- Sensors & Controls

- Wearable Biosensors Market

Wearable Biosensors Market Size, Share, and Growth Forecast 2025 - 2032

Wearable Biosensors Market by Product Type (Electrochemical Biosensors, Thermal Biosensors, Piezoelectric Biosensors, Accelerometer-Based Biosensors, Nanomechanical Biosensors, Optical Biosensors), by Distribution Channel (Online Sales, Offline Sales), by Application, by Regional Analysis, 2025 - 2032

Wearable Biosensors Market Size and Trend Analysis

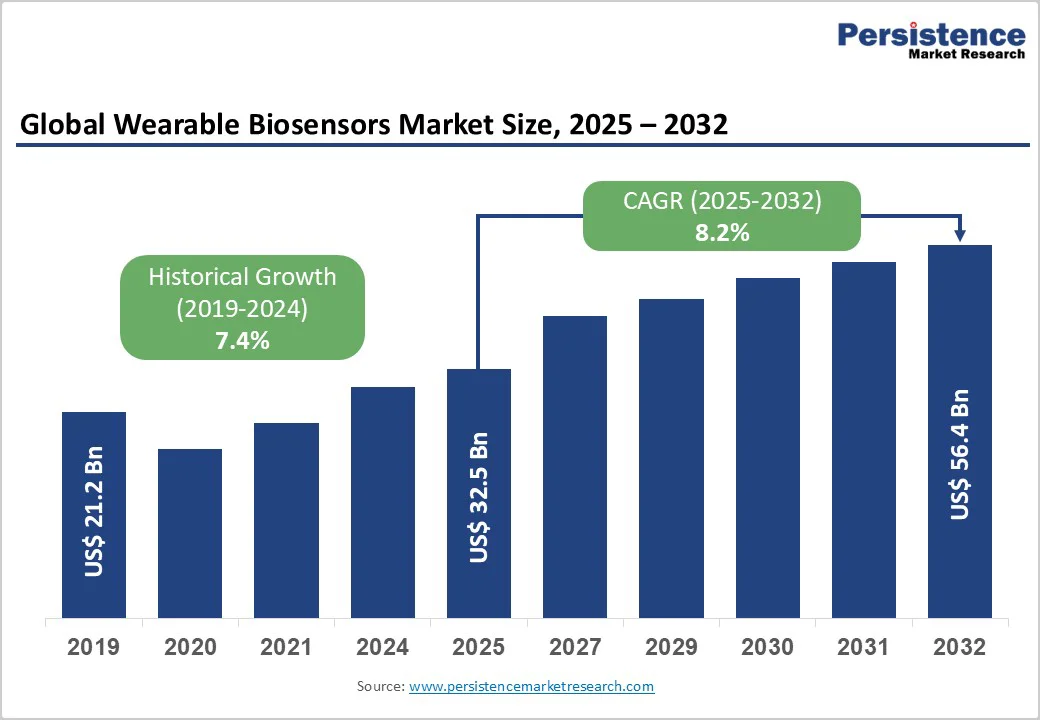

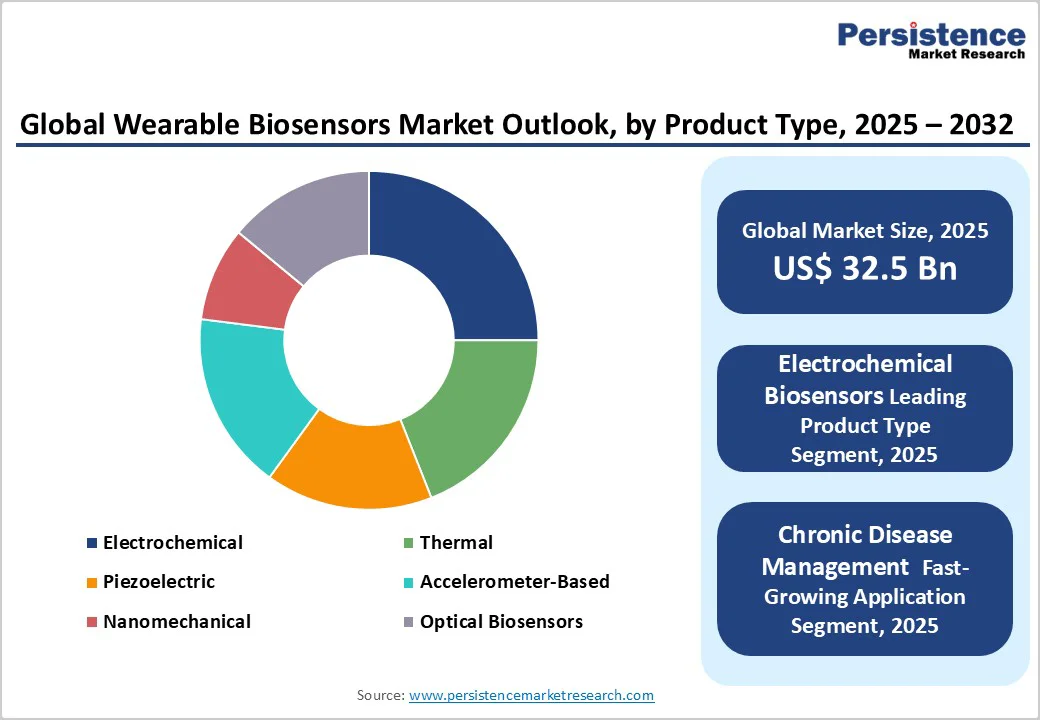

The global wearable biosensors market size was valued at US$ 32.5 Bn in 2025 and is projected to reach US$ 56.4 Bn by 2032, growing at a CAGR of 8.2% between 2025 and 2032.

Market growth is being fueled by the rise in global burden of chronic diseases such as diabetes and cardiovascular disorders, coupled with the rising adoption of remote patient monitoring and digital health integration. The convergence of AI-enabled biosensor technology, seamless smartphone connectivity, and advanced real-time analytics is transforming wearable biosensors into intelligent, clinical-grade diagnostic and predictive healthcare tools.

Key Market Highlights

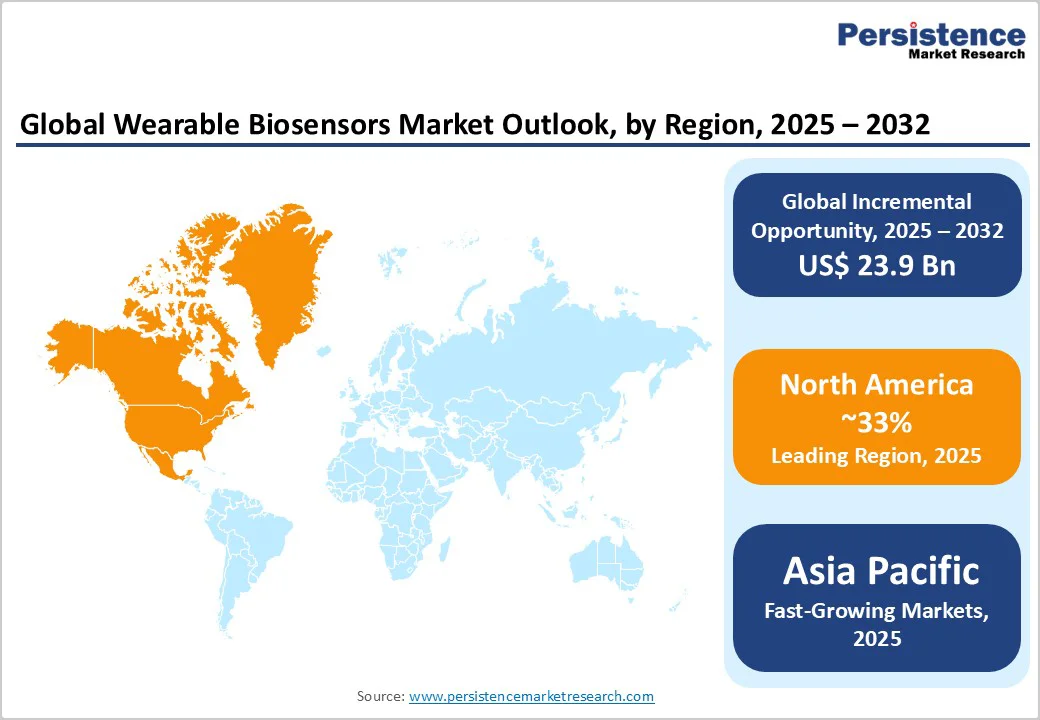

- Leading Region: North America dominates the wearable biosensors market, driven by robust regulatory frameworks, advanced R&D, strong clinical integration, and major brand investments in AI-enabled, high-accuracy biosensor platforms and telehealth infrastructure.

- Fastest Growing Region: Asia Pacific is the fastest-growing market, with strong expansion in China, India, and Japan backed by health tech incentives, population demand, and global manufacturing leadership.

- Leading Segment: Electrochemical Biosensors continue their leadership due to reliability and proven results in metabolic health, with CGM adoption accelerating.

- Fastest Growing Segment: Chronic Disease Management is the largest application, with global diabetes programs and healthcare systems embedding CGM and biosensor integration.

- Key Opportunity: New AI-driven analytics and predictive care models represent a transformative opportunity, with regulatory bodies actively supporting rapid device improvement and market entry.

| Key Insights | Details |

|---|---|

| Wearable Biosensors Market Size (2025E) | US$ 32.5 Billion |

| Market Value Forecast (2032F) | US$ 56.4 Billion |

| Projected Growth CAGR (2025-2032) | 8.2% |

| Historical Market Growth (2019-2024) | 7.4% |

Market Dynamics

Driver - Rise in Prevalence of Chronic Diseases Accelerating Biosensor Adoption

The global surge in chronic diseases is fundamentally reshaping healthcare delivery systems and driving the widespread adoption of wearable biosensors. Currently, over 1 billion people suffer from chronic ailments, with cardiovascular diseases alone causing more than 17.9 million deaths annually. Diabetes and obesity combined affect nearly one in eight people globally, presenting immense demand for continuous health monitoring solutions.

In India, diabetic patients are projected to surpass 101 million by 2030, underscoring an urgent need for preventive and real-time health tracking. Wearable biosensors play a crucial role in enabling timely medical interventions by continuously monitoring vital parameters such as glucose levels, heart rate, and oxygen saturation.

In the United States, the expansion of the wearable healthcare devices market reflects this transition toward preventive and personalized healthcare, where biosensors serve as an essential bridge between medical diagnosis and daily health management.

Technological Advancements Enhancing Precision and User Experience

Rapid technological advancements are the backbone of the wearable biosensors market’s growth. Innovations in miniaturization, flexible sensor materials, and AI integration have dramatically improved device precision, response time, and user convenience.

The integration of Internet of Things (IoT) platforms enables seamless transmission of biosensor data to healthcare providers and cloud systems for advanced analytics. Continuous Glucose Monitoring (CGM) devices, for example, have evolved to achieve less than 10% mean absolute relative difference, with sensor lifespans extending to 14 days.

Nanomaterial-based sensors enhance detection sensitivity, enabling applications in metabolic health, cancer biomarker tracking, and infectious disease diagnostics. Furthermore, the convergence of wearable biosensors with smartwatches, fitness trackers, and other wearable electronics is bridging the gap between fitness and clinical healthcare.

This convergence fosters broader mainstream acceptance as consumers increasingly adopt health technologies that blend wellness, style, and functionality.

Restraint - Data Privacy and Cybersecurity Concerns Undermining User Trust

Despite significant technological progress, persistent concerns about data privacy and cybersecurity continue to hinder mass adoption of wearable biosensors. These devices collect and transmit highly sensitive, personally identifiable health information, making them potential targets for breaches or unauthorized access. Inadequate encryption, insecure data storage, and weak authentication protocols exacerbate the risks of misuse.

Regulations such as the Health Insurance Portability and Accountability Act (HIPAA) in the U.S. and the General Data Protection Regulation (GDPR) in Europe have established strict compliance standards; however, consumer confidence remains fragile.

Surveys indicate that nearly 30% of users are comfortable sharing health data only with their physicians or themselves, reflecting ongoing mistrust in digital ecosystems. The U.S. wearable device market highlights the urgent need for robust cybersecurity frameworks, blockchain-based data management, and transparent privacy policies to build trust and ensure responsible data utilization.

High Device Costs and Inconsistent Insurance Coverage Limiting Accessibility

Affordability remains a significant barrier to the global proliferation of wearable biosensors, particularly in developing regions. Medical-grade biosensors, which offer clinical-grade accuracy, often come at a premium cost, restricting access for lower-income populations and underfunded healthcare systems.

Regulatory complexities further elevate expenses, as clinical validation and approval processes are both time-intensive and costly. Additionally, inconsistent insurance reimbursement policies across countries create uncertainty for both manufacturers and consumers.

In several emerging markets across Latin America, the Middle East, and Africa, limited healthcare infrastructure and low insurance penetration further slow adoption. While wellness-oriented biosensors are gaining traction, clinical-grade devices still face cost constraints that restrict scalability.

To overcome this challenge, industry stakeholders and regulators must collaborate to develop cost-effective production models, standardized approval processes, and comprehensive reimbursement frameworks that can enhance affordability and market inclusivity.

Opportunity - Artificial Intelligence Revolutionizing Predictive and Preventive Healthcare

The integration of Artificial Intelligence (AI) into wearable biosensors is transforming healthcare by shifting from reactive to predictive care models. Advanced machine learning algorithms continuously analyze real-time and historical biosensor data to detect early indicators of disease progression or potential health deterioration.

This capability supports personalized medical interventions, improving patient outcomes and reducing hospitalizations. Regulatory bodies such as the U.S. FDA and the UK’s MHRA are experimenting with AI regulatory sandboxes, encouraging innovation while ensuring safety and compliance.

Federated learning allows AI systems to train on decentralized health data without compromising user privacy. This convergence of AI and biosensing technologies is accelerating advancements in chronic disease management, mental health monitoring, and smart baby wearables, strengthening the market’s predictive and preventive healthcare potential.

Expanding Applications Beyond Healthcare Driving Market Diversification

The wearable biosensors market is expanding beyond traditional healthcare into mental wellness, occupational safety, and food safety domains. In mental health, biosensors track physiological stress indicators such as heart rate variability and cortisol levels, enabling timely interventions for anxiety or depression.

In workplace safety, continuous monitoring of fatigue or exposure to harmful substances enhances employee well-being and productivity. Asia Pacific emerges as a high-growth region, driven by its 68% mobile internet penetration, technological maturity, and proactive government support.

China’s inclusion of medical sensor technologies in its encouraged investment catalogue and India’s rising diabetes prevalence create favourable conditions for large-scale adoption. The convergence of digital infrastructure, public health priorities, and industrial safety needs positions emerging markets as key growth engines for next-generation biosensor applications.

Category-wise Analysis

Product Type Insights

Electrochemical Biosensors dominate with about 25% market share in 2025, due to successful glucose monitoring integration and metabolic disorder management. These biosensors offer rapid response, superior accuracy, and scalability for mass production. FDA-cleared CGM systems from firms like Dexcom and Abbott highlight commercial viability and foster further innovation in the wearable healthcare devices market.

Distribution Channel Analysis

Offline Sales remain the largest channel, with approximately 58% share in 2025. In-person consultations, product demonstration, and support from healthcare providers drive this preference, especially for advanced or prescription-wearable biosensors.

Online Sales are rapidly growing, with industry estimates showing 35% of health-conscious buyers preferring digital purchases in 2024 due to convenience and variety. E-commerce expansion now enables direct-to-consumer access, particularly among major brands such as Huawei and Withings.

Application Analysis

Chronic disease management leads the application, with about 34% share in 2025. CGM is rapidly scaling globally, especially in diabetes care, where about 90% of Type 1 diabetes patients in the UK use these devices. Hospitals increasingly use biosensor data for medication adherence and outcome optimization.

The Fitness and Wellness segment is the fastest growing, with about 75% of surveyed consumers open to wearable adoption for new metrics like stress or sleep. This strengthens biosensors’ role within the broader Wearable Electronics Market.

Regional Insights

North America Wearable Biosensors Market Trends

North America commands approximately 33% of the global wearable biosensors market by 2025, with the United States maintaining its lead due to strong technological innovation, supportive regulation, and growing consumer acceptance. The FDA’s rigorous approval processes ensure product reliability, encouraging trust and market stability.

Moreover, insurance companies increasingly recognize the value of biosensors in chronic disease management, enhancing reimbursement rates and accelerating adoption. The region’s strong telehealth infrastructure, significantly strengthened during the COVID-19 pandemic, continues to integrate biosensor data into remote monitoring systems.

Major technology brands such as Apple, Fitbit, and Garmin, along with medical device leaders, have transformed biosensors into integral components of connected healthcare ecosystems.

Europe Wearable Biosensors Market Trends

Europe demonstrates strong market growth, driven by its well-established healthcare infrastructure, stringent regulatory frameworks, and widespread digital health adoption. Key markets such as Germany, the UK, France, and Spain are leading regional advancements, supported by regulatory clarity from agencies like the MHRA and implementation of the EU Medical Device Regulation (MDR) and CE-marking standards.

With nearly 46% of adults in Europe living with chronic diseases, demand for biosensors in continuous glucose monitoring and cardiovascular care is rising rapidly. The NHS in the UK has played a pivotal role in integrating continuous glucose monitoring (CGM) devices into diabetic treatment programs. EU-funded research initiatives are accelerating the development of non-invasive, biodegradable, and eco-friendly biosensors aligned with the region’s sustainability goals.

Asia Pacific Wearable Biosensors Market Trends

Asia Pacific is witnessing the fastest expansion in the wearable biosensors market, propelled by increasing smartphone penetration, digital health adoption, and strong public healthcare investments. Major economies such as China, Japan, and India are at the forefront of this growth.

China’s government now includes sensor technology in its national encouraged investment policy, fostering a favorable ecosystem for both international and domestic players such as Huawei, which emerged as the world’s leading wearable device shipper in early 2024.

In India, rising rates of chronic diseases like diabetes and cardiovascular disorders are fueling demand for remote monitoring solutions. Meanwhile, Japan’s ageing population, projected to reach about 40% aged 65 and above by 2060, is driving innovation in elderly care and home diagnostics. The region’s expanding digital infrastructure and government-backed health initiatives make it a key engine of future biosensor market growth.

Competitive Landscape

The wearable biosensors market is moderately consolidated, with multinational technology, electronics, and healthcare firms dominating. Leaders such as Molex LLC, TDK Corporation, VitalConnect, Panasonic Corporation, TE Connectivity, Texas Instruments, Zimmer & Peacock AS, Infineon Technologies AG, Withings SA, Broadcom, and Koninklijke Philips N.V. combine extensive distribution, R&D, and regulatory expertise.

Differentiation occurs via sensors, AI integration, miniaturization, and ecosystem partnerships (with telehealth, insurance, digital health service providers). Quality and regulatory compliance (e.g., FDA clearance, CE Mark, ISO 13485) are critical, especially for new med-tech entrants.

Key Market Developments

- August 2024: Huawei Technologies unveiled its HUAWEI TruSense System, capable of measuring over 60 health and wellness indicators across six major body systems using integrated advanced sensors and AI-driven analytics.

- October 2023: the NHS AI Lab in the UK, in partnership with the Medicines and Healthcare products Regulatory Agency (MHRA) - committed £1 million to establish a regulatory sandbox for AI-based medical devices (AI as a Medical Device) to accelerate biosensor approval.

- May 2023: Dexcom, Inc. announced a collaboration with Oura Health Oy to integrate continuous glucose monitoring with sleep and other health metrics, advancing the development of multi-sensor health platforms.

Companies Covered in Wearable Biosensors Market

- Molex LLC

- TDK Corporation

- VitalConnect

- Huawei Technologies

- Robert Bosch GmbH

- Panasonic Corporation

- TE Connectivity

- Texas Instruments Incorporated

- Zimmer & Peacock AS

- Infineon Technologies AG

- Withings SA

- Broadcom

- Koninklijke Philips N.V.

- Abbott Laboratories

- Dexcom, Inc.

- Medtronic plc

- Apple Inc.

- Fitbit (Google)

- Garmin

- Samsung Electronics

- Xiaomi Corporation

- Oura Health

- Analog Devices, Inc.

- STMicroelectronics

- Bosch Sensortec

Frequently Asked Questions

The global wearable biosensors market is projected to reach US$ 56.4 billion by 2032, demonstrating an 8.2% CAGR driven by chronic disease prevalence and tech innovation.

Prevalent chronic diseases, IoT integration, AI analytics, and expanded use in diabetes/cardiac monitoring, all motivate adoption, with a rapid uptick seen during the pandemic in digital health usage.

Electrochemical Biosensors lead, with their 72%+ share attributed to clinical success in glucose and metabolic monitoring, reliability, and regulatory clearance.

North America holds the largest share due to robust health innovation and regulatory clarity.

AI-powered predictive analytics, real-time decision support, and privacy-centric machine learning open future growth, driven by investments in regulatory sandboxes and major health tech collaborations.

Major global leaders include Molex LLC, TDK Corporation, VitalConnect, Huawei Technologies, Alibaba Laboratories, Panasonic Corporation, TE Connectivity, Texas Instruments, Zimmer & Peacock AS, Infineon Technologies AG, Withings SA, Broadcom, Koninklijke Philips N.V., Apple, Fitbit, Garmin, and Samsung.