- Advanced Materials

- Stretch Films Market

Stretch Films Market Size, Share, and Growth Forecast, 2025 - 2032

Stretch Films Market by Material Type (Linear Low-Density Polyethylene (LLDPE), Low-Density Polyethylene (LDPE), High-Density Polyethylene (HDPE), Polyvinyl Chloride (PVC), Others), Manufacturing Process (Blown Stretch Film, Cast Stretch Film.), End-Use (Food & Beverage, Consumer Goods, Industrial Packaging, Logistics & Transportation, Agriculture, Pharmaceuticals, Others), and Regional Analysis for 2025 - 2032

Stretch Films Market Share and Trends Analysis

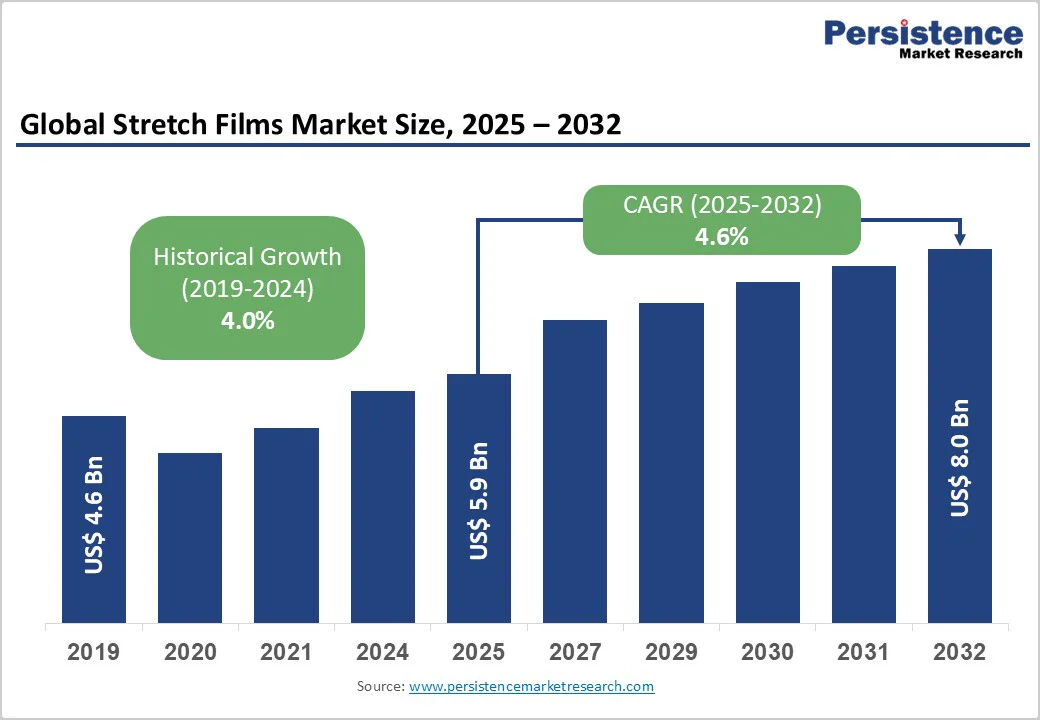

The global stretch films market size is likely to be valued at US$5.9 billion in 2025, and is projected to reach US$8.0 billion by 2032, growing at a CAGR of 4.6% during the forecast period 2025 - 2032.

This market expansion reflects sustained demand driven by accelerating e-commerce transformation, modernization of the logistics sector, and increasing adoption across agricultural and pharmaceutical packaging applications.

Global trade volume growth, combined with the rapid expansion of cold-chain logistics and supply chain automation, continues to reinforce the demand for high-performance stretch film solutions capable of securing diverse load configurations across multiple transportation modalities.

Regulatory drivers, including the European Union (EU) Packaging and Packaging Waste Regulation (PPWR), are catalyzing the adoption of recyclable and post-consumer recycled (PCR) stretch film formulations.

Key Industry Highlights

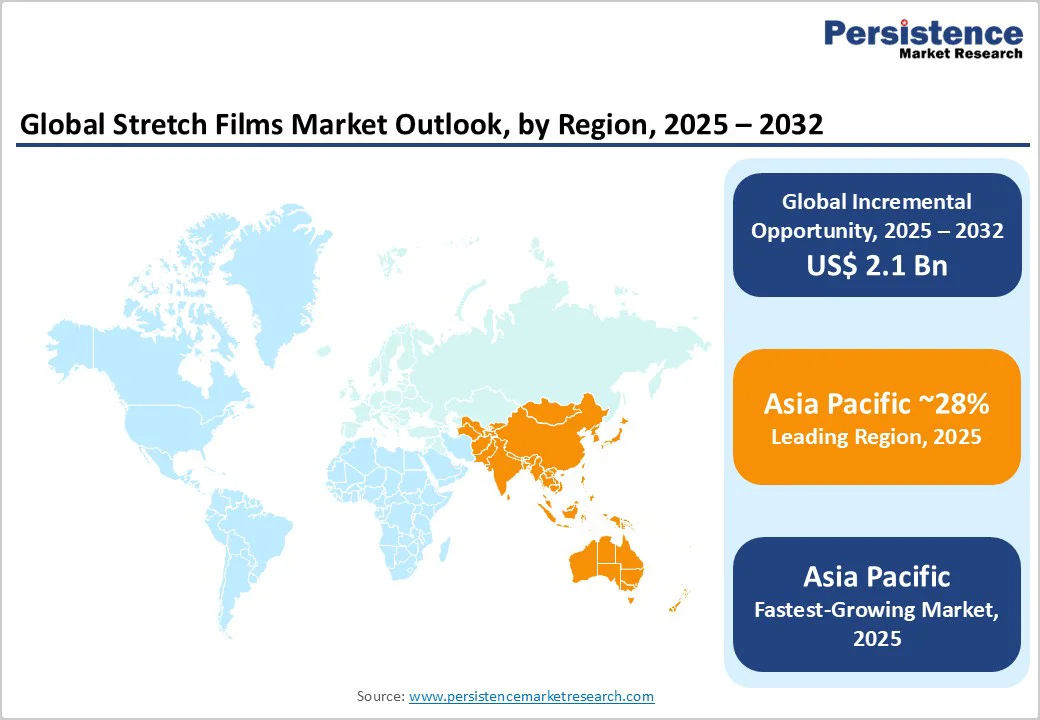

- Largest Regional Market: Asia Pacific leads with around 28% share in 2025, driven by strong manufacturing output and rapid e-commerce expansion in China and India.

- Second-largest Market: Europe holds about 24% of global demand in 2025, supported by stringent PPWR regulations driving the adoption of recycled and compostable stretch film formulations.

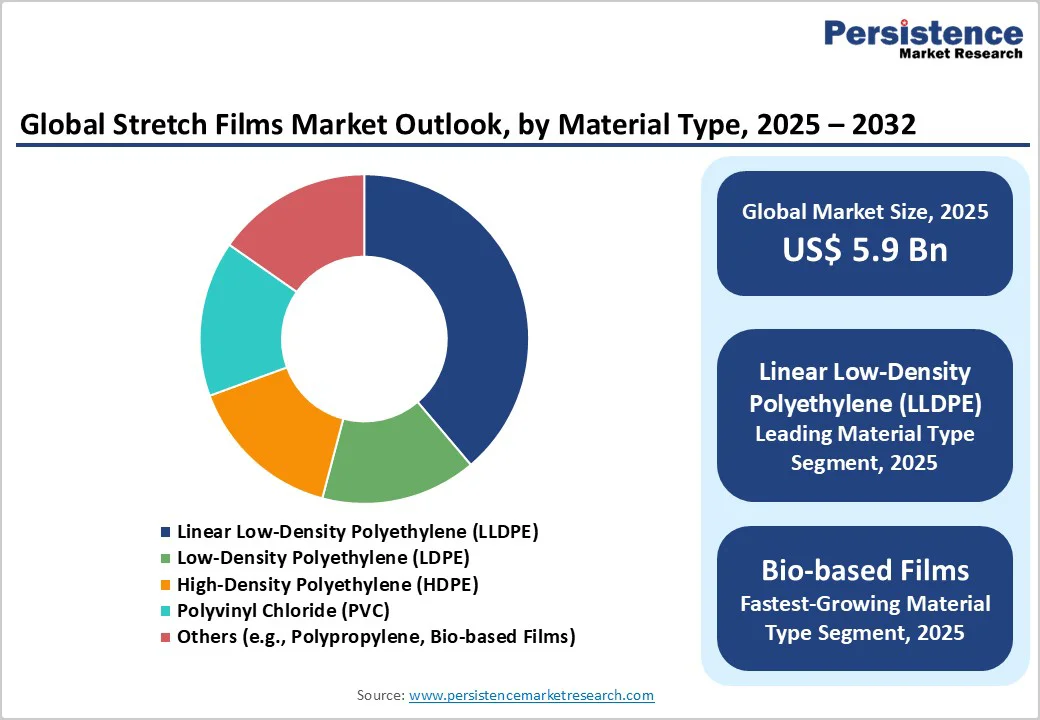

- Leading Material: Linear low-density polyethylene (LLDPE) dominates with around 55% share in 2025, owing to superior flexibility, strength, and cost-efficiency.

- Dominant Manufacturing Process: Blown extrusion dominates in 2025 with nearly 70% share, offering enhanced puncture resistance and strength for heavy-load applications.

- Dominant End-Use: Logistics and transportation emerge as the top end-use segment, holding about 32% market share in 2025, supported by a steady increase in global trade and 3PL infrastructure expansion.

| Key Insights | Details |

|---|---|

| Stretch Films Market Size (2025E) | US$ 5.9 Bn |

| Market Value Forecast (2032F) | US$ 8.0 Bn |

| Projected Growth (CAGR 2025 to 2032) | 4.6% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

E-Commerce Logistics Infrastructure Expansion Accelerating Palletization

E-commerce growth is significantly increasing demand for stretch films used to secure and protect products during shipping and storage across global supply chains. As online retail continues to expand worldwide, businesses require increasing quantities of stretch film for palletizing products, bundling orders, and consolidating loads for efficient transportation.

Major distribution centers and fulfillment facilities rely on stretch film to stabilize loads, prevent damage during transit, and reduce shipping costs. Supply chain automation is driving the adoption of specialized stretch films designed for high-speed wrapping equipment used in modern logistics operations.

Regulatory requirements for sustainable practices are also reshaping the trajectory of the stretch film market by mandating recycled content and promoting circular economy principles. The EU, for example, has established requirements for industrial films to incorporate recycled content and maintain recyclability standards by 2030.

Similar initiatives in the U.S. have encouraged manufacturers to develop stretch films with recycled content while maintaining performance quality. Companies are responding to these regulatory demands by innovating new stretch film formulations that incorporate recycled materials without compromising strength or durability.

This shift toward sustainable, recycled-content stretch films creates opportunities for manufacturers to meet both performance standards and environmental requirements, while supporting circular-economy objectives and reducing plastic waste in global supply chains.

Raw Material Price Volatility and Petroleum Derivative Cost Sensitivity

Stretch film manufacturers are facing pressure from fluctuating petroleum prices that directly impact production costs and profit margins. The cost of raw materials used in stretch film production varies significantly based on crude oil prices and global supply conditions.

When raw material costs increase substantially, manufacturers must raise product prices to maintain profitability. Still, customers often resist higher prices, creating challenges in price-competitive markets such as food packaging and standard logistics applications.

Recycled plastic materials offer a solution to some cost challenges but currently command higher prices than virgin materials, limiting their use primarily to premium market segments and applications where regulatory compliance requires them rather than where customers voluntarily choose them for environmental reasons.

Smaller manufacturers and regional companies struggle most with margin compression as raw material costs rise, since they have less pricing power with customers compared to larger industry players.

Biodegradable and bio-based stretch films represent an emerging market opportunity driven by regulatory requirements and brand owner demand for environmentally sustainable packaging solutions. Manufacturers are developing advanced stretch film formulations from plant-based materials that can be industrially composted while maintaining performance comparable to conventional petroleum-based films.

For instance, premium brand owners in food and beverage, personal care, and pharmaceutical sectors increasingly specify biodegradable stretch films to meet future regulatory requirements and differentiate products through environmental credentials.

Companies that develop biodegradable stretch film production capability and establish certification processes early will be well positioned to capture market share as regulatory timelines accelerate and industry standards for bio-based polymer systems are based.

Smart Packaging Integration and Track-and-Trace Technology Adoption Creating Value-Added Service Opportunities

Advanced tracking technologies such as RFID tags, barcode systems, and digital packaging identifiers are creating new opportunities in the stretch films market by shifting traditional film products toward intelligent packaging that supports real-time supply chain visibility, tamper detection, and product authentication.

Recent developments in track-and-trace stretch film solutions show that embedding identification technology directly into packaging is commercially feasible, enabling manufacturers to differentiate otherwise commodity films with added security and traceability features.

High-value sectors such as pharmaceuticals and premium consumer goods are particularly interested in these smart packaging capabilities because they help meet serialization rules, anti-counterfeiting requirements, and cold-chain monitoring needs for temperature-sensitive products that demand continuous documentation.

Digital packaging integration also allows brand owners and packaging converters to capture and analyze logistics data, optimize transport efficiency, identify recurring damage patterns, and support predictive maintenance programs, extending the value proposition beyond basic protection and containment.

As smart packaging adoption grows, stretch film producers that combine compatible equipment, such as printing, coding, and reader integration, with supporting software and analytics platforms can create new revenue streams from licensing, data services, and compliance reporting, while strengthening customer relationships and reducing price-based competition.

Category-wise Analysis

Material Type Insights

Linear low-density polyethylene (LLDPE) remains the dominant material in the stretch films market due to its exceptional balance of flexibility, strength, and puncture resistance, making it ideal for pallet wrapping, load consolidation, and bundle securing in logistics, food service, and industrial packaging.

Its unique molecular structure allows superior stretch capacity while maintaining mechanical integrity. LLDPE is cost-effective compared to other polymers, with resin prices consistently lower than high-density polyethylene and specialty polymers, enabling competitive pricing and healthy margins in both commodity and specialty applications.

On the other hand, bio-based and compostable polymers such as polylactic acid (PLA), polybutylene adipate terephthalate (PBAT), and polyethylene derived from renewable sources represent the fastest-growing segment, driven by regulatory compliance and increasing demand from premium brands for certified sustainable packaging solutions.

Manufacturing Process Insights

Blown extrusion dominates the stretch films market revenue share in 2025, accounting for around 70% of production due to its superior mechanical properties and performance suited to demanding containment applications.

This process involves extruding molten resin through a circular die, inflating it into a bubble, and cooling it to create a film with multi-directional strength, excellent puncture resistance, and high elongation capacity. These characteristics make blown films ideal for securing loads where durability and flexibility are critical.

In contrast, the cast extrusion process is the fastest-growing manufacturing segment through 2032, favored for its superior optical clarity, higher production efficiency, and better compatibility with automation systems, making it an economical choice for high-volume output.

Cast films are typically transparent or translucent, allowing visual inspection of wrapped products, which is especially important in pharmaceutical, food contact, and consumer goods packaging where product visibility and tamper-evident features build consumer trust and support regulatory compliance. The differences between blown and cast films allow businesses to select solutions tailored to their specific packaging and logistical needs.

End-Use Insights

Logistics & transportation is the largest end-use segment in the stretch films market, accounting for roughly one-third of the market in 2025. This dominance is driven by global trade growth, modernization of third-party logistics, and increased supply chain automation in key regions, including North America, Europe, and the Asia Pacific.

Applications in this segment include pallet wrapping, bundle consolidation, container securing, and load stabilization, which are essential for multimodal transportation methods such as trucking, rail, ocean freight, and air cargo. These logistics operations benefit from standardized load securing techniques compatible with automated material handling systems, improving efficiency and safety across supply chains.

Agricultural applications of stretch films are experiencing the fastest growth, fueled by advances in crop protection technology, sustainable farming practices, and climate adaptation needs. Specialized stretch film variants address critical agricultural needs, including moisture management, ventilation, and product preservation.

The fresh produce export market particularly demands vented stretch films that reduce condensation and allow oxygen permeability, preventing spoilage and fungal contamination during extended refrigerated transport. This growing demand reflects an increased focus on maintaining product quality during cold-chain logistics, driving innovation and adoption of tailored stretch film solutions in the agricultural sector.

Regional Insights

Asia Pacific Stretch Films Market Trends

Asia Pacific dominates the stretch films market, accounting for about 28% of demand in 2025, driven by its manufacturing strength, concentrated supply chain infrastructure, and rapid e-commerce growth across China, India, and Southeast Asia. China leads as both the primary consumption hub and major production center, with extensive manufacturing capacity supporting industrial packaging, consumer goods distribution, and export logistics.

India’s expanding e-commerce market and growing domestic production infrastructure sustain demand across quick-commerce logistics, third-party logistics, and retail supply chains. Government investments in infrastructure including port upgrades, rail expansion, and warehouse development across the region further reinforce the demand for stretch films by optimizing logistics and supporting trade volume growth.

Economic growth indicators such as China’s steady GDP growth, India’s vigorous e-commerce expansion, and Southeast Asia’s manufacturing sector development are driving East Asia to become the fastest-growing regional market in the stretch films sector.

Regional producers benefit from cost-competitive manufacturing, enabling them to supply multinational companies with integrated and efficient packaging solutions. These factors combine to position the Asia Pacific region as the key driver of global stretch film market growth, highlighting the importance of innovation, logistics optimization, and regulatory adaptation in sustaining the sector’s expansion.

Europe Stretch Films Market Trends

Europe holds the second-largest regional market share, capturing approximately 24% of the demand in 2025. This growth is supported by stringent regulations targeting plastic waste reduction, recycled content mandates, and compostability standards, all of which accelerate the adoption of sustainable and specialty stretch film products.

The EU’s PPWR, finalized in 2024 and effective between 2026 and 2030, sets binding targets for recycled content and mandatory compostability, driving a significant shift in material composition toward eco-friendly films. European brand owners and logistics companies are actively adopting recyclable and recycled-content stretch films to comply with regulations and meet corporate sustainability goals.

Demand dynamics in Europe prioritize premium products that emphasize sustainability credentials, regulatory compliance documentation, and advanced performance features over simply minimizing costs. This trend supports higher pricing and profitability for compliant films.

Leading manufacturers such as Coveris and POLIFILM, along with regional players, are investing in expanding production capacity and developing products aligned with evolving regulatory requirements. The Europe stretch film industry is transitioning toward environmentally responsible solutions, benefiting from innovation, regulatory support, and increasing customer preference for sustainable packaging options.

North America Stretch Films Market Trends

The North American stretch film market is expanding, driven by significant e-commerce penetration, advancements in pharmaceutical packaging, and modernization of the agricultural segment, creating diverse demand across logistics, food service, and specialty applications.

The United States, representing the majority of North American demand, experiences steady growth driven by e-commerce, which contributes a substantial share of retail sales and supports logistics packaging needs in fulfillment centers, third-party logistics operations, and distribution networks.

Pharmaceutical packaging is emerging as a major growth area, with manufacturers shifting toward sustainable stretch films to meet regulatory compliance and product protection needs while addressing brand sustainability commitments. The expanding cold-chain logistics sector, focused on refrigerated food distribution and temperature-controlled shipments, drives demand for vented and breathable stretch films that prevent condensation and preserve product integrity.

Regulatory initiatives in the United States, such as voluntary programs of the U.S. Environmental Protection Agency (EPA) and state-level extended producer responsibility (EPR) schemes, encourage the transition from virgin to recyclable and post-consumer recycled stretch film formulations, fostering sustainability while meeting market requirements.

Competitive Landscape

The global stretch films market structure is moderately consolidated, with major players such as Berry Global Group, Amcor plc, AEP Industries Inc., Intertape Polymer Group Inc., and Sigma Plastics Group leading through their extensive production capacities, technological advancements, and widespread global distribution networks.

These companies leverage advanced extrusion technologies and focus heavily on innovation in sustainability, including downgauging and bio-based films, to maintain their competitive advantage. Regional players are typically competing by offering more affordable products, localized services, and specialized film variants tailored to niche markets.

The competitive landscape is also shaped by strategic mergers, acquisitions, and capacity expansions, enabling leading manufacturers to reinforce their market positions while driving growth and responding to evolving consumer and regulatory demands.

Ongoing investments by other key players ensure that innovation in high-performance, recyclable, and bio-based films continues to accelerate, supporting the market’s robust outlook through 2035. This dynamic ecosystem fosters continuous product evolution aligned with environmental compliance, cost efficiency, and customer expectations, driving value across both commodity and premium stretch film segments.

Key Industry Developments

- In November 2025, Global Industrial launched the Mobile Robot Stretch Wrap Machine, a self-propelled, semi-autonomous solution designed to wrap irregular and oversized pallets directly on the floor. This innovative machine reduces forklift traffic by traveling to the load, enabling single-operator workflows and improving efficiency while reducing film consumption and waste through programmable film-tension control. The compact three-wheel design and front safety bumper, which stops movement on contact, make it suitable for busy warehouse and manufacturing environments, supporting safer, more sustainable, and cost-effective pallet wrapping operations.

- In October 2025, BioNatur Plastics introduced a European-manufactured biodegradable and 100% recyclable stretch wrap offered at the same cost as traditional non-biodegradable films, enabling shippers to enhance sustainability without additional logistics expenses. The biodegradable film fully decomposes in standard landfill conditions within eight to twelve years, unlike conventional stretch wrap that can persist for up to 1,000 years. The product contains a proprietary, food-safe organic polymer that promotes biodegradation without producing harmful microplastics, while maintaining the same handling and cargo protection performance as conventional films.

- In August 2025, Intec Bioplastics, Inc. rolled out a new customer incentive Buy Back Program targeting used stretch wrap film and cores to help customers comply with EPR legislation while reducing costs. The program addresses the environmental issue of over 250 million discarded stretch wrap cores in U.S. landfills annually, which cannot be recycled with standard cardboard due to material hardness and adhesives. Intec’s Hercules Bioflex Stretch Wrap Films, introduced in 2025, lead the North American market in sustainability, featuring APR-certified, recyclable, plant-based components.

Companies Covered in Stretch Films Market

- Berry Global Group, Inc.

- Intertape Polymer Group Inc.

- Scientex Berhad

- Sigma Plastics Group

- Anchor Packaging Inc.

- Paragon Films

- Coveris Holdings S.A

- Signode Industrial Group LLC

- Trioworld Group

- POLIFILM

- THE FROMM GROUP

- TG Group of Companies

- Inteplast Group

Frequently Asked Questions

The global stretch films market is projected to reach US$ 5.9 billion in 2025.

The market is driven by expanding e-commerce logistics infrastructure, increasing palletization needs, and rising adoption of sustainable films with post-consumer recycled content under global circular economy mandates.

The market is poised to witness a CAGR of 4.6% from 2025 to 2032.

Key market opportunities lie in the development of biodegradable and bio-based film formulations and the integration of smart packaging technologies enabling track-and-trace, sustainability, and value-added performance differentiation.

Berry Global Group, Amcor plc, AEP Industries Inc., and Intertape Polymer Group Inc. are the leading market players.