- Beverages

- U.S. Yogurt Market

U.S. Yogurt Market Size, Share, and Growth Forecast 2026 - 2033

U.S. Yogurt Market by Product Type (Dairy-based, Non-dairy), Flavor Type (Plain, Flavored), Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Convenience Stores, Online Retail, Others), and Zone Analysis, 2026 - 2033

U.S. Yogurt Market Size and Trend Analysis

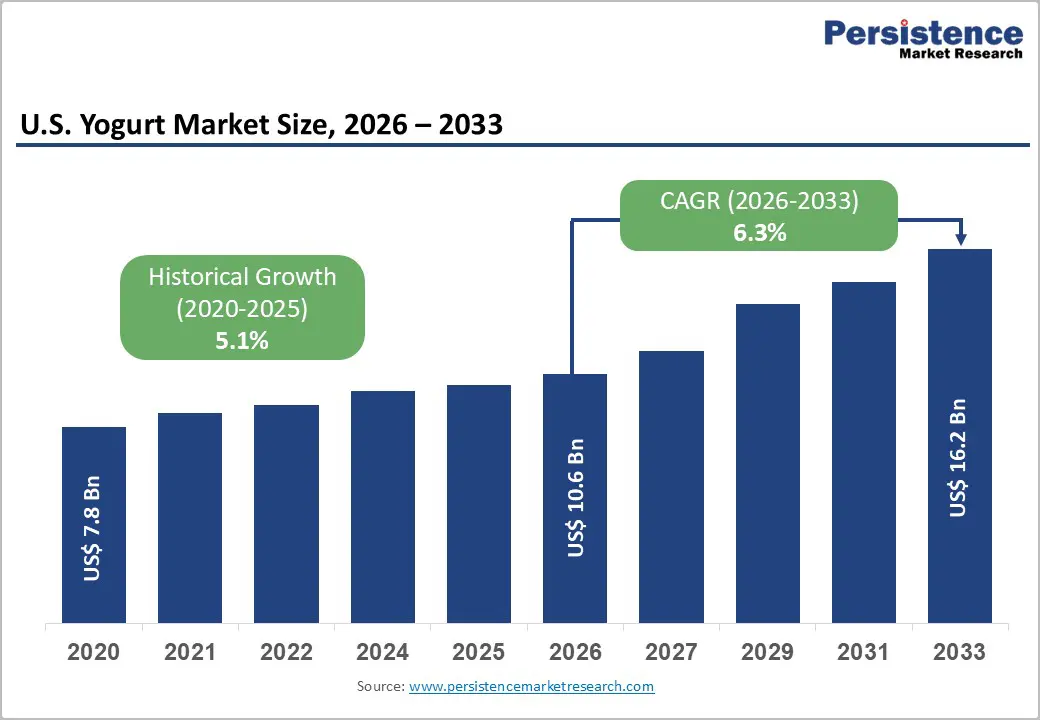

The U.S. yogurt market size is expected to be valued at US$ 10.6 billion in 2026 and projected to reach US$ 16.2 billion by 2033, growing at a CAGR of 6.3% between 2026 and 2033.

The U.S. yogurt market is experiencing steady growth, supported by rising consumer focus on digestive health, high-protein diets, and functional nutrition. Yogurt remains a staple dairy product due to its probiotic benefits, convenience, and wide product availability across supermarkets, convenience stores, and foodservice channels. Dairy-based yogurt dominates the market, particularly Greek yogurt, skyr, and probiotic-rich traditional varieties, driven by strong consumer familiarity and protein-focused consumption trends.

Meanwhile, non-dairy yogurt is the fastest-growing segment, fueled by increasing lactose intolerance, vegan preferences, and demand for plant-based alternatives made from almond, oat, soy, and coconut. Product innovation, clean-label formulations, and premium wellness positioning continue to strengthen market expansion across the U.S.

Key Industry Highlights

- Leading Region: The Northeast U.S. leads the U.S. yogurt market with approximately 28% of market revenue in 2025, driven by high population density, health-conscious urban consumers, premium grocery retail infrastructure, and proximity to major yogurt manufacturing facilities in New York and New England.

- Fastest Growing Region: The Southeast U.S. is the fastest growing regional market for yogurt over 2026–2033, propelled by rapid population growth, expanding suburban grocery infrastructure, and rising health consciousness in high-growth metros including Atlanta, Miami, and Charlotte.

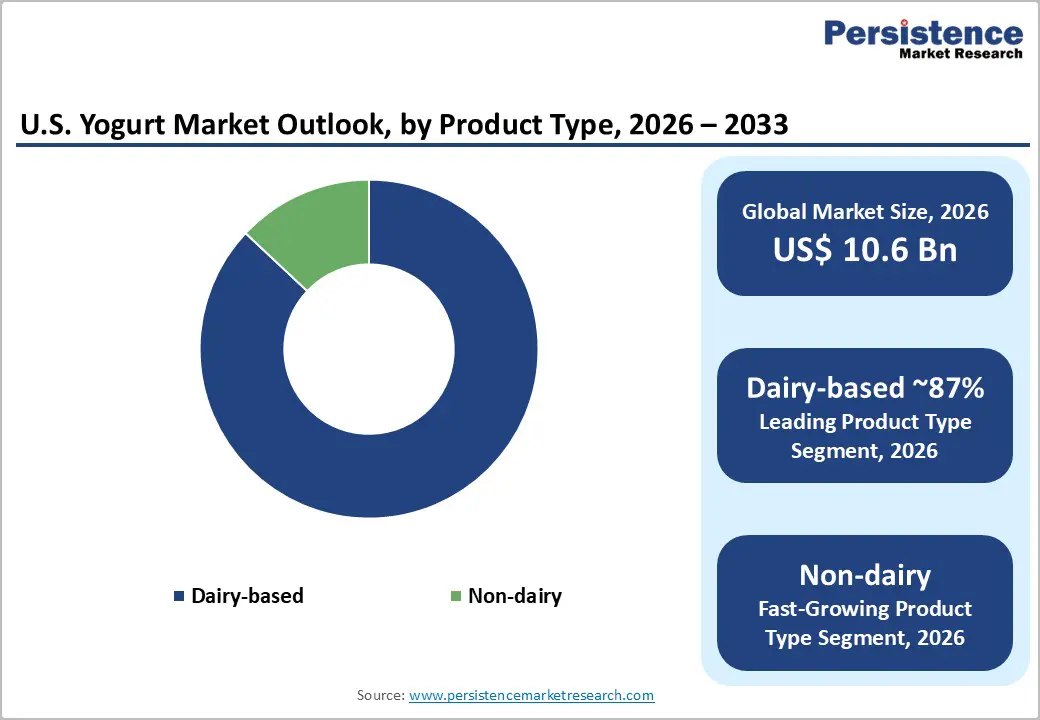

- Dominant Segment: Dairy-based yogurt dominates the U.S. yogurt market with approximately 87% market share in 2025, supported by decades of entrenched consumer purchasing habits, extensive retail availability, and continuous product innovation across Greek, drinkable, and low-fat formats.

- Fastest Growing Segment: Non-dairy yogurt is the fastest growing product type over 2026–2033, driven by lactose intolerance prevalence affecting approximately 36% of Americans per CDC data, rising veganism, and improving plant-based yogurt formulations in coconut, oat, and almond formats.

- Key Market Opportunity: The rapid expansion of e-commerce grocery platforms and direct-to-consumer models presents yogurt manufacturers with a compelling opportunity to reach premium-oriented, digitally engaged consumers, build subscription revenue streams, and drive incremental category growth beyond traditional brick-and-mortar retail.

Market Dynamics

Drivers - On-the-go Snacking Trends Propel Demand for Single-Serve Yogurt Formats

The shift of modern consumers toward smaller, convenient, and frequent eating occasions from conventional meals is anticipated to spur the U.S. yogurt market growth. Ready-to-eat yet nutritious snacks are gaining impetus among Gen Z and millennial consumers as these fit into their busy lifestyles. Mondelz International, for example, found in its State of Snacking survey that nearly 71% of consumers in the U.S. said they preferred snacking more than two times a day. Over 60% of consumers, revealed that they usually replace at least one meal with snacks.

Yogurt, specifically drinkable formats, pouches, and single-serve cups have become the ideal choice as it offers a balance of probiotics, calcium, and protein conveniently. Several brands capitalize on this trend with product development and innovation. Yoplait Go-GURT, for instance, which was originally launched for children, was recently reformulated and rebranded with adult appeal and clean labels. The brand aims to offer consumers a suitable on-the-go probiotic snack that does not require a spoon.

Restraints - Increasing Competition from Alternative Dairy and Plant-Based Protein Products

The U.S. yogurt market faces intensifying competitive pressure from adjacent categories including kefir, probiotic supplements, cottage cheese, and plant-based protein snacks all of which compete for the same health-oriented consumer wallet share. The Plant Based Foods Association (PBFA) reported that U.S. plant-based food retail sales have grown at double-digit rates in recent years, with consumers redistributing snack and dairy budgets across a widening array of functional food alternatives. This competitive fragmentation constrains volume growth for conventional dairy yogurt brands and intensifies pricing pressure, particularly in the mass-market segment of supermarkets and club stores.

Opportunities - Non-Dairy and Plant-Based Yogurt Addressing the Fastest Growing Consumer Segment

Non-dairy yogurt is the fastest growing product type segment in the U.S. yogurt market over 2026–2033, presenting a transformative opportunity for both established dairy brands and specialist plant-based manufacturers. The Good Food Institute (GFI) reports that U.S. plant-based dairy alternatives including non-dairy yogurt have sustained double-digit retail sales growth as consumers motivated by lactose intolerance, veganism, and sustainability concerns seek credible dairy substitutes. According to the Centers for Disease Control and Prevention (CDC), approximately 36% of Americans experience some degree of lactose malabsorption, representing a large medically motivated non-dairy consumer cohort. Companies investing in coconut milk, almond milk, oat milk, and cashew-based yogurt formulations with comparable texture and probiotic content to dairy yogurt can capture a significant share in this rapidly expanding, premium-priced segment.

Category-wise Analysis

Product Type Insights

Dairy-based yogurt is the dominant product type in the U.S. yogurt market, commanding approximately 87% of total market share in 2025. Its overwhelming market leadership reflects decades of entrenched consumer habit, broad retail availability, and the well-established nutritional reputation of dairy yogurt as a source of calcium, protein, and live active cultures. The International Dairy Foods Association (IDFA) reports that American households have consistently ranked yogurt among the top five most frequently purchased refrigerated dairy items.

Dairy-based yogurt benefits from continuous category innovation across Greek, traditional, drinkable, and low-fat formats, supported by powerful marketing investments by major brands. Non-dairy is identified as the fastest growing segment, driven by lactose intolerance prevalence, veganism adoption, and sustainability-driven consumer behavior shifts across younger U.S. demographics.

Distribution Channel Insights

Supermarkets and hypermarkets are the dominant distribution channel for yogurt in the U.S. market, accounting for approximately 58% of total channel share in 2025. The channel's leadership is anchored by high consumer footfall, prominent yogurt category aisle space, promotional pricing support, and the broad product range these large-format stores can accommodate enabling consumers to discover and trial new yogurt formats and flavors. Major chains including Kroger, Walmart, Target, and Costco are primary volume drivers for national yogurt brands.

Online retail is identified as the fast-growing distribution channel, propelled by the rapid expansion of grocery delivery services, subscription meal kit integrations, and the growing preference for digital-first shopping among millennial and Gen Z consumers across U.S. metropolitan areas.

Regional Insights

West U.S. Yogurt Market Trends and Insights

In West U.S., cities such as Seattle, San Francisco, and Los Angeles are showcasing a skyrocketing demand for dairy-free, organic, low-sugar, and high-protein yogurt offerings. As per a recent survey, sales of yogurt surged by 7.1% year-over-year in the West, outpacing other zones due to increasing inclination toward functional and specialty products.

The zone is further considered a significant hub for innovation when it comes to plant-based yogurt. For example, California, houses brands such as Forager Project and Kite Hill that mainly focus on producing coconut, cashew, and almond-based yogurts. They are striving to enhance their brand visibility by launching new products across retailers such as Sprouts and Whole Foods.

Southeast U.S. Yogurt Market Trends and Insights

Southeast U.S. is anticipated to account for a share of 37% in 2026. Key companies such as Danone exhibit high demand for multipack yogurts and fruit-on-the-bottom cups over plant-based varieties. Price sensitivity is a significant factor expected to influence growth in this zone. South Carolina, Alabama, Georgia, and Mississippi house a relatively higher proportion of middle-income and low-income households. Hence, affordability is the priority for consumers in these states over premium health claims. Renowned retail chains such as Publix are predicted to offer their store-brand yogurts at low costs to attract consumers’ attention.

Midwest U.S. Yogurt Market Trends and Insights

The Midwest has recently witnessed a steady shift of consumers from traditional yogurt toward probiotic-rich and high-protein options. The increasing popularity of family-sized tubs and multipacks catering to cost-conscious consumers and large households is presumed to create new opportunities in this zone. Retailers such as Hy-Vee, Kroger, and Meijer play an important role in the distribution of yogurt. These often provide weekly promotions or discounts on bulk purchases to influence buying behavior.

In states such as Wisconsin, Michigan, and Ohio, functional yogurt with added probiotics has become popular among the geriatric population. These consumers are adding yogurt to their daily diet to support immunity and boost digestion. It is further propelling the product sales, including Nancy’s Probiotic Yogurt and Activia.

Competitive Landscape

The U.S. yogurt market is moderately consolidated, with Danone (Activia, Oikos), Chobani LLC, and General Mills (Yoplait) commanding leading positions through scale, brand equity, and extensive retail distribution networks. FAGE USA and Lactalis hold strong positions in the premium Greek segment. Key competitive differentiators include probiotic strain diversity, protein content, clean-label formulations, and flavor innovation velocity. R&D investment is increasingly directed toward non-dairy formulation improvement, functional fortification, and sustainability-linked packaging. Direct-to-consumer digital channels and private-label competition from major retailers are reshaping competitive dynamics.

Key Developments

- In March 2025, Chobani exhibited its range of high-protein yogurt drinks and yogurt cups in the U.S. at the Natural Products Expo West. The products include naturally occurring whey protein.

- In January 2025, La Terra Fina launched its latest Jalapeño Ranch flavor to extend its Greek yogurt dips and spreads range. The new product was a result of high consumer demand for enhanced, bold flavors for entertaining moments and everyday meals.

- In September 2024, Lactalis Group acquired General Mills’ yogurt brands and facilities to extend its yogurt business in the U.S. The acquisition includes brands such as Ratio and Mountain High from General Mills as well as those under license, including Oui, Go-Gurt, and Yoplait.

U.S. Yogurt Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 7.8 billion |

|

Current Market Value (2026) |

US$ 10.6 billion |

|

Projected Market Value (2033) |

US$ 16.2 billion |

|

CAGR (2026–2033) |

6.3% |

|

Leading Region |

Northeast U.S., ~28% market share (2025) |

|

Dominant Product Type |

Dairy-based, ~87% market share (2025) |

|

Top-Ranking Flavor Type |

Flavored, ~68% market share (2025) |

|

Incremental Opportunity |

US$ 5.6 billion (Absolute Dollar Opportunity) |

Companies Covered in U.S. Yogurt Market

- Danone

- Chobani LLC

- General Mills Inc.

- Lactalis

- FAGE USA Dairy Industry Inc.

- Dairy Farmers of America Inc.

- Anderson Erickson Dairy

- Hain Celestial Group

- Tillamook County Creamery Association

- Dean Foods

- Others

Frequently Asked Questions

The U.S. yogurt market is expected to be valued at US$ 10.6 billion in 2026.

Increasing awareness of yogurt’s potential health benefits and launch of new flavors are the key market drivers.

The Northeast U.S. leads the U.S. yogurt market with approximately 28% of market revenue in 2025.

Innovations in plant-based yogurt and launch of single-serve yogurt formats are the key market opportunities.

The leading companies in the U.S. yogurt market include Danone, Chobani LLC, General Mills Inc., and Lactalis.