- Pharmaceuticals

- Antiviral Drugs Market

Antiviral Drugs Market Size, Share, and Growth Forecast 2026 - 2033

Antiviral Drugs Market by Product Type (DNA Polymerase Inhibitors, Reverse Transcriptase Inhibitors, Protease Inhibitors, Neuraminidase Inhibitors, Others), by Brand Type (Branded, Generics), by Application (HIV, Hepatitis, Herpes, Influenza, Others), by Distribution Channel, by Regional Analysis, 2026 - 2033

Antiviral Drugs Market Size and Trend Analysis

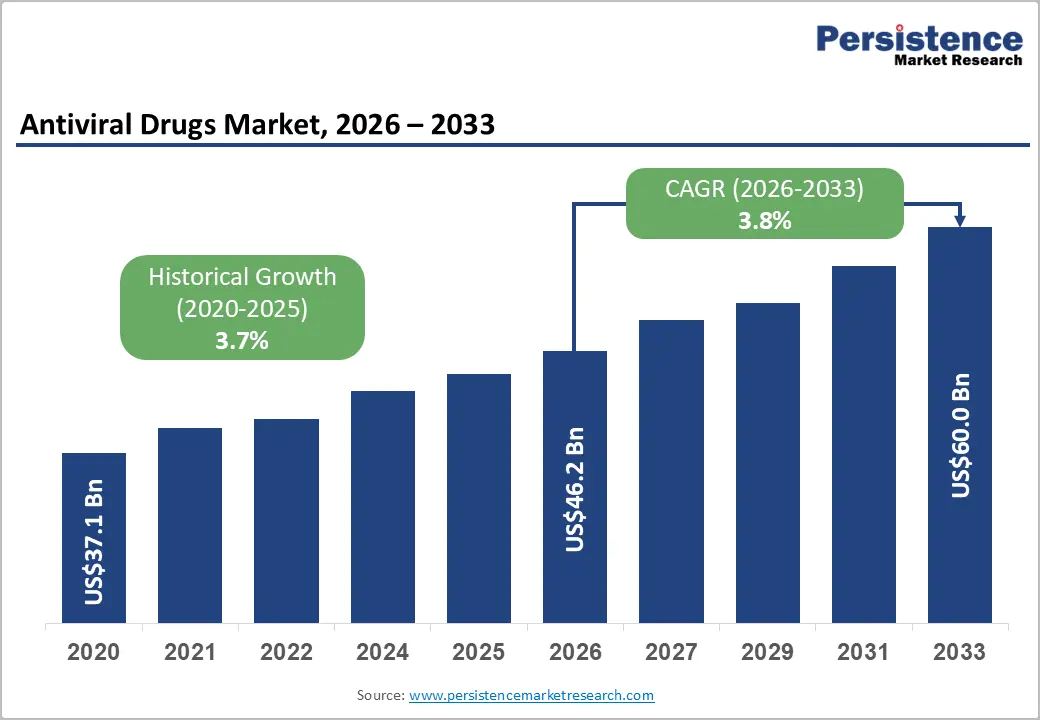

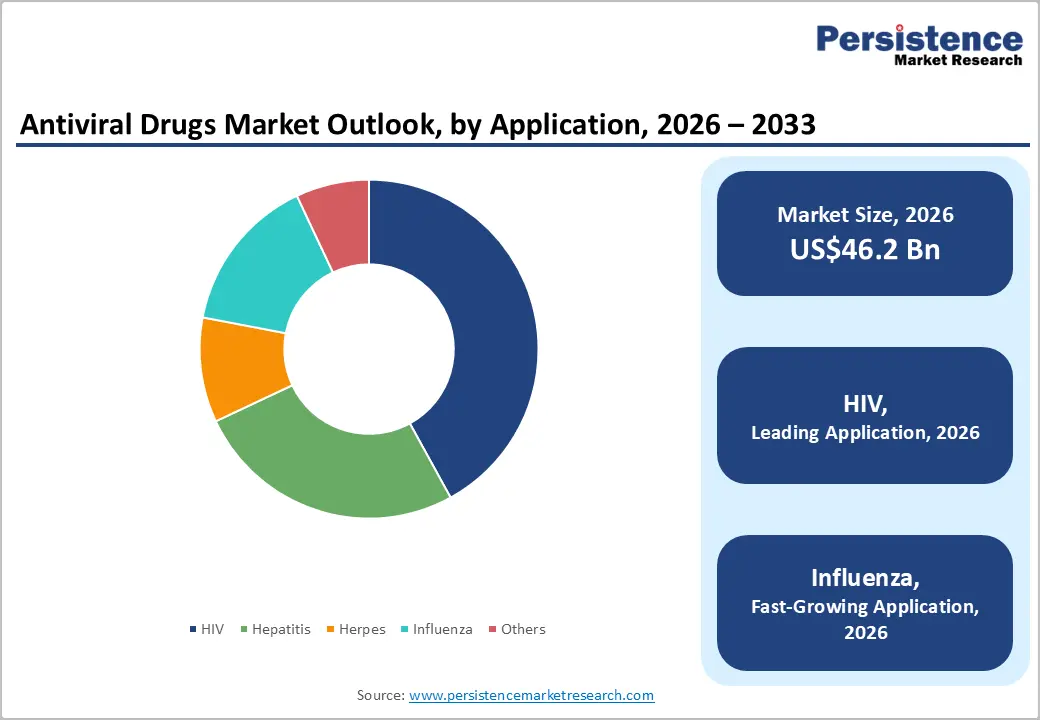

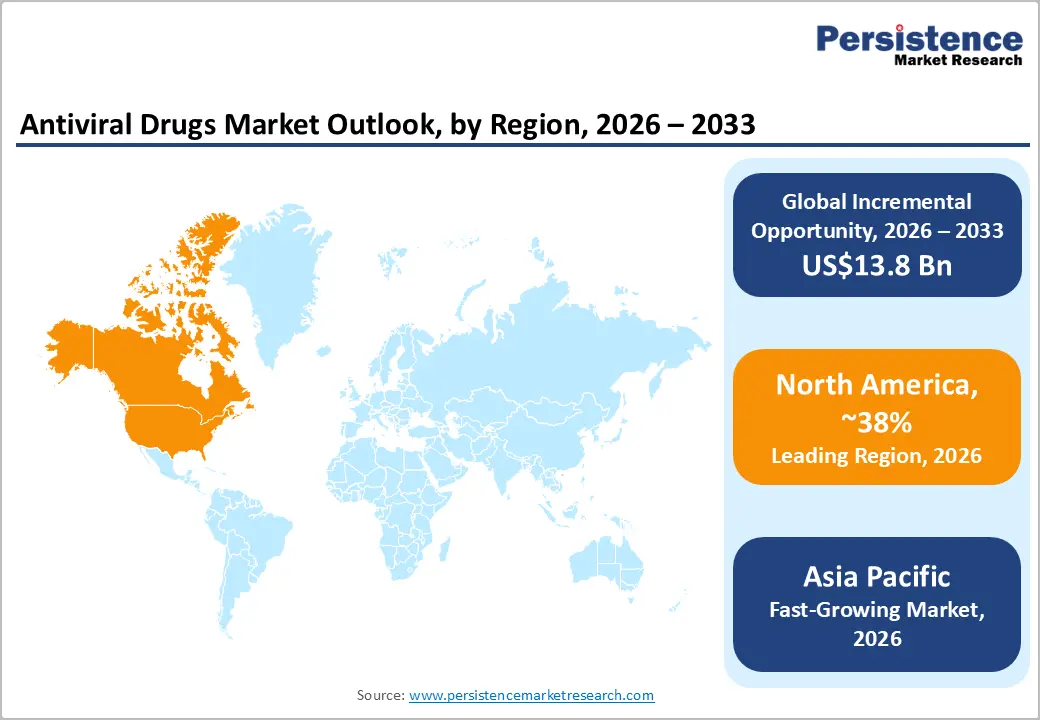

The global antiviral drugs market size is expected to be valued at US$ 46.2 billion in 2026 and projected to reach US$ 60.0 billion by 2033, growing at a CAGR of 3.8% between 2026 and 2033.

The global antiviral drugs market driven by the rising burden of viral infections, particularly HIV, hepatitis, and seasonal influenza. Expansion of HIV antiviral drug treatment programs under the WHO and UNAIDS, along with government-funded prevention and vaccination initiatives, is sustaining steady demand. Innovations in reverse transcriptase inhibitors, HIV drugs, and growth in the protease inhibitor drugs market segment are improving treatment outcomes. Faster approvals from the U.S. FDA and EMA, combined with increasing generic penetration in emerging economies, are further expanding access and supporting market growth.

Key Industry Highlights

- Leading Region: North America led the Antiviral Drugs market with a 38% share in 2025, supported by a large HIV treatment population, strong reimbursement systems, and the presence of major antiviral innovators including Gilead Sciences, AbbVie, and Merck & Co.

- Fastest Growing Region: Asia Pacific is projected to witness the fastest growth through 2033 due to rising hepatitis and HIV prevalence, expanding treatment access in China and India, and strong generic antiviral manufacturing capabilities across regional pharmaceutical companies.

- Dominating Segment: HIV remained the dominant application segment with 52% market share in 2025, driven by lifelong antiretroviral therapy requirements, increasing global ART coverage, and strong commercial performance of premium branded HIV therapies worldwide.

- Fastest Growing Segment: Influenza antivirals are expected to be the fastest-growing application segment through 2033, fueled by pandemic preparedness initiatives, expanding antiviral stockpiling programs, and increasing government investments in influenza outbreak management strategies globally.

- Key Opportunity: Gilead Sciences’ long-acting lenacapavir injectable HIV PrEP represents a major commercial opportunity, with strong Phase 3 efficacy results supporting next-generation HIV prevention approaches and expanding the long-acting antiviral therapeutics market globally.

Market Dynamics

Drivers - Expanding Global HIV Treatment Coverage Under UNAIDS 95-95-95 Targets

One of the most powerful structural drivers of the antiviral drugs market is the global scale-up of antiretroviral therapy (ART) for HIV, supported by the UNAIDS 95-95-95 targets which aim for 95% of people living with HIV to know their status, 95% of those diagnosed to receive ART, and 95% of those on treatment to achieve viral suppression by 2025. As of 2023, UNAIDS reported approximately 39.9 million people living with HIV globally, with approximately 29.8 million accessing ART representing a vast and growing treatment population generating sustained, recurring antiviral drug procurement.

Donor-funded treatment programs including PEPFAR (the U.S. President's Emergency Plan for AIDS Relief), which has disbursed over US$ 100 billion since its 2003 inception, institutionalize long-term antiviral procurement in sub-Saharan Africa and other high-burden regions, providing a structurally supported demand floor for both branded and generic HIV antivirals.

Restraints - Drug Resistance and High Development Cost Constraints

A key restraint impacting the antiviral drugs market is the rapid evolution of antiviral resistance and high R&D costs. Viruses such as HIV and influenza exhibit frequent mutations, reducing the long-term effectiveness of existing therapies, including reverse transcriptase inhibitors, HIV drugs, and neuraminidase inhibitors for influenza treatment. This requires continuous drug innovation cycles, significantly increasing development expenditure.

According to NIH and FDA regulatory frameworks, antiviral drug development can exceed US$1-2 billion per molecule due to long clinical validation periods. Additionally, strict compliance requirements from EMA and FDA slow approval timelines. Supply chain dependency on active pharmaceutical ingredients (APIs), largely concentrated in Asia, introduces additional risks of disruption. These structural challenges reduce profitability margins and limit the rapid scaling of next-generation antiviral therapies from 2026 to 2033.

Opportunities - Influenza Antiviral Market Expansion Driven by Pandemic Preparedness and Stockpiling Policies

Influenza antivirals represent the fastest-growing application segment within the Antiviral Drugs market over the 2026 - 2033 forecast period, driven by national pandemic preparedness stockpiling policies and the ongoing threat of novel influenza A strains with pandemic potential. The WHO Global Influenza Surveillance and Response System (GISRS) continuously monitors circulating strains and informs national stockpile recommendations for neuraminidase inhibitors including oseltamivir (Tamiflu) and baloxavir marboxil (Xofluza).

Following lessons from the COVID-19 pandemic, governments globally have accelerated strategic national antiviral stockpile investment. The U.S. Department of Health and Human Services (HHS) maintains the Strategic National Stockpile (SNS), which includes influenza antiviral reserves updated annually. Roche and Shionogi developers of Tamiflu and Xofluza respectively are primary commercial beneficiaries of this policy-driven demand, creating a resilient government procurement revenue stream that supplements commercial market sales.

Category-wise Insights

Product Type Analysis

DNA polymerase inhibitors dominate the antiviral drugs market with around 34% share in 2026, driven by strong use in herpesvirus and hepatitis treatment. These drugs are widely embedded in standard clinical guidelines across hospitals and outpatient care systems. Their consistent prescription base ensures stable demand across developed healthcare markets. Long-term hepatitis management programs further reinforce their leadership position.

Neuraminidase inhibitors are expected to grow at a 5.1% CAGR from 2026 to 2033, supported by the rising number of influenza cases globally. Governments are increasing antiviral stockpiling following seasonal outbreaks and the WHO flu alerts. Recent influenza surges in Asia and North America have strengthened hospital demand. BARDA-backed preparedness programs are also accelerating uptake.

Brand Type Analysis

Branded antiviral drugs hold about 61% share in 2026, supported by strong clinical efficacy and physician preference. Patent protection and established treatment protocols for HIV and hepatitis drive adoption. High-value therapies remain concentrated in developed healthcare systems. Companies such as GSK plc and AbbVie continue to dominate this segment.

Generics are growing at a 5.4% CAGR from 2026 to 2033, driven by affordability and patent expirations. Government procurement programs in emerging economies are accelerating adoption at scale. India’s pharmaceutical manufacturing base supports global supply expansion. HIV treatment programs in Africa are a key demand driver.

Application Analysis

HIV antiviral drug treatment leads with around 52% share in 2026, driven by lifelong therapy requirements. Combination antiretroviral therapy ensures continuous multi-drug usage across patient populations. Global programs such as the WHO and PEPFAR sustain treatment access across regions. This creates a stable and recurring demand base.

Influenza is expected to grow at a 4.6% CAGR from 2026 to 2033, due to rising seasonal outbreaks. Increased global surveillance and preparedness programs are boosting antiviral usage. Recent flu waves in Japan, the U.S., and Europe have increased hospital demand. Stockpiling initiatives are further strengthening growth momentum.

Regional Insights

North America Antiviral Drugs Market Trends and Insights

North America leads the global Antiviral Drugs market with a 38% share in 2025, driven predominantly by the United States home to a large HIV-positive population, high hepatitis C treatment uptake, comprehensive insurance reimbursement for branded antivirals, and the concentrated presence of leading innovator pharmaceutical companies. Strong FDA regulatory infrastructure supports rapid market authorization of next-generation antiviral therapies, sustaining the region's revenue leadership.

U.S. Antiviral Drugs Market Size

The U.S. accounts for approximately 88% of North American Antiviral Drugs revenues, estimated at roughly US$ 15.4 billion in 2026. The CDC reports approximately 1.2 million people living with HIV in the U.S., with 87% receiving ART. Medicaid and Medicare Part D coverage for branded antiretrovirals, combined with PEPFAR and ADAP program funding, sustains deep branded antiviral market penetration.

Canada Antiviral Drugs Market Size

Canada is expected to account for about 12% share of the regional market in 2026, supported by universal healthcare and coordinated infectious disease response systems. Post-pandemic reforms improved influenza surveillance and antiviral procurement efficiency during seasonal outbreaks. Government programs expanded access to neuraminidase inhibitors for influenza treatment and hepatitis therapies. Collaboration with U.S. research networks is further enhancing antiviral readiness and rapid response capabilities.

Europe Antiviral Drugs Market Trends and Insights

Europe is the second-largest Antiviral Drugs market, supported by universal public health reimbursement systems covering HIV and hepatitis C antivirals, national hepatitis C elimination programs, and a progressive biosimilar and generic policy environment under EMA regulatory oversight. Germany, France, and the UK collectively represent the majority of European antiviral revenues, with strong branded drug uptake in HIV management and accelerating generic penetration in hepatitis C.

Germany Antiviral Drugs Market Size

Germany holds approximately 21% of European Antiviral Drugs market revenues. The GKV statutory health insurance framework covers branded HIV and hepatitis C antivirals with minimal patient co-payment. Germany's large HIV-positive population of approximately 96,000 people on ART per the Robert Koch Institut (RKI), combined with national hepatitis C elimination initiatives, sustains high-value branded antiviral procurement.

UK Antiviral Drugs Market Size

The UK accounts for approximately 16% of European Antiviral Drugs revenues. NHS England commissions HIV antiretroviral therapy through specialist centres covering approximately 103,000 people on treatment per Public Health England (UKHSA) data. NICE technology appraisals govern branded antiviral reimbursement decisions, with recent approvals for long-acting injectable ART regimens expanding the premium therapy market.

France Antiviral Drugs Market Size

France represents approximately 13% of European Antiviral Drugs market revenues. The Agence Nationale de Recherches sur le SIDA (ANRS) and Haute Autorité de Santé (HAS) oversee antiviral treatment guidelines and reimbursement decisions. France's national hepatitis C elimination program targeting diagnosis and treatment of all identified HCV-infected individuals has driven significant growth in direct-acting antiviral procurement through hospital pharmacy channels.

Asia Pacific Antiviral Drugs Market Trends and Insights

Asia Pacific is the fastest-growing regional Antiviral Drugs market over 2026 - 2033, driven by the world's largest viral hepatitis burden, expanding HIV treatment coverage, and a dominant generic manufacturing base in India and China supplying both domestic and international markets. China is the largest country market in the region, with the National Health Commission reporting over 1.1 million people living with HIV receiving ART domestically and a major hepatitis B and C treatment scale-up underway through national health insurance expansion.

China Antiviral Drugs Market Size

China is set to contribute nearly 32% of the Asia Pacific market share in 2026, supported by large-scale pharmaceutical manufacturing and expanding biotech innovation. Post-COVID reforms strengthened infectious disease monitoring systems and antiviral stockpiling capacity. Government initiatives improved preparedness for influenza and emerging viral outbreaks. Increased participation in global clinical trials is enhancing long-term antiviral innovation strength.

India Antiviral Drugs Market Size

India contributes approximately 14% of Asia Pacific Antiviral Drugs revenues and serves as the world's largest producer of generic antivirals. The National AIDS Control Organisation (NACO) provides free first-line ART to over 1.4 million patients. Cipla, Aurobindo, and Sun Pharma are global leaders in WHO-prequalified generic HIV and hepatitis C antiviral supply, generating significant export revenues in addition to large domestic volumes.

Competitive Landscape

The global Antiviral Drugs market exhibits a moderately consolidated structure at the branded innovator level, with Gilead Sciences, AbbVie, Merck & Co., Johnson & Johnson (Janssen/ViiV Healthcare), and Roche collectively dominating HIV, hepatitis C, and herpesvirus antiviral revenues. Key differentiators include long-acting formulation development, pipeline depth in resistant-virus indications, and access program partnerships with PEPFAR and Global Fund. The generic segment is highly competitive, led by Cipla, Aurobindo Pharma, and Teva Pharmaceutical, which compete primarily on price and regulatory breadth.

Strategic priorities include long-acting injectable ART development, mRNA-based antiviral innovation (led by Moderna), and portfolio expansion into emerging viral targets including respiratory syncytial virus (RSV).

Key Developments

- In January 2026, GSK acquired Rapt Therapeutics for approximately US$2.2 billion to strengthen its immunology and inflammation pipeline, securing global rights to ozureprubart, a long-acting anti-IgE monoclonal antibody. This deal enhances GSK’s positioning in immune-driven antiviral and inflammatory disease pathways, supporting expansion into next-generation antiviral-related therapies.

- In November 2025, Merck acquired Cidara Therapeutics for approximately US$9.2 billion to reinforce its influenza antiviral portfolio, gaining access to CD388, a long-acting flu prevention therapy. This acquisition strengthens Merck’s infectious disease pipeline and helps diversify its portfolio amid rising patent pressure on Keytruda.

- In July 2025: Gilead Sciences announced positive Phase 3 results for lenacapavir as twice-yearly injectable HIV pre-exposure prophylaxis (PrEP), with PURPOSE 1 and PURPOSE 2 trials demonstrating 100% and 96% efficacy respectively, positioning the product for potential FDA approval in 2025.

Antiviral Drugs Market - Key Insights

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 37.6 billion |

| Current Market Value (2026) | US$ 46.2 billion |

| Projected Market Value (2033) | US$ 60.0 billion |

| CAGR (2026 - 2033) | 3.8% |

| Leading Region | North America, 38% market share |

| Dominant Product Type | Reverse Transcriptase Inhibitors, 38% market share |

| Top-ranking Application | HIV, 52% market share |

| Incremental Opportunity | US$ 13.8 billion |

Companies Covered in Antiviral Drugs Market

- Gilead Sciences

- Pfizer

- AbbVie

- Merck & Co.

- Roche

- GSK plc

- Johnson & Johnson

- Bristol Myers Squibb

- Novartis

- Aurobindo Pharma

- Cipla

- Teva Pharmaceutical Industries

- Moderna

- Boehringer Ingelheim

- Others

Frequently Asked Questions

The global market is estimated at US$ 46.2 billion in 2026, supported by expanding HIV and hepatitis treatment populations, premium antiviral therapies, and increasing pandemic preparedness initiatives globally.

Key demand drivers include rising HIV treatment adoption under UNAIDS targets, increasing hepatitis C elimination programs, growing antiviral procurement, and strong government funding supporting global infectious disease management initiatives.

North America leads the market with a 38% share, driven by high HIV treatment penetration, strong reimbursement systems, advanced healthcare infrastructure, and major antiviral drug manufacturers.

Long-acting HIV therapies and expanding generic antiviral access across Asia Pacific and Africa represent major growth opportunities, supported by global healthcare programs, licensing agreements, and increasing infectious disease treatment coverage.

Leading companies include Gilead Sciences, AbbVie, Merck & Co., Johnson & Johnson/ViiV Healthcare, Roche, Shionogi, Cipla, Aurobindo Pharma, Teva Pharmaceutical Industries, and Sun Pharmaceutical Industries.