- Automotive Components & Materials

- Wheel Balancing Weights Market

Wheel Balancing Weights Market Size, Share, and Growth Forecast, 2025 - 2032

Wheel Balancing Weights Market By Product Type (Clip-on Weights, Adhesive Weights), Material Type (Lead, Zinc, Others), Vehicle Type (Passenger Cars, Others), Wheel Type (Steel Wheel, Alloy Wheel), Sales Channel, and Regional Analysis for 2025 - 2032

Wheel Balancing Weights Market Size and Trends Analysis

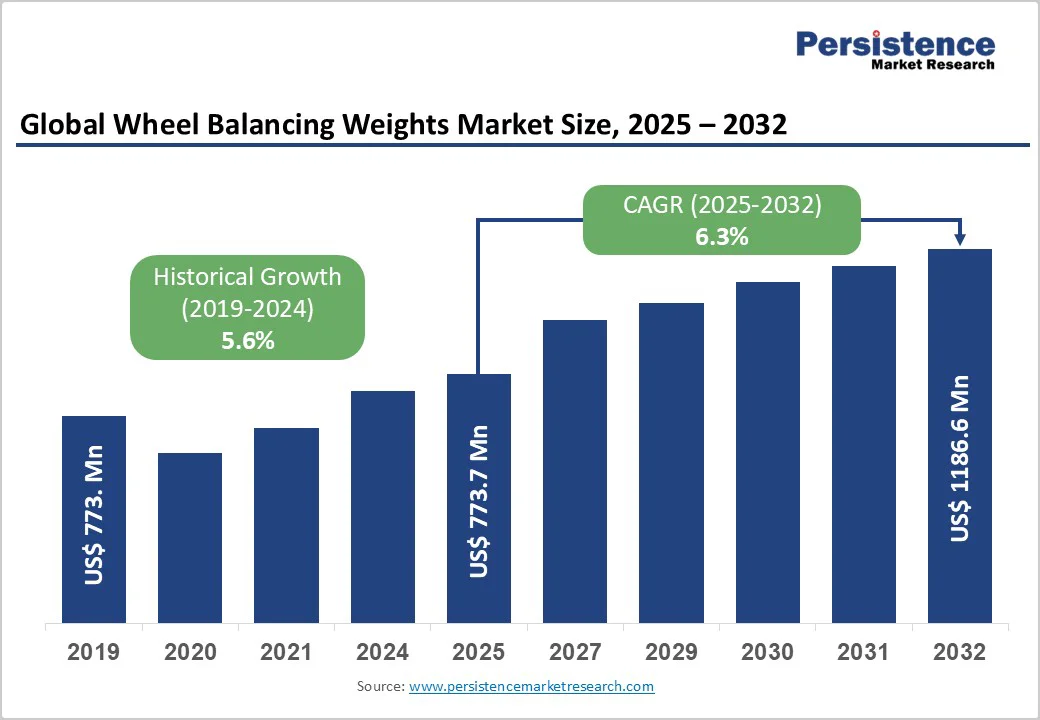

The global wheel balancing weights market size was valued at US$773.7 Million in 2025 and is projected to reach US$1,186.5 Million by 2032, growing at a CAGR of 5.1% during the forecast period from 2025 to 2032, driven by stringent quality requirements in automotive and aerospace manufacturing, growing metal fabrication activities globally, and the integration of automation technologies enabling efficient consumable utilization and reduced operational costs.

Key Industry Highlights:

- Product Technology Leadership: Clip-on weights command 63.4% market share through installation ease and widespread compatibility, while adhesive weights achieve the fastest growth, driven by alloy wheel adoption and aesthetic considerations in premium vehicle segments.

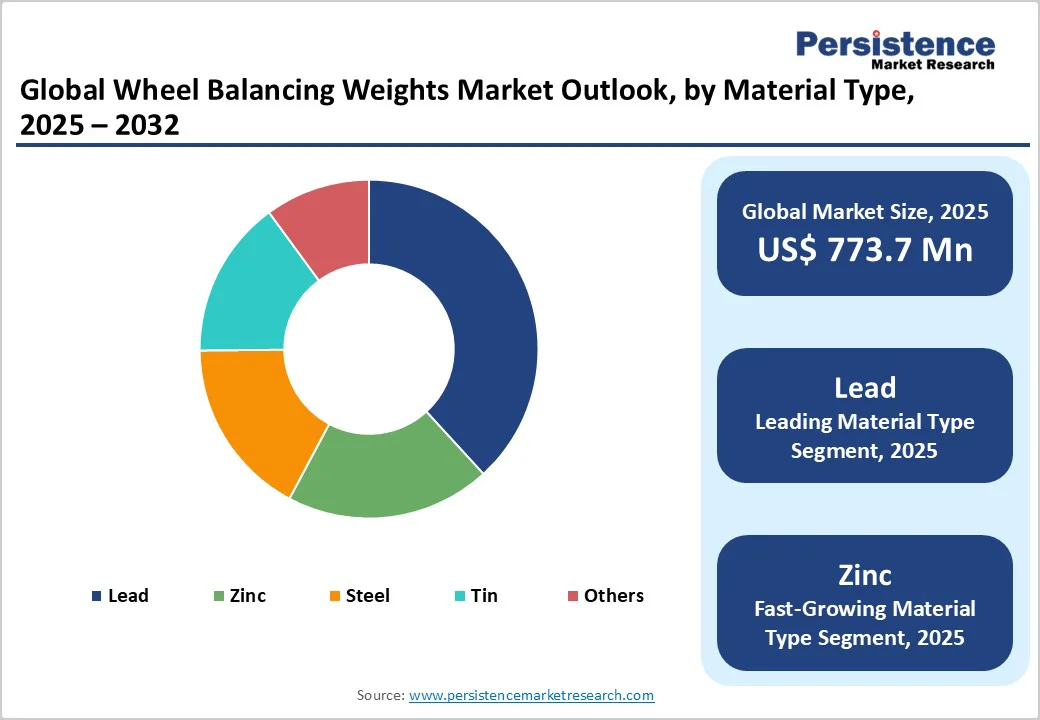

- Material Innovation Dynamics: Lead maintains 36% market dominance through cost-effectiveness and established infrastructure, with Zinc materials demonstrating the fastest growth, driven by environmental regulations and sustainable manufacturing initiatives.

- Vehicle Segmentation Performance: Passenger cars represent the dominant segment with a 60% market share through a large installed base and maintenance emphasis, while light commercial vehicles achieve the fastest growth, supported by e-commerce expansion and fleet modernization requirements.

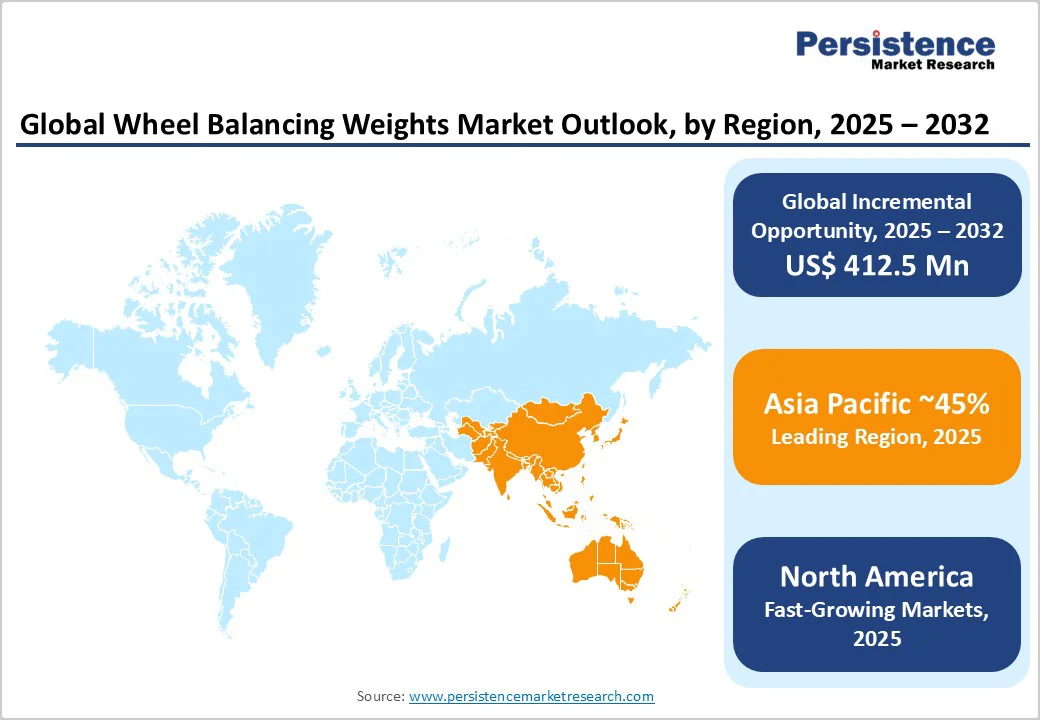

- Regional Growth Patterns: Asia Pacific leads with a 45% market share, driven by massive vehicle production and market expansion, while North America and Europe focus on environmental compliance and quality enhancement initiatives.

- Strategic Market Developments: 3M's eco-friendly adhesive innovations, WEGMANN's US$18 Million India facility, and Arconic's RFID technology partnership demonstrate industry focus on sustainability, geographic expansion, and digital integration.

| Key Insights | Details |

|---|---|

| Wheel Balancing Weights Market Size (2025E) | US$773.7 Mn |

| Market Value Forecast (2032F) | US$1,186.5 Mn |

| Projected Growth (CAGR 2025 to 2032) | 6.3% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Global Vehicle Production and Fleet Expansion

Global automotive production continues driving substantial demand for wheel balancing weights, with the International Organization of Motor Vehicle Manufacturers (OICA) estimating global car production reaching over 95 million units by 2025.

According to the U.S. Department of Transportation, the automotive sector is projected to reach a value of US$3.9 Trillion by 2025, highlighting substantial opportunities for wheel weight manufacturers within this expansive market landscape.

China remains the world's largest vehicle market with sales exceeding 28 million units in 2016, demonstrating year-on-year growth of 9% from 2015, while the Chinese Central Government projects automobile output will reach 30 million units by 2020 and 35 million by 2025.

The global automotive wheel market, valued at US$30 Billion in 2017, is projected to reach US$47.4 Billion by 2025, registering a CAGR of 5.7%, directly correlating with wheel balancing weight demand across passenger and commercial vehicle segments. The expanding vehicle population worldwide creates sustained demand for both original equipment manufacturer (OEM) installations and aftermarket replacement applications requiring regular wheel balancing services.

Stringent Emission Standards and Fuel Efficiency Requirements

Global regulatory frameworks increasingly mandate improved fuel efficiency and reduced emissions, driving demand for precise wheel balancing solutions that optimize tire performance and minimize rolling resistance. Stricter vehicle emission regulations globally necessitate precise wheel balancing to optimize fuel efficiency and reduce tire wear, with properly balanced wheels contributing to a 2-3% improvement in fuel economy.

The European Union committed to reducing carbon emissions by 20% compared to 1990 greenhouse gas emission levels, incentivizing automotive manufacturers to implement weight-saving technologies and maintain optimal vehicle performance through proper wheel balancing.

Improperly balanced wheels increase tire wear by up to 15%, create vibrations affecting fuel consumption, and compromise vehicle handling characteristics, making wheel balancing weights essential components for meeting environmental and performance standards.

The shift toward EVs, which require specialized balancing solutions to handle unique weight distributions and performance characteristics, creates additional market opportunities estimated at US$180-US$200 Million through 2032.

Barrier Analysis - Raw Material Price Volatility and Environmental Regulations

The wheel balancing weight market faces significant challenges from raw material price fluctuations, particularly for lead, which remains widely used in traditional wheel weights despite environmental concerns. Lead price volatility can impact overall production costs by 15-25%, leading to increased consumer prices and potential demand compression in price-sensitive market segments.

Increasing regulatory scrutiny regarding environmental impacts, with the EU implementing stringent regulations aimed at reducing lead use in automotive applications, forces manufacturers to adapt production processes and material compositions rapidly.

The transition from traditional lead weights to environmentally friendly alternatives, including zinc, steel, and tin, creates short-term cost pressures and requires manufacturing process modifications, quality validation, and market acceptance development. Supply chain vulnerabilities, including geographic concentration of raw material sources and potential disruption, affect production consistency and pricing stability across the industry.

Intense Market Competition and Counterfeit Product Proliferation

The wheel balancing weight market experiences intense competition among manufacturers, requiring constant innovation and differentiation to maintain market share and profitability. The proliferation of low-cost, inferior quality counterfeit products in aftermarket channels creates significant challenges for end-users regarding performance consistency, installation reliability, and long-term durability.

Price competition from low-cost producers, particularly in emerging markets, pressures profit margins and forces established manufacturers to balance quality maintenance with competitive pricing strategies.

Economic fluctuations, particularly related to post-pandemic recovery patterns, affect consumer spending power and demand for new vehicles and aftermarket services, creating market volatility and forecasting challenges for manufacturers and distributors managing inventory and production capacity planning.

Opportunity Analysis - Eco-Friendly Material Innovation and Sustainable Solutions

The global push toward environmental sustainability presents substantial opportunities for manufacturers developing and commercializing eco-friendly wheel balancing weight alternatives.

Traditional lead weights are being phased out due to environmental concerns and regulations aimed at reducing lead exposure, creating demand for alternatives, including zinc, steel, aluminum, and composite materials offering comparable performance while meeting environmental safety standards.

The development of innovative, lightweight materials, including advanced composites and engineered polymers, can cater to the growing demand for efficiency and performance enhancement in modern vehicles.

Material innovation focusing on enhanced durability, improved adhesion properties for adhesive weights, and extended service life represents significant differentiation opportunities valued at approximately US$140-160 Million by 2032.

Green technology investments and development of environmentally responsible manufacturing processes create competitive advantages while addressing regulatory compliance requirements and corporate sustainability commitments across the automotive supply chain.

Emerging Markets and Aftermarket Growth

Developing economies in Asia Pacific, Latin America, and Africa present substantial growth opportunities, with rapid industrialization, infrastructure development, and expanding middle-class populations driving vehicle ownership and associated service demand.

Rapid automotive industry growth across Asia Pacific, particularly in China and India, underpins rising demand for wheel balancing weights, supported by China’s extensive manufacturing base and India’s expanding vehicle output.

The aftermarket segment represents 25-30% of total market value and demonstrates faster growth compared to OEM channels, driven by increasing vehicle age requiring regular maintenance, expanding independent service networks, and growing consumer participation in vehicle maintenance activities.

The global installed vehicle base exceeding 1.4 billion units creates recurring demand for wheel balancing services, with an average balancing frequency of 6-12 months depending on usage patterns, supporting market stability and predictable revenue streams.

Market penetration rates for professional wheel balancing services remain below 45% in many emerging economies, representing approximately US$250-280 Million in additional market opportunity through 2032.

Segment-wise Analysis

Product Type Insights

Clip-on wheel weights hold a dominant 63.4% market share, favored for their easy installation, reusability, and compatibility with steel wheels commonly used in passenger and commercial vehicles.

Available in lead, steel, and zinc variants, these weights benefit from established manufacturing networks and technician familiarity, ensuring steady OEM and aftermarket demand. In contrast, adhesive wheel weights represent the fastest-growing segment, driven by the rising adoption of alloy wheels and aesthetic preferences for concealed placement.

Advanced adhesive technologies now offer superior temperature resistance, bonding strength, and durability. Their use in premium and luxury vehicles enhances market growth, supported by their clean appearance and suitability for modern wheel designs.

Material Type Analysis

Lead Retains Dominance, While Zinc Gains Momentum as a Sustainable Alternative

Lead wheel weights maintain a 36% market share due to their cost efficiency, high density (11.34 g/cm³), and mature production infrastructure, enabling compact, effective balancing solutions across traditional and commercial vehicle applications.

Despite this, environmental regulations and sustainability trends are curbing lead usage in developed markets. Conversely, zinc is the fastest-growing material segment, offering strong balancing performance, corrosion resistance, and full regulatory compliance.

With a density of 7.14 g/cm³, zinc provides reliable performance while appealing to eco-conscious consumers through recyclability and aesthetic advantages. Although zinc weights carry a 15-25% price premium, technological advancements and higher production volumes are improving affordability, solidifying zinc’s role as the preferred sustainable alternative in modern automotive markets.

Vehicle Type Insights

Passenger cars dominate the market with over 60% share, supported by a vast vehicle base, regular maintenance needs, and rising consumer focus on ride quality and tire life. Growth is reinforced by expanding alloy wheel adoption, premium maintenance spending, and widespread service network accessibility. This segment benefits from continuous replacement demand aligned with global passenger vehicle production and aftermarket expansion.

Light Commercial Vehicles (LCVs) represent the fastest-growing segment, fueled by e-commerce growth, last-mile delivery expansion, and fleet modernization. LCV applications require durable, high-capacity balancing solutions for heavy loads and long-duty cycles. Fleet operators increasingly prioritize wheel balancing to reduce fuel use (2-3%), extend tire life (20-30%), and optimize total cost of ownership, enhancing profitability and operational efficiency.

Regional Insights

North America Wheel Balancing Weights Market Trends

North America accounts for 22-25% of the market, valued at $170-193 million in 2025 and projected to reach $261-297 million by 2032. The U.S. dominates regional demand due to its mature automotive infrastructure, extensive aftermarket network, and high vehicle ownership rates. Key states such as California, Texas, New York, and Florida represent major consumption hubs driven by large vehicle fleets and active service industries.

The region’s regulatory framework prioritizes environmental compliance and safety, accelerating the shift toward lead-free materials. Competitive dynamics feature international and regional suppliers offering diverse clip-on and adhesive products. Investment trends highlight eco-friendly innovations, automation in manufacturing, and digitalized supply chains, enhancing operational efficiency and sustainability across the automotive aftermarket.

Europe Wheel Balancing Weights Market Trends

Europe holds 20-23% of the wheel balancing weights market, driven by strict EU environmental regulations, mature automotive service infrastructure, and advanced manufacturing standards. Germany, the U.K., and France dominate regional adoption due to robust automotive sectors and quality-driven maintenance practices. Northern European countries such as Denmark, Sweden, and the Netherlands are at the forefront of lead-free and recyclable weight adoption, reflecting strong environmental commitment.

The regulatory landscape enforces harmonized safety and recycling mandates, fostering innovation in zinc and steel alternatives. Established European manufacturers and global players compete through sustainable materials, certified quality, and circular economy initiatives, reinforcing Europe’s leadership in eco-friendly automotive components.

Asia Pacific Wheel Balancing Weights Market Trends

Asia Pacific leads the market with a 50-55% share. China, India, Japan, and South Korea drive demand through large-scale vehicle manufacturing, increasing ownership rates, and extensive service infrastructure. The region benefits from cost-efficient production, supportive government policies, and rapid automotive industry modernization.

Emerging economies such as Indonesia, Thailand, and Vietnam add momentum through expanding middle-class populations and infrastructure growth. Both global and domestic manufacturers strengthen regional presence via localized production and distribution networks. Investments focus on manufacturing expansion, advanced balancing technology adoption, and local supply chain development to meet rising OEM and aftermarket demand across diverse vehicle segments.

Competitive Landscape

The global wheel balancing weights market exhibits moderate fragmentation, with leading players maintaining significant positions through comprehensive product portfolios, established distribution networks, and manufacturing scale advantages. 3M Company, WG Wheelweights Group GmbH, and WEGMANN Automotive command substantial combined market share exceeding 30% through innovation leadership, global presence, and comprehensive product offerings spanning diverse weight types and material compositions.

Regional players, including Zhejiang Wanbang Technology Co., Ltd., Ningbo Jiejun Auto Parts Co., Ltd., and Shanghai Henglong Auto Accessories Co., Ltd., maintain strong positions in Asia Pacific markets through local manufacturing capabilities, cost competitiveness, and distribution network access.

The market structure includes multinational corporations, specialized weight manufacturers, and regional suppliers competing across different technology segments, material types, and price points through differentiated positioning and value-added services supporting diverse customer requirements globally.

Key Industry Developments

- In March 2024, 3M Company launched its latest generation of eco-friendly adhesive wheel weights, incorporating advanced acrylic adhesive formulations, providing enhanced temperature resistance from -40°C to +100°C while eliminating lead content, meeting stringent European Union regulatory requirements. The innovation addresses growing market demand for environmentally responsible solutions while maintaining superior performance characteristics.

- In August 2024, WEGMANN Automotive completed construction of a new manufacturing facility in India valued at US$18 Million, targeting the growing South Asian automotive market and establishing regional production capabilities serving domestic OEMs and aftermarket distributors. The facility incorporates automated production lines, quality control systems, and environmental management technologies supporting competitive positioning in cost-sensitive markets.

Companies Covered in Wheel Balancing Weights Market

- WEGMANN Automotive GmbH

- 3M Automotive

- Hennessy Industries, LLC (BADA)

- Wurth USA, Inc.

- HARTEC s.a.l (Hatco brand)

- Hangzhou Yaqiya Auto Parts Manufacturer Co., Ltd.

- BeiJiaDe Auto Accessory Co., Ltd.

- BendPak Inc.

- Banner GmbH

- Trax JH Ltd.

Frequently Asked Questions

The wheel balancing weights market is estimated to be valued at US$773.7 Million in 2025.

The key demand driver for the Wheel Balancing Weights market is the growing global vehicle production and expanding automotive aftermarket services that require precise wheel balancing for performance, safety, and tire longevity.

In 2025, the Asia Pacific region will dominate the market with an exceeding 40% revenue share in the wheel balancing weights market.

Among the product types, clip-on weights hold the highest preference, capturing beyond 63.4% of the market revenue share in 2025, surpassing other parts.

The key players in wheel balancing weights are WEGMANN Automotive GmbH, 3M Automotive, Hennessy Industries, LLC (BADA), Wurth USA, Inc., and HARTEC s.a.l.