- Electrical Equipment & Services

- Coil Wound Devices Market

Coil Wound Devices Market Size, Share, and Growth Forecast 2026 - 2033

Coil Wound Devices Market by Application (Electrical Motors (DC Motors, AC Motors), Transformers (Low Voltage, Medium Voltage, High Voltage), Valves & Actuators, Switches, Contactors & Relays, Other Electrical Devices), End-user (Transportation (Automotive, Railways, Marine, Aerospace), Energy (Power Generation & Distribution, Oil & Gas), Industrial Machinery & Equipment, Medical & Healthcare, Mining, Others), Device Type (Sensors, Bobbins, Electromagnetic Coils, Solenoids, Lightning Coil), by Regional Analysis, 2026 - 2033

Coil Wound Devices Market Size and Trend Analysis

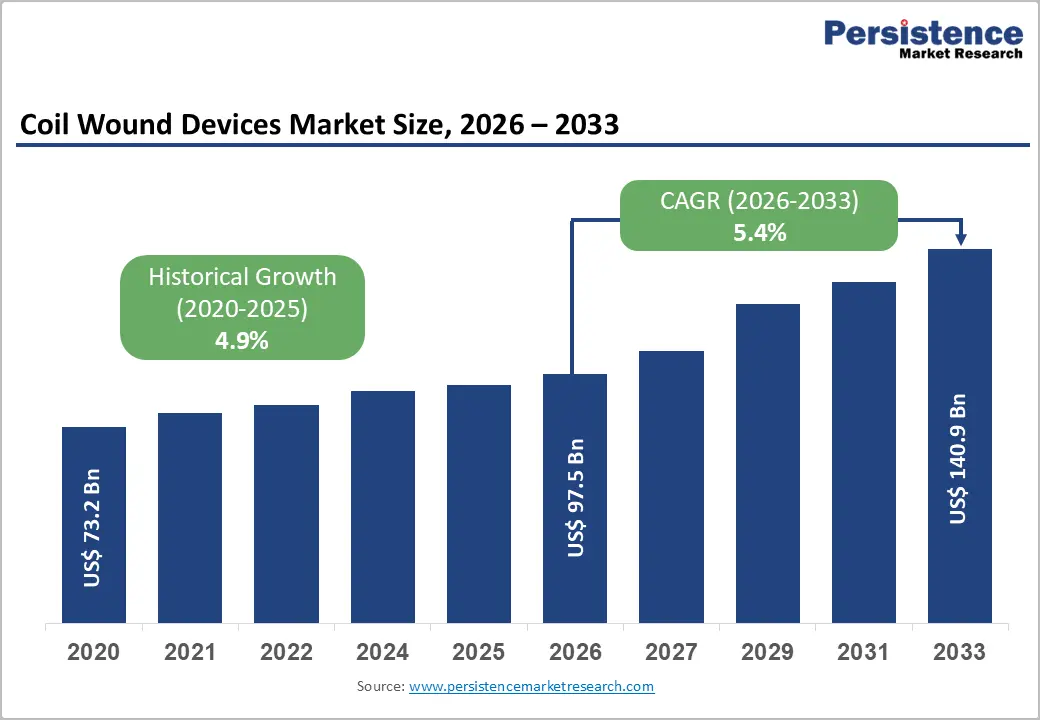

The global coil wound devices market size is expected to be valued at US$ 97.5 billion in 2026 and projected to reach US$ 140.9 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033.

Market expansion is fundamentally propelled by accelerating electrification across transportation and energy sectors, rapidly growing renewable energy infrastructure deployment, and widespread adoption of advanced automation in industrial manufacturing and facilities management. The global transition toward electric vehicles is driving substantial coil wound device demand for electric motors, power inverters, onboard chargers, and battery management systems, with electric vehicle sales projected to exceed 30 million units annually by 2030. Additionally, expanding power transmission and distribution networks in developing economies, combined with increasing investment in industrial automation and precision machinery, create consistent demand growth for transformers, electromagnetic coils, solenoids, and integrated electrical systems incorporating wound coil technology.

Key Industry Highlights:

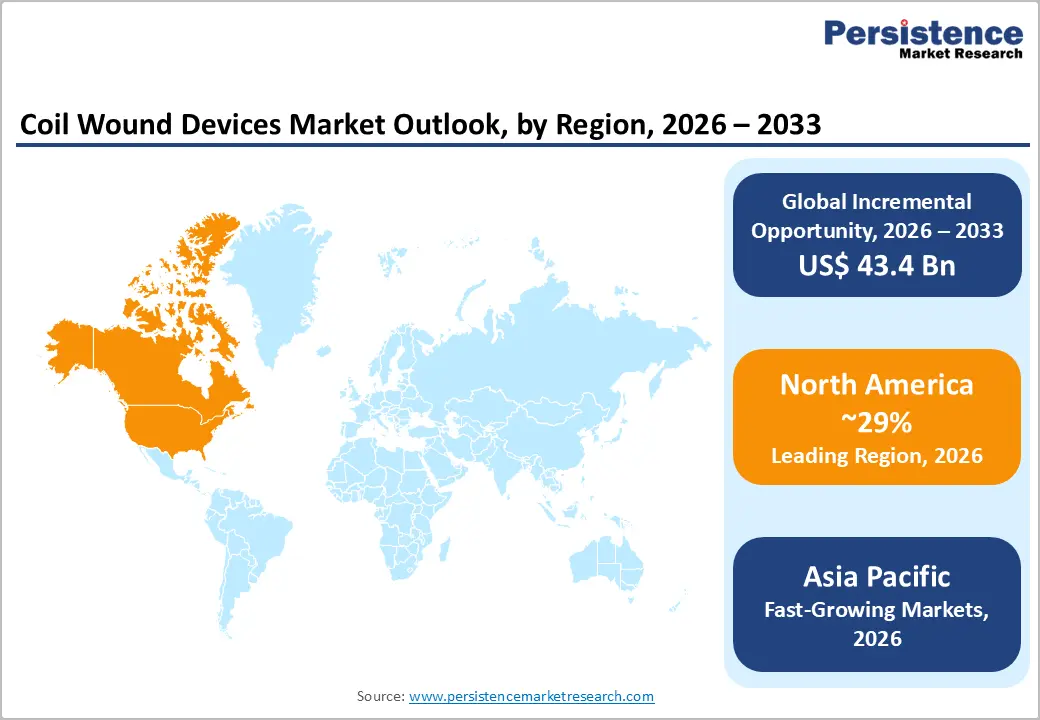

- Leading Region: North America leads the global Coil Wound Devices Market with approximately 29% share in 2025, supported by advanced manufacturing infrastructure, electric vehicle development, and power grid modernization investments driving substantial electromagnetic component demand.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, expected to post approximately 6.9% CAGR through 2033, driven by rapid industrialization, electric vehicle adoption in China and emerging markets, and expanding renewable energy infrastructure across the region.

- Dominant Segment: Electrical Motors dominate with roughly 32% share in 2025, driven by universal adoption across industrial equipment, transportation systems, and emerging electric vehicle platforms requiring sophisticated motor technologies.

- Fastest Growing Segment: Transportation is the fastest-growing sector with an estimated 7.3% CAGR through 2033, fueled by electric vehicle adoption exceeding 30 million annual units by 2030, requiring advanced coil wound electromagnetic components.

- Key Market Opportunity: Advanced material integration and superconducting coil technologies offer significant opportunity for developing next-generation transformers and motors achieving 99%+ efficiency, supporting power grid decarbonization and transportation electrification objectives.

| Key Insights | Details |

|---|---|

| Coil Wound Devices Market Size (2026E) | US$ 97.5 billion |

| Market Value Forecast (2033F) | US$ 140.9 billion |

| Projected Growth CAGR (2026 - 2033) | 5.4% |

| Historical Market Growth (2020 - 2025) | 4.9% |

Market Dynamics

Drivers - Rapid Electrification of Transportation and Growing Electric Vehicle Market

The automotive industry’s paradigm shift toward electrification represents the most significant growth driver for coil wound devices, as electric vehicle architectures require sophisticated electromagnetic components including high-performance electric motors, precise power electronic controllers, and advanced transformer systems. Global electric vehicle sales reached approximately 17 million units in 2024, with projections indicating 30+ million annual sales by 2030 according to the International Energy Agency, directly amplifying demand for specialized coil wound electromagnetic components.

Electric vehicle propulsion systems require complex stator and rotor assemblies fabricated using precision coil winding technology, with performance and efficiency directly dependent on wound coil quality and electromagnetic optimization. The European Union’s commitment to banning internal combustion engine vehicle sales by 2035, combined with supportive policies from governments worldwide, ensures sustained investment in EV production infrastructure and component development. Furthermore, advancing battery electric vehicle (BEV) and plug-in hybrid vehicle (PHEV) platform complexity, including integrated onboard chargers utilizing wound coil inductors and transformers, supports premium positioning and expanded addressable market for specialized coil wound device manufacturers.

Expansion of Renewable Energy Infrastructure and Power Grid Modernization

The accelerating global transition toward renewable energy sources is driving sustained demand for coil wound devices essential to power generation, transmission, and distribution infrastructure. Renewable energy capacity additions, particularly wind and solar installations, require substantial quantities of electromagnetic coils and transformers for energy conversion, voltage regulation, and system efficiency optimization. According to the International Renewable Energy Agency (IRENA), renewable energy capacity is expected to grow by approximately 50% through 2030, requiring parallel expansion of supporting electrical infrastructure incorporating coil wound transformers, inductors, and electromagnetic components.

Power grid modernization initiatives across developed and emerging economies emphasize efficiency improvements and integration of distributed energy resources, necessitating enhanced transformer technologies and electromagnetic devices. The United States Department of Energy estimates approximately US$ 2.7 trillion investment in power grid infrastructure modernization through 2035, directly translating to substantial demand for transformers, electromagnetic coils, and precision-wound electrical components essential for grid upgrades, capacity expansion, and integration of renewable energy sources and electric vehicle charging infrastructure.

Restraints - Supply Chain Complexity and Raw Material Price Volatility

Coil wound device manufacturing confronts significant supply chain challenges stemming from dependence on specialized materials including copper windings, insulation materials, and ferromagnetic cores subject to significant price volatility and intermittent supply constraints. Copper prices have experienced substantial volatility, ranging from US$ 8,000 to US$ 11,000 per metric ton over the past five years, creating cost pressures and margin compression for coil wound device manufacturers lacking hedging capabilities or long-term supply contracts.

Specialized insulation materials, rare earth magnets for advanced motor designs, and high-performance core materials face supply constraints exacerbated by geopolitical tensions and trade restrictions affecting global supply networks. These supply chain challenges necessitate substantial working capital investments, inventory management complexity, and risk exposure for manufacturers, particularly smaller firms lacking negotiating power with material suppliers and financial resources for advanced procurement strategies.

Technical Complexity and Precision Manufacturing Requirements

Coil wound device manufacturing demands exceptional precision and sophisticated technical expertise, as electromagnetic performance characteristics depend critically on winding patterns, coil geometry, material selection, and manufacturing tolerances. Advanced applications in electric vehicles, aerospace, and high-power energy transmission require increasingly stringent performance specifications, reliability standards, and environmental certifications that elevate manufacturing complexity and development costs.

Achieving consistent performance requires specialized equipment, skilled labor, quality control systems, and process optimization capabilities that represent significant capital investments constraining market entry for smaller manufacturers. The transition toward automated coil winding technologies, while improving efficiency, requires substantial capital investment and advanced engineering expertise, creating competitive advantages for established players with existing infrastructure but raising barriers for emerging market participants.

Opportunities - Integration of Advanced Materials and Next-Generation Coil Winding Technologies

Significant opportunities exist for coil wound device manufacturers developing advanced materials and innovative winding technologies enabling enhanced electromagnetic performance, improved thermal management, and reduced manufacturing complexity. Superconducting materials, including high-temperature superconductors for specialized applications, offer potential for transformational improvements in electromagnetic device efficiency, enabling breakthroughs in power transmission efficiency, electric motor performance, and energy storage system capabilities.

Research institutions including MIT and leading electrical equipment manufacturers have demonstrated superconducting transformer prototypes achieving 99.7% efficiency compared to conventional transformers at approximately 98.5%, supporting substantial efficiency gains and reduced operational losses across electrical grids. Nanomaterial integration, including copper nanoparticles and carbon-based additives, enables enhanced winding conductivity, improved thermal dissipation, and reduced coil resistance, supporting development of lighter, more efficient electromagnetic components.

Emerging Opportunities in Medical Device and Healthcare Applications

The healthcare and medical device sectors present expanding opportunities for precision coil wound devices utilized in diagnostic imaging equipment, surgical systems, therapeutic devices, and patient monitoring technologies. Medical imaging systems including MRI machines require sophisticated superconducting magnets and precision electromagnetic coils, creating specialized market segments with premium pricing and rigorous quality requirements. Surgical robotics systems, advanced diagnostic equipment, and emerging therapeutic technologies, including electromagnetic stimulation devices and precision dosing systems, incorporate specialized coil wound components requiring custom engineering and stringent biocompatibility certifications.

The global medical device market is projected to exceed US$ 600 billion annually by 2030, with electromagnetic device components representing growing market segments as advanced technology adoption accelerates. Coil wound device manufacturers developing specialized medical-grade products, obtaining relevant regulatory certifications, including FDA approval and ISO 13485 medical device quality standards, and establishing relationships with medical equipment manufacturers can access high-margin market segments with sustained growth driven by aging populations, increased healthcare expenditures, and expanding access to advanced diagnostic and therapeutic technologies.

Category-wise Analysis

Application Insights

Electrical motors represent the largest application segment, accounting for approximately 32% of market share in 2025 due to their widespread use across industrial machinery, transportation systems, consumer appliances, and electric vehicles. Motors rely heavily on coil-wound electromagnetic components to enable efficient energy conversion, torque generation, and speed control. Industrial motors dominate demand through continuous use in manufacturing equipment, HVAC systems, and automated production lines. The rapid growth of electric vehicles further reinforces this segment, as each EV integrates multiple high-performance motors requiring advanced electromagnetic designs. As electrification expands across industries, electrical motors remain the primary application driver sustaining volume demand and technological advancement in coil-wound components.

End-user Insights

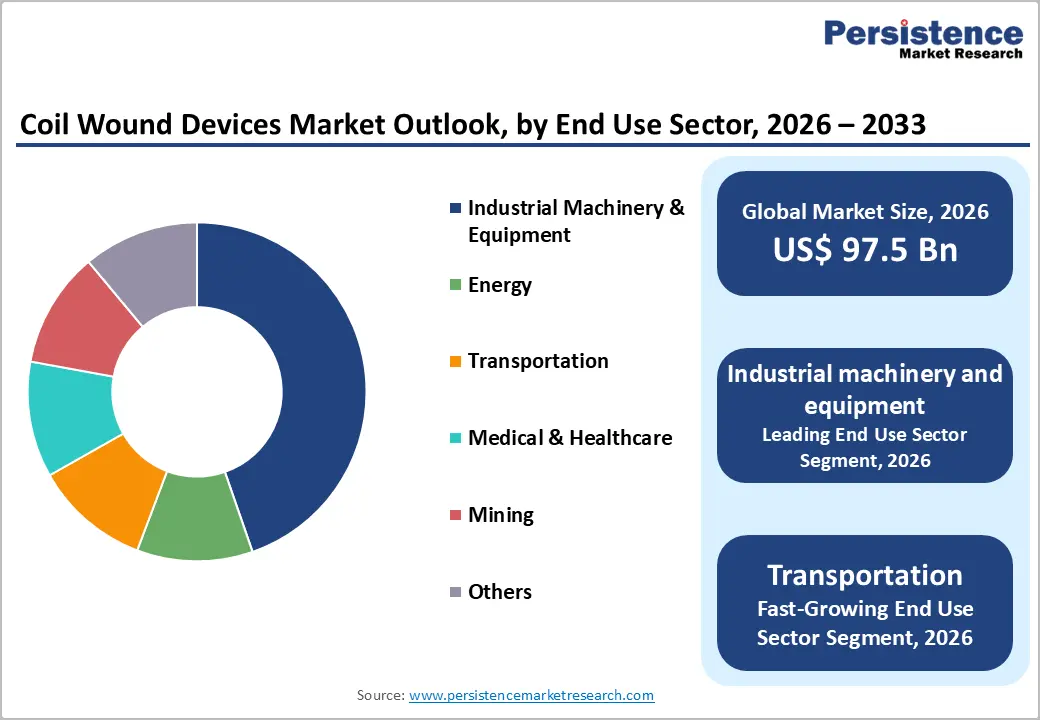

Industrial machinery and equipment dominate the end-use sector, holding approximately 41% market share in 2025, supported by rising investments in automation, process optimization, and advanced manufacturing. Coil-wound electromagnetic components are integral to industrial drives, robotic systems, power supplies, and precision control equipment, where reliability and efficiency are critical. Manufacturers increasingly deploy automated machinery to improve productivity, reduce downtime, and enhance operational precision, driving consistent demand for high-quality electromagnetic devices. The ongoing transition toward smart factories and digitally controlled production systems further strengthens this segment, making industrial machinery the core end-use contributor to overall market stability and long-term growth.

Device Type Insights

Electromagnetic coils dominate the device type segment, accounting for roughly 38% of market share in 2025 due to their foundational role in electrical and electronic systems. These coils form the core functional element in motors, transformers, inductors, and actuators, directly influencing system efficiency, thermal performance, and reliability. Their broad applicability across industrial, automotive, and energy systems ensures sustained demand. Continuous advancements in winding techniques, insulation materials, and thermal management are enhancing performance while reducing energy losses. As electrification and automation intensify across sectors, electromagnetic coils remain the most critical and widely adopted coil-wound component in the market.

Regional Insights

North America Coil Wound Devices Market Trends and Insights

North America accounts for approximately 29% of the global coil wound devices market in 2025, underpinned by a strong electrical equipment manufacturing base, advanced production technologies, and sustained investments in electrification. The United States remains the regional growth engine, supported by the presence of leading manufacturers such as Siemens, ABB, Honeywell, and Schneider Electric, alongside robust research and development capabilities.

Demand is reinforced by accelerating electric vehicle production, requiring high-precision motors, inductors, and power electronics incorporating advanced coil wound designs. In parallel, large-scale power grid modernization programs and renewable energy integration initiatives are driving steady requirements for transformers and voltage regulation equipment. The region’s focus on automation, manufacturing efficiency, and regulatory compliance supports premium demand for high-performance coil wound devices tailored to stringent safety, efficiency, and reliability standards.

Europe Coil Wound Devices Market Trends and Insights

Europe holds around 27% market share in 2025, characterized by strong regulatory emphasis on energy efficiency, decarbonization, and industrial automation. The European Union’s long-term climate objectives are translating into sustained investments in renewable energy, grid upgrades, and transportation electrification, all of which rely heavily on advanced coil wound electromagnetic components.

Countries such as Germany, France, the United Kingdom, and Spain serve as major demand centers due to their strong automotive and industrial manufacturing ecosystems. Leading European manufacturers continue to invest in innovation to meet stringent efficiency standards, including motor and transformer regulations under the Ecodesign framework. These regulatory drivers, combined with high adoption of automation and electric mobility solutions, position Europe as a premium market for technologically advanced and high-efficiency coil wound devices.

Asia Pacific Coil Wound Devices Market Trends and Insights

Asia Pacific is the fastest-growing regional market, projected to expand at approximately 6.9% CAGR through 2033, driven by rapid industrialization, large-scale manufacturing expansion, and accelerating electrification. China dominates regional demand as the world’s largest producer of electrical equipment, motors, transformers, and electric vehicles, supported by strong government policies promoting renewable energy and EV adoption.

Japan and South Korea contribute through advanced automotive and electronics manufacturing, emphasizing high-precision coil wound components. India is emerging as a high-potential market due to infrastructure development, expanding industrial capacity, and growing electric mobility adoption. Competitive manufacturing costs, improving technical capabilities, and rising domestic demand collectively establish Asia Pacific as the primary growth engine for the global coil wound devices market.

Competitive Landscape

The global coil wound devices market demonstrates a moderately consolidated structure, characterized by the presence of large multinational suppliers alongside a broad base of specialized and regional manufacturers. Market leadership is primarily supported by vertically integrated operations, wide-ranging product portfolios, and strong global distribution capabilities that enable suppliers to serve multiple end-use industries efficiently. Leading participants emphasize scale efficiencies, long-term supply agreements, and continuous investment in research and development to maintain technological leadership and cost competitiveness.

Business strategies increasingly focus on product differentiation through advanced materials, improved thermal management, and enhanced energy efficiency to meet evolving regulatory and performance requirements. Customization and application-specific design have become critical competitive levers, particularly for transportation, renewable energy, and industrial automation segments. Companies are also prioritizing capacity expansion in high-growth regions, supply chain localization, and digital manufacturing adoption to improve responsiveness and resilience. Overall, competitive positioning is shaped by a balance between scale-driven advantages and innovation-led specialization.

Key Market Developments

- August 2025: ABB announced breakthrough high-efficiency transformer design achieving 99.4% energy efficiency through advanced coil winding optimization and next-generation insulation materials, supporting power grid modernization initiatives across Europe and North America.

- December 2025: Naxatra Labs raised $3 million in Pre-Series A funding led by Rainmatter Investments, with participation from Mohit Tandon, Vijay Shekhar Sharma, and others, to scale electric motor manufacturing for EVs and industrial applications, aiming for 50,000 units monthly.

- July 2025: Orbis Electric launched HaloDrive, an advanced axial flux motor-generator with V8-matching torque, slimmer design, and 97% efficiency. It enables versatile e-Mobility applications, cuts costs by 35%, boosts fuel efficiency by 61%, and reduces CO2 emissions significantly.

Companies Covered in Coil Wound Devices Market

- ABB

- Honeywell International Inc.

- Parker Hannifin Corporation

- Danaher Corporation

- SIEMENS AG

- Magnet-Schultz of America Inc.

- Murata Manufacturing Co., Ltd.

- Emerson

- Schneider Electric

- TDK Corporation

- Asco Valve

- Hubbell Industrial Controls

- Standex Electronics

- Meidensha

- Toshiba

- Mitsubishi Electric Corporation

- GE Industrial Solutions

- Regal Rexnord

Frequently Asked Questions

The coil wound devices market is projected to reach US$ 97.5 billion in 2026.

Key drivers include electric vehicle adoption, power grid modernization, renewable energy expansion, and industrial automation.

North America leads the coil wound devices market with around 29% share in 2025.

Advanced materials and superconducting coil technologies represent the most attractive growth opportunity.

Key players include ABB, Siemens AG, Schneider Electric, Honeywell International, Parker Hannifin, Danaher Corporation, TDK Corporation, Murata Manufacturing, Emerson, Magnet-Schultz of America, and Toshiba, among others.