- Beverages

- Zero Sugar Beverages Market

Zero Sugar Beverages Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Zero Sugar Beverages Market by Product Type (Carbonated soft drinks, Energy drinks, Sports drinks, RTD Coffee & Tea, Juices), by Packaging Type (Cans, PET bottles, Glass bottles, Others), by Sales Channel (HoReCa, Hypermarkets/Supermarkets, Convenience Stores, Specialty stores, Online Retail, Others), and Regional Analysis, 2026 - 2033

Zero Sugar Beverages Market Share and Trends Analysis

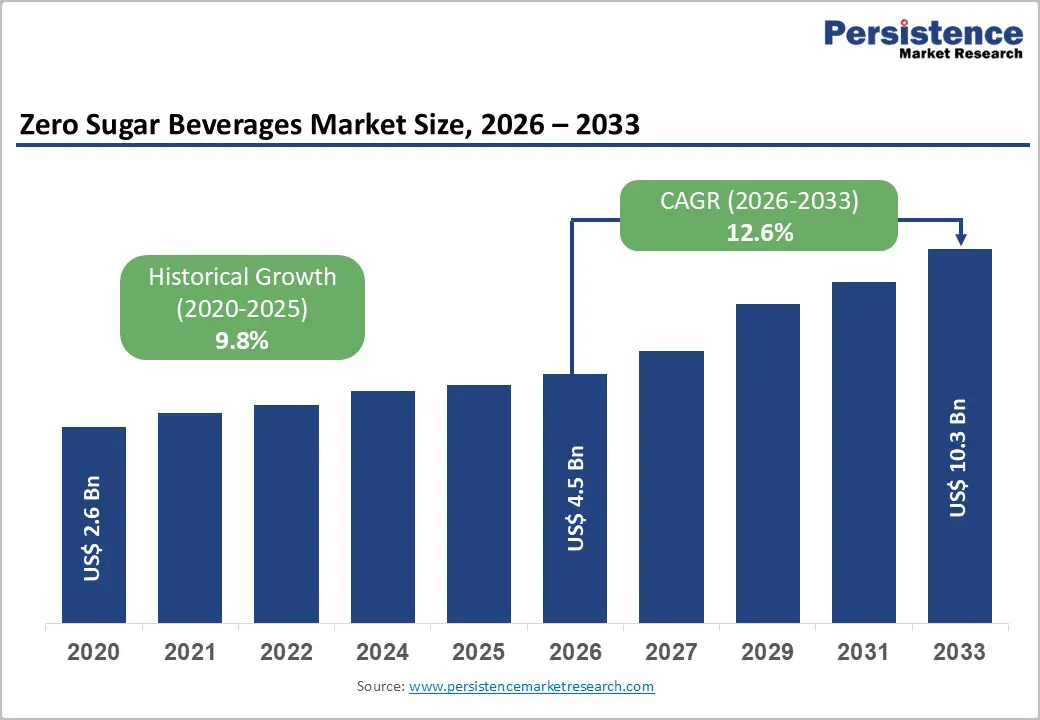

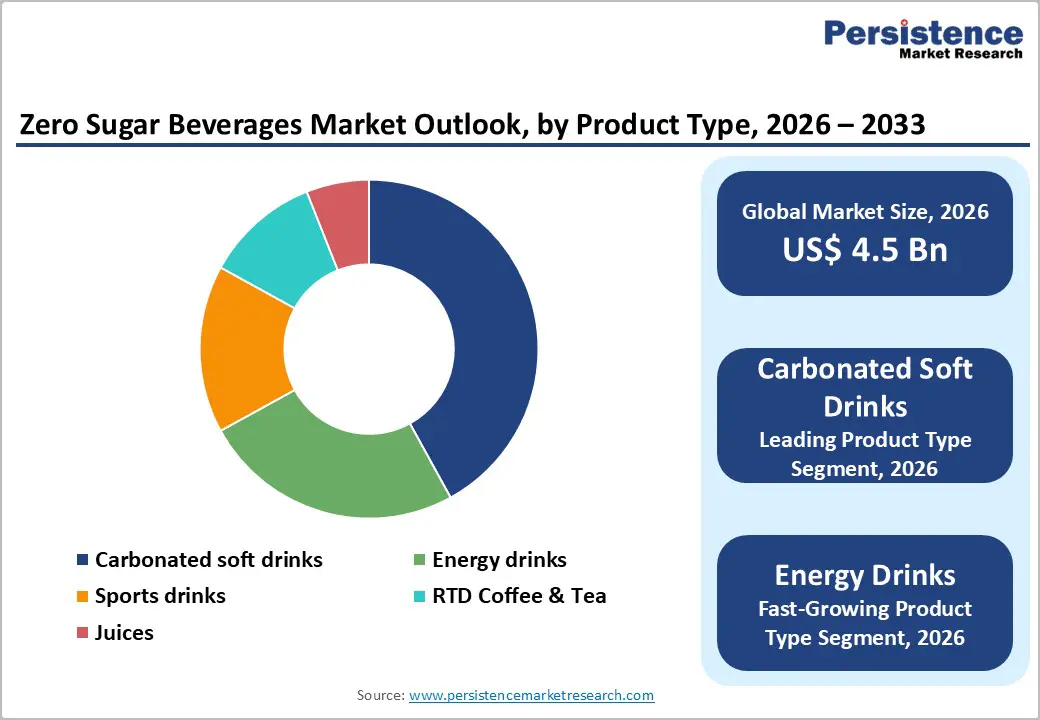

The global zero sugar beverages market size is expected to be valued at US$ 4.5 billion in 2026 and projected to reach US$ 10.3 billion by 2033, growing at a CAGR of 12.6% between 2026 and 2033. Consumer demand for healthier lifestyle choices and the rapid rise in metabolic disorders like diabetes are the primary catalysts for this aggressive market expansion.

Governments worldwide are intensifying these efforts through the implementation of sugar taxes and mandatory front-of-pack labeling, which effectively nudges both manufacturers and consumers toward calorie-free alternatives. Furthermore, the evolution of natural sweetener technologies, such as high-purity Stevia and Monk Fruit, has bridged the taste gap, ensuring that health-conscious transitions no longer require a compromise on sensory satisfaction.

Key Industry Highlights:

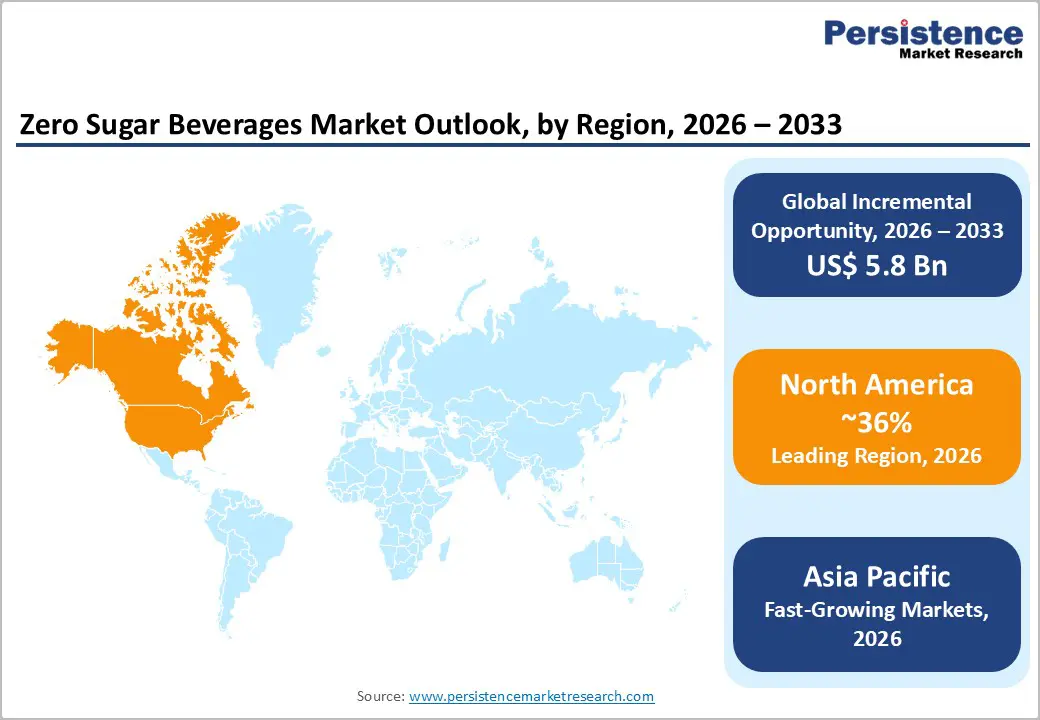

- North America remains the dominant force with a 36% market share, fueled by high health awareness, a mature retail landscape, and stringent FDA labeling regulations that promote lower sugar consumption.

- Asia Pacific is the fastest-growing region, projected to lead global expansion due to rising disposable incomes, Healthy China 2030 initiatives, and rapid urbanization in India and Southeast Asia.

- Carbonated Soft Drinks (CSDs) are the dominant product segment, accounting for 42% of the market share, driven by the global rebranding of iconic soda variants into zero-sugar versions.

- Energy Drinks represent the fastest-growing segment, as athletes and health-conscious professionals seek performance-enhancing caffeine boosts without the sugar crash associated with traditional high-calorie energy formulations.

- The integration of Functional Ingredients and Natural Sweeteners like Stevia and Monk Fruit offers the largest market opportunity, allowing brands to cater to the growing Clean Label movement.

| Key Insights | Details |

|---|---|

|

Global Zero Sugar Beverages Market Size (2026E) |

US$ 4.5 Bn |

|

Market Value Forecast (2033F) |

US$ 10.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

12.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

9.8% |

Market Dynamics

Driver - Rising Global Prevalence of Metabolic Disorders and Health Consciousness

The escalating burden of lifestyle-related conditions, particularly Type 2 Diabetes and Obesity, has become the most potent catalyst for the transition to zero-sugar alternatives. According to the World Health Organization (WHO), global obesity rates have nearly tripled since 1975, with over 650 million adults now classified as obese. This health crisis has sparked a Better-for-You revolution, where consumers actively scan nutrition labels for Added Sugar content. The International Diabetes Federation (IDF) estimates that approximately 537 million adults are currently living with diabetes, a figure expected to rise significantly. Consequently, the Zero Sugar Beverages market has moved from a niche dietary requirement to a mainstream lifestyle choice, as individuals seek to enjoy familiar carbonated or energy-boosting flavors without the associated glycemic impact or caloric load.

Restraints - Persistent Taste Perception Challenges and Aftertaste Limitations

Despite significant scientific advancements in sweetener technology, a sizeable segment of the consumer base remains skeptical of the sensory profile of zero-sugar products. The presence of high-intensity sweeteners like Aspartame or Saccharin often leaves a lingering metallic or bitter aftertaste that many traditional beverage drinkers find unappealing. Research by the Institute of Food Technologists (IFT) suggests that flavor fidelity remains the primary barrier to repeat purchase for approximately 25% of new entrants in the sugar-free category. This taste gap necessitates constant and expensive R&D investment from companies like Suntory Holdings Limited and Keurig Dr Pepper Inc. to maintain brand loyalty, as consumers may revert to full-sugar versions or switch to plain water if the flavor experience does not match expectations.

Opportunity - Evolution of Functional Zero-Sugar Drinks with Clean Label Profiles

A massive opportunity is emerging at the intersection of zero sugar and functional wellness, where beverages offer more than just hydration. Consumers are increasingly seeking Clean Label products that are free from artificial colors, preservatives, and synthetic sweeteners, favoring plant-based alternatives like Erythritol and Thaumatin. This trend is particularly visible in the Energy Drinks and Sports Drinks segments, where brands are infusing products with vitamins, minerals, and adaptogens to provide a clean energy boost. The Food and Agriculture Organization (FAO) has noted a rise in the demand for transparent sourcing of ingredients, suggesting that companies that can offer a Zero Sugar + High Function proposition will capture the highest value. The integration of immunity-boosting ingredients like Zinc and Vitamin C into sugar-free juices represents a significant revenue pocket for established players such as Nestlé S.A. and Unilever Plc.

Category-wise Analysis

Product Type Insights

Carbonated Soft Drinks (CSDs) remain the dominant powerhouse in the market accounting for 42% share as of 2025. This leadership is primarily driven by the massive global footprint and aggressive marketing of iconic brands such as Coca-Cola Zero Sugar and Pepsi Zero Sugar, which have successfully repositioned themselves as no-compromise alternatives to traditional sodas. The segment benefits from deep distribution networks through Hypermarkets/Supermarkets and a high degree of brand familiarity. Growth is further propelled by Flavor Innovation where manufacturers launch limited-edition sugar-free variants Zero Sugar Beverages ranging from spiced cherry to tropical blends Zero Sugar Beverages to maintain consumer engagement among younger cohorts like Gen Z and Millennials, who demand both health and novelty in their beverage choices.

Sales Channel Insights

Hypermarkets/supermarkets represent the leading sales channel for zero-sugar beverages, capturing nearly 38% of the market share in 2025. These retail giants provide the necessary Shelf Visibility and bulk-buying options that allow consumers to compare different brands and nutritional labels side-by-side. The presence of private-label sugar-free options within these stores further drives volume by offering cost-effective alternatives to premium brands. Meanwhile, Online Retail is emerging as the fastest-growing channel, particularly post-pandemic, as e-commerce platforms like Amazon and JD.com offer unparalleled convenience and Subscription Models for health-focused consumers. The ability to access niche, specialty zero-sugar brands that may not be available in local stores is a primary driver for the 15% annual growth projected for the digital commerce segment.

Regional Insights

North America Zero Sugar Beverages Market Trends and Insights

North America maintained its status as the global market leader in 2025, holding a commanding 36% market share. This dominance is rooted in a highly mature innovation ecosystem and a consumer base that is acutely aware of the health risks associated with high fructose corn syrup. The U.S. Centers for Disease Control and Prevention (CDC) has consistently highlighted the link between sugary drinks and chronic health issues, which has spurred a massive cultural shift toward Diet and Zero varieties. In the United States, the market is characterized by intense competition among The Coca-Cola Company, PepsiCo Inc., and Keurig Dr Pepper, with a heavy focus on functional additives and natural sweetening systems.

Recent developments in the region include the FDA's revised Healthy claim guidelines, which are expected to favor zero-sugar beverages that meet specific nutrient density criteria. Furthermore, the Soda Tax implementations in cities like Philadelphia and San Francisco have served as localized pilots that successfully shifted consumption toward sugar-free alternatives. The region also leads in the adoption of Sports Drinks and RTD Coffee variants without added sugar, as the Fitness Culture continues to expand across suburban and urban demographics, making North America the primary hub for premium market experimentation and high-value product launches.

Asia Pacific Zero Sugar Beverages Market Trends and Insights

Asia Pacific is slated to be the fastest-growing region through 2033, driven by Massive Urbanization and a rising middle class in China and India. The National Health Commission of China has launched Healthy China 2030 initiatives that specifically target the reduction of sugar intake, providing a strong tailwind for the zero-sugar category. In Japan, the market is exceptionally advanced, with a high penetration of functional sugar-free teas and FOSHU (Foods for Specified Health Uses) certified beverages produced by leaders like Suntory Holdings Limited and Asahi. The region's manufacturing advantage also allows for rapid scaling of new product lines at competitive price points.

In India, the market is witnessing an Explosion of Choice as local startups and global giants like The Coca-Cola Company introduce zero-sugar variants tailored to local tastes, such as masala-flavored sodas or fruit-based sugar-free drinks. The proliferation of Online Retail and smartphone usage across the ASEAN region has simplified the distribution of niche sugar-free products to previously unreachable rural and semi-urban populations.

Competitive Landscape

The zero sugar beverages market exhibits a moderately consolidated structure, where a handful of global conglomerates coexist with a rapidly expanding tier of specialized niche players. Established brands such as The Coca-Cola Company and PepsiCo Inc. have maintained dominance through their unmatched supply chains and multi-billion-dollar marketing budgets. However, the market is currently undergoing a Fragmentation Phase as consumer demand for variety and Clean Labels allows smaller, agile brands like Zevia and Arizona Beverage Company to capture significant share in specialty categories. The primary competitive strategies involve Aggressive Portfolio Diversification, moving from traditional sodas into energy and sports drinks, and Strategic Mergers and Acquisitions to absorb innovative startups that possess proprietary natural sweetener technologies or unique functional ingredients.

Key Developments:

- In February 2026, Coca-Cola expanded its cherry portfolio with new Cherry Float and Diet Coke Cherry variants, reinforcing cherry as a high-performing flavor across the U.S. and Canadian zero and low-calorie segments.

- In February 2026, Milo broadened its beverage lineup with the launch of Fruit Punch and Zero Sugar Lemonade, strengthening its presence in flavor-led refreshment while responding to rising demand for no-sugar alternatives.

- In January 2026, CELSIUS introduced four zero-sugar, fruit-forward flavors under its core range, strategically timed to capture New Year wellness momentum and drive incremental sales aligned with its LIVE FIT™ positioning.

Companies Covered in Zero Sugar Beverages Market

- The Coca-Cola Company

- PepsiCo Inc.

- Keurig Dr Pepper Inc.

- Nestlé S.A.

- Monster Beverage Corporation

- Red Bull GmbH

- Suntory Holdings Limited

- Britvic PLC

- National Beverage Corp.

- Arizona Beverage Company

- Unilever Plc

- Others

Frequently Asked Questions

The global zero sugar beverages market is projected to be valued at US$ 4.5 Bn in 2026.

The rising global prevalence of metabolic disorders and health consciousness is driving demand for zero sugar beverages market.

The global zero sugar beverages market is poised to witness a CAGR of 12.6% between 2026 and 2033.

Evolution of functional zero-sugar drinks with clean label profiles is a key opportunity for key market players.

Leading companies include The Coca-Cola Company, PepsiCo Inc., Keurig Dr Pepper Inc., Nestlé S.A., Monster Beverage Corporation, Red Bull GmbH, Others.