- Technology

- Super Apps Market

Super Apps Market Size, Share, and Growth Forecast, 2026 - 2033

Super Apps Market by Service Offering (Payments, Financial Services, E-Commerce, Food Delivery, Messaging & Social, Government Services, Others), Platform (Monolithic Apps, Mini-App Platforms, Aggregator Models, White-Label Platforms), End-User (Consumers, Small & Medium Businesses, Large Enterprises, Government Entities), and Regional Analysis for 2026 - 2033

Super Apps Market Share and Trends Analysis

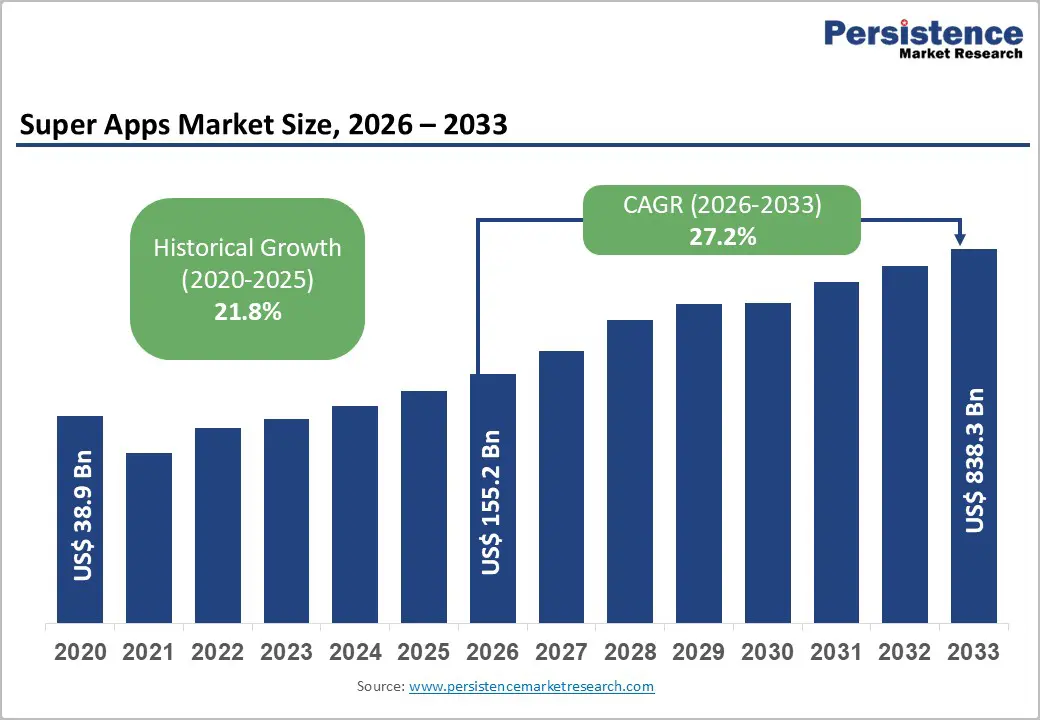

The global super apps market is projected to reach US$ 155.2 billion in 2026 and is estimated to reach US$ 838.3 billion by 2033, growing at a CAGR of 27.2% over the forecast period 2026 - 2033. Market expansion is accelerating as digital payments, embedded finance, mobility digitization, and platform-based commerce are increasingly converging into unified consumer ecosystems.

In the Asia-Pacific region, digital wallet penetration exceeds 70% in several major economies, according to the World Bank Global Findex Database and national payment authorities. This penetration depth is strengthening daily transaction frequency and reinforcing platform stickiness. The Bank for International Settlements (BIS) reports that digital payment volumes are growing by more than 15% annually across emerging Asian economies, indicating sustained transaction volume.

Regulatory infrastructure is also improving interoperability. Systems such as India’s Unified Payments Interface (UPI) and open banking frameworks across the European Union (EU) are reducing transaction friction and enabling multi-service integration within single digital platforms. Super apps are now functioning as integrated financial gateways rather than simple transaction aggregators. Public filings from top market players indicate that embedded lending, insurance distribution, and digital wealth services are expanding at faster rates than core transaction services. Platforms are also strengthening monetization by leveraging proprietary data for risk assessment and personalization.

Key Industry Highlights

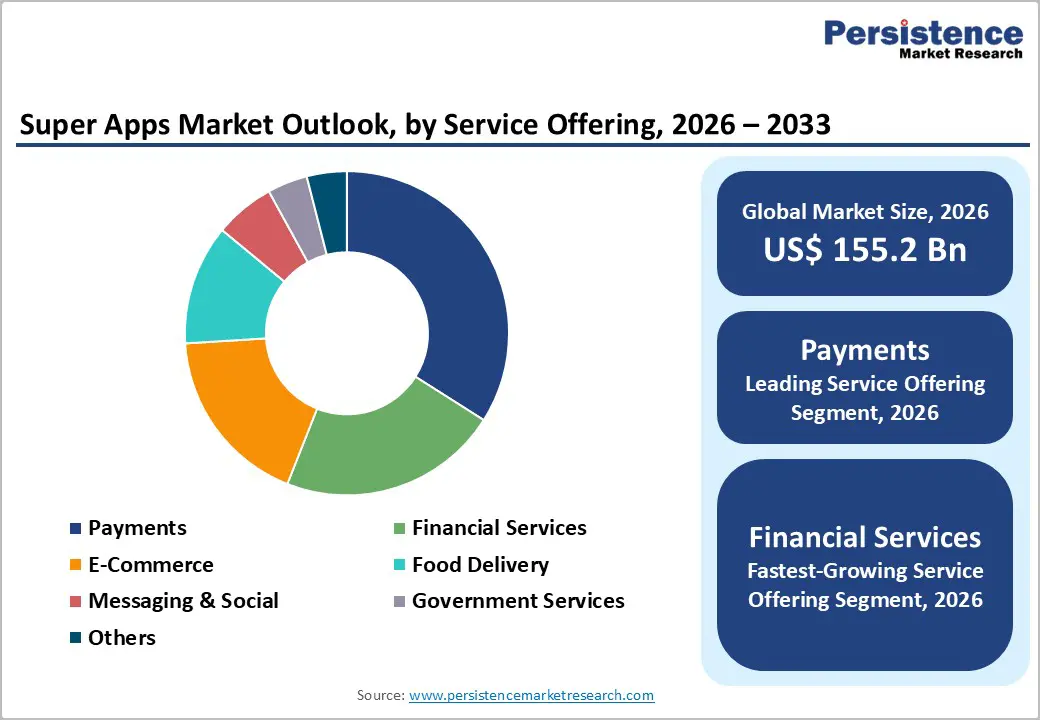

- Dominant Service Offering: Payments are projected to account for approximately 33% revenue share in 2026, owing to their role as the primary engagement anchor.

- Fastest-growing Service Offering: Financial services are expected to be the fastest-growing segment, with a roughly 31% CAGR through 2033, driven by embedded lending, digital insurance penetration, and AI-enabled credit underwriting.

- Leading Platform: Monolithic super app architectures are projected to account for around 55% of the market in 2026, driven by integrated data control and vertical monetization efficiency.

- Fastest-growing Platform: Mini-app platforms are expected to grow the fastest through 2033, driven by expansion of developer ecosystems and lower service integration costs.

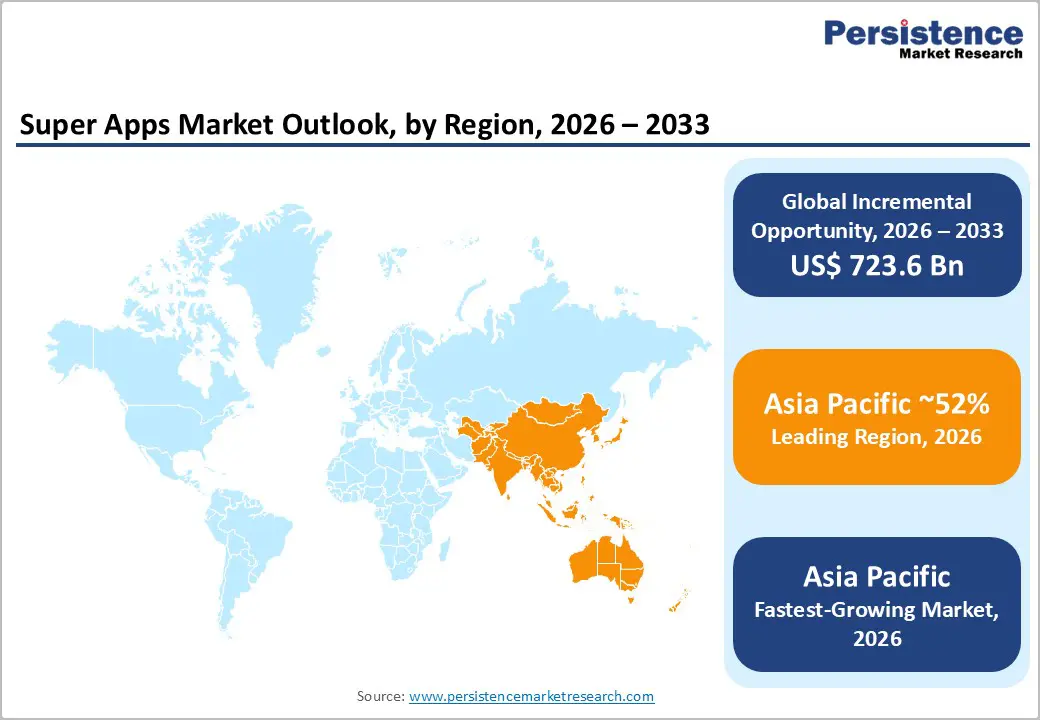

- Regional Leadership: Asia Pacific is poised to dominate with an estimated 52% market share in 2026, and exhibit a CAGR of around 29% through 2033, supported by high digital wallet penetration and government-backed instant payment systems.

- Main Drivers: Embedded finance integration, AI-driven personalization and underwriting models, and regulatory-backed instant payment infrastructure are strengthening multi-service digital ecosystems, propelling the market.

- January 2026: UnionPay rolled out the Nihao China super app to streamline payments and travel services for foreign visitors in China, integrating digital payments, travel tools, and localized services for international users.

| Key Insights | Details |

|---|---|

| Super Apps Market Size (2026E) | US$ 155.2 Bn |

| Market Value Forecast (2033F) | US$ 838.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 27.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 21.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Embedded Finance Integration within Consumer Platforms

Central banks and financial regulators are strengthening real-time payment infrastructure to improve transparency, interoperability, and transaction efficiency. The Reserve Bank of India (RBI) reported that UPI volumes exceeded 11 billion transactions per month in 2024, indicating widespread adoption of the instant payment architecture. This regulatory formalization provides a stable foundation for super apps to embed financial products into high-frequency payment flows. Platforms are integrating credit, micro-insurance, and digital investment tools directly into wallet interfaces, which is increasing user engagement and expanding average revenue per account.

Embedded finance adoption is reducing customer acquisition costs because platforms cross-sell financial products to existing user bases rather than acquiring new customers through standalone channels. Public disclosures from Tencent Holdings Ltd. indicate that fintech and business services account for a significant share of consolidated revenue, reflecting increasing monetization from financial integration. This structural shift is repositioning super apps from transaction-processing utilities into diversified financial ecosystems.

Urban Mobility Digitization and On-Demand Logistics Expansion

According to the United Nations Department of Economic and Social Affairs (UN DESA), the developing economies of Asia and Africa are undergoing sustained urban population growth across Asia and Africa. This demographic shift is increasing daily demand for app-based transportation, meal delivery, and hyperlocal logistics. Expanding metropolitan clusters require more efficient mobility coordination and faster fulfillment systems. Governments are simultaneously investing in smart-city infrastructure, including digital mapping platforms, integrated traffic management systems, and intelligent transport networks. These public investments are improving route optimization and reducing operational friction for platform-based service providers.

Super apps are consolidating ride-hailing, courier services, and food logistics within unified interfaces, and this aggregation is generating scale efficiencies across supply and demand pools. At the same time, car ownership growth is moderating in several emerging economies due to congestion, fuel costs, and infrastructure constraints, reinforcing shared mobility adoption and strengthening network effects within multi-service platforms. As mobility ecosystems deepen and cross-service engagement expands, super apps are extending their economic relevance beyond payments and into integrated urban consumption infrastructure.

Regulatory Fragmentation and Data Sovereignty Constraints

The European Union (EU) is enforcing stricter digital governance through the Digital Markets Act (DMA) and the General Data Protection Regulation (GDPR), and these frameworks are tightening data portability, interoperability, and consent requirements. Super app operators are facing increased compliance obligations when processing consumer data across multiple services within a single platform. Cross-border expansion also requires formal financial service authorizations, including banking, insurance, and consumer credit licenses. These regulatory requirements are increasing legal, capital, and reporting costs. Companies operating across jurisdictions are navigating fragmented supervisory regimes that are extending product-approval timelines and increasing operational complexity.

Financial regulators are also applying capital adequacy standards to embedded lending activities, particularly when platforms underwrite credit risk directly. This is increasing balance sheet exposure and constraining aggressive geographic rollouts. Firms that lack licensed financial subsidiaries are entering into partnerships with regulated banks, which is limiting revenue capture and compressing margins. Variations in consumer protection laws, data localization rules, and licensing thresholds across regions are further complicating expansion strategies. However, this regulatory heterogeneity moderates the pace of international scaling and increases the cost of cross-border integration.

Platform Congestion and Competitive Ecosystem Saturation

Large technology ecosystems are intensifying competition for consumer engagement across payments, messaging, commerce, and financial services. In mature markets, established messaging applications, independent fintech platforms, and dominant e-commerce marketplaces are already securing strong user loyalty. This structural entrenchment is creating barriers to consolidation under a single super-app model. Digital advertising markets are becoming more expensive as companies bid aggressively for visibility on search engines and social media platforms. As a result, customer acquisition costs are increasing, particularly in North America and Europe where user switching behavior is more limited.

Corporate disclosures are confirming that promotional incentives and rider or driver subsidies are continuing to represent significant operating expenditures in mobility and delivery verticals. When competitors are offering price discounts to capture market share, margin pressure is intensifying. This dynamic is compressing contribution margins in urban logistics and ride-hailing operations. In regions where the super app model has not historically dominated digital behavior, multi-app usage patterns are persisting. This competitive saturation is limiting pricing power and delaying the expansion of profitability. Super app operators are responding by prioritizing operational efficiency and focusing on high-frequency service bundles, yet sustained discount-led competition is moderating earnings acceleration in developed markets.

Emerging Market Financial Inclusion Expansion

The World Bank Global Findex Database shows that nearly 76% of adults worldwide now hold a bank or mobile money account, jumping from 51% in 2011. This expansion reflects substantial progress in financial access, yet substantial inclusion gaps persist across Sub-Saharan Africa and parts of Southeast Asia. In several low-income economies, large segments of the population are still relying on informal financial channels. Super apps are addressing this gap by integrating digital payments, microcredit, and low-ticket insurance products within a single mobile interface. By embedding financial services within widely used digital platforms, providers reduce onboarding friction and expand access among underbanked users. Governments and central banks are also promoting digital identification systems and interoperable payment rails, which are facilitating broader participation in formal financial ecosystems.

If platforms are generating conservative average revenue per user in the range of US$ 20 to US$ 30 annually, this incremental base represents a multi-billion-dollar expansion opportunity. Revenue potential continues to increase as credit penetration and insurance attachment rates improve over time. Early engagement with regulators and banking partners is increasingly critical, as licensing alignment accelerates product rollout and strengthens trust. Super apps that are establishing compliant financial frameworks at an early stage are positioning themselves to capture durable market share as inclusion rates continue rising.

AI-Driven Personalization and Monetization Optimization

Artificial intelligence (AI) is enhancing credit underwriting, dynamic pricing frameworks, and recommendation systems across super app ecosystems. Platforms are deploying machine learning models to analyze transaction histories, behavioral data, and repayment patterns in real time. For instance, Tencent and Sea Limited are increasing investments in AI infrastructure to enhance personalization and improve service matching across payments, commerce, and financial products. These investments are supporting more accurate demand forecasting and targeted cross-selling. As data-processing capabilities improve, platforms are refining risk segmentation and adjusting product offerings at scale.

AI-driven credit scoring models are reducing default probabilities in micro-lending portfolios by improving borrower risk assessment. Personalization engines are increasing conversion rates in digital commerce and financial service subscriptions. This integration is raising average revenue per user while lowering marginal customer acquisition and servicing costs. Operational efficiency is improving as automated decision systems reduce manual intervention in underwriting and fraud detection. AI-enabled monetization enhancements can add approximately two to four percentage points to effective revenue growth rates when compared with transaction-only platform models over the 2026-2033 forecast period. Companies that are embedding advanced analytics into their core architecture are strengthening competitive differentiation and long-term margin resilience.

Category-wise Analysis

Service Offering Insights

Payments are projected to command approximately 33% of the super app market revenue share in 2026. Payment functionality serves as the foundational layer across most ecosystems, supporting high-frequency, low-friction transactions. Users are conducting daily transfers, merchant payments, and bill settlements through integrated wallet interfaces, which is strengthening engagement intensity and platform stickiness. Instant payment frameworks supported by central banks are reducing transaction costs and settlement delays, thereby increasing usage density. High transaction frequency is generating behavioral data that supports targeted lending, insurance, and wealth distribution. Platforms are leveraging payment histories to enhance risk assessment and personalize financial offerings. This structural advantage allows payment-led ecosystems to maintain revenue leadership despite diversifying into other service categories.

Embedded financial services are likely to record the highest growth at an estimated 2026 - 2033 CAGR of 31%. Financial services are benefiting from existing payment data, which is improving underwriting precision and accelerating approval timelines. Financial deepening is increasing average revenue per user by expanding monetization beyond transaction fees. AI-based risk models are improving portfolio performance and enhancing risk-adjusted returns. Regulatory clarification across the Asia Pacific is enabling licensed lending expansion and product diversification. As consumer trust in digital financial services continues to rise and regulatory frameworks mature, revenue from the financial services segment can increase by a tangible amount by 2033.

Platform Insights

The monolithic super app model is projected to account for approximately 55% of the total revenue share in 2026. This dominance stems from integrated control over payments, mobility services, commerce operations, and embedded financial products within a unified technical architecture. Platforms that operate end-to-end infrastructure retain greater economic value because they manage user acquisition, transaction processing, and service fulfillment internally. Vertical integration strengthens margin preservation by minimizing third-party commission leakage and reducing dependence on external application programming interfaces. Integrated architecture is also enabling tighter data synchronization across services. Companies are optimizing internal data flows to enhance personalization, risk scoring, and cross-selling efficiency. This internal control is improving monetization precision and lowering operational friction.

Mini-app ecosystems are projected to expand at a CAGR of approximately 30% between 2026 and 2033. Open-platform architectures enable third-party developers to deploy lightweight applications within host environments, reducing internal development expenditure and accelerating service diversification. This modular approach is expanding the breadth of available services without requiring proportional capital investment from the core platform operator. Platform-as-a-service models are encouraging external innovation by providing software development kits, payment rails, and user authentication infrastructure. Developers are leveraging existing user bases, while platforms earn commission or service fees, accelerating ecosystem expansion and broadening developer participation.

Regional Insights

North America Super Apps Market Trends

North America is projected to account for approximately 18% of the super app market share in 2026. Market growth here is expected to reach nearly 24% CAGR between 2026 and 2033. Adoption dynamics are differing from Asia Pacific since the digital ecosystem is already fragmented across specialized applications for messaging, payments, mobility, and commerce. Regulatory oversight remains strong, particularly in financial services and data governance, thereby limiting rapid consolidation into a single multi-service platform. Competition from established fintech firms, card networks, and large e-commerce marketplaces is continuing to moderate ecosystem unification.

Despite these structural constraints, the integration of embedded finance is gaining momentum. Financial institutions and technology firms in the United States are expanding partnerships to enable wallet-based credit, buy-now-pay-later solutions, and subscription-based service bundles. Digital payment penetration is increasing as contactless transactions and real-time settlement systems are becoming more widespread. Platforms are leveraging subscription models to enhance recurring revenue and strengthen user loyalty. As financial product integration deepens and regulatory clarity evolves, super apps operating in North America are gradually increasing service convergence, which is supporting steady yet relatively moderate growth through 2033.

Europe Super Apps Market Trends

Europe is forecasted to account for approximately 15% of the global market for super apps in 2026, with growth estimated near a 23% CAGR from 2026 to 2033. The revised Payment Services Directive (PSD2) facilitates open banking integration by requiring banks to provide secure access to customer data via application programming interfaces (APIs). This regulatory framework supports financial aggregation on digital platforms and encourages the development of multi-service ecosystems. Payment interoperability is improving across the EU, which is facilitating cross-border digital transactions and strengthening wallet-based services.

At the same time, the GDPR and the DMA impose strict controls on data use, data portability, and platform gatekeeping practices. These rules limit large-scale data centralization and restrict preferential service bundling across integrated ecosystems. Compliance requirements are increasing operational costs and extending product rollout timelines. As a result, growth in Europe remains steady but comparatively moderate. Platforms that are aligning with regulatory standards while optimizing open banking integration are likely to capture sustainable expansion during the 2026-2033 forecast period.

Asia Pacific Super Apps Market Trends

Asia-Pacific is projected to account for an estimated 52% of the super app market value in 2026 and to register a CAGR of nearly 30% through 2033. Digital wallet adoption remains high across major economies, supported by government-backed instant payment infrastructure and widespread mobile penetration. Central bank-led payment systems such as India’s UPI and real-time settlement frameworks across Southeast Asia are increasing transaction interoperability and lowering processing costs. Rapid urbanization and dense metropolitan clusters are strengthening demand for ride-hailing, food delivery, and digital financial services within integrated mobile ecosystems.

China, India, Indonesia, and Singapore are leading regional transaction volumes due to strong consumer engagement and expanding merchant digitization. Regulatory frameworks are becoming more structured, particularly in areas such as digital lending, insurance distribution, and electronic know your customer (eKYC) compliance. This formalization is increasing trust and enabling broader expansion of financial products within super app platforms. With payment penetration deepening and financial inclusion policies advancing at a notable pace, Asia Pacific is expected to have consolidated its leadership position by 2033, supported by scale efficiencies and ecosystem integration advantages.

Competitive Landscape

The global super apps market structure is demonstrating moderate concentration, with a small group of large multi-service ecosystems accounting for a substantial share of total revenue. Collectively, the top five operators are contributing an estimated 35-40% of global market revenue. Market power is increasingly consolidating around platforms that have achieved scale in digital payments and embedded financial services. Companies such as Tencent Holdings, Ant Group, Grab Holdings Limited, Sea Limited, and Meituan are representing the most influential ecosystem operators within this structure.

Competitive dynamics are increasingly being shaped by payment transaction density, regulatory licensing depth, capital capacity, and ecosystem integration breadth. Platforms that are controlling proprietary payment infrastructure and holding formal financial service licenses are retaining higher margins and expanding monetization per user. Network effects are strengthening as integrated mobility, commerce, and financial services are reinforcing cross-service engagement. Regulatory scrutiny and capital requirements are raising entry barriers, which is favoring established players with diversified revenue streams and compliance infrastructure. Competitive positioning is likely to be determined by scale efficiency, embedded finance capability, and the ability to sustain multi-service ecosystem cohesion across regions.

Key Industry Developments

- In August 2025, Rappi partnered with the digital wallet platform AstroPay to introduce Latin America’s first wallet-on-file integration inside a super-app, now live in Argentina, Brazil, and Peru. This integration enables users to pay seamlessly from multi-currency wallet balances without needing a card, benefiting from real-time foreign exchange conversion and reducing friction at checkout as cross-border payment volumes in the region grow rapidly.

- In August 2025, Lloyds Banking Group introduced a barcode-based cash deposit feature in its mobile banking app that allows customers to deposit notes and coins at over 30,000 PayPoint locations across the U.K., with the barcode valid for two hours after generation and deposits appearing in accounts within minutes. Customers can deposit up to £300 per day and up to £600 per month using the barcode at participating outlets such as local convenience stores.

- In July 2025, Kazakhstan’s Halyk Bank agreed to acquire a 49% stake in Uzbekistan’s fintech super-app Click for US$ 176.4 million, while Click’s shareholders will acquire a 49% interest in Halyk’s Uzbek unit Tenge Bank for US$ 60.76 million, creating a strategic cross-border partnership to scale digital financial services across both markets.

Companies Covered in Super Apps Market

- Tencent Holdings Ltd.

- Ant Group Co., Ltd.

- Grab Holdings Limited

- Sea Limited

- Meituan

- PT GoTo Gojek Tokopedia Tbk

- One97 Communications Limited

- LINE Corporation

- Kakao Corp.

- Rappi Inc.

- PayPal Holdings, Inc.

- Block, Inc.

- Uber Technologies, Inc.

- Careem Networks FZ-LLC

Frequently Asked Questions

The global super apps market is projected to reach US$ 155.2 billion in 2026.

The accelerating unification of digital payments, embedded finance, mobility digitization, and platform-based commerce into consumer ecosystems is primarily driving the market.

The market is poised to witness a CAGR of 27.2% from 2026 to 2033.

The incorporation and expansion of lending, insurance distribution, and digital wealth services, explosion of monetization avenues for platforms by leveraging proprietary data for risk assessment and personalization producing highly lucrative market opportunities.

Tencent Holdings Ltd., Ant Group Co., Ltd., Grab Holdings Limited, and Sea Limited are some of the key players in the market.