- Biotechnology

- Lentiviral Vectors Market

Lentiviral Vectors Market Size, Share, and Growth Forecast, 2026 - 2033

Lentiviral Vectors Market By Product (Third-Generation SIN Vectors, First-Generation Vectors, Others), Component (Upstream Vector Production, Downstream Purification, Others), Application, End-user, and Regional Analysis for 2026 - 2033

Lentiviral Vectors Market Size and Trends Analysis

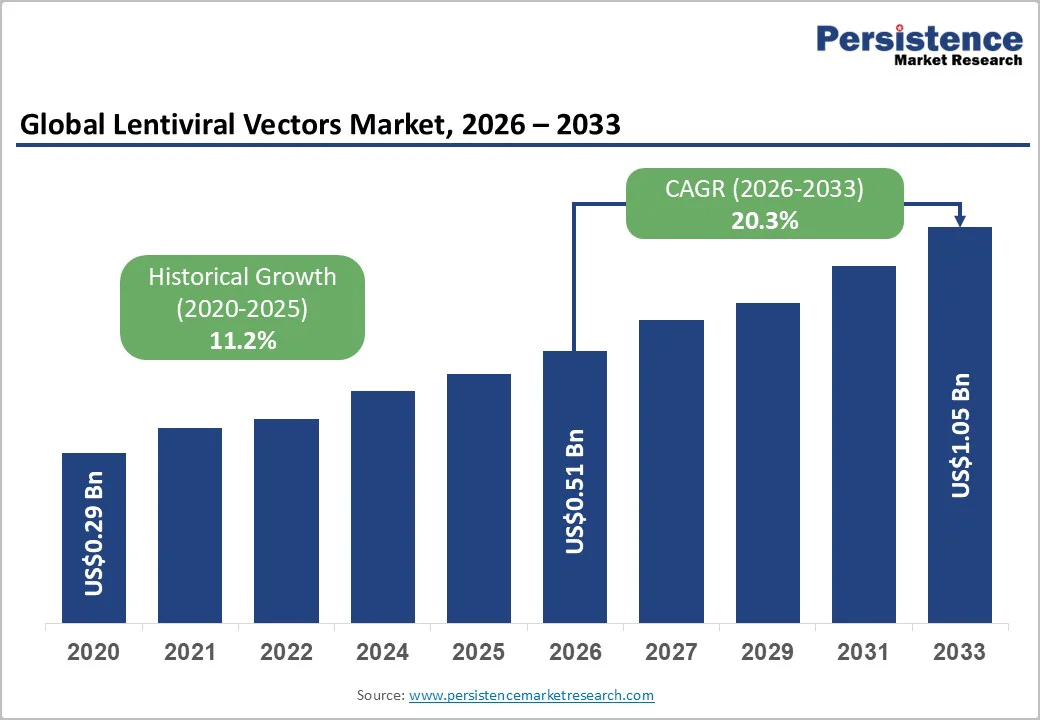

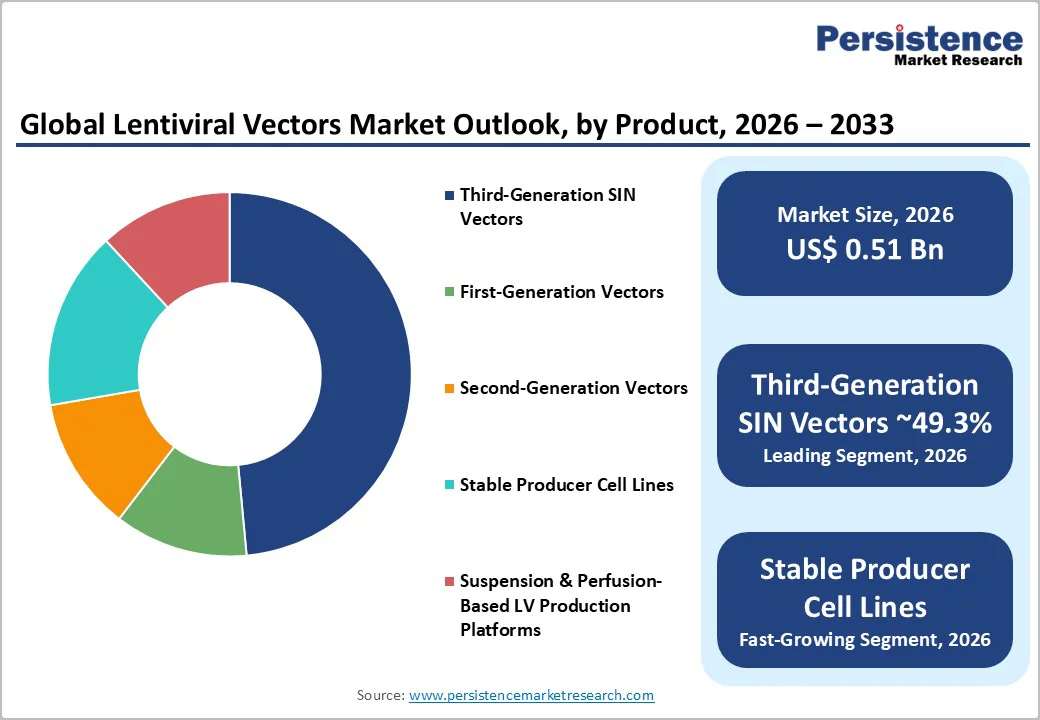

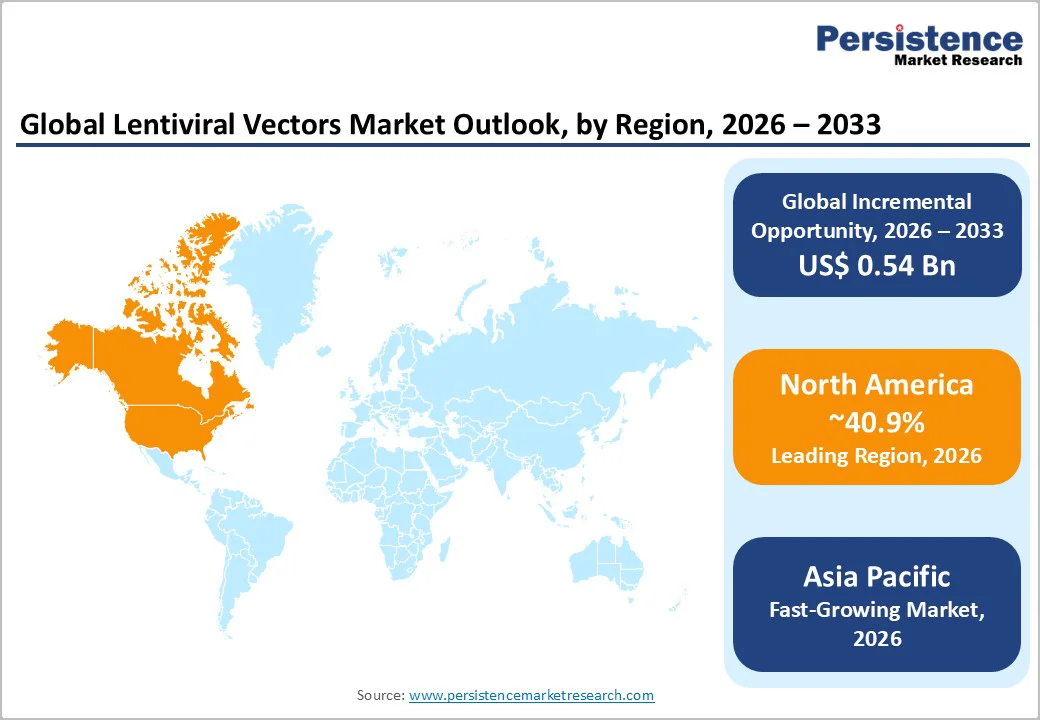

The global lentiviral vectors market size is likely to be valued at US$0.51 Billion in 2026 and is expected to reach US$1.05 Billion by 2033, growing at a CAGR of 20.3% during the forecast period from 2026 to 2033, driven by expanding clinical adoption of gene-modified cell therapies, rising R&D investments in ex vivo gene-transfer platforms, and increasing application in rare disease therapeutics. Demand is reinforced by ongoing advancements in manufacturing efficiency, safety optimization, and regulatory standardization across major therapeutic markets.

Key Industry Highlights

- Leading Region: North America remains the largest market, accounting for over 40.9% of global revenue, supported by a strong U.S. CAR-T therapy pipeline, deep CDMO presence, and advanced regulatory infrastructure.

- Fastest-growing Region: Asia Pacific is projected to be the fastest-expanding market, driven by China’s CGT manufacturing scale-up, Japan’s regulatory incentives, and India’s emerging biomanufacturing ecosystem.

- Investment Plans: Post-2023, capacity-building investments increased significantly, with over 25% of active CDMOs announcing expansions in plasmid supply, suspension-based LV production suites, or GMP facilities. Examples include EU footprint expansion, U.S. Greenfield builds, and large platform commercialization efforts.

- Dominant Product: Third-generation SIN lentiviral vectors hold the largest share, representing nearly 49.3% of clinical and commercial demand due to improved safety, scalability, and regulatory acceptance.

- Leading Application: Ex vivo cell therapies, especially CAR-T and T-cell engineering programs, account for over 54.6% of total lentiviral vector usage owing to their reliance on high-titer, GMP-grade LV batches.

| Key Insights | Details |

|---|---|

|

Lentiviral Vectors Market Size (2026E) |

US$0.51 Bn |

|

Market Value Forecast (2033F) |

US$1.05 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

20.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

11.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rapid Expansion of Gene-Modified Cell Therapies

The demand for lentiviral vectors continues to grow as gene and cell therapies progress from early-stage research to commercial deployment. Regulatory approvals for T-cell–based therapies and pipeline expansion across oncology, rare genetic disorders, and regenerative medicine significantly increase vector consumption. Manufacturing workflows now employ higher-yield platforms and improved purification steps, enabling scalable production. As clinical trials broaden across multiple indications globally, lentiviral vectors remain essential due to their stable gene integration and ability to transduce dividing and non-dividing cells, resulting in sustained expression. This creates a durable and recurring demand cycle, especially across large commercial production programs.

Advancements in Vector Engineering and Process Optimization

Process innovations such as suspension-based production systems, serum-free media, and stable producer cell lines improve yield reproducibility and batch-to-batch consistency. Refined safety elements, including self-inactivating (SIN) designs and reduction of replication-competent lentivirus (RCL) formation risks, strengthen regulatory confidence. Standardized analytical assays and automation solutions lower operational variability and reduce production bottlenecks. Manufacturing optimization supports both clinical-grade and commercial-scale requirements, making lentiviral vector platforms more accessible to therapy developers and contract manufacturers. These improvements collectively raise throughput and lower cost per dose, reinforcing market uptake.

Increased Global Investment in Advanced Therapies Infrastructure

Government-supported innovation hubs, national gene-therapy programs, and targeted funding initiatives continue to expand GMP-grade vector manufacturing capacity. Collaborative public–private models accelerate technology transfer and enhance regional production capabilities, enabling more companies to meet stringent regulatory requirements. Infrastructure expansion supports localized supply to reduce international logistics challenges and strengthen supply-chain resilience. Rising investment in workforce training and specialized manufacturing sites improves readiness for commercial-scale production, making lentiviral vectors a central component of future therapeutic pipelines.

Barrier Analysis - High Production Costs and Complex Manufacturing Requirements

Lentiviral vector production involves multi-step upstream and downstream processes requiring highly controlled environments, specialized analytical assays, and skilled scientific teams. Contamination risks and stringent quality-control standards increase operational challenges. Many manufacturers face high capital expenditure for facility setup, and small or emerging therapy developers often rely on external CDMOs, which can significantly increase per-batch costs. These structural cost barriers may limit the adoption of lentiviral-based therapies in price-sensitive markets.

Regulatory Variability and Capacity Limitations

Although regulatory agencies have established clearer frameworks for advanced therapies, variability in requirements across regions complicates development timelines and increases compliance burden. Inconsistent expectations on testing, documentation, and release specifications can delay production. Limited global GMP-grade manufacturing capacity also creates long wait times for production slots, affecting therapy developers with aggressive commercialization plans. These constraints slow market progression, particularly for small and mid-sized developers.

Opportunity Analysis - Expansion of Rare Disease and Pediatric Therapy Pipelines

An increasing number of lentiviral-based therapeutic candidates target inherited metabolic disorders, blood disorders, and immune deficiencies. Many of these conditions lack effective treatments, creating a strong demand for long-term gene-correction platforms. The opportunity exists for therapy developers to capture value in indications with relatively small patient populations but substantial unmet needs. As newborn screening programs grow globally, earlier diagnosis will increase the eligible patient pool for gene-modifying technologies, supporting market expansion.

Growth of CDMO Partnerships and Flexible Manufacturing Models

The rise of modular production facilities, closed-system manufacturing, and single-use bioprocessing technologies creates opportunities for scalable outsourcing. Contract manufacturers that invest in automated vector platforms and integrated production suites will benefit from increased demand for customized lentiviral vector batches. End-to-end service offerings that combine development, optimization, analytics, and GMP production provide therapy developers with faster turnaround times and reduced capital burden.

Integration of AI-Assisted Process Development and Quality Analytics

Digital manufacturing tools and advanced analytics are enabling real-time monitoring and predictive quality control. AI-assisted optimization of vector design, viral titers, and impurity profiles enhances process robustness and accelerates development timelines. As regulatory frameworks begin to recognize data-driven validation approaches, these technologies may become central to reducing failure rates, improving reproducibility, and enhancing regulatory confidence. Adoption of AI-enabled systems presents a significant opportunity for differentiation and operational efficiency.

Category-wise Analysis

Product Insights

Third-generation self-inactivating (SIN) lentiviral vectors hold the largest share of 49.3% due to clinical programs preferring them for their established safety profile and regulatory familiarity. These vectors employ split-packaging architectures and remove accessory genes that historically raised biosafety concerns, making them suitable for both early-stage and late-stage trials. Their dominance is reinforced by the fact that most commercial CAR-T therapies have been developed using SIN-based systems, which provide stable gene delivery and long-term expression without replication capability. GMP manufacturers prioritize these platforms because production processes, quality expectations, and release testing workflows are well understood, which reduces variability and accelerates study progression. Sponsors also benefit from mature analytical frameworks and predictable regulatory review pathways, elevating SIN vectors as the de facto baseline for clinical-grade manufacturing.

The fastest-expanding segment is driven by stable producer cell lines and next-generation packaging systems that deliver higher titres, improved scalability, and consistent commercial-scale vector production. While transient transfection is useful in early research, it becomes costly and complex at scale. Stable lines reduce COGS, enhance reproducibility, and improve regulatory alignment for late-phase programs. As more therapies advance toward commercialization, demand accelerates for industrial-scale manufacturing. CDMOs are investing heavily in suspension-based stable systems with optimized promoters and modular bioreactors, making this the highest-growth vector-generation technology segment.

Application Insights

Ex vivo cell therapy is the leading application segment for lentiviral vectors, holding a market share of 54.6%. Autologous CAR-T therapies rely heavily on lentiviral transduction because the vector enables stable integration, long-term expression, and predictable gene modification outcomes. The significant number of approved CAR-T therapies and the large pipeline of new programs create sustained demand for clinical-grade lentiviral vector supply. Manufacturing workflows for these therapies are well-established, and developers prefer lentiviral vectors due to consistent performance in T-cell engineering. As more hematologic and solid-tumor CAR-T programs enter trials, the volume of required vector batches continues to climb, reinforcing ex vivo cell therapy as the dominant user segment in the market.

The fastest-growing segment involves emerging in-vivo gene therapy applications that utilize lentiviral delivery approaches. Although historically overshadowed by AAV systems for systemic delivery, lentiviral vectors are gaining ground in localized or compartmentalized applications such as ocular, neurologic, and hepatic indications. Improvements in vector tropism, delivery methods, and safety engineering are expanding their suitability for in vivo use. Developers are increasingly exploring lentiviral options for indications where stable long-term gene expression is essential and where integration provides therapeutic durability. As early-phase clinical programs advance, demand for specialized manufacturing, high-precision analytics, and targeted delivery technologies is increasing.

Regional Insights

North America Lentiviral Vectors Market Trends - Leading Engine for Clinical-Scale Lentiviral Manufacturing

North America is the largest regional market, accounting for over 40.9% of market share, driven by a high concentration of cell and gene therapy developers, a strong ecosystem of clinical trial activity, and sizable investments in manufacturing infrastructure. The U.S. contributes the majority of regional revenue and GMP vector demand. Many commercial-stage cell therapies originate in the U.S., and this clinical density directly translates into substantial consumption of lentiviral drug substance. The region also benefits from well-established biotechnology clusters that integrate research, manufacturing, analytics, and regulatory expertise in proximity.

The U.S. supports the highest number of CAR-T and gene therapy trials globally, creating recurring demand for early-stage, late-stage, and commercial-scale vector production. Regulatory clarity further reinforces market leadership. Agencies provide detailed guidance for CMC requirements, vector characterization, potency assays, and replication-competent virus testing. This predictable regulatory environment reduces development risk and encourages sponsors to progress programs toward licensure, which in turn increases manufacturing needs.

Europe Lentiviral Vectors Market Trends - Established Ecosystem Advancing Next-Generation Vector Development

Europe represents the second-largest regional market for lentiviral vectors, supported by a robust academic research base, strong translational infrastructure, and established manufacturing capabilities. Countries such as the United Kingdom, Germany, France, and Spain serve as focal points for next-generation cell and gene therapy development. The region benefits from long-standing research traditions in vector engineering and clinical innovation, enabling a steady pipeline of early-stage and mid-stage programs.

The U.K. hosts some of the most sophisticated lentiviral manufacturing operations, with companies that have decades of experience in GMP vector production. Germany contributes through its strong biotechnology clusters, advanced analytical capabilities, and consistent investment in biomanufacturing. France and Spain have expanded their activity in recent years through facility upgrades, new CDMO entrants, and increased public investment in cell and gene therapy infrastructure.

Europe’s regulatory landscape strengthens growth by providing harmonized EMA frameworks for ATMP manufacturing and evaluation. Although stringent, consistent rules streamline multi-country clinical development. Expansion is driven by strong academic-industry collaborations, rising CAR-T and gene-modified therapy trials, and targeted funding initiatives that enhance regional infrastructure and manufacturing capacity.

Asia Pacific Lentiviral Vectors Market Trends - Rapidly Expanding Hub for Viral Vector Production

Asia Pacific is the fastest-growing market for lentiviral vectors, supported by expanding biotechnology ecosystems, rising clinical activity, and strong government backing for advanced therapies. China, Japan, India, and ASEAN countries are investing heavily in biomanufacturing, accelerating the region’s role in global vector supply. China leads this expansion, with major CDMOs building large viral vector and plasmid facilities and a more supportive regulatory environment enabling advanced therapy approvals and late-stage trials. Its large patient base and increasing oncology burden make it a key clinical market for CAR-T and gene-modified therapies, driving demand for clinical-grade lentiviral vectors.

Japan maintains a strong research-oriented ecosystem, supported by regulatory frameworks for regenerative medicine that accelerate early adoption. This fosters collaboration between academic institutions, hospitals, and manufacturers. Japan’s focus on precision medicine and cell therapy innovation contributes meaningfully to regional demand. India and ASEAN countries are emerging as manufacturing and clinical trial hubs due to cost advantages, skilled talent pools, and expanding GMP capabilities. Multinational companies are increasingly establishing regional collaborations or capacity-sharing agreements with local CDMOs.

Competitive Landscape

The global lentiviral vectors market is shaped by a mix of global CDMOs, major life science suppliers offering reagent and platform technologies, and smaller in-house manufacturing units at therapeutic developers. Market concentration is moderate: a limited number of large CDMOs with global GMP facilities serve late-stage and commercial programs, while many regional or specialist providers focus on early development and niche applications. This creates a two-tier landscape in which large platform-based manufacturers dominate high-value programs, and smaller firms differentiate by offering flexibility, rapid turnaround, and customized technical support.

Key strategies include platform-based manufacturing using stable producer cell lines, expansion of integrated supply chains covering plasmids through fill-finish, and capacity scaling through acquisitions or new facilities. Market leaders emphasize regulatory credibility, manufacturing consistency, and global GMP networks, while emerging players compete through process flexibility, rapid project onboarding, and specialized technical expertise.

Key Industry Development

- In May 2025, Wacker Biotech entered a strategic partnership with Expression Manufacturing to deliver end-to-end lentiviral vector development and production, combining optimized plasmid DNA manufacturing and vector production under a unified supply-chain framework.

- In June 2024, Charles River Laboratories announced a collaboration with the Gates Institute at the University of Colorado Anschutz Medical Campus to provide GMP-grade lentiviral vector manufacturing for novel CAR-T therapies targeting hematological cancers.

Companies Covered in Lentiviral Vectors Market

- Thermo Fisher Scientific

- Oxford Biomedica

- Merck KGaA (MilliporeSigma)

- Charles River Laboratories

- Lonza Group

- VGXI

- WuXi AppTec

- WuXi Biologics

- Catalent Biologics

- VectorBuilder

- FinVector

- Sirion Biotech

- Cobra Biologics

- Takara Bio

- Sartorius

- Cytiva

- Brammer Bio

- BlueBird Bio (Vector Core)

- OriGene Technologies

- Sino Biological

Frequently Asked Questions

The global lentiviral vectors market size in 2026 is estimated at US$0.51 Billion.

By 2033, the market value is projected to reach US$1.05 Billion.

Key trends include rapid adoption of third-generation SIN lentiviral vectors in clinical programs and transition toward suspension-based and scalable platforms supporting commercial cell therapy volumes.

The leading segment is third-generation SIN lentiviral vectors, accounting for the largest share due to improved safety, regulatory acceptance, and compatibility with both ex vivo and in vivo therapeutic development.

The lentiviral vectors market is expected to grow at a CAGR of 20.3% between 2026 and 2033.

Major companies with strong portfolios include Thermo Fisher Scientific, Oxford Biomedica, Merck KGaA (MilliporeSigma), Charles River Laboratories, and Lonza Group.