- Nutraceuticals & Functional Foods

- Vitamins and Supplements Market

Vitamins and Supplements Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Vitamins and Supplements Market by Product Type (Vitamins, Minerals, Omega-3 Fatty Acids, Probiotics, Botanicals, Others), by Form (Tablets & Capsules, Powders, Gummies, Liquids, Softgels, Others), by Sales Channel (Hypermarkets/Supermarkets, Pharmacies & Drugstores, Health & Wellness Stores, Specialty Stores, Online Retail, Others), by Regional Analysis, 2026-2033

Vitamins and Supplements Market Size and Share Analysis

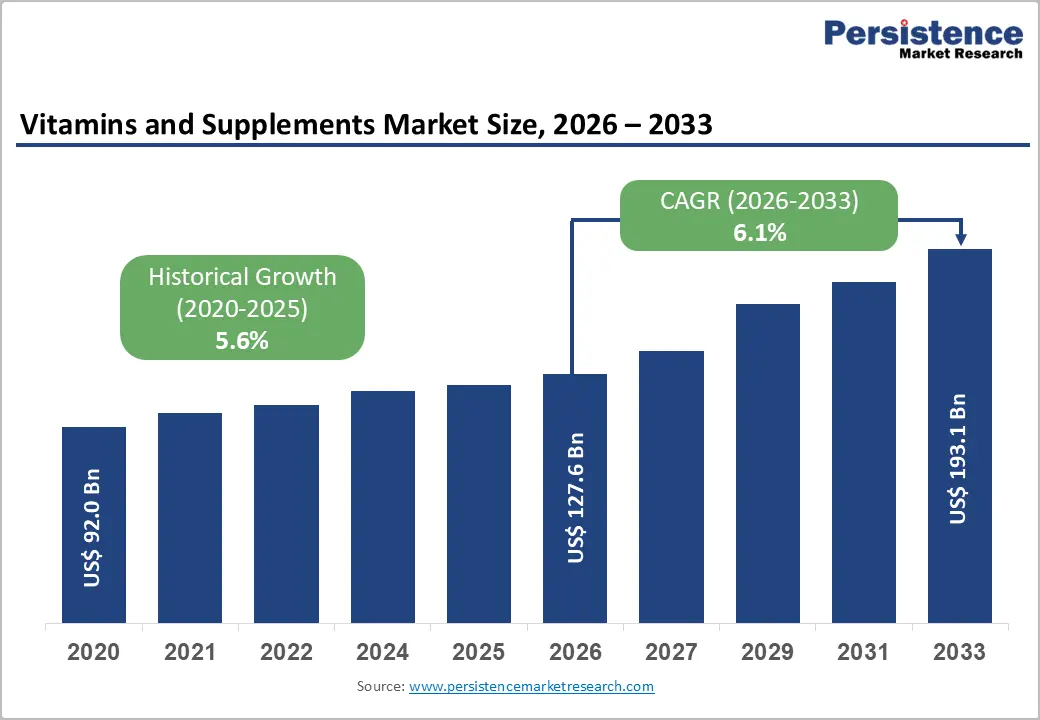

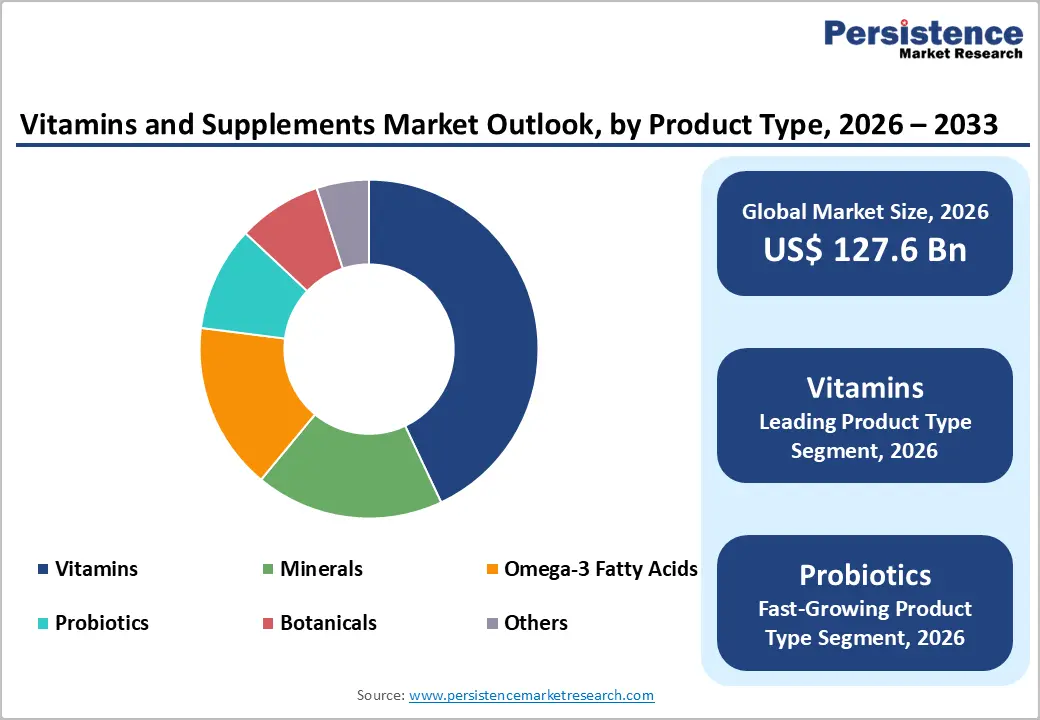

The global Vitamins and Supplements market size is expected to be valued at US$ 127.6 billion in 2026 and projected to reach US$ 193.1 billion by 2033, growing at a CAGR of 6.1% between 2026 and 2033

The market's upward trajectory is primarily anchored in the systemic transition of healthcare from reactive treatment to proactive prevention, as global populations increasingly integrate self-care into their daily routines. This evolution is further catalyzed by the escalating prevalence of lifestyle-related ailments such as obesity and metabolic syndrome and a demographic shift toward aging populations that require specialized nutritional support. Furthermore, the democratization of health information via digital platforms has empowered consumers to seek personalized solutions, ensuring sustained demand for diverse supplement categories across both developed and emerging economies.

Key Industry Highlights

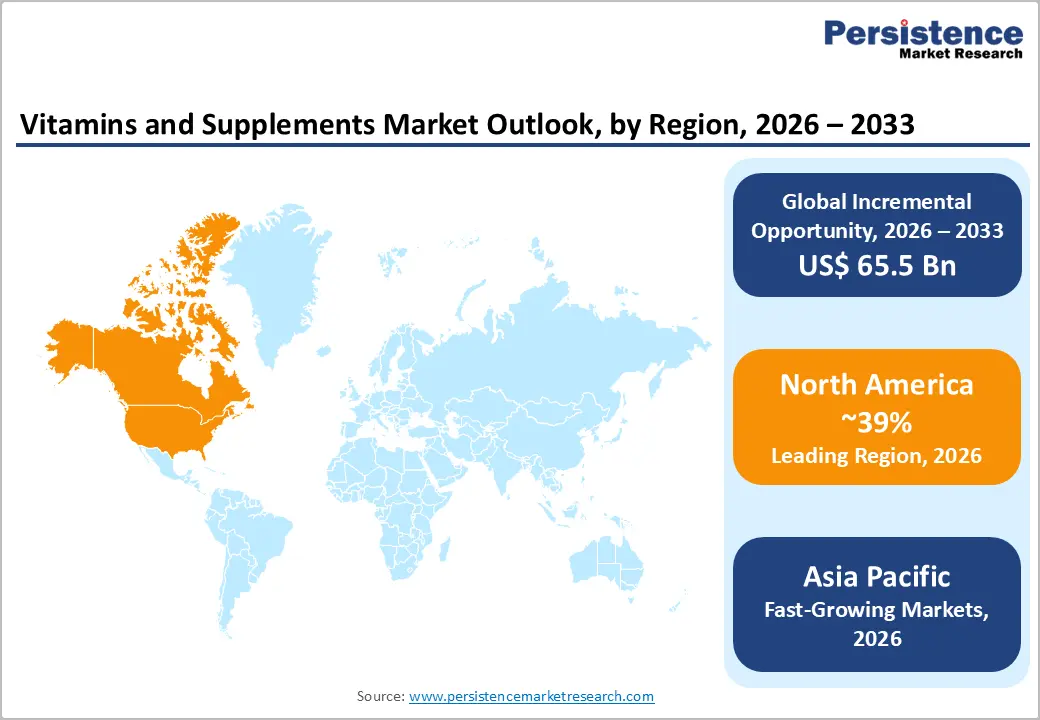

- Leading Region: North America continues to dominate the market with a 39% share in 2025, underpinned by a mature consumer base and a strong innovation ecosystem.

- Fastest Growing Region: Asia Pacific is set for the most rapid growth through 2033, driven by rising urban disposable incomes and high demand for preventive health in China and India.

- Dominant Segment: Vitamins remain the leading product category with a 43% share, reflecting their status as an essential daily nutrient staple globally.

- Fastest Growing Segment: Probiotics are expected to witness the highest CAGR, fueled by growing awareness of the gut microbiome's role in overall health and immunity.

- Key Market Opportunity: Personalized Nutrition driven by A.I. and genetic testing represents the most significant revenue pocket for future market participants.

- Key Development: In November 2025, Amway India launched Nutrilite Vitamin D Plus Boron; In March 2025, Innovaoleo by Natac introduced Omega 3 Star, a high-quality fish oil developed specifically for applications across the food, nutraceutical, and pet nutrition industries.

| Key Insights | Details |

|---|---|

| Vitamins and Supplements Market Size (2026E) | US$ 127.6 Bn |

| Market Value Forecast (2033F) | US$ 193.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.6% |

Market Dynamics

Driver – Rising Global Health Awareness and the Shift Toward Preventive Wellness

The fundamental catalyst propelling the Vitamins and Supplements market is the paradigm shift in consumer behavior toward preventive healthcare. As chronic lifestyle diseases become more prevalent, the World Health Organization (WHO) has emphasized that over 2 billion people globally suffer from micronutrient deficiencies. This realization has transitioned dietary supplements from occasional remedial use to a foundational component of daily wellness rituals. In the United States, the Council for Responsible Nutrition (CRN) indicates that a significant majority of adults now consume supplements daily to bolster immunity and bridge nutritional gaps. The Better-for-You movement, particularly among Millennials and Gen Z, has further intensified demand for products that offer functional benefits beyond basic nutrition, such as cognitive enhancement and stress management. This trend is bolstered by rising disposable incomes in developing nations, allowing consumers to invest in high-quality Vitamins and Minerals as a safeguard against long-term healthcare expenditures.

Restraints – Stringent Regulatory Frameworks and Compliance Complexities

A significant hurdle for the Vitamins and Supplements market is the increasingly fragmented and rigorous regulatory environment. In the United States, the Food and Drug Administration (FDA) recently intensified its oversight of products containing undeclared pharmaceutical ingredients, issuing multiple recalls in 2024 and 2025. Furthermore, a burgeoning patchwork of state-level age restrictions such as New York’s recent law restricting sales to minors has increased compliance costs for national retailers and Online Retail platforms. Internationally, the lack of harmonization between organizations like the European Food Safety Authority (EFSA) and the National Medical Products Administration (NMPA) in China poses substantial barriers for companies attempting to scale their portfolios across borders. These complexities often lengthen product launch timelines and escalate operational risks for emerging brands.

Opportunity – The Frontier of AI-Driven Personalization and Precision Nutrition

The integration of Artificial Intelligence (AI) and genetic testing presents a transformative opportunity for market participants to move beyond generic formulations. Personalized nutrition is no longer a niche concept; it is projected to grow at a CAGR of over 15% through 2033 as consumers demand solutions tailored to their specific DNA profiles and microbiome health. Companies like Novogenia are already combining genetic insights with tailor-made micronutrient plans to optimize individual wellness. The rise of at-home testing kits and digital health apps allows for real-time tracking of nutrient levels, creating a feedback loop that encourages continuous consumption. By leveraging A.I. to analyze vast datasets of lifestyle habits and biometric markers, brands can offer precision-engineered Probiotics and Botanicals that cater to unique metabolic needs, thereby fostering intense brand loyalty and premium pricing models.

Category-wise Analysis

By Product Type, vitamins dominates the global market

The Vitamins segment remains the undisputed leader in the Vitamins and Supplements market, commanding a dominant 43% market share in 2025. This leadership is attributed to the deep-rooted consumer awareness of essential micronutrients like Vitamin C, Vitamin D, and B-Complex, which are perceived as fundamental staples for immune support and energy metabolism. The segment's resilience is further bolstered by the widespread availability of multivitamins in both prescription and over-the-counter formats. However, Probiotics are identified as the fastest-growing segment for the 2025-2032 period. Driven by emerging research on the gut-brain axis and the role of the microbiome in systemic immunity, consumers are increasingly seeking out high-quality bacterial strains. In 2024, companies like Persephone Biosciences launched innovative synbiotics aimed at infant gut health, highlighting the segment's expansion into pediatric and specialized wellness niches.

By Sales Channel, online retail is expected to show promising growth in the global market

Pharmacies & Drugstores represent the leading sales channel, capturing over 36% of the market share in 2025. This dominance is fueled by consumer trust in professional medical guidance and the perceived authenticity of products found in regulated healthcare environments. Pharmacies often serve as the first point of contact for consumers seeking advice on nutrient deficiencies, providing a captive audience for both premium and generic supplement brands. On the other hand, Online Retail is the fastest-growing sales channel, expanding at an estimated CAGR of over 11%. The convenience of comparing prices, accessing peer reviews, and utilizing subscription services has shifted purchasing power away from physical storefronts. The rise of digitally native brands and the expansion of platforms like Amazon Health have further accelerated this trend, making supplements more accessible to rural and younger urban populations alike.

Region-wise Insights

North America Vitamins and Supplements Market Trends and Insights

North America remains the global frontrunner in the Vitamins and Supplements industry, accounting for a significant 39% market share in 2025. This leadership is primarily driven by the United States, where a highly developed innovation ecosystem and a robust regulatory framework under the Dietary Supplement Health and Education Act (DSHEA) have fostered a mature and competitive market. The region’s consumers are among the most proactive globally regarding health and wellness, with a strong emphasis on clean label and non-GMO products.

Recent trends in the U.S. highlight an explosion in the sports nutrition and energy segment, as fitness enthusiasts seek out amino acids and plant-based protein blends. Furthermore, the private-label market is witnessing significant growth, with major retailers like CVS and Walgreens launching their own lines of high-quality, affordably priced vitamins. The region also leads in technological integration, with North American companies pioneering the use of A.I. for personalized subscription boxes, thereby solidifying its position as the primary hub for market value and technological advancement.

Europe Vitamins and Supplements Market Trends and Insights

The Europe Vitamins and Supplements market is characterized by a strong emphasis on sustainability and a preference for botanical and natural ingredients. Western European countries, including Germany, the U.K., and France, lead the region due to high consumer awareness and a well-established healthcare infrastructure. In Germany, there is a particular demand for Organic and plant-based supplements, with the European Commission continuing to work on harmonizing regulations for health claims across member states to facilitate cross-border trade.

The U.K. remains a leader in the sports nutrition category, driven by a growing fitness culture and the rise of boutique wellness brands. Furthermore, the region’s aging population—with over 90 million citizens aged 65 and above is a major driver for bone and cardiovascular health supplements. European manufacturers are increasingly focusing on eco-friendly packaging and transparent supply chains, aligning with the Green Deal initiatives and meeting the demands of eco-conscious consumers who prioritize environmental responsibility alongside personal health.

Asia Pacific Vitamins and Supplements Market Trends and Insights

Asia Pacific is recognized as the fastest-growing region in the global Vitamins and Supplements market. This rapid expansion is fueled by the rising middle-class populations in China, India, and Japan, who are increasingly incorporating dietary supplements into their daily lives to combat urban lifestyle-related health issues. China currently accounts for over 50% of the regional share, supported by a long-standing tradition of herbal medicine and a modern push for preventive healthcare.

In India, the market is benefiting from increased disposable income and a surge in digitally native wellness brands. The Asia Pacific region also serves as a major manufacturing hub, with local companies increasingly adopting global quality standards to cater to international export markets. The high prevalence of mobile-first consumers has made the region a fertile ground for Online Retail and social commerce, particularly through platforms like Tmall and Flipkart. As health awareness spreads to Tier-2 and Tier-3 cities, the regional market is poised to become a dominant player in the global landscape by 2033.

Market Competitive Landscape

The global Vitamins and Supplements market is moderately fragmented, featuring a complex mix of pharmaceutical giants, diversified food companies, and specialized nutraceutical brands. Large-scale players like Amway, Herbalife Nutrition, and Nestlé Health Science maintain their dominance through extensive global distribution networks and massive R&D budgets that allow for continuous product innovation. A key strategy for these leaders is the acquisition of niche, high-growth brands to strengthen their portfolios in segments like personalized nutrition and probiotics.

In recent years, the market has seen a surge of Digitally Native Vertical Brands (DNVBs) that utilize D2C models to offer transparency and premium branding. Key differentiators in this competitive space include ingredient traceability, clinical validation of health claims, and the ability to offer diverse delivery formats like gummies and powders. Emerging business model trends are also seeing a shift toward holistic wellness platforms, where supplement sales are bundled with nutritional coaching and digital health monitoring.

Key Developments:

- In November 2025, Amway India launched Nutrilite Vitamin D Plus Boron, a scientifically formulated supplement designed to help maintain optimal vitamin D levels while supporting bone strength and immune health, reinforcing the brand’s focus on evidence-backed micronutrient solutions.

- In April 2025, research-driven innovation at North Carolina State University led to the development of CodonRX, a probiotic supplement designed to reduce gastrointestinal inflammation, demonstrating the growing role of academic spin-offs in advancing next-generation digestive health solutions.

- In March 2025, Innovaoleo by Natac introduced Omega 3 Star, a high-quality fish oil developed specifically for applications across the food, nutraceutical, and pet nutrition industries, addressing rising demand for multifunctional omega-3 ingredients with broad formulation flexibility.

Companies Covered in Vitamins and Supplements Market

- Amway

- Pfizer Inc.

- Abbott Laboratories

- Herbalife Nutrition

- Glanbia plc

- ADM

- DuPont de Numerous, Inc.

- Lonza Group

- Nature’s Sunshine Products

- Bayer AG

- Nestle S.A.

- Nutraceutical International Corporation

- Ostuka Holdings Co., Ltd.

- Rainbow Light

- Sanofi

- The Himalaya Drug Company

- USANA Health Sciences, Inc.

- Vitamin Shoppe

- Zhejiang NHU Co., Ltd.

Frequently Asked Questions

The global Vitamins and Supplements market is projected to be valued at US$ 127.6 Bn in 2026.

Key drivers include the global shift toward preventive healthcare, an aging population requiring specialized bone and cardiovascular support.

The Global Vitamins and Supplements market is poised to witness a CAGR of 6.1% between 2025 and 2032

North America is the leading region, accounting for 39% of the market share in 2025, primarily due to high consumer health consciousness and a robust retail infrastructure in the United States

Key players include global leaders such as Amway, Herbalife Nutrition, Nestlé Health Science, NOW Foods, Bayer AG, Pfizer Inc.