- Medical Devices

- Wound Debridement Products Market

Wound Debridement Products Market Size, Share, and Growth Forecast 2026 - 2033

Wound Debridement Products Market by Product Type (Hydrosurgical Debridement Devices, Low Frequency Ultrasound Devices, Surgical Wound Debridement Devices, Mechanical Debridement Pads), Application (Chronic Ulcers, Surgical Wounds, Traumatic Wounds, Burn Cases), End-user (Hospitals, Specialized Clinics, Ambulatory Surgical Centers, Homecare Settings), and Regional Analysis, 2026–2033

Wound Debridgement Products Market Share and Trends Analysis

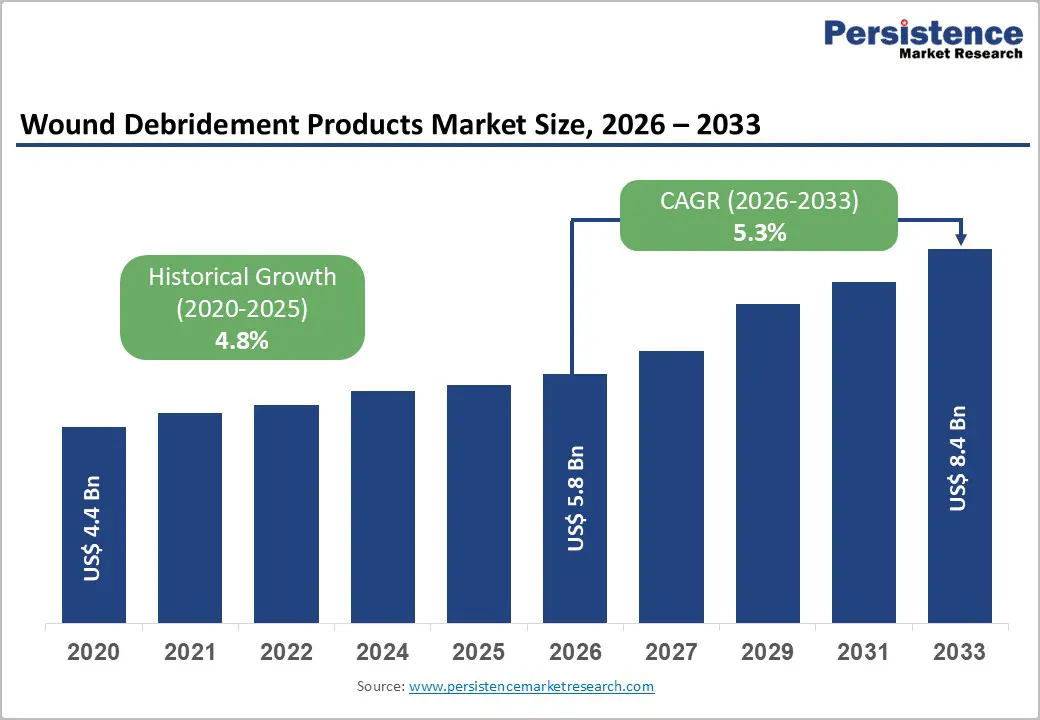

The global wound debridement products market size is expected to be valued at US$ 5.8 billion in 2026 and projected to reach US$ 8.4 billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033. The global rise in burden of chronic wounds in the population, particularly diabetic foot ulcers, pressure injuries, and venous leg ulcers, combined with increasing surgical and trauma wound volumes and the progressive adoption of advanced energy-based debridement technologies.

The International Diabetes Federation (IDF) projects the global diabetic population will reach 783 million by 2045, with approximately 15–25% developing foot ulcers requiring debridement intervention. Rising hospital-acquired pressure injury rates, expanding home care wound management programs, and growing preference for hydrosurgical and ultrasound-based over traditional sharp debridement are collectively reinforcing market demand across all geographies.

Key Industry Highlights:

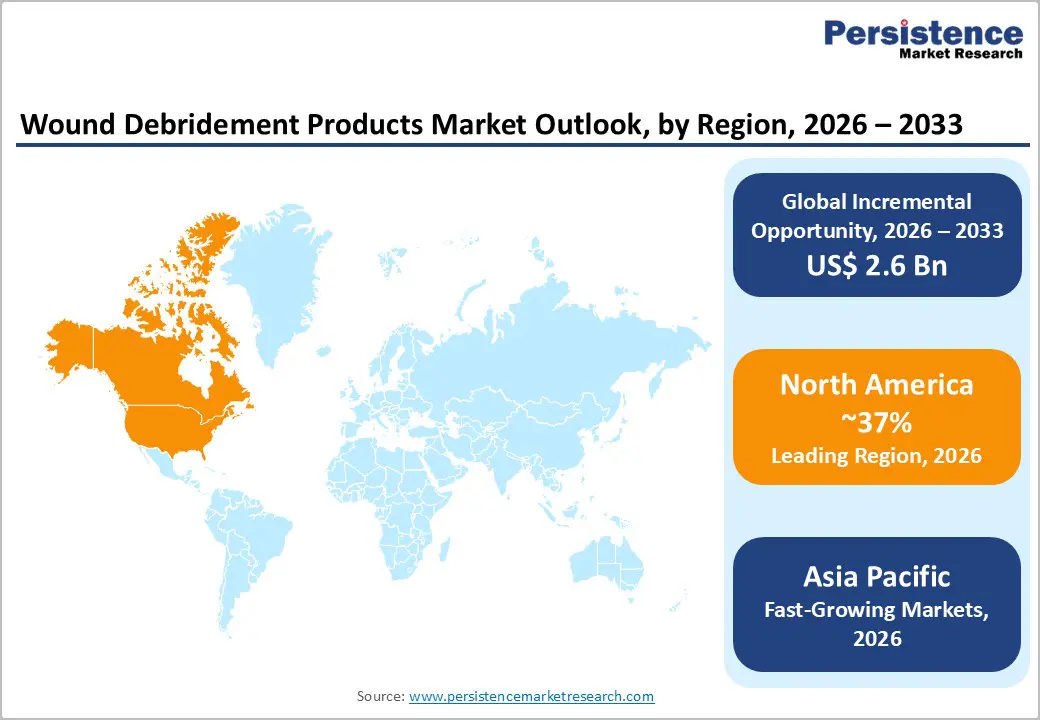

- Regional Leadership: North America leads the global wound debridement products market with approximately 37% share in 2025, driven by over 6 million Americans with chronic wounds per AHRQ data, CMS reimbursement support, and advanced hydrosurgical adoption by Smith & Nephew and Integra LifeSciences.

- Fast-growing Market: Asia Pacific is the fastest-growing wound debridement market, with China's Healthy China 2030 driving wound care center expansion, India's 101 million diabetic patients per IDF sustaining demand, and Southeast Asia's accelerating private hospital sector adoption.

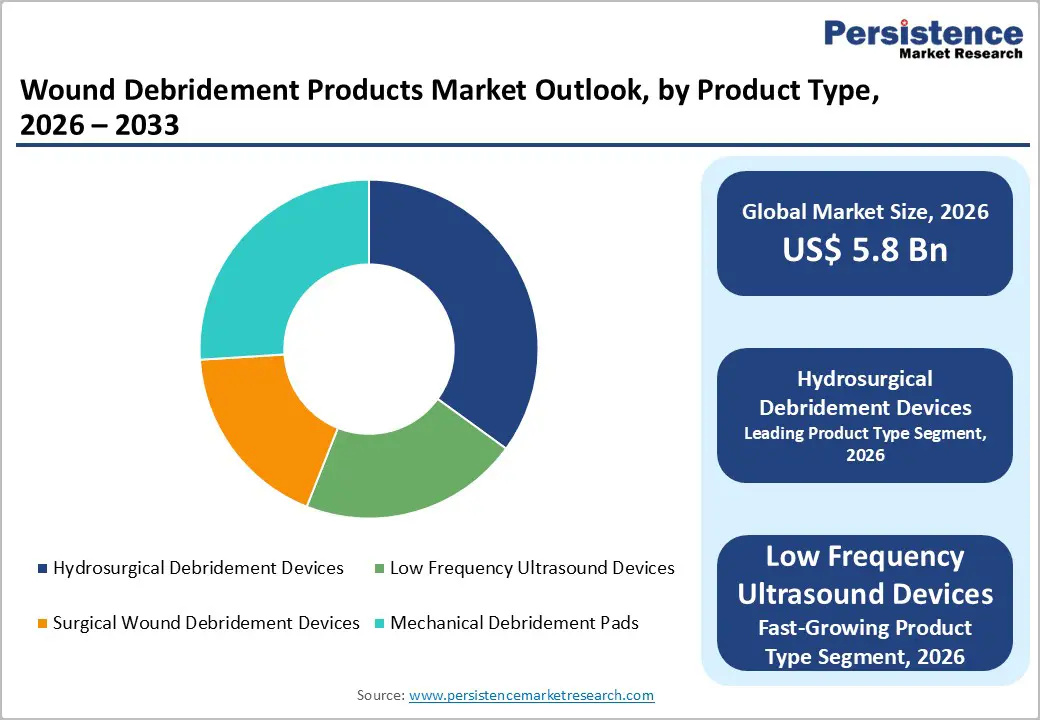

- Leading Product: Hydrosurgical debridement devices lead the product type segment with approximately 35% share in 2025, anchored by Smith & Nephew's VERSAJET clinical evidence demonstrating superior tissue selectivity, with endorsement from WOCN and EWMA clinical wound care guidelines.

- Fast-growing Product Type: Low-frequency ultrasound debridement devices are the fastest-growing product type, with expanded FDA clearance for homecare use by Bioventus (Misonix) and clinical evidence in Advances in Wound Care demonstrating superior healing outcomes in diabetic foot and venous leg ulcer wound cohorts.

- Opportunity: The key market opportunity lies in homecare and outpatient LFU debridement expansion, enabled by nurse-administered non-contact technology, serving over 783 million projected diabetics by 2045 per IDF, and the growing decentralization of advanced wound care beyond traditional hospital settings.

Market Dynamics

Drivers - Rising Global Prevalence of Chronic Wounds and Diabetic Foot Ulcers

The rapidly escalating global prevalence of chronic wounds, driven primarily by the diabetes epidemic, aging populations, and rising obesity rates, drives the wound debridement products market. The International Diabetes Federation (IDF) estimates approximately 537 million adults lived with diabetes in 2021, projected to rise to 783 million by 2045. Diabetic foot ulcers affect approximately 15–25% of diabetic patients over their lifetime, according to studies in The Lancet.

The National Pressure Injury Advisory Panel (NPIAP) reports that pressure injuries affect over 2.5 million patients annually in U.S. acute care facilities alone. Each chronic wound episode requiring management creates repeated debridement procedure needs, making this patient population a high-frequency, high-volume demand generator for debridement device and product suppliers.

Growing Preference for Advanced Energy-Based Debridement Over Traditional Sharp Methods

The clinical migration from conventional surgical sharp debridement toward advanced energy-based modalities, particularly hydrosurgical systems and low-frequency ultrasound devices, is materially expanding the wound debridement products market value by substituting simple manual procedures with higher-value capital and consumable device systems. Hydrosurgical debridement systems such as Smith & Nephew's VERSAJET and Medtronic's Mist Therapy have demonstrated superior selective tissue removal and reduced procedural time in clinical studies published in Wound Repair and Regeneration. The Wound, Ostomy and Continence Nurses Society (WOCN) endorses evidence-based debridement modality selection, with clinical evidence increasingly supporting advanced device-based approaches for complex chronic wounds, accelerating institutional adoption in wound care centers and hospital settings.

Restraints - High Capital Costs of Advanced Debridement Systems Limiting Adoption

Advanced wound debridement platforms, including hydrosurgical systems and low-frequency ultrasound devices, represent significant capital investments for healthcare facilities, with capital equipment costs ranging from US$ 15,000 to over US$ 50,000 per system. For smaller wound care clinics, community hospitals, and healthcare facilities in emerging economies, these acquisition costs create prohibitive adoption barriers. The ongoing consumable costs associated with hydrosurgical handpieces and ultrasound transducer maintenance further elevate the total cost of ownership, limiting broader market penetration beyond well-resourced hospital wound care departments in high-income countries.

Reimbursement Limitations and Coverage Gaps for Advanced Debridement Procedures

Inconsistent and restrictive reimbursement policies for advanced wound debridement procedures create significant barriers to market growth. In the United States, CMS (Centers for Medicare & Medicaid Services) reimbursement rates for advanced debridement procedures have faced periodic reductions, while coverage criteria for energy-based modalities remain restrictive in several states. In European markets, national health technology assessment bodies apply varying coverage standards for hydrosurgical and ultrasound debridement systems versus standard sharp debridement, creating uneven market development across countries and limiting the commercial opportunity for premium debridement device manufacturers.

Opportunities - Low Frequency Ultrasound Debridement Adoption in Outpatient and Homecare Settings

Low-frequency ultrasound (LFU) debridement devices represent the fastest-growing product segment and a compelling commercial opportunity for market participants targeting the expanding outpatient and home care wound management market. LFU systems, including Bioventus (Misonix)'s MIST Therapy and Enraf-Nonius platforms, deliver non-contact acoustic cavitation wound debridement that can be administered by trained wound care nurses without requiring physician presence, enabling deployment in outpatient wound clinics and even home care settings. Studies published in Advances in Wound Care document significantly improved wound healing outcomes with LFU therapy versus standard care in diabetic foot ulcer and venous leg ulcer cohorts. As home care infusion and wound care expand with the National Home Infusion Association (NHIA) documenting accelerating home wound care adoption, LFU debridement devices are positioned to capture significant new demand beyond traditional hospital wound care settings.

Market Expansion in Asia Pacific Driven by Chronic Disease Burden and Healthcare Modernization

Asia Pacific represents the most significant geographic growth opportunity for wound debridement product manufacturers, with the region hosting the world's largest and fastest-growing diabetic populations alongside rapidly expanding modern healthcare infrastructure. China alone has over 140 million diabetes patients per IDF estimates, with India close behind at over 101 million. Both countries are investing heavily in advanced wound care infrastructure under national health programs, India's Ayushman Bharat and China's Healthy China 2030 creating growing institutional demand for advanced debridement devices. Smith & Nephew plc and Mölnlycke Health Care AB are actively expanding Asia Pacific commercial infrastructure to capitalize on this structural demand growth opportunity through dedicated wound care center partnerships and distributor network expansion.

Category-wise Analysis

Product Type Insights

Hydrosurgical debridement devices lead the wound debridement products market by product type, commanding approximately 35% of total product-based market share in 2026. Hydrosurgical systems led by Smith & Nephew's VERSAJET Hydrosurgery System use high-velocity saline jets to precisely excise necrotic tissue, slough, biofilm, and debris while preserving healthy tissue structures, offering superior clinical outcomes versus traditional sharp debridement in complex wound types. Clinical evidence published in the Journal of Wound Care demonstrates significantly reduced procedure time and improved wound bed preparation with hydrosurgical systems. The devices' applicability across diabetic foot ulcers, burns, traumatic wounds, and surgical site infections, combined with their adoption in hospital operating theaters and advanced wound care centers, sustains the hydrosurgical segment's leading market position globally.

Application Analysis

Chronic ulcers represent the leading application segment in the wound debridement products market, accounting for approximately 42% of total application-based market share in 2025. This dominance reflects the enormous and growing global burden of chronic non-healing wounds, including diabetic foot ulcers, venous leg ulcers, and pressure injuries that require repeated debridement procedures throughout their clinical course. The International Diabetes Federation (IDF) estimates over 537 million diabetic patients globally, with significant foot ulcer prevalence. The National Pressure Injury Advisory Panel (NPIAP) further documents pressure injuries affecting millions of hospitalized patients annually. Chronic wounds' prolonged healing trajectories often require debridement at multiple clinical encounters, generating high per-patient lifetime debridement product consumption, sustaining the application segment's dominant revenue contribution.

End-user Insights

Hospitals constitute the dominant end-user segment in the wound debridement products market, accounting for approximately 55% of total end-user share in 2025. Hospitals serve as the primary site for complex wound debridement procedures, particularly for burns, surgical wounds, and advanced chronic ulcers requiring operating theater-level procedures or specialist wound care team intervention. The concentration of advanced hydrosurgical and ultrasound debridement capital equipment in hospital wound care departments and operating theaters reflects both the clinical complexity managed and the capital investment capacity of institutional healthcare settings. Joint Commission accreditation standards for wound management and hospital infection control protocols further embed structured debridement protocols into hospital wound care pathways, sustaining consistent product procurement volumes from established suppliers.

Regional Insights

North America Wound Debridement Products Market Trends and Insights

North America leads the global wound debridement products market with approximately 37% of total market share in 2025, driven by the United States' high chronic wound prevalence, well-developed wound care center infrastructure, strong reimbursement environment under CMS for debridement procedures, and rapid adoption of advanced hydrosurgical and LFU technologies by hospital wound care programs and outpatient specialty clinics.

U.S. Wound Debridement Products Market Size

The United States accounts for approximately 84% of the North American market in 2026. With over 6 million Americans affected by chronic wounds annually per AHRQ data and 2.5 million pressure injury cases per NPIAP, the U.S. generates the world's highest wound debridement product consumption, supported by Smith & Nephew and Integra LifeSciences leadership.

Europe Wound Debridement Products Market Trends and Insights

Europe is a mature wound debridement market governed by EU MDR 2017/745 and characterized by well-established national wound care protocols endorsed by bodies including the European Wound Management Association (EWMA). Germany, the U.K., and France lead European consumption, with hydrosurgical and advanced mechanical debridement devices gaining traction in hospital wound care departments through structured clinical pathway integration.

Germany Wound Debridement Products Market Size

Germany is likely to account for approximately 22% of the Europe wound debridement market in 2026. Germany's large diabetic population over 7.5 million people per Deutsches Institut für Medizinische Dokumentation und Information (DIMDI) combined with its well-developed hospital wound care infrastructure and B. Braun Melsungen AG's domestic manufacturing presence drive consistent advanced debridement product demand.

U.K. Wound Debridement Products Market Size

The United Kingdom represents approximately 17% of the European market in 2025. NHS England's Commissioning for Quality and Innovation (CQUIN) framework for wound care has driven structured debridement protocol implementation across NHS trusts. The National Institute for Health and Care Excellence (NICE) guidelines on wound management actively support evidence-based debridement modality selection in clinical practice.

France Wound Debridement Products Market Size

France accounts for approximately 14% of the European wound debridement products market in 2026. The Haute Autorité de Santé (HAS) provides wound care management guidelines that drive debridement product procurement across France's network of hospital wound care teams and independent wound care specialists. Mölnlycke Health Care AB and ConvaTec Group plc maintain strong French market positions.

Asia Pacific Wound Debridement Products Market Trends and Insights

Asia Pacific is the fastest-growing regional market for wound debridement products, anchored by the world's largest diabetic populations and rapidly expanding modern wound care infrastructure. China's Healthy China 2030 national health initiative has accelerated hospital wound care center development, with advanced debridement technologies gaining traction in tier-1 and tier-2 city hospitals as clinical wound management practices modernize toward international standards.

India Wound Debridement Products Market Size

India holds approximately 18% of the Asia Pacific market share in 2025, driven by over 101 million diabetic patients per IDF and a rapidly expanding private hospital wound care sector. Ayushman Bharat program hospital expansion and growing specialty wound care clinic networks are driving demand for both advanced and conventional debridement products across urban and peri-urban healthcare settings.

Competitive Landscape

The global wound debridement products market is moderately consolidated, with leading players including Smith & Nephew plc, Mölnlycke Health Care AB, ConvaTec Group plc, Integra LifeSciences Corporation, and Bioventus (Misonix) dominating the advanced energy-based debridement segment, while a broader group of wound care companies competes in mechanical and conventional product tiers. Key differentiators include clinical evidence portfolios for advanced debridement outcomes, specialized wound care sales force capabilities, integrated wound management system offerings, and partnerships with wound care center networks. Emerging business model trends include outcome-based supply agreements with hospital systems and subscription-based wound care program bundling encompassing debridement devices and consumables.

Key Developments:

- In May 2026, Convatec showcased its advanced wound care innovation pipeline at the European Wound Management Association (EWMA) 2026 conference, highlighting its evidence-led approach to improving healing outcomes and reshaping clinical practice through Wound Hygiene.

- In April 2026, Amrutanjan Health Care expanded its portfolio by launching new products across personal care, wound care, and pain management segments in the domestic Indian market.

- In October 2024, MediWound Ltd. announced the initiation of a controlled, multicenter Phase II clinical study, evaluating EscharEx® against collagenase ointment for venous leg ulcers.

Global Wound Debridement Products Market - Key Insights & Details

|

Key Insights |

Details |

|

Historical Market Value (2020) |

US$ 4.4 Billion |

|

Current Market Value (2026) |

US$ 5.8 Billion |

|

Projected Market Value (2033) |

US$ 8.4 Billion |

|

CAGR (2026–2033) |

5.3% |

|

Leading Region |

North America, ~37% market share (2025) |

|

Dominant Category (Product Type) |

Hydrosurgical Debridement Devices, ~35% share (2025) |

|

Top-ranking Category (Application) |

Chronic Ulcers, ~42% share (2025) |

|

Incremental Opportunity (2026–2033) |

US$ 2.6 Billion |

Companies Covered in Wound Debridement Products Market

- Smith & Nephew plc

- Mölnlycke Health Care AB

- ConvaTec Group plc

- Coloplast A/S

- Integra LifeSciences Corporation

- B. Braun Melsungen AG

- Medline Industries, Inc.

- Solventum (formerly 3M Healthcare)

- Medtronic plc

- Organogenesis Inc.

- Cardinal Health

- Paul Hartmann AG

- Bioventus (Misonix)

Frequently Asked Questions

The global wound debridement products market is estimated to be valued at US$ 5.8 billion in 2026.

The primary demand drivers are the global chronic wound epidemic, with over 6 million Americans affected annually per AHRQ and 2.5 million pressure injury cases per NPIAP, accelerating clinical adoption of advanced hydrosurgical systems over traditional sharp debridement, and rapidly expanding Asia Pacific wound care infrastructure driven by the world's largest diabetic patient concentrations.

North America leads the global wound debridement products market with approximately 37% of the total market share in 2025.

The most significant opportunity lies in low-frequency ultrasound debridement device expansion into home care and outpatient settings, where Bioventus (Misonix)'s FDA-cleared MIST Therapy enables nurse-administered non-contact debridement outside hospitals.

The key market players include Smith & Nephew plc, Mölnlycke Health Care AB, ConvaTec Group plc, Integra LifeSciences Corporation, Bioventus (Misonix), Coloplast A/S, B. Braun Melsungen AG, Medtronic plc, Solventum (formerly 3M Healthcare), Organogenesis Inc.,