- Non-food Packaging

- Stretch Wrapper Market

Stretch Wrapper Market Size, Share, and Growth Forecast, 2026 - 2033

Stretch Wrapper Market by Machine Type (Rotary Arm, Robotic, Others), End-user (Food & Beverages, Pharmaceuticals, Others), Operation, and Regional Analysis for 2026 - 2033

Stretch Wrapper Market Size and Trends Analysis

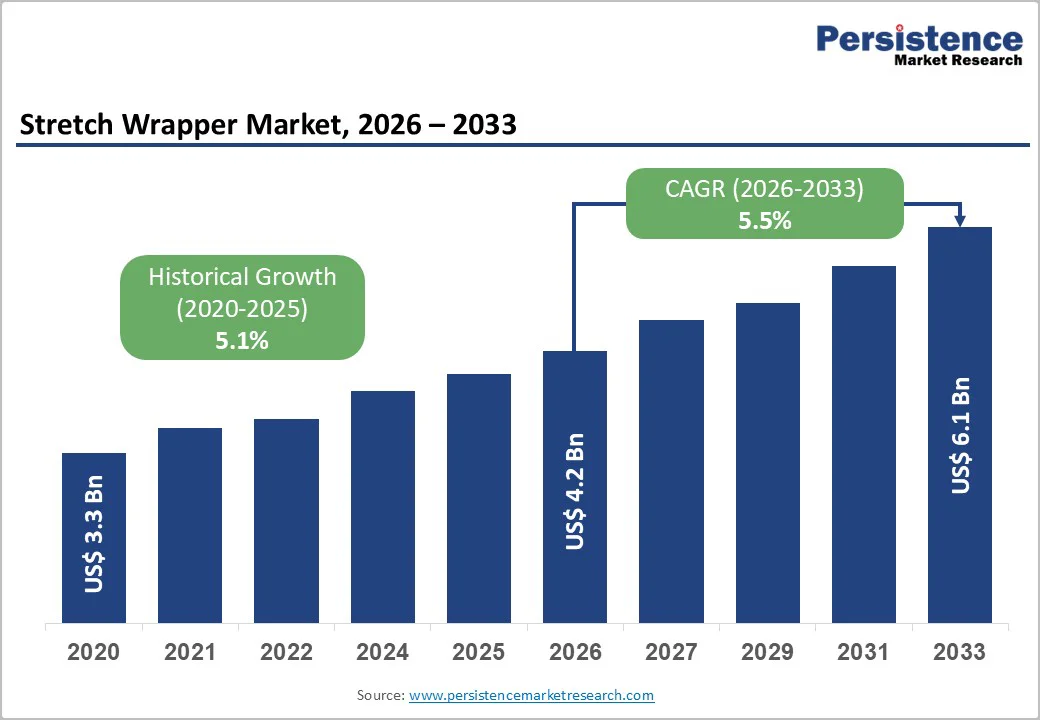

The global stretch wrapper market size is likely to be valued at US$4.2 billion in 2026. It is expected to reach US$6.1 billion by 2033, growing at a CAGR of 5.5% between 2026 and 2033, driven by increasing warehouse automation, expanding food and beverage packaging volumes, and the need for higher throughput and improved film efficiency.

Investments in robotic and rotary-arm high-speed platforms are accelerating across large distribution centers, while sustainability pressures are encouraging the adoption of high-yield stretch films and system upgrades. Market concentration remains moderate, with global OEMs leading innovation and regional players strengthening local distribution and aftermarket services.

Key Industry Highlights

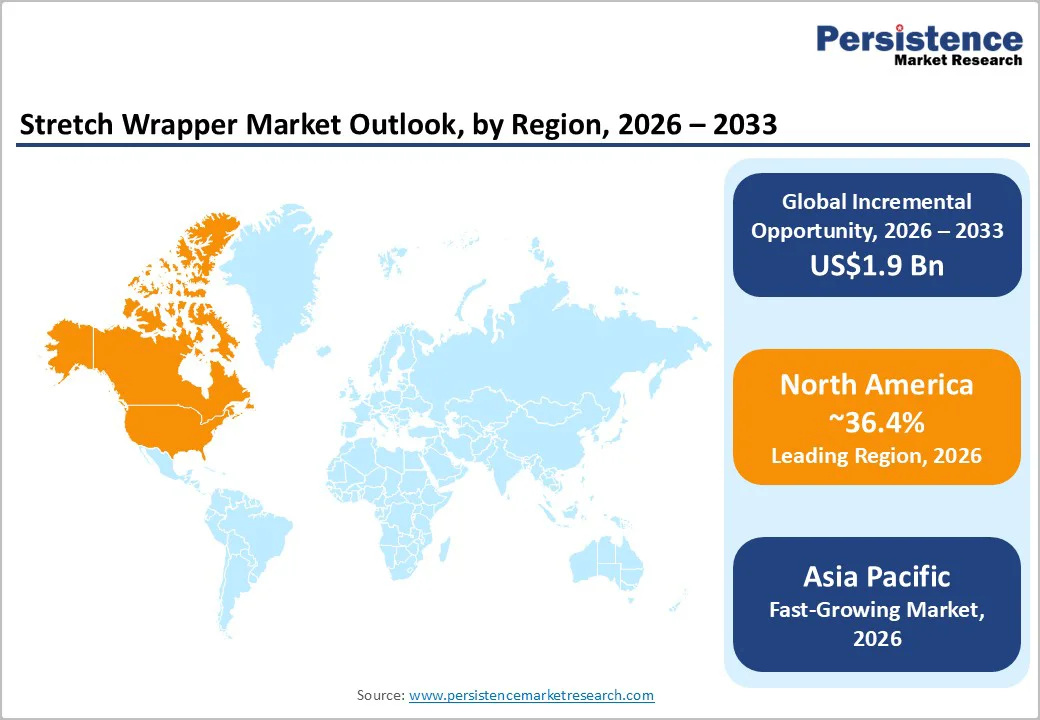

- Leading Region: North America is projected to account for approximately 36.4% of market share, driven by high automation maturity, extensive food and beverage manufacturing, and advanced logistics infrastructure in the U.S.

- Fastest-growing Region: Asia Pacific, to register the highest growth rate due to the rapid expansion of manufacturing capacity, strong e-commerce growth, and rising adoption of semi-automatic and automatic stretch wrappers across China, India, and Southeast Asia.

- Investment Plans: Ongoing investments focus on warehouse automation, film-efficient technologies, and robotic stretch wrapping systems, with capital allocation increasingly directed toward retrofitting existing facilities to reduce film usage and improve load stability, particularly in food, beverage, and pharmaceutical distribution.

- Dominant Machine Type: Rotary-arm stretch wrappers are expected to account for approximately 49.6% of revenue share, supported by their suitability for high-throughput operations and their ability to handle unstable pallet loads in automated environments.

- Leading End-user: The food and beverage segment is estimated to account for around 40.2% revenue share, driven by high pallet volumes, strict hygiene requirements, and sustained investments in automated packaging and palletizing lines.

| Key Insights | Details |

|---|---|

| Stretch Wrapper Market Size (2026E) | US$4.2 Bn |

| Market Value Forecast (2033F) | US$6.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Automation and E-Commerce Warehouse Expansion

Automation of end-of-line and warehouse packaging represents the most significant demand driver for stretch wrappers. Rapid growth in e-commerce, combined with rising order volumes and shorter fulfillment timelines, is forcing distribution centers to replace manual wrapping with semi-automatic, automatic, and robotic systems capable of continuous operation.

These systems integrate seamlessly with conveyor and palletizing lines, improving throughput and reducing labor dependency.

As warehouse operators prioritize uptime and operational efficiency, replacement cycles for legacy turntable machines are accelerating. Capital expenditure is increasingly directed toward robotic and rotary-arm systems that deliver consistent load containment, higher wrapping speeds, and remote monitoring capabilities. These structural shifts directly underpin the projected market growth trajectory.

Food and Beverage Demand

The food and beverage sector remains the largest end-user segment for stretch wrappers and remains the primary driver of volume growth. Food and beverage supply chains require reliable load stability, hygienic handling, and high-speed palletization, making rotary-arm and conveyor-integrated systems well-suited to this sector.

Global growth in processed foods, bottled beverages, and convenience formats supports steady demand for pallet stabilization and protective wrapping. With food and beverage accounting for approximately 40.2% of market share, even incremental increases in production volumes translate into meaningful demand for new equipment and higher film consumption per pallet. Growth is especially pronounced in export-oriented manufacturing regions.

Sustainability and Film-efficiency Technologies

Sustainability objectives and cost-reduction pressures are driving investments in advanced film-efficiency technologies. Modern stretch wrappers increasingly incorporate high-yield pre-stretch systems, multi-zone tension control, and software-driven wrap recipes that reduce film usage by 20-40%, depending on load characteristics.

Buyers evaluate return on investment through combined savings in film consumption, waste handling, and energy use. Corporate sustainability targets and evolving packaging waste regulations are accelerating the replacement of older machines with systems optimized for material efficiency and performance monitoring. This shift is raising average selling prices for advanced equipment while delivering measurable reductions in operating costs for end users.

Barrier Analysis - High Capital Cost and Long Procurement Cycles

Automatic and robotic stretch wrappers require significant upfront investment and often involve integration with conveyors, palletizers, and warehouse control systems. Smaller manufacturers and third-party logistics providers frequently delay purchases, favoring semi-automatic machines to preserve capital.

Limited access to financing and conservative equipment replacement strategies slow the near-term adoption of high-end systems. Sensitivity analysis indicates that increases in interest rates or equipment costs can extend payback periods by six to twelve months, leading to deferred purchasing decisions in cost-constrained projects.

Supply Chain and Component Lead Times

Periodic supply-chain disruptions, particularly for electronic components such as PLCs, sensors, and servo motors & drives, have extended manufacturing lead times for stretch wrappers. Delivery uncertainty can push buyers toward simpler or locally sourced machines.

For OEMs and integrators, component shortages increase production costs, complicate scheduling, and elevate warranty risks. These challenges require proactive mitigation through dual-sourcing strategies and higher inventory buffers, increasing working capital requirements.

Opportunity Analysis - Retrofit and Service-led Growth

A significant opportunity exists in upgrading the installed base of legacy turntable machines with film-optimization modules, remote diagnostics, and enhanced safety features. Service agreements and performance-based pricing models allow customers to convert capital expenditure into predictable operating costs.

Retrofitting even 20-30% of installed small and mid-scale fleets in developed markets represents an incremental revenue opportunity equivalent to approximately 5-8% of annual new-machine sales, while strengthening long-term customer relationships.

Automation Leapfrogging Opportunities in Emerging Markets

Emerging markets in the Asia Pacific and parts of Latin America present strong potential for leapfrog adoption of automated rotary-arm and robotic stretch wrappers. As labor cost advantages narrow and supply-chain resilience becomes a strategic priority, manufacturers are increasingly open to automation investments.

Targeted financing programs, local assembly partnerships, and distributor-led service models can accelerate penetration. Capturing even a modest share of new warehouse automation projects in high-growth economies could materially enhance global market growth and regional revenue mix.

Category-wise Analysis

Machine Type Insights

Rotary-arm stretch wrappers are expected to be the leading machine type, accounting for approximately 49.6% of revenue. These systems apply stretch film around a stationary pallet. At the same time, the wrap arm rotates, making them particularly effective for tall, unstable, or lightweight loads commonly used in beverage, bottled water, dairy, and packaged food operations.

The stationary load configuration minimizes the risk of product shift or collapse, which is critical for high-speed production lines handling glass bottles, liquid-filled containers, and stacked cartons.

Rotary-arm machines support high wrapping speeds and continuous operation, and they integrate seamlessly with conveyorized palletizing systems in large manufacturing and distribution facilities.

In beverage bottling plants and large food processing facilities, rotary-arm systems are widely deployed at the end of fully automated lines to maintain consistent load containment at high throughput levels. Their ability to operate reliably in 24/7 production environments reinforces their dominance in enterprise-scale installations where uptime and wrapping consistency are operational priorities.

Robotic stretch wrappers are the fastest-growing machine type, driven by operational flexibility, compact footprints, and declining costs of industrial robotic components. Unlike traditional turntable or rotary systems, robotic wrappers move around a stationary pallet, enabling them to accommodate mixed pallet sizes, irregular load shapes, and frequent SKU changes without mechanical adjustments. This makes robotic systems highly attractive to contract packers, third-party logistics providers, and distribution centers handling diverse product profiles.

Robotic stretch wrappers are increasingly adopted in e-commerce fulfillment centers and multi-client warehouses, where flexibility and space efficiency are critical.

Advancements in safety fencing alternatives, vision-based load detection, and software-driven wrap pattern optimization have expanded their use beyond niche applications. As warehouse operators seek scalable automation solutions that can be redeployed or expanded with minimal infrastructure changes, robotic wrappers are expected to continue outpacing the growth of traditional machine formats.

End-user Insights

Food and beverage is estimated to lead, accounting for approximately 40.2% of revenue. High pallet throughput, strict hygiene requirements, and continuous investment in automated packaging and palletizing lines support this dominance.

Stretch wrappers are extensively used in bottling plants, dairy processing facilities, frozen food warehouses, and beverage distribution centers to ensure load stability and product protection during storage and transportation.

Rotary-arm and turntable machines are commonly deployed to handle standardized pallet loads such as beverage cases, cartons, and shrink-wrapped multipacks. Growth in packaged and processed food consumption, particularly in fast-urbanizing and export-driven economies, continues to generate consistent demand for reliable and high-speed stretch wrapping solutions.

Pharmaceuticals represent the fastest-growing end-use segment due to tightening regulatory standards, increased serialization requirements, and rapid expansion of cold-chain logistics. Pharmaceutical manufacturers and distributors require precise load containment to protect high-value and temperature-sensitive products throughout the supply chain.

Automatic and robotic stretch wrappers are increasingly deployed in pharmaceutical packaging and distribution facilities, often integrated with track-and-trace systems, barcode verification, and quality-control checkpoints.

These systems help maintain compliance, reduce contamination risk, and ensure consistent pallet integrity during long-distance and temperature-controlled transportation. Rising global demand for vaccines, biologics, and specialty medicines is further accelerating the adoption of stretch wrappers in this segment.

Regional Insights

North America Stretch Wrapper Market Trends - Automation-Led Palletizing and Film-Efficiency Upgrades

North America is projected to represent the largest regional market, accounting for approximately 36.4% of global stretch wrapper demand, with the U.S. leading adoption. The region benefits from a highly developed food and beverage manufacturing base, extensive third-party logistics (3PL) networks, and advanced warehouse automation maturity.

Large consumer goods producers and retailers continue to invest in high-speed palletizing and stretch wrapping systems to support omnichannel distribution. For example, major U.S. retailers and e-commerce operators have expanded automated fulfillment centers, increasing demand for rotary-arm and fully automatic stretch wrappers integrated with conveyors and palletizers.

Growth is further supported by retrofit demand as older turntable machines are replaced with film-efficient systems that reduce material usage. Sustainability initiatives, including downgauging stretch film and reducing plastic waste, encourage the adoption of pre-stretch technologies offered by suppliers such as Lantech, Signode, and ProMach.

Regulatory oversight from agencies such as OSHA and UL influences standards for machine safety, guarding, and ergonomics, prompting manufacturers to invest in advanced control systems and safety-certified automation. Warehouse modernization programs across food, beverage, and pharmaceuticals continue to reinforce North America’s leadership position in high-performance stretch wrapping solutions.

Europe Stretch Wrapper Market Trends - Industry 4.0 Compliance and Energy-Efficient Wrapping Systems

Europe is a mature but stable stretch wrapper market, characterized by high automation density, strong engineering standards, and regulatory harmonization across the EU. Germany, the U.K., France, and Spain account for the majority of regional demand, supported by well-established food processing, beverage bottling, and industrial manufacturing sectors.

European manufacturers place strong emphasis on energy efficiency, precise load containment, and digital monitoring, aligning with Industry 4.0 initiatives. OEMs such as Robopac, Fromm, and Mosca have continued to enhance machine connectivity and film optimization features to meet these requirements.

Sustainability regulations under EU packaging and waste directives play a critical role in shaping purchasing decisions. End users increasingly favor stretch wrappers that support recyclable films, reduce film consumption, and provide data-driven reporting on material usage.

High labor costs across Western Europe further accelerate investment in fully automatic and robotic stretch wrapping systems, particularly in logistics hubs serving cross-border trade. Compliance with harmonized CE safety standards also drives consistent demand for equipment upgrades, ensuring Europe remains a steady contributor to global market revenues despite slower overall volume growth compared to the Asia Pacific.

Asia Pacific Stretch Wrapper Market Trends - E-Commerce Expansion and Scalable Automation Adoption

Asia Pacific is the fastest-growing regional market for stretch wrappers, driven by expanding manufacturing capacity, rising packaged food consumption, and rapid growth in e-commerce and contract logistics. China leads the region in volume, supported by large-scale food processing, consumer goods production, and export-oriented manufacturing.

Domestic and international suppliers have expanded local production and service capabilities to address demand for high-throughput automatic systems in Chinese distribution centers. Japan, by contrast, prioritizes high-precision and compact stretch wrappers, reflecting space constraints and a strong focus on operational efficiency and reliability.

India and Southeast Asian markets such as Indonesia, Vietnam, and Thailand are witnessing growing adoption of semi-automatic and entry-level automatic stretch wrappers, particularly among small and mid-sized manufacturers upgrading from manual pallet wrapping. Expansion of regional e-commerce platforms and cold-chain logistics has increased demand for consistent load containment and reduced product damage.

While regulatory frameworks vary widely across the Asia Pacific, this diversity creates selective opportunities for suppliers offering scalable, cost-efficient systems tailored to local operating conditions. As automation penetration deepens, the region is expected to contribute the highest incremental growth to the global stretch wrapper market over the forecast period.

Competitive Landscape

The global stretch wrapper market is moderately concentrated. A limited number of global OEMs dominate the high-spec automatic and robotic segments, while numerous regional manufacturers compete in semi-automatic and entry-level categories. Competition in premium segments is based on technology differentiation, integration capability, and service reach, while price competition is more pronounced in lower-end offerings.

Recent strategic activity has focused on high-speed product launches, film-efficiency enhancements, modular automation upgrades, and consolidation through acquisitions. OEMs are strengthening portfolios through integrated solutions and expanding aftermarket capabilities to increase recurring revenue.

Leading companies prioritize innovation in film efficiency, expansion of service and retrofit offerings, and geographic growth through distributor and partner networks. Integration of robotics, data analytics, and flexible financing models is increasingly central to competitive positioning.

Key Industry Developments

- In September 2025, Signode unveiled the Octopus Prestige stretch wrapper at PACK EXPO 2025, featuring a new Double-S film carriage system that enhances wrapping speed and reduces film use, reinforcing the company’s leadership in automated packaging solutions.

- In September 2025, Lantech showcased its SL Automatic Stretch Wrapper with an automatic roll-change system and LeanWrap technologies at Drinktec 2025 in Munich and PackExpo 2025 in Las Vegas, emphasizing improved operational efficiency and sustainability for beverage and general packaging lines.

Companies Covered in Stretch Wrapper Market

- Signode Industrial Group

- Robopac (Aetna Group)

- Lantech

- ARPAC

- Wulftec

- ProMach (including related brands)

- FROMM Packaging Systems

- Aetna Group

- Strapping Systems

- Phoenix Wrappers

- ORION Packaging Systems

- Cousins Packaging

- Transpak

- Apex Packaging Equipment

- Panther Industries

- Spartanics

- Lenk Engineering

- AutoShrink

- B Pack (B&R Industrial)

- ITW (Industrial and Scientific division)

Frequently Asked Questions

The global stretch wrapper market size is expected to be valued at US$4.2 billion in 2026.

By 2033, the stretch wrapper market is forecast to reach US$6.1 billion.

Key trends include increasing adoption of fully automatic and robotic stretch wrappers, integration with conveyorized palletizing systems, growing focus on film reduction and sustainability, and rising demand from e-commerce and cold-chain logistics.

By machine type, rotary-arm stretch wrappers lead the market, supported by their high-speed performance, ability to handle unstable loads, and suitability for high-volume food and beverage operations.

The market is projected to grow at a CAGR of 5.5% between 2026 and 2033.

Major players with strong global portfolios include Lantech, Robopac (Aetna Group), Signode, ProMach, and FROMM Packaging Systems.