- Automotive Components & Materials

- Tyre Inner Tubes Market

Tyre Inner Tubes Market Size, Share, and Growth Forecast, 2025 - 2032

Tyre Inner Tubes Market by Product Type (Butyl Rubber Inner Tubes, Natural Rubber Inner Tubes, Others), Vehicle Type (Passenger Cars, Commercial Vehicles, Two-Wheelers, Bicycles, Others), Distribution Channel (OEMs, Aftermarket), and Regional Analysis for 2025 - 2032

Tyre Inner Tubes Market Size and Trend Analysis

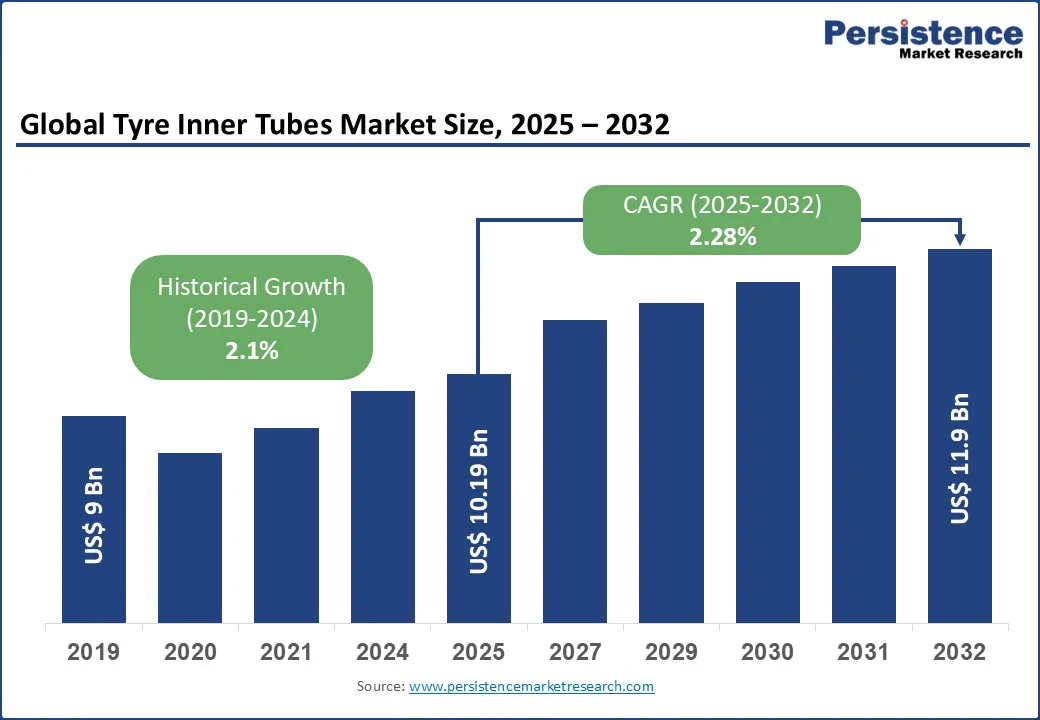

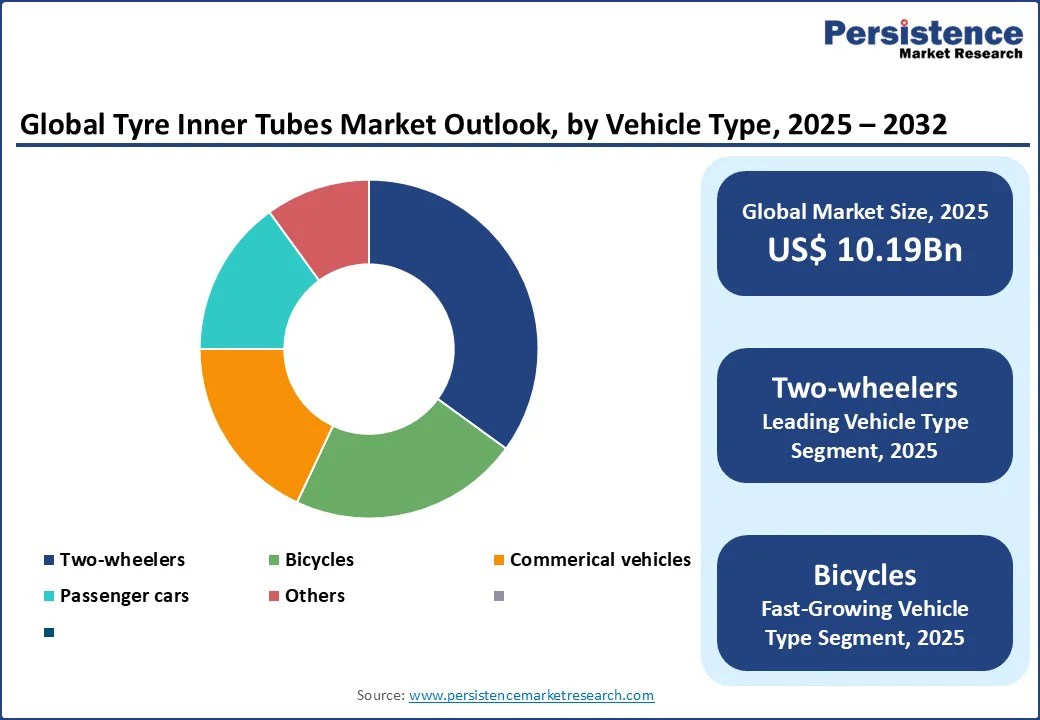

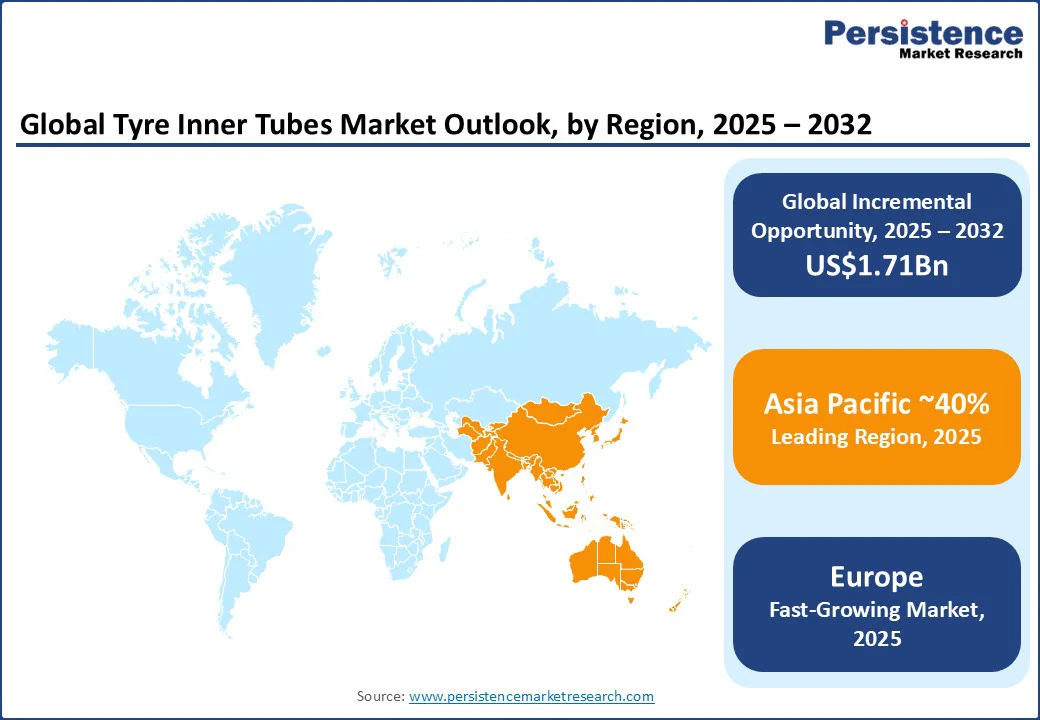

The global tyre inner tubes market size is likely to be value at US$10.19 Bn in 2025 and reach US$11.9 Bn by 2032, growing at a CAGR of 2.3% during the forecast period from 2025 to 2032.

Key Industry Highlights

- Leading Region: Asia Pacific is likely to hold a leading share in 2025, driven by robust automotive production and bicycle usage in countries such as China and India.

- Fastest-Growing Region: Europe is the fastest-growing region, propelled by the rising adoption of electric vehicles and stringent safety regulations.

- Dominant Product Type: Butyl rubber inner tubes account for nearly 60% of the tyre inner tubes market share, due to their superior air retention and durability.

- Leading Application: Two-wheelers contribute over 35% of market revenue, driven by high motorcycle and bicycle usage in emerging markets.

- Investment Plans: India’s Production Linked Incentive (PLI) scheme, announced in 2021, aims to boost domestic tyre manufacturing, increasing demand for inner tubes by 2030. This momentum helped attract INR 3,000 crore in investments from global tyre giants to ramp up local manufacturing.

| Global Market Attribute | Key Insights |

|---|---|

| Tyre Inner Tubes Market Size (2025E) | US$ 10.19Bn |

| Market Value Forecast (2032F) | US$ 11.9Bn |

| Projected Growth (CAGR 2025 to 2032) | 2.28% |

| Historical Market Growth (CAGR 2019 to 2024) | 2.1% |

The tyre inner tubes market is witnessing stable growth, fueled by increasing vehicle production, particularly in emerging economies, and the rising popularity of bicycles and two-wheelers.

Market Dynamics

Driver: Rising Vehicle Production and Bicycle Usage Fuel Market Expansion

The global tyre inner tubes market is experiencing steady growth due to the surge in vehicle production and the increasing popularity of bicycles worldwide. According to the International Organization of Motor Vehicle Manufacturers (OICA), global vehicle production reached 93.55 million units in 2023, with emerging economies such as China and India contributing significantly. Tyre inner tubes are essential for maintaining air pressure in vehicles such as motorcycles, passenger cars, and commercial vehicles, ensuring safety and efficiency.

The growing adoption of bicycles, driven by urbanization and environmental consciousness, further boosts demand. Companies such as Michelin and Continental are capitalizing on this trend by offering durable inner tubes for both automotive and bicycle applications. Government initiatives, such as India’s Smart Cities Mission, promote sustainable transport, ensuring sustained demand for tyre inner tubes through 2032.

Restraint: Shift Toward Tubeless Tyres and Raw Material Price Volatility

The global tyre inner tubes market is undergoing a period of transformation, facing several structural and market-driven challenges that are impeding its growth trajectory. These challenges are both technological and economic in nature, affecting manufacturers, suppliers, and downstream industries alike. Tubeless tyres, which eliminate the need for inner tubes, are gaining traction due to their puncture resistance and fuel efficiency.

Additionally, raw materials such as natural and butyl rubber are subject to price volatility due to supply chain disruptions and geopolitical factors. The cost fluctuations put tremendous pricing pressure on manufacturers, especially small and medium-sized enterprises (SMEs) that lack the scale or financial buffer to absorb sudden cost hikes.

This results in margin compression, reduced profitability, and in some cases, market exit. The lack of standardization in some regions and concerns over inner tube durability in extreme conditions further restrain market growth.

Opportunity: Growing Demand in Electric Vehicles and Sustainable Transport

The rise of electric vehicles (EVs) and sustainable transportation presents significant opportunities for the tyre inner tubes market. EVs, particularly two-wheelers and bicycles, require specialized inner tubes to support their unique performance needs. The International Energy Agency (IEA) projects global EV sales to reach 40 million units annually by 2030 under the Stated Policies Scenario (STEPS), driving demand for high-quality inner tubes.

Additionally, the global push for sustainable transport, such as cycling, is increasing inner tube usage. Companies such as Schwalbe and Kenda are innovating with eco-friendly materials, such as recyclable butyl rubber, to align with sustainability trends.

Government incentives, such as the EU’s Green Deal and India’s FAME II scheme, encourage investments in green mobility, creating opportunities for manufacturers to develop advanced inner tubes tailored for EVs and bicycles, positioning the tyre inner tubes market for growth through 2032.

Category-wise Insights

By Product Type

- Butyl rubber inner tubes dominate the tyre inner tubes market, accounting for a leading market share in 2025. Their superior air retention, durability, and resistance to punctures make them the preferred choice for vehicles ranging from bicycles to commercial trucks. Major players such as Bridgestone and Goodyear leverage advanced manufacturing to produce high-quality butyl rubber tubes, catering to the growing demand in the automotive and cycling sectors, particularly in the Asia Pacific and North America.

- Natural rubber inner tubes are the fastest-growing segment, driven by their eco-friendly properties and cost-effectiveness. They are increasingly adopted in emerging markets, where affordability is key, and in bicycle applications due to rising environmental consciousness. Companies such as Maxxis International are expanding their natural rubber offerings, targeting cost-sensitive regions such as South Asia and Latin America.

By Vehicle Type

- Two-wheelers account for over 35% of market revenue in 2025, driven by the high penetration of motorcycles and bicycles in emerging economies. Countries such as India and China, with large two-wheeler populations, fuel demand for inner tubes. Major manufacturers such as Apollo Tyres and MRF Limited supply durable tubes for this segment, supporting applications in urban commuting and recreational cycling.

- Bicycles are the fastest-growing segment, propelled by the global surge in cycling as a sustainable transport option. Urbanization and government initiatives, such as Europe’s cycling infrastructure investments, drive demand for bicycle inner tubes. Companies such as Continental and Schwalbe are innovating with lightweight, puncture-resistant tubes to meet the needs of urban cyclists and e-bike users.

By Distribution Channel

- OEMs dominate the tyre inner tubes market, contributing nearly 55% of revenue in 2025, due to their integration with automotive and bicycle manufacturing. OEMs ensure high-quality, standardized inner tubes for new vehicles, with companies such as Michelin and Pirelli partnering with major manufacturers such as Hero MotoCorp and Toyota to supply tailored solutions for two-wheelers and passenger cars.

- The aftermarket is the fastest-growing segment, driven by the rising need for replacement inner tubes in aging vehicle fleets and bicycles. The growth of e-commerce platforms, such as TyresnMore, facilitates easy access to aftermarket products, with brands such as Yokohama Rubber and Hankook Tire expanding their online presence to cater to consumer demand in North America and Europe.

Regional Insights

Asia Pacific Tyre Inner Tubes Market Trends

The Asia-Pacific region commands a leading share in the global tyre inner tubes market, accounting for approximately 40% of the total market as of 2025, and is expected to maintain its dominance through 2032. This strong position is underpinned by a combination of economic scale, industrial capacity, and socio-transportational trends unique to the region.

Asia-Pacific is home to two of the world’s largest automotive manufacturing hubs: China and India. China, the world’s largest tyre producer, contributes significantly to inner tube manufacturing, per the National Bureau of Statistics. India’s two-wheeler market, supported by initiatives such as the Smart Cities Mission, boosts demand for inner tubes.

The region’s cycling trend, with countries such as Japan promoting eco-friendly transport, further drives growth. Major players such as Bridgestone and Yokohama Rubber expand their presence, leveraging low-cost manufacturing and strong supply chains. Rapid urbanization and infrastructure investments ensure the Asia Pacific’s market dominance through 2032.

Europe Tyre Inner Tubes Market Trends

Europe is the fastest-growing region for the tyre inner tubes market, propelled by the rising adoption of electric vehicles and stringent safety regulations. The European Union’s focus on sustainable transport, with initiatives such as the Green Deal, drives demand for bicycle and e-bike inner tubes.

EV sales in Europe have seen exponential growth, with battery electric vehicles (BEVs) accounting for over 14.6% of all new car registrations in 2023. This surge creates a parallel demand for specialized inner tubes in electric motorcycles, mopeds, cargo bikes, and commercial light vehicles. Germany and France, key automotive hubs, support market growth through high vehicle ownership and cycling infrastructure investments.

Companies such as Continental and Pirelli innovate with puncture-resistant tubes for EVs and bicycles. The European Cyclists’ Federation reported surge in bicycle sales from 2020 to 2023, further boosting demand. Europe’s emphasis on eco-friendly materials and regulatory compliance ensures rapid market expansion.

North America Tyre Inner Tubes Market Trends

North America stands as the second fastest-growing region in the global tyre inner tubes market. This growth is driven by a robust automotive industry, infrastructure investment, and a rising preference for personal and sustainable mobility solutions, particularly in the U.S. and Canada.

According to the Alliance for Automotive Innovation, the overall automotive ecosystem (including manufacturing, sales, service, and related supplier activities) contributes about US$ 1.2 trillion annually to the U.S. economy, representing approximately 4.8% of GDP relies on inner tubes for commercial vehicles and motorcycles. Canada’s cycling infrastructure investments, per the Canadian Cycling Association, support demand for bicycle inner tubes.

Major players such as Goodyear and Cooper Tire dominate with extensive distribution networks, catering to both OEM and aftermarket segments. Consumer preference for durable, high-performance inner tubes and the rise of e-bikes further strengthen North America’s market position through 2032.

Competitive Landscape

The global tyre inner tubes market is fragmented, with a mix of global giants and regional players competing through extensive product portfolios and distribution networks. Leading companies such as Bridgestone Corporation, Michelin, and Goodyear dominate due to their advanced manufacturing capabilities and global reach.

Regional players such as Apollo Tyres and MRF Limited focus on cost-effective solutions for emerging markets. Companies are investing in eco-friendly materials and puncture-resistant technologies to enhance market share, driven by demand for sustainable and durable inner tubes in automotive and cycling applications.

Key Industry Developments:

- August 2024: Nokian Tyres is shifting heavy tyre inner tube production from its Lieksa, Finland, plant to a new dedicated production line at its Nokia, Finland, facility, with initial production in Nokia expected in early 2025. This strategic investment aims to increase capacity and improve its heavy tyre product portfolio to meet growing market demand. The Lieksa plant will wind down production throughout 2025 as the transition takes place.

- May 2024: Continental introduced the ContiTPU, a high-performance bicycle inner tube crafted from seven layers of micrometer-thick thermoplastic polyurethane (TPU). This design aims to enhance airtightness and durability, making it suitable for both road and off-road cyclists. It utilizes seven sealed layers of high-grade TPU to maximize airtightness and durability.

Companies Covered in Tyre Inner Tubes Market

- Bridgestone Corporation

- Michelin

- Goodyear Tire & Rubber Company

- Continental AG

- Pirelli & C. S.p.A.

- Sumitomo Rubber Industries, Ltd.

- Hankook Tire & Technology Co., Ltd.

- Yokohama Rubber Company

- Maxxis International

- Cooper Tire & Rubber Company

- Apollo Tyres Ltd.

- Others

Frequently Asked Questions

The tyre inner tubes market is projected to reach US$10.19 Bn in 2025.

Rising vehicle production, increasing bicycle usage, and expanding applications in electric vehicles are the key market drivers.

The tyre inner tubes market is poised to witness a CAGR of 2.28% from 2025 to 2032.

The growing demand for electric vehicles and sustainable transport is the key market opportunity.

Bridgestone Corporation, Michelin, Goodyear Tire & Rubber Company, and Continental AG are key market players.