body size.

Regional Insights

Asia Pacific Automotive Seat Belt Market Trends

In 2025, Asia Pacific is projected to contribute approximately 35.9% of the market share as several countries are strengthening seat belt regulations to improve road safety. For instance, India's Bureau of Indian Standards has introduced strict seat belt standards, complying with global safety norms. This move is part of a broad effort to improve vehicle safety standards and reduce road fatalities. Japan continues to lead in terms of seat belt compliance, with driver usage rates exceeding 99%. These regulatory developments are pushing a safe driving environment across Asia Pacific.

The automotive industry in Asia Pacific is further witnessing constant developments in seat belt technology. Manufacturers are integrating unique features such as pretensioners and load limiters to refine occupant protection during collisions. Also, the adoption of sensor-based seat belt systems is on the rise, allowing for more personalized safety measures. These technological developments are contributing to the improvement in vehicle safety standards across the region.

North America Automotive Seat Belt Market Trends

North America is anticipated to witness the fastest growth due to regulatory requirements. The U.S. is enforcing stringent norms for rear-seat belt reminders, with all new vehicles required to have audible and visual alerts by 2027. Front-seat reminders are already being strengthened. This is aimed at improving rear-seat compliance, which has historically lagged behind front-seat use.

States with primary enforcement laws, where drivers can be stopped solely for not wearing a seat belt, report slightly high compliance, keeping total usage rates relatively high. Automakers in North America are extensively integrating smart seat belt technologies. For example, Volvo has introduced multi-adaptive belts that adjust force based on occupant size, seating position, and crash scenario. These systems work with sensors and onboard safety electronics to improve protection for every passenger.

Europe Automotive Seat Belt Market Trends

In Europe, seat belt regulations are constantly evolving. The European Union mandates seat belt reminders for all seating positions, including rear seats, in new vehicles. These reminders must be activated upon vehicle startup and persist until the seat belt is fastened. The EU's road safety policy also aims to reduce road deaths and serious injuries by 50% by 2030, emphasizing the importance of seat belt use in achieving this goal.

Domestic automakers are at the forefront of integrating novel seat belt technologies. Developments such as adaptive seat belts, which adjust tension based on occupant size and crash severity, are becoming more prevalent. These systems improve occupant protection by providing optimal restraint during collisions. The development of smart seat belt systems that interact with other vehicle safety features, including airbags and collision sensors, is further gaining momentum.

Competitive Landscape

The global automotive seat belt market is characterized by a few dominant global players such as Autoliv, ZF Friedrichshafen, Joyson Safety Systems, and Tokai Rika, which collectively hold a substantial share of OEM contracts. These companies compete on innovation, reliability, and integration with unique safety systems rather than just price. Following the Takata recall crisis a few years ago, the market has consolidated heavily, with automakers now preferring suppliers that can ensure long-term quality, traceability, and compliance with global safety standards.

Key Industry Developments

- In July 2025, the Colorado Department of Transportation introduced its new ‘Buckle Up- Someone Needs You’ seat belt campaign. The campaign urges people to think about the ripple effects that would take place if they were to be killed or severely injured in a crash.

- In June 2025, Volvo announced that it is planning to improve vehicle safety with the introduction of an adaptive seat belt in its upcoming fully electric EX60, launching in 2026. This novel seat belt utilizes real-time data from various sensors to adjust its response based on the occupant's body characteristics and crash dynamics.

Companies Covered in Automotive Seat Belt Market

- ZF Friedrichshafen AG

- Autoliv Inc.

- Joyson Safety Systems

- Key Safety Systems (now part of Joyson Safety Systems)

- Takata Corporation (now part of Joyson Safety Systems)

- Delphi Automotive (Aptiv PLC)

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- Hyundai Mobis

- Toyoda Gosei Co., Ltd.

- Far Europe Inc.

- Goradia Industries (Beam's Seatbelts)

- Seatbelt Solutions LLC.

- Ashimori Industry Co., Ltd.

Frequently Asked Questions

The automotive seat belt market is projected to reach US$19.9 Billion in 2025.

Rising government safety regulations and surging awareness of driver protection are the key market drivers.

The automotive seat belt market is poised to witness a CAGR of 3.1% from 2025 to 2032.

Collaborations with automakers and the growth of retrofit programs are the key market opportunities.