- Plastics, Polymers & Resins

- Acrylonitrile Butadiene Styrene Market

Acrylonitrile Butadiene Styrene Market Size, Share, and Growth Forecast 2026 - 2033

Acrylonitrile Butadiene Styrene Market by Grade (High Impact, Flame Retardant, Heat Resistant, Electroplatable, Other), Technology (Extrusion, Injection Molding, Blow Molding, Thermoforming, 3D Printing), Application (Appliances, Electrical & Electronics, Automotive, Consumer Goods, Construction), and Regional Analysis for 2026 - 2033

Acrylonitrile Butadiene Styrene Market Size and Trend Analysis

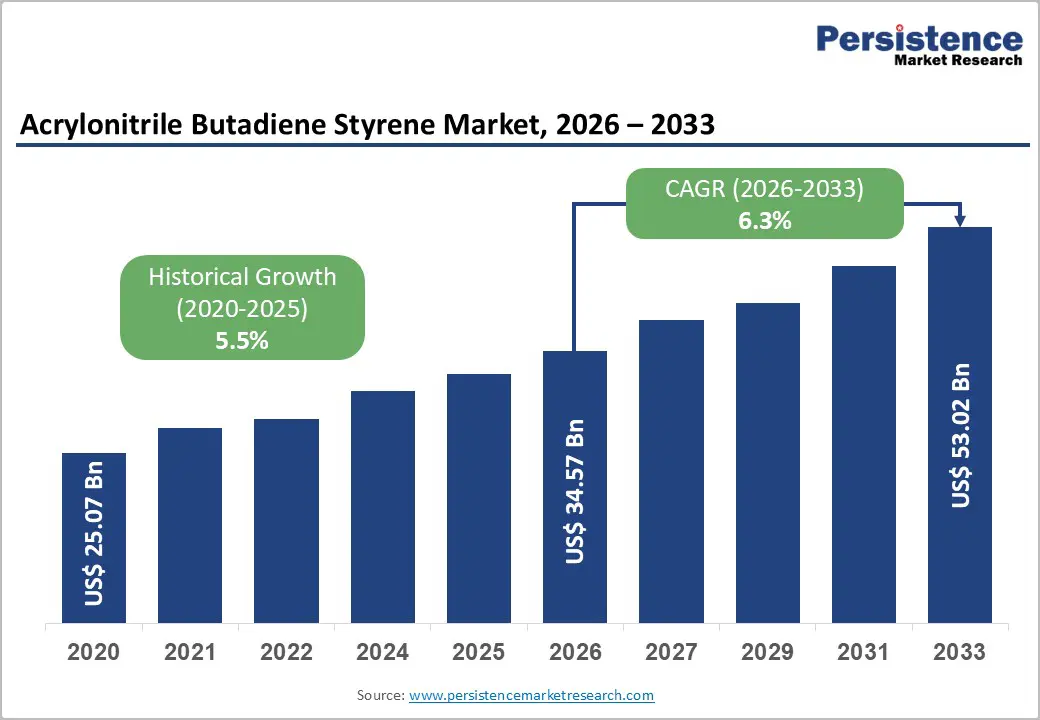

The global acrylonitrile butadiene styrene (ABS) market size is likely to be valued at US$ 34.6 Bn in 2026 and is projected to reach US$ 53.0 Bn by 2033, growing at a CAGR of 6.3% between 2026 and 2033.

The market is experiencing robust expansion driven by accelerating demand from the automotive sector for lightweight, impact-resistant materials and the proliferation of consumer electronics requiring durable protective casings. The rising adoption of lightweight materials to enhance fuel efficiency in vehicles, combined with the growing consumer preference for durable and aesthetically appealing products, creates substantial growth opportunities. Automotive manufacturers are increasingly adopting ABS resins to reduce vehicle weight, thereby improving fuel efficiency and meeting stringent emission regulations across North America, Europe, and the Asia Pacific region.

Key Market Highlights

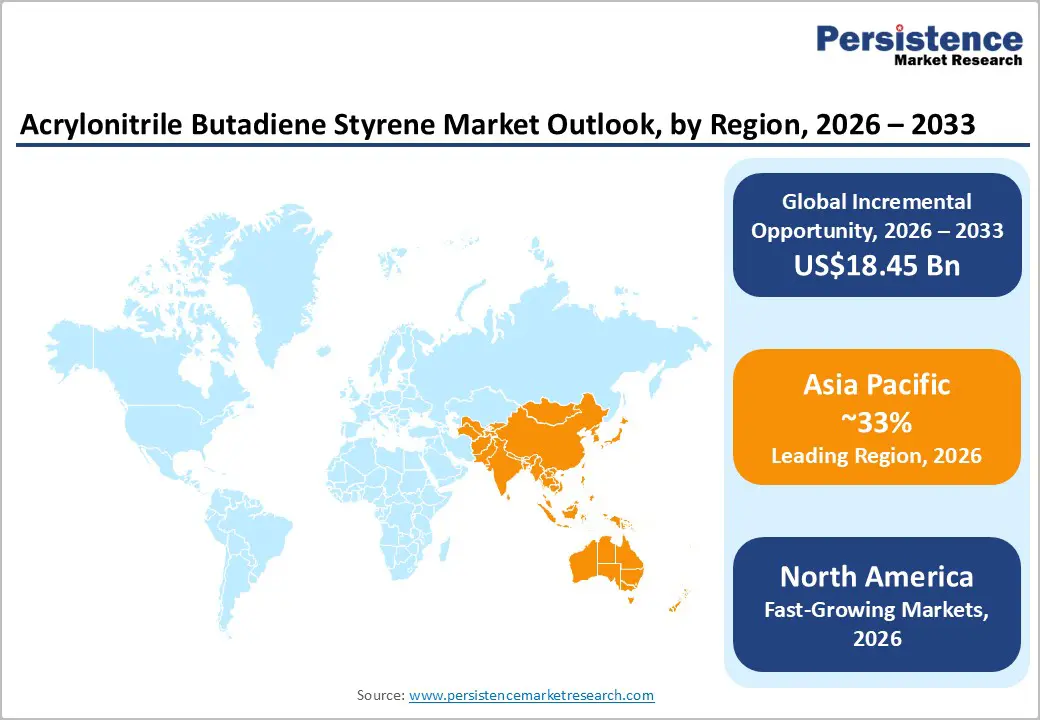

- Regional Leader: Asia Pacific dominates the global ABS market with over 33% of global revenue and approximately 80% of global production capacity, driven by China's manufacturing prowess, India's emerging demand, and Japan's advanced technological capabilities.

- Fastest Growing Region: North America emerges as the fastest-growing regional market, driven by electric vehicle adoption, stringent emission regulations, and accelerating investment in 3D printing.

- Leading Segment: The Opaque ABS segment maintains market leadership with approximately 40% market share, driven by extensive automotive and industrial applications.

- Fastest Growing Segment: 3D Printing technologies represent the fastest-expanding processing method segment, transitioning from prototyping to production-scale applications in aerospace, automotive, and consumer goods sectors.

- Key Market Opportunity: The emergence of bio-based and recyclable ABS solutions aligned with circular economy policies such as EU Green Deal climate neutrality targets, Energy Star sustainability mandates, and consumer preferences for environmentally responsible materials.

| Key Insights | Details |

|---|---|

|

Acrylonitrile Butadiene Styrene Market Size (2026E) |

US$ 34.6 Bn |

|

Market Value Forecast (2033F) |

US$ 53.0 Bn |

|

Projected Growth CAGR (2026-2033) |

6.3% |

|

Historical Market Growth (2020-2025) |

5.5% |

Market Dynamics

Drivers - Accelerating Demand from Automotive OEMs for Lightweight Components

The global automotive industry is increasingly prioritizing weight reduction to improve fuel efficiency and meet stringent emissions standards established by regulatory agencies. ABS's combination of low density, high impact resistance, and superior dimensional stability makes it an ideal material for interior trim components, dashboard panels, and exterior protective elements. The International Energy Agency (IEA) reported that improving vehicle lightweighting can reduce fuel consumption by 5-10% per 100 kilograms of mass reduction, directly incentivizing automotive manufacturers to adopt advanced materials like ABS.

Furthermore, the global shift toward electric vehicles (EVs) has intensified material demands, with China producing over 11 million electric vehicles in 2024, a 40% increase from 2023, substantially elevating ABS requirements for battery housings, charging system components, and thermal management structures. As EV penetration is projected to reach 50–54% by 2025, ABS will remain critical for battery housings, charging systems, and thermal management applications through 2033.

Expansion of Consumer Electronics and Smart Device Manufacturing

The rapid expansion of consumer electronics and smart devices has become a key driver of ABS market growth, supported by rising disposable incomes and technological advancements across both developed and emerging economies. ABS plastic is extensively employed in manufacturing protective casings, housings, and structural components for smartphones, laptops, televisions, and wearable devices due to its high impact strength, aesthetic finish, and ease of processing. The rising adoption of smart home devices, Internet of Things (IoT) products, and portable electronics has created unprecedented demand for durable, lightweight plastic materials.

The global appliance market, valued at significant levels, continues to expand as rising middle-class populations in India, China, and Southeast Asia drive demand for durable, aesthetically appealing consumer goods. Leading electronics manufacturers have standardized ABS specifications across product lines, ensuring consistent, long-term demand. Furthermore, sustainability initiatives have accelerated the development of recyclable ABS, exemplified by LG Chem’s introduction of a 70% bio-based ABS resin in 2022, reducing carbon emissions by up to 50% compared to conventional formulations.

Restraint - Environmental Regulations and Plastic Waste Management Compliance

Stringent environmental regulations have significantly impacted traditional ABS manufacturing and consumption, particularly in developed economies where sustainability compliance is mandatory. The European Union’s Directive on Single-Use Plastics and Design-for-Recycling requirements mandate that all plastic packaging include 10–35% post-consumer recycled content by 2030.

Furthermore, India’s Plastic Waste Management (Amendment) Rules 2024 require 30% recycled content for Category I plastics by 2025–2026, increasing to 60% by 2028–2029, creating substantial compliance challenges for manufacturers. These regulations have driven investments in advanced recycling technologies and bio-based ABS formulations, raising production costs. The WHO’s 2023 guidelines on plastic pollution and growing concerns over microplastic contamination have intensified consumer advocacy for reduced plastic use, particularly in single-use applications, potentially limiting ABS demand growth in mature markets.

Rising Raw Material and Feedstock Costs

Volatility in crude oil prices and disruptions in the acrylonitrile supply chain have exerted significant pricing pressure on ABS manufacturers, adversely affecting profitability and market competitiveness. Acrylonitrile feedstock costs, closely tied to petroleum markets, have historically fluctuated by 15–20% annually, creating uncertainty for producers operating on narrow margins. China’s aggressive capacity expansion, adding over 3 million metric tons annually since 2021, has led to regional oversupply, with utilization rates falling below 70%.

This surplus has caused 15–20% price erosion in Asian markets, compelling global players such as BASF SE, SABIC, and Trinseo to reassess growth strategies and consolidate operations. The situation is further aggravated by China’s slowing construction sector, a key ABS consumer, resulting in inventory surpluses likely to persist through 2025 and limiting pricing power globally.

Opportunity - Emergence of 3D Printing and Additive Manufacturing Applications

3-D printing has emerged as a significant growth area for ABS consumption, driven by rapid prototyping needs, complex geometries beyond traditional manufacturing, and increasing adoption in aerospace, healthcare, and automotive sectors. ABS filaments for 3D printing recorded around 12–18% annual growth between 2022 and 2024, supported by improved printer accessibility, lower equipment costs, and advanced material formulations. The aerospace industry increasingly employs 3D-printed ABS for interior fixtures, non-structural brackets, and prototypes due to its dimensional accuracy and impact resistance at elevated temperatures.

Technologies such as powder bed fusion and selective laser sintering enable the production of conformal cooling channels in injection molds, enhancing efficiency by 20–30%. With growing Industry 4.0 investments, 3D printing is projected to account for an additional 8–12% of industrial ABS consumption by 2033, creating substantial opportunities for specialty ABS manufacturers and technology providers.

Rising Demand from Construction and Infrastructure Applications in Emerging Markets

Rapid urbanization across Asia Pacific, Latin America, and the Middle East & Africa is driving significant demand for ABS in construction applications such as pipes, fittings, cable conduits, and building components. India’s urban population is projected to reach 600 million by 2030, supported by infrastructure investments in residential, commercial, and industrial projects. The Indian construction sector is expected to grow at 7–8% annually through 2030, well above global averages, creating strong opportunities for ABS suppliers in plumbing, electrical, and structural components.

Southeast Asian countries, including Vietnam, Indonesia, and Thailand, are witnessing accelerated construction activity, with ASEAN infrastructure investments estimated at US$150–160 billion annually. Furthermore, the adoption of ABS in renewable energy infrastructure, such as wind turbine housings, solar panel mounts, and thermal management systems, offers new application areas aligned with global sustainability goals. Companies focusing on specialty ABS grades and expanding distribution networks in emerging markets are well-positioned to capture substantial growth through 2033.

Category-wise Analysis

Product Type Insights

Opaque ABS holds the dominant position in the product type segment with approximately 40% market share, primarily due to its extensive use in automotive, appliance, and construction applications where transparency is not required. These formulations offer superior thermal stability, excellent color retention, and high-quality surface finishes that enable advanced aesthetic designs and brand differentiation. Automotive interior components such as instrument panels, air vent housings, and door trims account for the largest share of this segment.

Leading appliance manufacturers, including LG Electronics, Samsung Electronics, and Whirlpool Corporation, have standardized opaque ABS for washing machine housings, refrigerator parts, and microwave panels, ensuring consistent, high-volume demand. Transparent and colored ABS are gaining traction in consumer electronics, gaming devices, and smart home products, where optical clarity and distinctive aesthetics drive premiumization and higher-margin opportunities.

Grade Insights

High Impact ABS dominates the grade segment with approximately 42% market share, offering exceptional toughness and impact resistance for applications exposed to mechanical stress or requiring dimensional stability under varying temperatures. It is widely used in automotive safety components such as dashboard frames and impact-absorbing structures, where reliability is critical. Consumer electronics manufacturers also favor high-impact grades for smartphone, tablet, and portable device casings, ensuring drop resistance and long-term durability. This segment benefits from strong supply relationships with major injection molding processors across Asia Pacific, North America, and Europe, supporting consistent demand.

Flame retardant ABS meets stringent safety standards in electrical and electronics applications, including circuit breaker housings and enclosures, driven by UL 94 compliance mandates. Heat-resistant and Electroplatable ABS serve specialized, high-margin uses such as automotive exterior trims requiring electroplating and industrial components operating in elevated temperature environments.

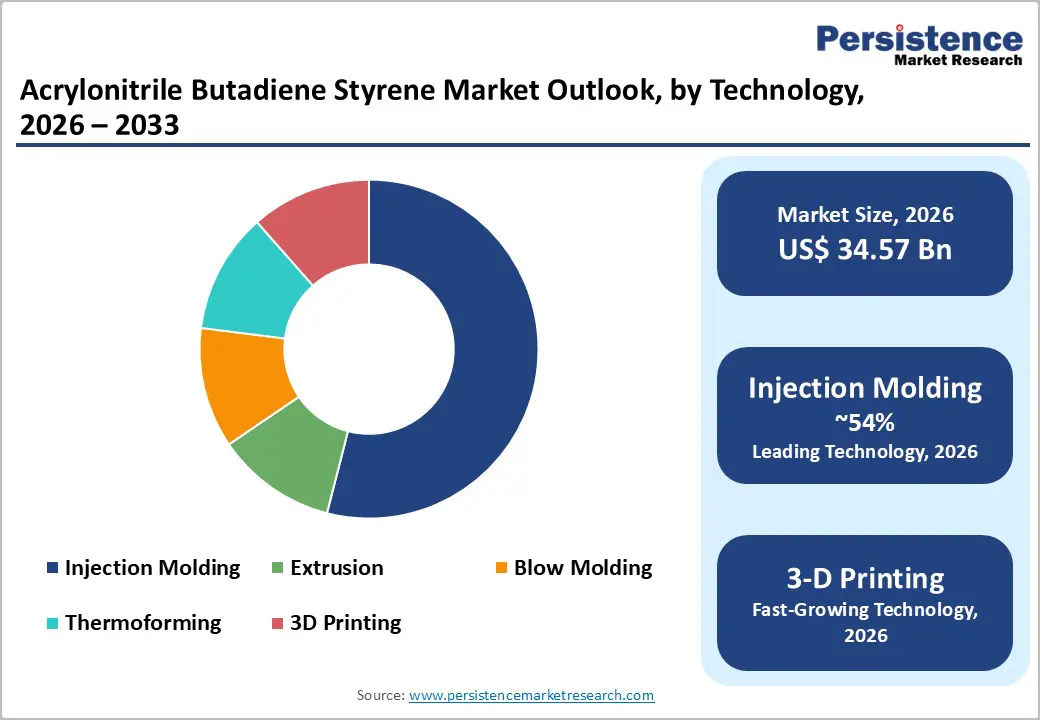

Technology Insights

Injection Molding leads the technology segment with approximately 54% market share, driven by superior manufacturing efficiency, precise tolerances, and scalability for cost-effective production of complex geometries. Its dominance reflects broad applicability across automotive interiors, consumer electronics housings, and appliance panels, where high-volume output and consistent quality are essential. Integration of Industry 4.0 technologies in modern facilities has enhanced real-time monitoring, predictive maintenance, and process optimization, improving efficiency and quality margins by 15–20%.

Extrusion accounts for about 22%, producing profiles, sheets, and tubing for construction, automotive trims, and industrial components, supported by automation and digitalization for rapid changeovers and customization. Blow Molding serves hollow products such as containers and reservoirs, while Thermoforming addresses sheet-based applications. Emerging 3D Printing is growing rapidly, driven by prototyping, aerospace, and custom manufacturing, positioning additive manufacturing as the fastest-growing segment through 2033.

Application Insights

Automotive applications command approximately 32% of the market, supported by extensive use in interior trim, dashboard components, protective bumper elements, and emerging EV-specific applications. The automotive segment benefits from stringent quality and performance requirements that create high barriers to entry, supporting long-term customer relationships and reducing competitive pressure from emerging suppliers.

The Electrical and Electronics segment is supported by the expansion of consumer electronics, smart devices, and industrial electrification, aligning with global digitalization trends. Appliances segment, encompassing major household equipment such as washing machines, refrigerators, and air conditioners, where ABS ensures durability and aesthetic appeal. Consumer Goods, including toys, furniture, and sporting equipment, offering cost-effective solutions for price-sensitive segments. Construction applications involve pipes, fittings, and structural components, with growth fueled by infrastructure development in emerging markets.

Regional Insights

North America Acrylonitrile Butadiene Styrene Trends

North America is emerging as the fastest-growing regional market for ABS, supported by advanced manufacturing capabilities, regulatory emphasis on vehicle lightweighting, and leadership in 3D printing adoption. Major automotive manufacturers such as General Motors, Ford, and Stellantis have standardized ABS specifications across platforms, creating stable, high-volume demand. The region’s electronics sector, concentrated in California and Texas, further drives ABS consumption in computing devices, telecommunications equipment, and consumer electronics.

Stringent regulatory frameworks, including ROHS compliance and sustainability mandates, have increased demand for specialty ABS grades incorporating recycled and bio-based feedstock. Agencies such as the EPA and CARB enforce strict emissions and waste reduction standards, prompting investments in advanced processing technologies. Recent developments include Trinseo’s launch of MAGNUM™ ECO+ and TYRIL™ CR recycled-content ABS and BASF SE’s expansion of sustainable ABS production capacity to serve premium, environmentally compliant segments.

Europe Acrylonitrile Butadiene Styrene Trends

Europe represents a mature and highly regulated ABS market, where demand is increasingly shaped by stringent sustainability mandates and advanced performance requirements. Leading automotive manufacturers such as Volkswagen AG, BMW, and Mercedes-Benz have implemented rigorous ABS specifications addressing safety, durability, and environmental compliance, creating high-value opportunities for suppliers meeting premium standards. The European Union’s Circular Economy Action Plan and Extended Producer Responsibility (EPR) mandates require the incorporation of post-consumer recycled material in plastic products by 2030, reinforcing sustainability-driven demand.

Recent developments include BASF SE’s investment in bio-based ABS production in Ludwigshafen and collaborative initiatives between OEMs and suppliers to meet evolving compliance requirements. Mandatory Design-for-Recycling standards and bans on single-use plastics have elevated technical specifications, supporting premium pricing.

Asia Pacific Acrylonitrile Butadiene Styrene Trends

Asia Pacific dominates the global ABS market, accounting for over 33% of global revenue in 2024 and hosting nearly 80% of global production capacity. China remains the largest producer and consumer of ABS resin, supported by expanding manufacturing capacity and strong demand from automotive, electronics, and appliance sectors. The region’s competitive advantages, lower labor costs, established industrial ecosystems, and proximity to raw material sources position it as the global hub for ABS production and consumption.

India is emerging as a key growth market, driven by rapid industrialization, rising middle-class populations, and expanding automotive and electronics sectors. Japan contributes through advanced manufacturing and high-performance ABS grades for specialized applications. ASEAN nations, including Vietnam and Thailand, are witnessing accelerating demand through growing manufacturing bases and integration into global supply chains. Planned investments exceeding US$ 2.2 billion for 12 ABS projects by 2030 underscore Asia Pacific’s strategic importance in global market dynamics.

Competitive Landscape

The global ABS market exhibits moderate consolidation characteristics with substantial market share concentrated among approximately 15-20 multinational producers, including LG Chem Ltd., ChiMei Corporation, BASF SE, SABIC, Trinseo, INEOS Styrolution, and Toray Industries Inc. These established manufacturers benefit from significant capital investments, advanced processing technologies, and extensive customer relationships, supporting barriers to entry. Emerging Chinese manufacturers, including PetroChina Co., Ltd. and Formosa Chemicals & Fibre Corporation, have rapidly expanded production capacity, contributing to global oversupply conditions and pricing pressure. Strategic research and development initiatives focused on heat-resistant and electroplatable grades for premium applications support higher-margin business segments and customer lock-in through specialized property requirements.

Key Market Developments

- June 2024: Trinseo launched MAGNUM™ ECO+ and MAGNUM™ CR recycled-content ABS brands, incorporating post-consumer recycled material and addressing emerging regulatory requirements for sustainable polymers across automotive, electronics, and appliance applications.

- August 2024: LG Chem Ltd. announced capacity expansion for bio-based ABS resin incorporating 70% bio-derived feedstock, reducing carbon footprint by up to 50% compared to conventional ABS production.

- December 2024: BASF SE launched comprehensive advanced recycling programs converting plastic waste into virgin-quality ABS feedstock, establishing partnerships with waste management companies across Europe and North America.

Top Companies in Acrylonitrile Butadiene Styrene Market

LG Chem Ltd. (Seoul, South Korea) operates as one of the world's largest ABS producers with a comprehensive product portfolio addressing automotive, electronics, appliance, and construction applications. The company has established dominant market positions in Asia Pacific through vertically integrated operations, advanced specialty grade capabilities, and strategic partnerships with major automotive OEMs.

SABIC (Riyadh, Saudi Arabia) ranks among the world's leading chemical companies with substantial ABS production capacity serving global automotive, electronics, and appliance industries. The company benefits from integrated feedstock advantages through petrochemical operations and advanced processing technologies, enabling high-performance specialty grades.

BASF SE (Ludwigshafen, Germany) operates as one of the world's largest chemical manufacturers with extensive ABS production and research capabilities supporting technical innovation and regulatory compliance. BASF's integrated ABS portfolio addresses diverse application requirements, including automotive, electronics, appliances, and emerging applications in renewable energy and aerospace sectors.

Companies Covered in Acrylonitrile Butadiene Styrene Market

- LG Chem Ltd.

- ChiMei Corporation

- Petrochina Co., Ltd.

- Formosa Chemicals & Fibre Corporation

- SABIC

- Toray Industries Inc.

- Lotte Chemical

- Versalis

- Kumho Petrochemical

- BASF SE

- Asahi Kasei Corporation

- Trinseo

- INEOS Styrolution

- Covestro AG

- LyondellBasell Industries

- Dow Chemical Company

- Styron GmbH

- Guangdong Xuanhai Chemical Co., Ltd.

Frequently Asked Questions

The global Acrylonitrile Butadiene Styrene (ABS) market is projected to reach approximately US$ 53.0 billion by 2033, growing from about US$ 34.6 billion in 2026 at a forecast CAGR of 6.3% between 2026 and 2033.

Key demand drivers include accelerating automotive OEM demand for lightweight, impact-resistant materials supporting fuel efficiency improvements, and rapid expansion of consumer electronics and smart device manufacturing requiring durable protective casings.

Injection Molding commands the leading position with approximately 54% of market share, driven by its superior manufacturing efficiency, tight tolerance capabilities, and scalability advantages.

Asia Pacific dominates the global ABS market with over 33% of global revenue and approximately 80% of global production capacity, driven by China's manufacturing prowess and India's emerging demand.

The emergence of bio-based and recyclable ABS solutions aligned with circular economy policies represents a multi-billion-dollar opportunity, driven by EU Green Deal climate neutrality targets, environmental regulations, and manufacturer demand for sustainable materials.