- Bulk Chemicals

- Alpha Methyl Styrene Market

Alpha Methyl Styrene Market Size, Share, and Growth Forecast, 2025 - 2032

Alpha Methyl Styrene Market by Purity Type (>99.5%, 95%-99%, Other), End-use (Automotive, Electronics, Chemical Manufacturing, Personal Care & Cosmetics, Other), and Regional Analysis for 2025 - 2032

Alpha Methyl Styrene Market Size and Trend Analysis

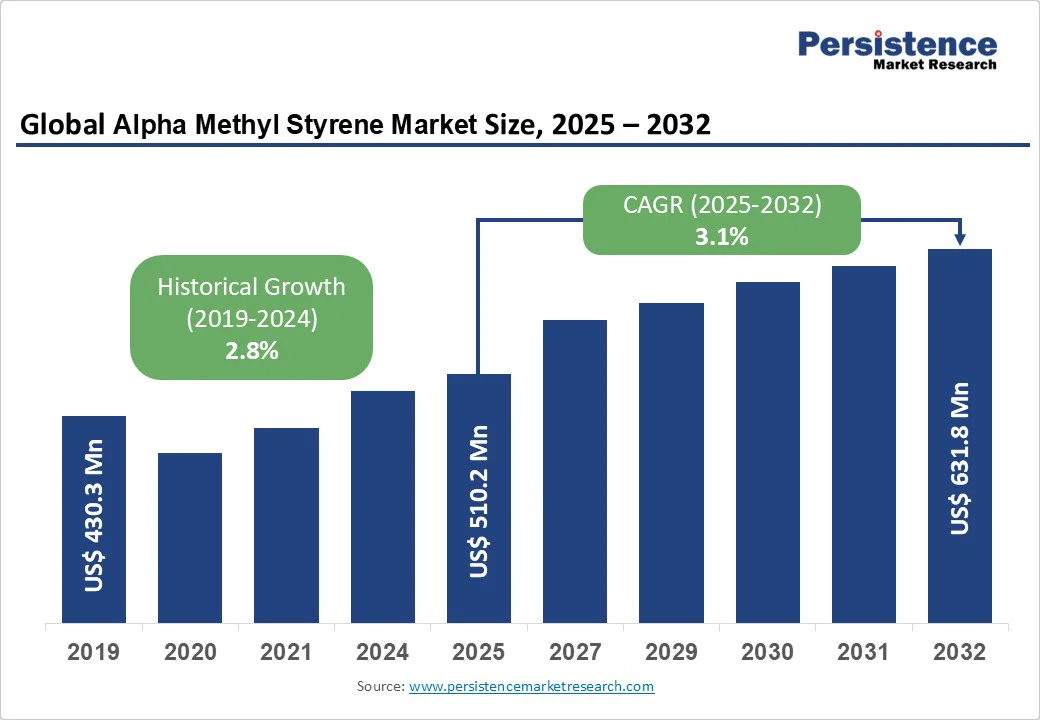

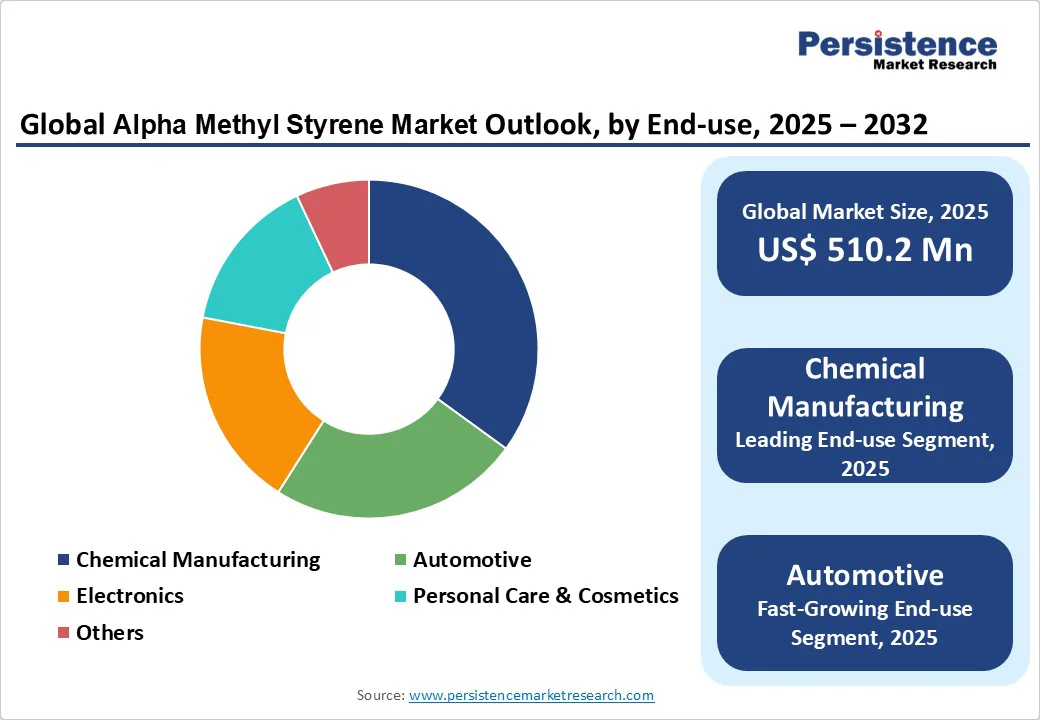

The global alpha methyl styrene market size is likely to value at US$510.2 Mn in 2025 and is expected to reach US$631.8 Mn by 2032, growing at a CAGR of 3.1% during the forecast period from 2025 to 2032. Rising demand for high-performance polymers in automotive, electronics, and chemical manufacturing drives growth.

Key Industry Highlights:

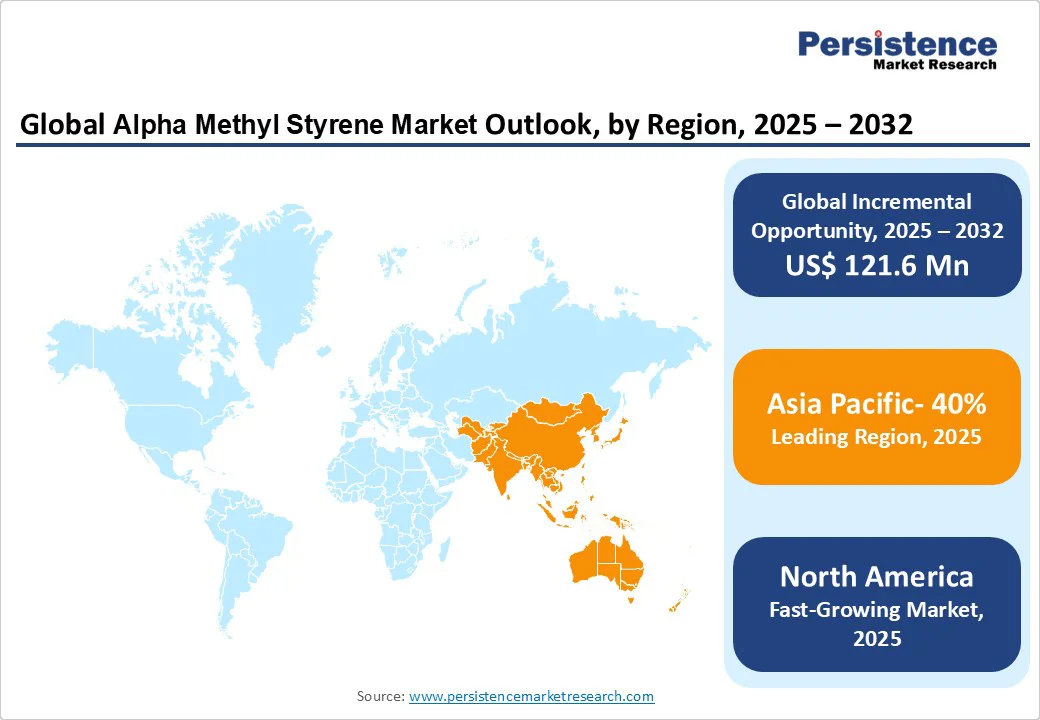

- Leading Region: Asia Pacific dominates with 40% global alpha methyl styrene market share in 2025, driven by strong chemical manufacturing growth, particularly in China’s automotive and electronics sectors.

- Fastest-Growing Region: North America is expanding rapidly, supported by increasing automotive and electronics production in the U.S., boosting demand for AES-based polymers and resins.

- Dominant Purity Type: AES with >99.5% purity holds a 50% share, favored for high-performance applications requiring heat resistance, durability, and consistent quality in advanced polymer production.

- Dominant End-Use: Chemical manufacturing leads with a 35% share, driven by extensive AES usage in producing resins, polymers, and plasticizers for diverse industrial applications.

- Key Developments: In February 2025, Kraton expanded its AMS-based plasticizer production by 15%, and in January 2025, Mitsubishi Chemical launched a high-purity (>99.5%) AMS line in Asia Pacific.

| Key Insights | Details |

|---|---|

|

Alpha Methyl Styrene Market Size (2025E) |

US$ 510.2 Mn |

|

Market Value Forecast (2032F) |

US$ 631.8 Mn |

|

Projected Growth (CAGR 2025–2032) |

3.1% |

|

Historical Market Growth (CAGR 2019–2024) |

2.8% |

Market Dynamics

Drivers - Increasing Demand for Polymers and Plasticizers in Automotive and Electronics

The growing need for polymers and plasticizers in automotive and electronics applications is a major driver of the alpha ethyl styrene (AES) market. AES is a critical monomer in the production of high-performance polymers such as acrylonitrile-butadiene-styrene (ABS) resins, commonly used in car components such as dashboards, bumpers, and interior panels. These materials offer excellent heat resistance, durability, and dimensional stability, which are essential for modern vehicles. With global automotive production rising, particularly in emerging economies, the demand for AES in ABS resins continues to expand.

In electronics, AES-based polymers are used to manufacture heat-resistant housings, connectors, and circuit boards. These materials ensure reliable performance and longevity in electronic devices. For instance, the U.S. Department of Energy highlights the increasing use of advanced polymer materials in electronics and automotive applications to enhance energy efficiency and product durability, reflecting a steady rise in AES demand.

Restraints - Raw Material Price Volatility and Environmental Concerns

Fluctuating raw material prices pose a significant restraint on the alpha ethyl styrene (AES) market. AES production relies on petrochemical feedstocks such as benzene and ethylene, whose prices are highly sensitive to global oil market dynamics. Sudden increases in these raw material costs can directly impact production expenses, leading to reduced profit margins for manufacturers. Additionally, supply chain disruptions or geopolitical tensions can further exacerbate price volatility, making it challenging for AES producers to maintain stable operations and consistent product pricing.

Environmental regulations and sustainability concerns also restrict the alpha methyl styrene market growth. The production and handling of AES involve emissions and waste that require strict management to meet environmental standards. Governments worldwide are enforcing stringent policies to minimize chemical pollution and promote sustainable industrial practices. Compliance with these regulations increases operational costs for manufacturers, potentially limiting large-scale expansion and influencing strategic investment decisions in the AES sector.

Opportunities - Growth in Emerging Markets and Sustainable Formulations

The expansion of emerging markets presents a significant opportunity for the alpha ethyl styrene (AES) industry. Rapid industrialization, increasing automotive production, and growing electronics manufacturing in regions such as the Asia Pacific, Latin America, and the Middle East are driving the demand for AES-based polymers. These markets offer substantial growth potential due to rising infrastructure development, expanding consumer bases, and increasing adoption of high-performance materials in end-use industries. Manufacturers can leverage these opportunities by establishing local production facilities and strengthening distribution networks to meet the rising demand efficiently.

Simultaneously, the shift toward sustainable formulations creates new avenues for AES applications. The chemical industry is increasingly adopting eco-friendly polymers and resins to reduce environmental impact. AES can be utilized in developing bio-based or low-emission polymer blends, aligning with global sustainability trends. Companies investing in greener production processes and innovative, sustainable formulations are likely to gain a competitive edge while meeting regulatory requirements and evolving consumer preferences.

Category-wise Analysis

Purity Type Insights

In 2025, alpha ethyl styrene (AES) with a purity of >99.5% dominates, accounting for approximately 50% of the total share. This segment’s leadership is driven by its widespread use in high-performance polymers such as acrylonitrile-butadiene-styrene (ABS) resins and styrene-acrylic copolymers, which require superior thermal stability, impact resistance, and dimensional accuracy. Industries such as automotive, electronics, and construction prefer high-purity AES to ensure consistent quality and optimal performance in critical applications, reinforcing the segment’s dominant position.

AES with a purity of 95%-99% is the fastest-growing segment. This range is increasingly adopted in applications where slightly lower purity suffices, but cost efficiency and production scalability are prioritized. Rising demand from emerging markets and expanding industrial applications is driving rapid growth in this segment, as manufacturers balance performance requirements with economic feasibility.

End-use Insights

In 2025, the chemical manufacturing sector dominates the alpha ethyl styrene (AES) market, holding approximately 35% of the total share. This dominance is attributed to AES’s extensive use in producing high-performance polymers, resins, and specialty chemicals. Chemical manufacturers rely on AES for applications in acrylonitrile-butadiene-styrene (ABS) resins, styrene-acrylic copolymers, and other polymer blends due to its thermal stability, impact resistance, and versatility. The consistent demand from chemical production ensures that this end-use segment maintains its leadership.

The automotive sector, however, is the fastest-growing end-use segment for AES. Increasing vehicle production, particularly in emerging economies, is driving demand for AES-based polymers used in dashboards, bumpers, interior panels, and other components. The growth is further fueled by the automotive industry’s focus on lightweight, durable, and high-performance materials, making AES an essential chemical for meeting evolving industry standards and consumer expectations.

Regional Insights

North America Alpha Methyl Styrene Market Trends

North America is the fastest-growing region in the alpha ethyl styrene (AES) market, driven by strong demand from the automotive, electronics, and chemical manufacturing sectors. The region’s well-established industrial infrastructure, advanced technological capabilities, and focus on high-performance polymers support the widespread use of AES in applications requiring heat resistance, impact strength, and dimensional stability. Additionally, increasing investments in sustainable and eco-friendly polymer formulations align with stringent environmental regulations and evolving consumer expectations, further boosting market growth. Favorable government policies, rising industrialization, and modernization in key sectors create significant opportunities for AES producers to expand their presence and cater to the growing regional demand.

Europe Alpha Methyl Styrene Market Trends

Europe holds a significant share in the alpha ethyl styrene (AES) market, driven by the region’s well-established chemical, automotive, and electronics industries. AES is extensively used in high-performance polymers such as ABS resins and styrene-acrylic copolymers, which are critical for automotive components, electronic housings, and construction materials. The presence of leading AES manufacturers and strong R&D infrastructure in countries such as Germany, France, and Italy supports consistent production and supply. Additionally, Europe’s stringent environmental regulations encourage the adoption of sustainable and low-emission polymer formulations, positioning AES as a preferred material. Steady industrial demand, technological advancements, and regulatory compliance collectively contribute to Europe’s significant market share in the global AES landscape.

Asia Pacific Alpha Methyl Styrene Market Trends

Asia Pacific dominates the alpha ethyl styrene (AES) market, accounting for about 40% of the global share. The region’s dominance is driven by rapid industrialization, growing automotive and electronics manufacturing, and rising infrastructure development. Key countries such as China, India, and Japan have strong demand for AES-based polymers such as ABS resins and styrene-acrylic copolymers, used in automotive parts, electronic components, and construction materials for their heat resistance and durability. The availability of raw materials, cost-effective production, and expanding consumer markets further strengthen the region’s position. Continuous investment in advanced materials and increasing industrial activity reinforce Asia Pacific’s dominant role in the global market.

Competitive Landscape

The global alpha ethyl styrene (AES) market is highly competitive, characterized by a mix of large-scale chemical manufacturers and regional producers. Companies focus on expanding production capacities, adopting advanced manufacturing technologies, and developing high-purity and sustainable AES grades to meet evolving industry demands. Strategic partnerships, mergers, and investments in research and development are common approaches to strengthening market presence. Innovation in polymer formulations, cost optimization, and compliance with environmental regulations play a crucial role in maintaining a competitive edge in the global AES market.

Key Developments

- February 2025: Kraton increased its AMS-based plasticizer production capacity by 15% at the Niort facility to address growing demand from the automotive sector for high-performance polymer applications.

- January 2025: Mitsubishi Chemical launched a high-purity (>99.5%) AMS line in Asia Pacific, enhancing performance in electronics applications and supporting the production of advanced polymers for high-temperature and durable components.

Companies Covered in Alpha Methyl Styrene Market

- Altivia

- Cepsa

- Domo Chemicals

- INEOS Group

- Kraton Corporation

- KUMHO P&B CHEMICALS

- Mitsubishi Chemical Corporation

- Prasol Chemicals Limited

- Solvay

- Others

Frequently Asked Questions

The alpha methyl styrene market is projected to reach US$510.2 mn in 2025, driven by demand in polymers and coatings.

Rising demand for polymers, plasticizers, and high-performance materials in automotive and electronics fuel market growth.

The alpha methyl styrene market will grow from US$510.2 Mn in 2025 to US$631.8 Mn by 2032, with a CAGR of 3.1%.

Expansion in emerging markets and sustainable formulations drive opportunities in automotive and electronics.

Leading players include Altivia, Cepsa, Domo Chemicals, INEOS Group, Kraton Corporation, KUMHO P&B CHEMICALS, Mitsubishi Chemical Corporation, Prasol Chemicals Limited, and Solvay.