- Medical Devices

- Surgical Imaging Market

Surgical Imaging Market Size, Trends, Share, Growth, and Regional Forecast, 2026 - 2033

Surgical Imaging Market by Product (Mobile C-arms, Mini C-arms, Endoscopy cameras, Others), by Technology (Image intensifier, Flat panel detector (FPD)), by Application, by End User, and Regional Analysis from 2026 - 2033

Surgical Imaging Market Share and Trends Analysis

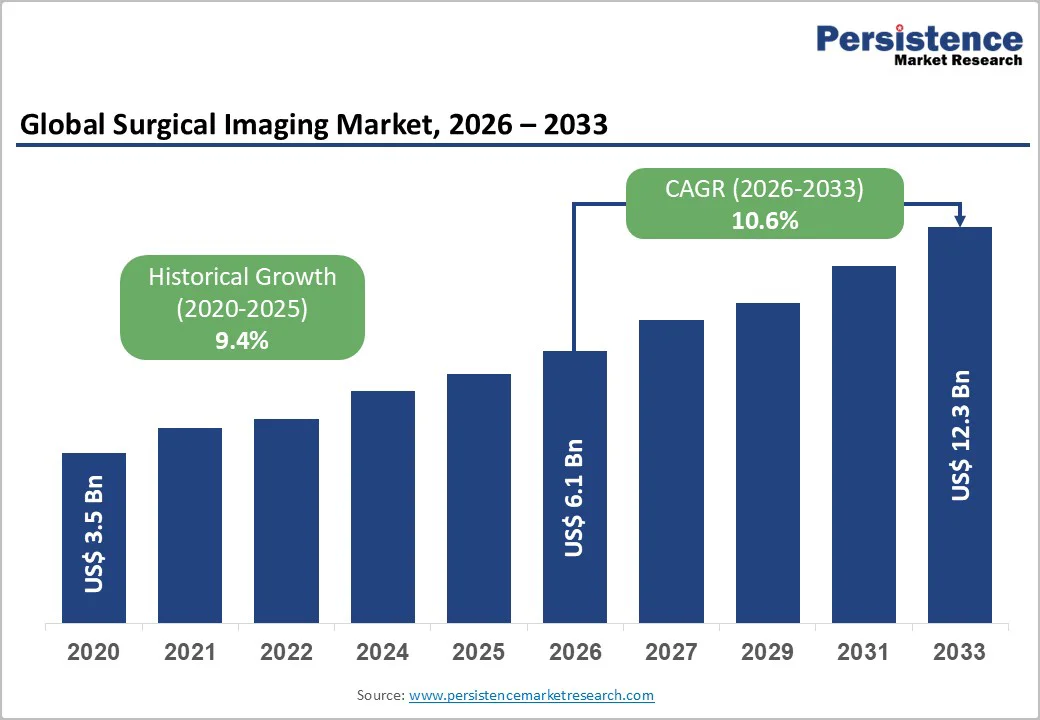

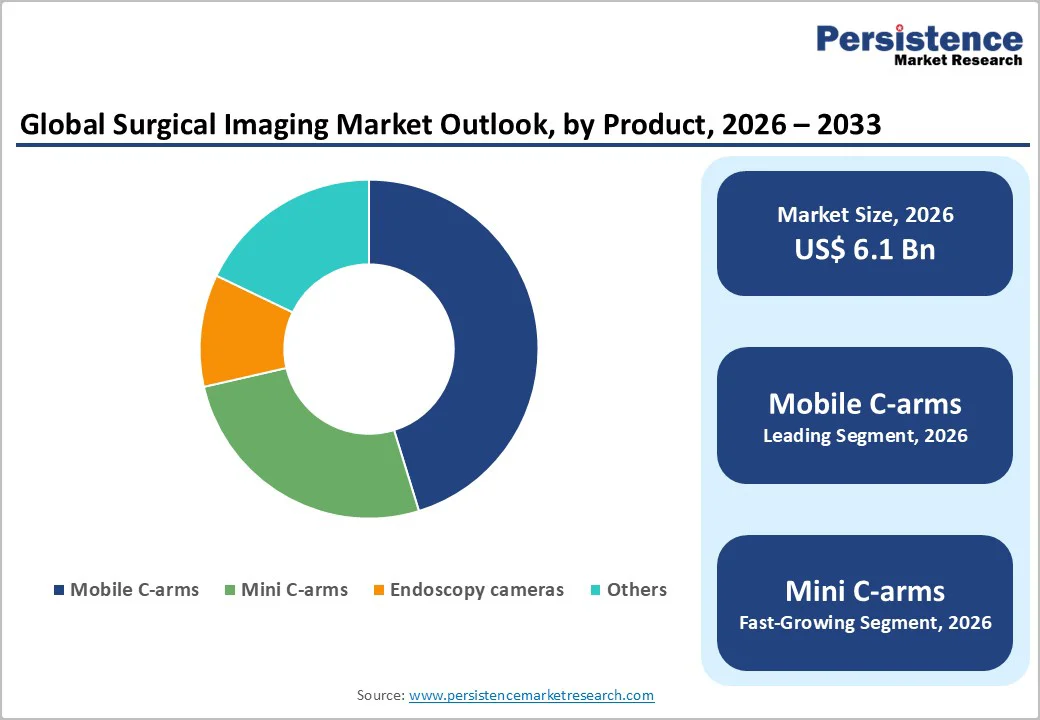

The global surgical imaging market size is likely to be valued at US$6.1 billion in 2026 and projected to reach US$12.3 billion by 2033. The market is projected to grow at a CAGR of 7.5% from 2026 to 2033. Market growth is steady as hospitals shift toward minimally invasive, image-guided procedures that demand high accuracy.

Mobile C-arms, flat-panel detector systems, and intraoperative CT/MRI are used to improve surgical precision, reduce complications, and support faster recovery. The rise in cases of orthopedic, cardiovascular, and neurological disorders further drives demand for real-time imaging in operating rooms. Technological advancements such as 3D imaging, hybrid ORs, and AI-enhanced visualization are transforming surgical workflows. Additionally, expanding healthcare infrastructure in emerging markets and greater adoption of digital imaging solutions continue to strengthen market growth across hospitals and ambulatory surgical centers.

Key Industry Highlights:

- Hybrid operating rooms are rapidly transforming surgical workflows by combining advanced imaging with minimally invasive procedures.

- Flat-panel detector C-arms are gaining dominance due to superior image clarity, low radiation, and faster workflow integration.

- Ambulatory surgical centers (ASCs) are adopting compact C-arms and portable imaging devices to support same-day surgeries.

- Leading Product: Mobile C-arms hold the largest share because they are used across a wide range of surgeries, orthopedic, cardiovascular, gastrointestinal, urology, spine, and trauma, making them essential equipment in most operating rooms.

| Key Insights | Details |

|---|---|

|

Surgical Imaging Market Size (2026E) |

US$6.1 Bn |

|

Market Value Forecast (2033F) |

US$12.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

10.6% |

|

Historical Market Growth (CAGR 2020 to 2024) |

9.4% |

Market Dynamics

Driver - Growing prevalence of orthopedic, trauma, and cardiovascular disorders

The growing prevalence of orthopedic, trauma, and cardiovascular disorders is significantly boosting the demand for advanced surgical imaging systems. With aging populations, road accidents, lifestyle-related diseases, and rising obesity rates, hospitals are witnessing a sharp increase in joint replacements, fracture repairs, spine surgeries, and cardiac interventions. These procedures rely heavily on accurate, real-time imaging for precise implant placement, vascular navigation, and safe tissue handling. Trauma cases, in particular, require rapid intraoperative visualization to make quick decisions in emergency settings. Similarly, cardiovascular surgeries increasingly depend on high-resolution fluoroscopy and 3D imaging for stent placement and structural heart interventions. As these conditions rise globally, healthcare providers are investing more in mobile C-arms, 3D systems, and hybrid-OR imaging platforms.

Restraints - Large Installation and Maintenance Expenses

Large installation and maintenance expenses remain a major restraint in the Surgical Imaging Market, particularly for hospitals in developing regions. Advanced imaging systems such as mobile C-arms, hybrid OR platforms, and intraoperative CT/MRI require significant capital investment not only for equipment purchase but also for specialized room preparation, electrical upgrades, shielding, and workflow integration. Additionally, ongoing maintenance costs, including annual service contracts, software updates, calibration, and part replacements, add substantial financial pressure on healthcare facilities. These systems often demand highly trained technical staff for upkeep, further increasing operational expenses. For smaller hospitals, ambulatory surgical centers, and budget-constrained institutions, such high lifetime costs limit adoption and delay modernization of surgical imaging capabilities.

Opportunity - Integration with Robotic-Assisted Surgery

Integration with robotic-assisted surgery is opening a powerful new opportunity in the surgical imaging market. As robotic systems take on increasingly complex procedures, surgeons require precise, real-time imaging to guide instrument movement, verify implant placement, and ensure accurate tissue targeting. Advanced C-arms, 3D imaging systems, and intraoperative CT/MRI now serve as the “eyes” of robotic platforms, enabling safer, more predictable outcomes. The growing shift toward fully digital, AI-supported surgical ecosystems further strengthens demand for imaging systems that seamlessly communicate with robotic arms and navigation software. This convergence is driving hospitals to upgrade to smarter, robotics-ready imaging infrastructure.

Category-wise Analysis

By Product Insights

Mobile C-arms lead the surgical imaging market because they are the most versatile and widely used imaging tools across operating rooms. Their ability to deliver real-time fluoroscopic images during orthopedic, cardiovascular, gastrointestinal, trauma, and spine procedures makes them essential for surgical decision-making. Hospitals prefer mobile C-arms for their portability, lower cost than intraoperative CT/MRI, and ease of integration into existing OR setups. Continuous technological improvements, such as flat-panel detectors, reduced radiation dose, and enhanced 3D capabilities, further strengthen their dominance. With high procedure volumes and broad clinical applications, mobile C-arms naturally capture the highest market share globally.

By Application Insights

Orthopedic surgery accounts for the largest share of the surgical imaging market due to its frequent reliance on real-time imaging to achieve precise surgical outcomes. Procedures like fracture fixation, joint replacements, spinal fusion, and trauma interventions require continuous fluoroscopic guidance to ensure accurate alignment and implant placement.

The global rise in orthopedic cases, driven by aging populations, sports injuries, and increasing road accidents, further boosts demand. Mobile C-arms and other imaging devices are essential tools in nearly every orthopedic operating room, making imaging indispensable. High procedure volumes and the critical need for intraoperative visualization make orthopedic surgery the leading application segment in the market.

Region-wise Insights

North America Surgical Imaging Trends

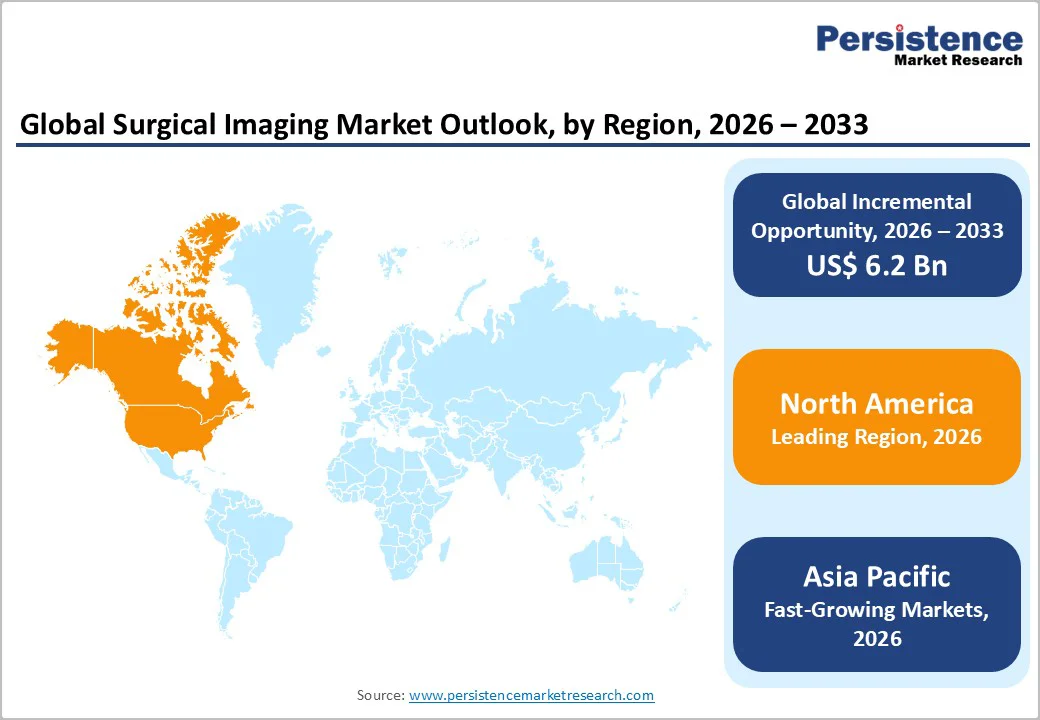

North America is the leading region in the surgical imaging market, driven by advanced healthcare infrastructure, high adoption of minimally invasive procedures, and continuous technological innovation. The U.S., as the largest contributor, benefits from significant investments in hybrid operating rooms, mobile C-arms, and AI-enhanced imaging systems. Surgeons increasingly rely on real-time intraoperative imaging for orthopedic, cardiovascular, and neurosurgical procedures, improving accuracy and reducing complications. Strong reimbursement policies, widespread digital integration, and a focus on patient safety further support market growth. Additionally, increasing hospital expansions and upgrades in imaging equipment sustain North America’s dominance and position the U.S. as a key global market leader.

Asia Pacific Surgical Imaging Market Trends

The Asia-Pacific surgical imaging market is growing rapidly, fueled by expanding healthcare infrastructure, rising hospital investments, and growing medical tourism. Countries such as China, India, Japan, and South Korea are upgrading operating rooms with advanced imaging systems, including mobile C-arms, mini C-arms, and intraoperative CT/MRI, to support minimally invasive and complex surgeries. Rising incidence of orthopedic, cardiovascular, and neurological disorders drives demand for real-time imaging. Affordable healthcare initiatives, increasing government funding, and the presence of private hospital chains are accelerating adoption. Continuous technological innovation and rising awareness of advanced surgical procedures position the Asia Pacific as a high-growth, emerging market.

Competitive Landscape

The global surgical imaging market is highly competitive, driven by continuous technological advancements such as flat-panel detectors, 3D imaging, AI-assisted visualization, and integration with robotic surgery. Companies compete on image quality, portability, workflow efficiency, and radiation safety. Strategic collaborations, mergers, and regional expansions are common to strengthen market presence. Emerging players in developing regions offer cost-effective solutions to meet rising demand.

Key Industry Developments:

- In October 2025, Royal Philips installed its 5,000th Zenition mobile surgical imaging system at Kolín Regional Hospital in the Czech Republic. Since its launch in 2019, Zenition has become a trusted solution in hospitals across more than 170 countries, enabling surgeons and interventional teams to perform image-guided procedures more efficiently and support improved treatment outcomes.

Companies Covered in Surgical Imaging Market

- GE Healthcare

- Siemens Healthineers

- Philips Healthcare

- Canon Medical Systems

- Ziehm Imaging

- Medtronic

- Shimadzu Corporation

- Hologic

- Carestream Health

- Fujifilm

- Other

Frequently Asked Questions

The global surgical imaging market is projected to be valued at US$6.1 Bn in 2026.

Increasing preference for MIS procedures requires real-time imaging for precision, shorter recovery, and reduced complications.

The global market is poised to witness a CAGR of 10.6% between 2026 and 2033.

Imaging systems supporting real-time navigation and verification.

GE Healthcare, Siemens Healthineers, Philips Healthcare, Canon Medical Systems, and others.