- Medical Devices

- Diabetes Wearables Market

Diabetes Wearables Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Diabetes Wearables Market by Product Type (Continuous Glucose Monitoring (CGM), Insulin Delivery Systems, Others), Technology (Sensor-Based Glucose Monitoring, Optical / Noninvasive Glucose Monitoring, Connected / Bluetooth-Enabled Devices, Mobile App / Cloud Integrated Systems), Distribution Channel (Hospital pharmacies, Retail pharmacies, Online pharmacies), and Regional Analysis from 2026 to 2033.

Diabetes Wearables Market Outlook

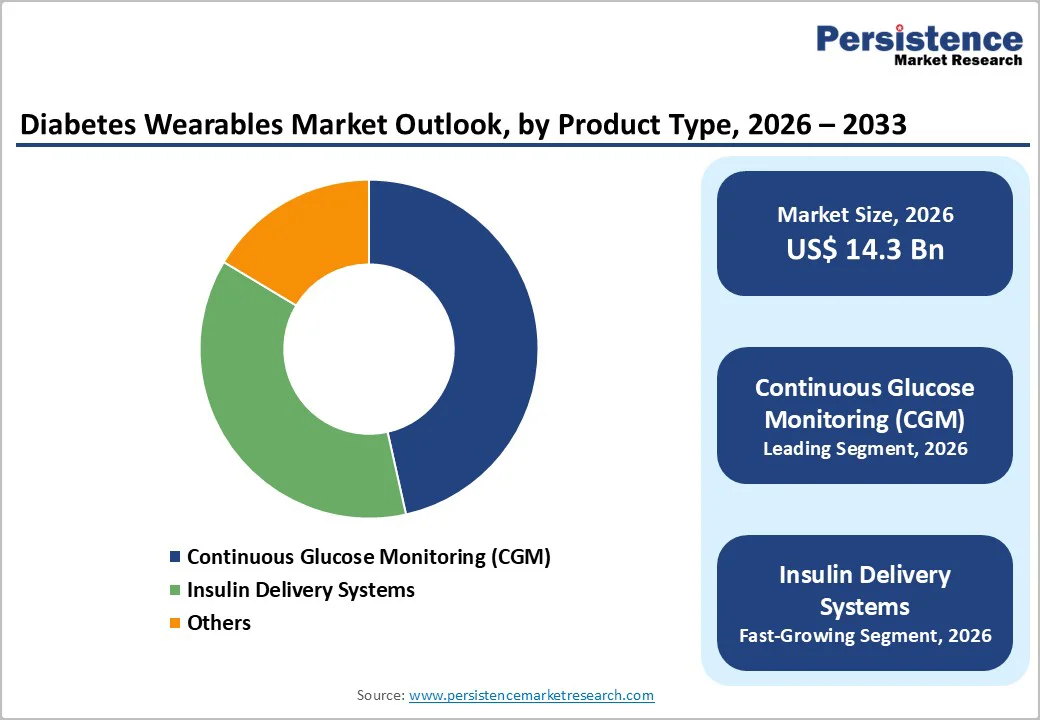

The global diabetes wearables Market is estimated to grow from US$ 14.3 Bn in 2026 to US$ 30.6 Bn by 2033. The market is projected to record a CAGR of 11.5% during the forecast period from 2026 to 2033.

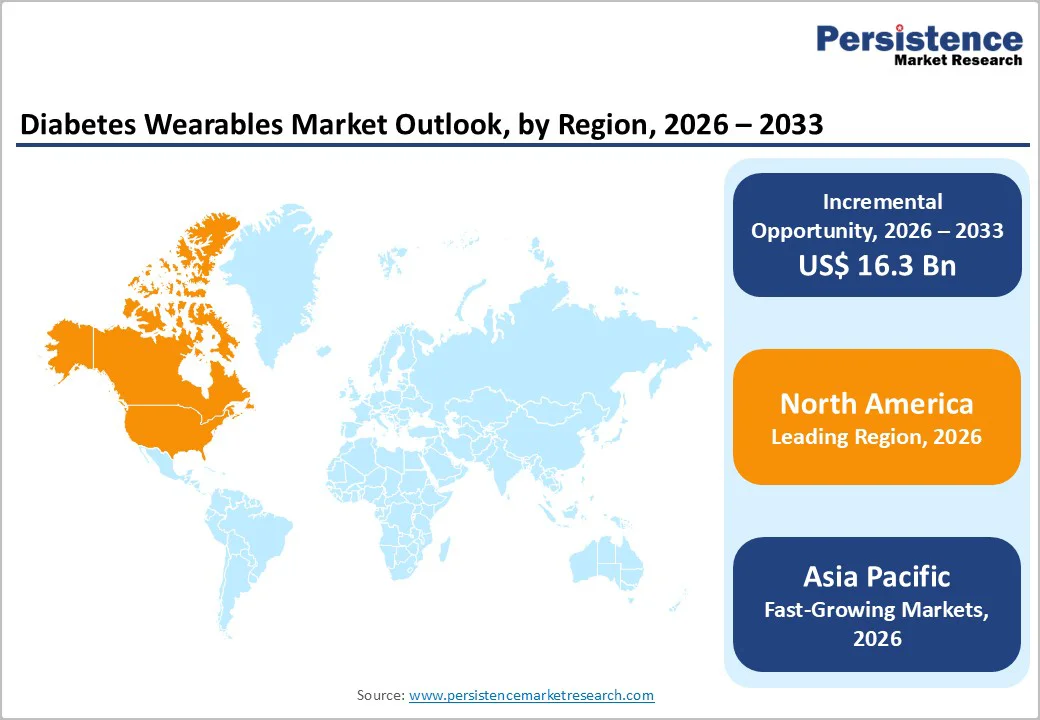

The diabetes wearables market is growing steadily, driven by rising diabetes prevalence and demand for continuous monitoring and connected insulin delivery. North America leads due to advanced healthcare, high awareness, and strong CGM adoption. Asia-Pacific is growing rapidly, driven by expanding healthcare access, rising incomes, and growing acceptance of digital health. Europe shows steady growth through mature markets and established healthcare systems.

Key Industry Highlights

- Dominant Segment: Continuous Glucose Monitoring (CGM) devices lead the market, accounting for around 46.5% in 2025, due to real-time monitoring, ease of use, and integration with insulin delivery systems. CGMs are widely adopted for glucose tracking, diabetes management, and integration with mobile and cloud platforms.

- Dominant Region: North America holds the largest share 42.8 owing to advanced healthcare infrastructure, high diabetes awareness, strong reimbursement support, and widespread adoption of CGMs and connected insulin delivery systems. Asia-Pacific is the fastest-growing region, supported by rising diabetes prevalence, expanding healthcare access, increasing disposable income, and digital health adoption.

- Market Drivers: Growth is driven by increasing diabetes prevalence, rising demand for continuous monitoring, adoption of connected devices, technological innovations, and growing awareness of remote and self-managed care.

- Market Opportunity: Key opportunities include noninvasive and next-generation CGM development, smart insulin pens, integration with AI-based management platforms, expansion into emerging markets, and strategic partnerships with hospitals, clinics, and telehealth providers.

| Key Insights | Details |

|---|---|

| Diabetes Wearables Market Size (2026E) | US$ 14.3 Bn |

| Market Value Forecast (2033F) | US$ 30.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 11.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 10.2% |

Market Dynamics

Driver – Increasing demand for continuous glucose monitoring (CGM) and remote monitoring solutions

Increasing demand for continuous glucose monitoring (CGM) and remote monitoring solutions is a key driver of the diabetes wearables market, as CGMs provide real-time, actionable glucose data that traditional finger-stick testing cannot match. Adoption of CGM among people with diabetes has risen sharply over recent years: for example, utilization of CGM in individuals with type?1 diabetes increased from about 20?% in 2010–2013 to nearly 50?% in 2016–2019 among commercially insured patients, reflecting growing clinical acceptance and patient demand for improved glucose control and reduced complications. This trend aligns with broader shifts toward remote monitoring and data-driven diabetes care pathways.

The demand for CGM is further justified by the rising global diabetes burden and expanding access to monitoring technology. In the United States alone, over 38 million people have diabetes, and advances in CGM technology, such as smartphone integration and insurance coverage expansions, are enhancing uptake. Government programs and subsidies targeting type?1 diabetes encourages broader use of CGM, creating sustained demand for continuous and remote glucose monitoring solutions.

Restraints – Limited insurance coverage for wearable diabetes devices in some countries

Limited insurance coverage for wearable diabetes devices is a notable restraint in the diabetes wearables market because access to continuous glucose monitoring (CGM) and related technologies often depends on reimbursement policies that vary widely by insurer and region. For example, in the United States, CGMs are covered under Medicare Part B only if specific eligibility criteria are met, and beneficiaries must pay a 20% coinsurance after a deductible, meaning substantial out-of-pocket costs can remain for many patients. Private insurance plans also require strict documentation or prior authorization for CGM approval, which can delay or prevent coverage even when clinicians support device use.

Globally, public insurance coverage for CGM remains inconsistent. In Canada, provincial health plans differ markedly in whether and how they reimburse CGMs; several provinces provide little or no coverage, forcing individuals to pay out of pocket for devices that can cost thousands of dollars annually. Limited public or private reimbursement in many regions means patients either forego advanced wearable glucose monitoring or bear high expenses, restricting adoption among lower-income populations. This disparity underscores how insurance gaps act as a barrier to broader adoption of wearable diabetes technology across both developed and emerging markets.

Opportunity – Integration with AI, cloud, and mobile platforms for predictive management

Integration with AI, cloud, and mobile platforms for predictive management is a significant opportunity in the diabetes wearables market because it enhances personalized care and real-time decision support. Wearable devices like continuous glucose monitors (CGMs) generate dense streams of glucose data throughout the day, and AI algorithms can analyze this data to predict glucose trends, personalize interventions, and improve clinical outcomes. Peer-reviewed studies show that AI paired with wearables supports adaptive insulin guidance and earlier detection of glycemic events, enabling tailored management strategies rather than reactive care.

Moreover, the integration of cloud and mobile technologies expands accessibility and remote monitoring, which is increasingly important for chronic conditions like diabetes. Software platforms such as mobile apps connected to CGM devices allow patients and clinicians to view glucose trends, share data remotely, and receive alerts or insights on the go. For example, CGM mobile applications with predictive analytics have been shown to improve “time in range” metrics—raising glucose control durations across diverse populations—thereby reducing the risk of hypoglycemia. and hyperglycemia. This convergence of AI, cloud, and mobile capabilities not only empowers patients with actionable insights but also supports clinicians in optimizing care pathways.

Category-wise Analysis

By Product Type, Continuous Glucose Monitoring (CGM)Dominates the Diabetes Wearables Market

Continuous Glucose Monitoring (CGM) dominates with a 46.5% share in 2025, as it delivers continuous, real-time glucose data that significantly improves diabetes management compared with traditional finger-stick testing, which is intermittent and less informative. CGMs lead wearable diabetes technology, with standalone CGM devices accounting for the largest share of global revenue and widespread adoption driven by convenience, accuracy, and digital integration. Continuous monitoring allows patients and clinicians to track glucose trends throughout the day and night, leading to better glycemic control and fewer complications. Increased utilization is evident in healthcare data: CGM use among people with type?1 diabetes rose from roughly 20% to nearly 50% over several years, reflecting clinical acceptance and patient demand for real-time monitoring over periodic testing.

By Technology, Sensor-Based Glucose Monitoring dominates due to real-time accuracy, continuous data, and widespread adoption

Sensor-based glucose monitoring dominates the diabetes wearables market because it provides continuous, real-time glucose data with clinically validated accuracy, improving diabetes management more than traditional intermittent testing. Wearable CGM sensors now generate up to 288 glucose readings per day, alerting users to hyperglycemia trends and enabling proactive therapeutic decisions. More than 40 million CGM devices have been used globally, with large installed bases in North America and Europe, demonstrating widespread adoption. Sensors accounted for 40–50% of the CGM device share in recent analyses, reflecting their central role in wearables. Continuous sensor technology also integrates seamlessly with mobile and cloud platforms, supporting remote monitoring and enhancing patient engagement in chronic care

Regional Insights

North America Diabetes Wearables Market Trends

North America dominates the diabetes wearables market with a 42.8% share in 2025, driven by high diabetes prevalence, advanced healthcare infrastructure, and strong adoption of continuous glucose monitoring (CGM) and connected technologies. In 2024, North America held the largest regional share (over 40?%) of the wearable diabetes management market, supported by early adoption of digital health devices and favorable reimbursement policies. The U.S. alone has more than 38 million people with diabetes and nearly 98 million with prediabetes, creating substantial demand for real-time glucose tracking and remote monitoring solutions. Medicare and Medicaid coverage expansions for CGMs have further increased utilization, with CGM use rising steadily across coverage types, reinforcing market leadership. These factors, coupled with high healthcare spending and widespread smartphone use, sustain North America’s market dominance.

Europe Diabetes Wearables Market Trends

Europe is an important region in the diabetes wearables market due to its high diabetes prevalence, aging population, and strong healthcare infrastructure. In 2023, the WHO reported that approximately 74 million adults in Europe live with diabetes, and the prevalence is increasing with lifestyle changes and aging. National health systems in countries like Germany, the United Kingdom, and France provide reimbursement or partial coverage for continuous glucose monitoring (CGM) devices, improving access and encouraging adoption. The region also emphasizes digital health and chronic disease management programs, integrating wearables with telemedicine and electronic health records, which supports patient engagement, remote monitoring, and timely clinical interventions.

Asia-Pacific Diabetes Wearables Market Trends

Asia-Pacific is the fastest-growing region in the Diabetes Wearables Market primarily because it bears a disproportionately large and rising diabetes burden alongside expanding healthcare access and digital technology adoption. In the Asia-Pacific region, approximately 227 million people live with type 2 diabetes, with about half undiagnosed, reflecting both scale and unmet management needs. Many countries in the region account for a significant share of global diabetes cases; for example, China alone has nearly 148 million adults with diabetes, representing a high prevalence that drives demand for continuous monitoring solutions. At the same time, nations such as India have over 89 million adults with diabetes, reinforcing the urgent need for wearable monitoring technologies. The rapid urbanization, lifestyle changes, and growing healthcare infrastructure in these populous countries increase accessibility and adoption of digital and wearable glucose monitoring tools, positioning Asia-Pacific as the fastest-growing regional market.

Market Competitive Landscape

Leading applications of diabetes wearables focus on glucose monitoring, insulin management, and remote patient care. Their effectiveness in improving glycemic control, preventing complications, and supporting personalized therapy drives clinical adoption. High accuracy, real-time data, and patient engagement enable widespread use, expand access to diabetes management, and fuel steady growth in the global diabetes wearables market.

Key Industry Developments:

- In May 2025, Medtronic announced it would separate its Diabetes business into a new standalone company as part of a strategic portfolio reorganization. The separation was planned to occur within about 18 months, likely through an initial public offering (IPO) and a subsequent split-off to create an independent entity focused exclusively on diabetes technologies, including insulin pumps and continuous glucose monitoring systems.

- In April 2025, Dexcom announced that the U.S. Food and Drug Administration (FDA) had cleared the Dexcom G7 15 Day Continuous Glucose Monitoring (CGM) System for adults aged 18 years and older with diabetes in the United States. The G7 15 Day system extended the sensor wear time to approximately 15.5 days with a mean absolute relative difference (MARD) of about 8.0%, making it one of the longest-lasting and most accurate CGM devices approved to date.

Companies Covered in Diabetes Wearables Market

- Abbott Laboratories

- Dexcom, Inc.

- Medtronic plc

- Roche Diabetes Care

- Insulet Corporation

- Tandem Diabetes Care

- Ascensia Diabetes Care

- Senseonics Holdings

- GlucoMe Ltd.

- DarioHealth Corp.

- GlySens Incorporated

- Ypsomed AG

- iHealth Labs, Inc.

- AgaMatrix, Inc.

- BioTelemetry, Inc.

- Others