- Nutraceuticals & Functional Foods

- Yogurt Powder Market

Yogurt Powder Market Size, Share, and Growth Forecast 2026 - 2033

Yogurt Powder Market by Yogurt Type (Whole, Skimmed, Lactose-free, Organic, Others), Application (Food & Beverages, Supplements/Nutrition products, Household, Foodservice), Packaging (Sachets, Cans, Bulk packs), Sales Channel (Supermarkets / Hypermarkets, Online stores, Convenience stores, Specialty stores), and Regional Analysis, 2026 - 2033

Yogurt Powder Market Share and Trends Analysis

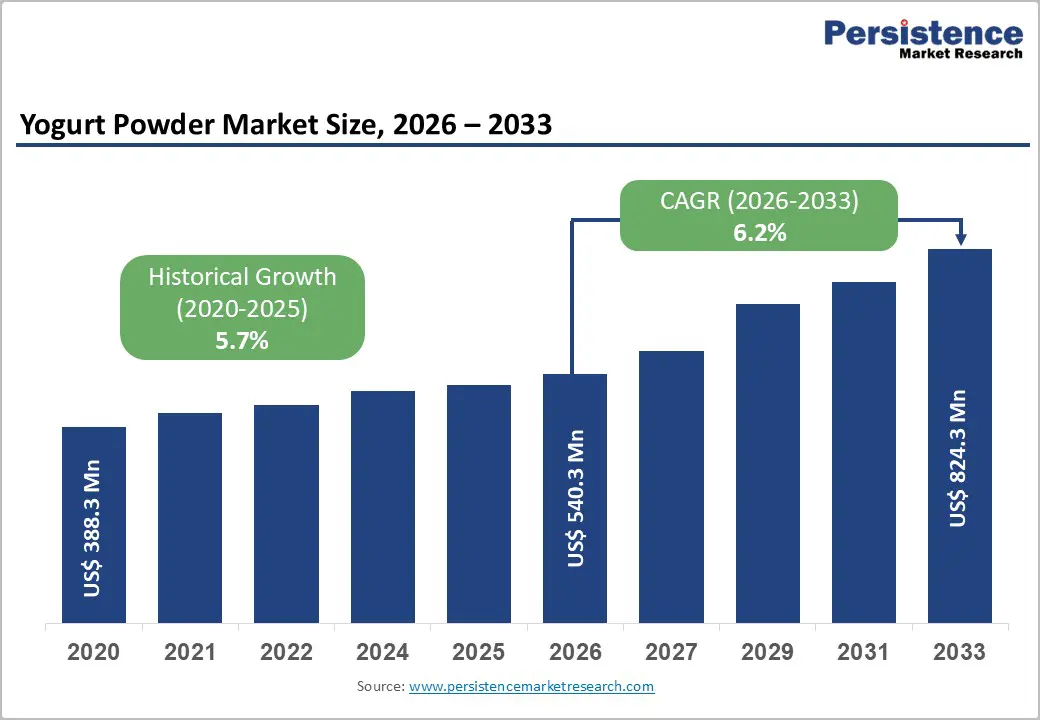

The global yogurt powder market size is expected to be valued at US$ 540.3 million in 2026 and projected to reach US$ 824.3 million by 2033, growing at a CAGR of 6.2% between 2026 and 2033.

Strong demand for shelf-stable dairy ingredients in food & beverage processing, increasing use in functional foods, and rapid penetration in convenience nutrition products are the primary growth engines. Growing consumer preference for high-protein and probiotic-enriched foods, combined with busy lifestyles that favor long-life formats over chilled yogurt, is expanding the adoption of yogurt powder in smoothies, bakery mixes, instant desserts, and ready-to-drink beverages. Additionally, improvements in spray-drying and freeze-drying efficiency are enhancing flavor retention and nutritional stability, helping manufacturers launch premium variants, such as organic and lactose-free yogurt powders, that appeal to health-conscious consumers.

Key Market Highlights

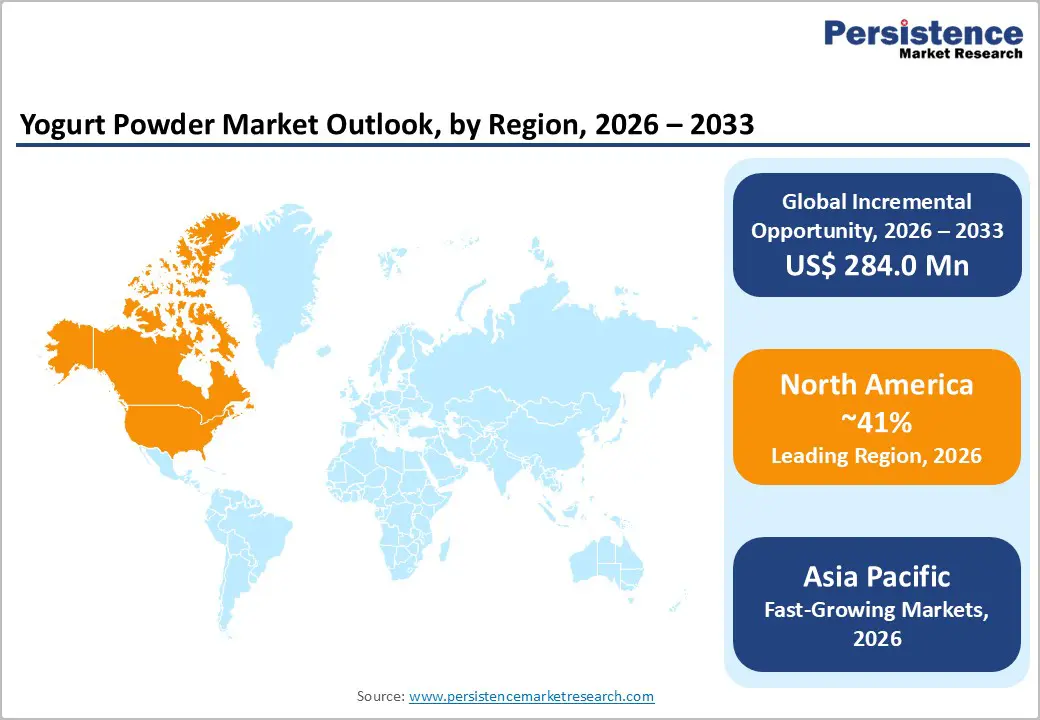

- North America leads the global yogurt powder market, supported by a strong U.S. processed food sector, advanced dairy infrastructure, and high adoption of functional snacks, beverages, and convenient dairy ingredients across retail and foodservice channels.

- Asia Pacific is the fastest-growing yogurt powder region, with China, India, Japan, and ASEAN markets driving demand through rising incomes, Westernized eating habits, and investments in food processing and value-added dairy manufacturing.

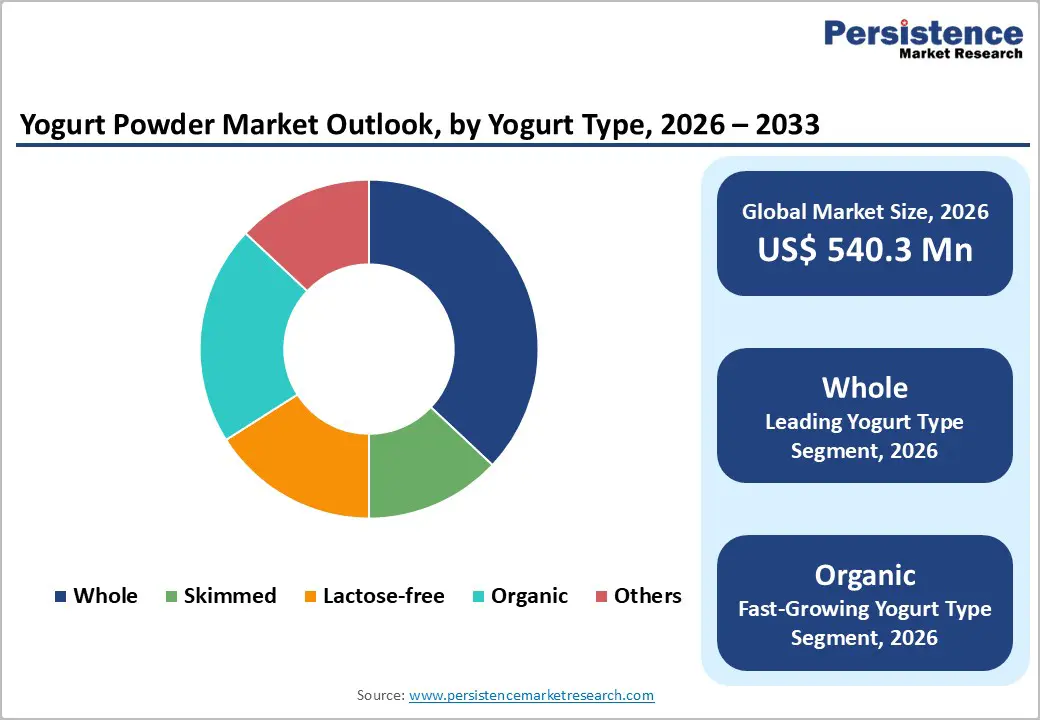

- The Whole yogurt powder segment dominates yogurt type, capturing about 37% share in 2025 due to its superior creaminess and flavor delivery in indulgent applications such as desserts, coatings, and premium snack products.

- Organic and specialized yogurt powders are among the fastest-growing segments, benefiting from clean-label, lactose-free, and high-protein trends as consumers increasingly seek premium, health-oriented functional dairy ingredients.

| Key Insights | Details |

|---|---|

| Yogurt Powder Market Size (2026E) | US$ 540.3 million |

| Market Value Forecast (2033F) | US$ 824.3 million |

| Projected Growth CAGR (2026 - 2033) | 6.2% |

| Historical Market Growth (2020 - 2025) | 5.7% |

Market Dynamics

Drivers - Rising demand for convenient, shelf-stable functional dairy

A major driver of the yogurt powder market is the shift toward convenient, shelf-stable dairy formats that retain the nutritional and sensory benefits of traditional yogurt. Powdered yogurt enables manufacturers to formulate high-protein, probiotic, and flavored products without relying on cold-chain logistics, which is especially valuable in emerging markets with infrastructure gaps. Industry sources note that shelf-stable dairy ingredients, including yogurt powders, are increasingly used in sports nutrition, instant breakfast drinks, dry bakery mixes, and snack bars to deliver indulgent taste while improving functionality and extending shelf life. This combination of convenience, reduced waste, and formulation flexibility directly supports stronger adoption of yogurt powder in both foodservice and packaged food segments.

Health and wellness focus boosts protein- and probiotic-rich products

Escalating health consciousness and the global pivot toward functional foods rich in protein and beneficial bacteria are driving significant growth in yogurt powder demand. Research on dairy-based functional ingredients shows consumers increasingly associate yogurt products with digestive health, immunity support, and satiety, encouraging brand owners to incorporate yogurt powder into fortified beverages, infant nutrition, and supplements/nutrition products. Industry analyses note that yogurt powder offers a concentrated source of milk proteins and can retain live cultures when processed appropriately, aligning with trends in clean-label, high-protein and reduced-sugar formulations. As functional snacking and better-for-you convenience foods expand globally, the role of yogurt powder as a versatile health-forward ingredient is expected to strengthen further.

Market Restraints

Volatility in dairy raw material prices and supply

One of the key restraints for the yogurt powder market is the exposure to volatility in milk and dairy commodity prices, which directly affects production costs and margins. Global dairy markets are influenced by climate events, feed costs, and trade policies, leading to fluctuations in the availability and pricing of skimmed milk and cream, the primary inputs for yogurt production. When input prices rise sharply, manufacturers may be forced to adjust pricing or reformulate, which can dampen demand in price-sensitive applications such as mass-market snacks and foodservice mixes. This cost uncertainty can also suppress long-term investment in new capacity in some regions.

Stringent food safety, labeling, and additive regulations

The market also faces headwinds from increasingly stringent regulations governing food safety, labeling, and the use of additives in dairy powders. Authorities in North America, Europe, and parts of the Asia Pacific require compliance with strict microbiological standards, contaminant limits, and traceability rules for powdered dairy ingredients. In addition, shifting expectations around the labeling of sugars, flavors, and stabilizers can necessitate reformulating yogurt powder-based products to meet clean-label and allergen declarations. Meeting these regulatory and documentation requirements can raise compliance costs, especially for small and mid-sized processors, potentially slowing market entry and innovation.

Opportunities - Premiumization through organic, lactose-free, and clean-label formulations

One of the most attractive opportunities lies in premium yogurt powder variants such as organic, lactose-free, and clean-label formulations targeting sensitive and sustainability-oriented consumers. Organic dairy consumption has been growing steadily in North America and Europe, with consumers willing to pay a premium for certified supply chains and animal welfare standards that support higher-value organic yogurt powder offerings. Lactose-free and reduced-allergen formulations are also gaining traction among populations with lactose intolerance and digestive sensitivities, particularly in the Asia Pacific and Latin America. These specialized powders can be incorporated into plant-forward and hybrid products, smoothie mixes, and supplements/nutrition products, creating a differentiated value proposition that supports margin expansion and long-term brand loyalty.

Expansion in emerging markets and new applications

Another key opportunity is expanding yogurt powder use in emerging markets and in adjacent applications such as bakery, confectionery, and personal care. As rising incomes and urbanization reshape diets in China, India, and ASEAN, demand for convenient, Western-style dairy flavors in beverages, desserts, and breakfast products is accelerating, and yogurt powder offers a cost-effective way to deliver taste and nutrition without full cold-chain investment. In parallel, formulators in cosmetics and personal care are experimenting with yogurt-based powders in face masks and topical products due to their perceived skin-conditioning benefits and natural positioning, mirroring trends seen in the broader functional dairy ingredients market. These emerging use cases broaden the addressable market for yogurt powders and help reduce dependency on traditional applications alone.

Category-wise Analysis

Yogurt Type Insights

Within yogurt type, whole yogurt powder accounts for an estimated 37% share in 2025, making it the leading segment. Industry data indicate that full-fat or whole yogurt variants remain popular among consumers seeking richer mouthfeel and better flavor delivery in applications like instant desserts, dips, and premium snack coatings. Whole yogurt powder delivers superior creaminess and flavor intensity compared with reduced-fat alternatives, which is critical in indulgent segments such as confectionery fillings and ice-cream mixes. At the same time, the segment benefits from the broader acceptance of dairy fats in balanced diets, particularly in Europe and North America, where research has nuanced consumer attitudes toward milk fat. These factors collectively support the dominant position of Whole yogurt powder, even as organic and lactose-free segments post faster growth.

Application Insights

In terms of application, the Food & Beverages segment is the leading contributor to yogurt powder demand, accounting for an estimated share of well over half of global consumption in 2025. Industry reports indicate that yogurt powder is widely used in sports drinks, breakfast beverages, nutrition bars, ready-to-mix smoothies, baked goods, and instant dessert mixes due to its ability to deliver tangy flavor, protein, and a creamy texture without refrigeration. The ongoing shift toward on-the-go and better-for-you snacking, particularly in urban populations, reinforces the use of yogurt powder as a functional flavoring and nutritional component in processed foods. Furthermore, the foodservice channel leverages yogurt powder in sauces, dressings, and drink bases to simplify operations and reduce waste, which indirectly boosts volume in the Food & Beverages application category.

Sales Channel Insights

Among sales channels, supermarkets/hypermarkets account for the largest share of yogurt powder distribution, reflecting their dominance in modern grocery retail and their broad assortment of dairy, baking, and nutrition products. Large-format retailers provide extensive shelf space for both branded and private-label yogurt powders, often positioning them alongside baking mixes, milk powders, and breakfast items to capture cross-category demand. The visibility and promotional capabilities of supermarkets through in-store displays, sampling, and loyalty programs help accelerate consumer trial and repeat purchases. While online stores are growing rapidly, particularly for specialized and bulk formats, supermarkets remain the primary touchpoint in many regions, where consumers still prefer to evaluate new dairy ingredients in person before buying.

Regional Insights

North America Yogurt Powder Market Trends and Insights

The North American yogurt powder market has emerged as a leading region due to strong consumer preference for convenient, shelf-stable, and protein-rich dairy products. Increasing awareness of digestive health and the rising demand for functional foods, including high-protein snacks and supplements, has driven widespread adoption of yogurt powders in both retail and foodservice sectors. Manufacturers in the U.S. and Canada have focused on product innovation, introducing lactose-free, organic, and flavored variants to cater to diverse consumer needs. The growing trend of home-based baking and smoothie preparations has further boosted household consumption. Additionally, the expansion of e-commerce platforms has made yogurt powders more accessible, allowing smaller brands to reach niche markets effectively. Partnerships between dairy ingredient suppliers and food processors have strengthened distribution channels, ensuring consistent product availability across supermarkets, convenience stores, and online retail. Overall, the North American market’s growth is supported by health-conscious consumer behavior, strong infrastructure, and ongoing product diversification, making it a key leader in the global yogurt powder industry.

Asia Pacific Yogurt Powder Market Trends and Insights

The Asia Pacific yogurt powder market is rapidly emerging as a high-growth region, driven by increasing health awareness, rising disposable incomes, and shifting dietary preferences toward protein-rich and functional foods. Countries such as China, India, Japan, and South Korea are witnessing growing demand for convenient, shelf-stable dairy products for use in beverages, bakery items, and nutritional supplements. Urbanization and busier lifestyles have fueled the popularity of ready-to-use yogurt powders among households and foodservice providers. The region is also seeing a surge in the adoption of organic, lactose-free, and flavored variants, reflecting consumers’ evolving tastes and health concerns. Additionally, expanding retail infrastructure, including supermarkets, hypermarkets, and e-commerce platforms, has improved accessibility and availability of yogurt powders across both metropolitan and semi-urban areas. Local manufacturers are increasingly investing in R&D and partnerships with global dairy ingredient suppliers to enhance product quality and variety. With supportive government initiatives promoting dairy consumption and nutrition, the Asia Pacific market is positioned for sustained growth, emerging as a dynamic and promising segment in the global yogurt powder industry.

Competitive Landscape

The yogurt powder market is highly competitive, characterized by the presence of numerous global and regional players focusing on product innovation, quality, and differentiation. Companies are increasingly introducing specialty variants such as organic, lactose-free, flavored, and high-protein powders to cater to evolving consumer preferences. Strategic partnerships with food processors, retailers, and e-commerce platforms help expand distribution reach and market penetration. Pricing strategies, certification standards, and consistent supply chains play a crucial role in maintaining competitiveness. Continuous R&D and marketing initiatives aimed at health-conscious and convenience-seeking consumers further intensify the competitive landscape, driving innovation and growth across the sector.

Key Market Developments

- In May 2025, Foster Clark launched “My Yogo,” a new flavored yoghurt beverage powder as part of its expansion into the dairy drinks category. The product was introduced to offer a convenient, nutritious, and tasty yogurt-based drink option tailored to local consumer tastes. This launch marked the company’s first foray into this beverage segment in key markets, aiming to broaden its portfolio and strengthen its presence by meeting growing demand for innovative and accessible dairy products.

Companies Covered in Yogurt Powder Market

- Kerry Group plc

- Glanbia plc

- Arla Foods Ingredients

- Epi Ingredients

- Prolactal GmbH

- Bluegrass Dairy & Food, Inc.

- CP Ingredients Ltd.

- Ace International LLP

- Ingredion Incorporated

- FrieslandCampina

- Fonterra Co-operative Group

- Danone S.A.

- Nestlé S.A.

- General Mills, Inc.

- Yakult Honsha Co., Ltd.

- MSK Specialist Ingredients

Frequently Asked Questions

The global yogurt powder market size is expected to reach about US$ 540.3 million in 2026, reflecting steady growth from 2020 supported by rising demand for shelf-stable, functional dairy ingredients in food and beverage applications.

The main demand driver is growing consumption of convenient, high-protein and probiotic-rich foods, as yogurt powder enables manufacturers to formulate shelf-stable snacks, beverages, and nutrition products without depending on cold-chain logistics.

North America leads the yogurt powder market, underpinned by a large U.S. processed food industry, strong sports nutrition and snack sectors, and advanced dairy processing capabilities ensuring consistent ingredient quality.

A key opportunity lies in premium organic, lactose-free, and clean-label yogurt powders and in expanding into emerging markets and new applications such as bakery, confectionery, and personal care, where functional dairy ingredients are gaining traction.

Major companies include Kerry Group plc, Glanbia plc, Arla Foods Ingredients, Epi Ingredients, FrieslandCampina, Fonterra Co-operative Group, Danone S.A., Nestlé S.A., General Mills, Inc., and Yakult Honsha Co., Ltd.