- Specialty & Fine Chemicals

- Specialty Lubricant Market

Specialty Lubricant Market Size, Share, and Growth Forecast, 2026 – 2033

Specialty Lubricant by Base Oil Type (Synthetic Oil, Mineral Oil, Bio-based Oil), Additive Technology (Anti-wear, Anti-friction, Others), Application (Automotive & Transport, Industrial Machinery, Metalworking), and Regional Analysis 2026 – 2033

Specialty Lubricant Market Size and Trends Analysis

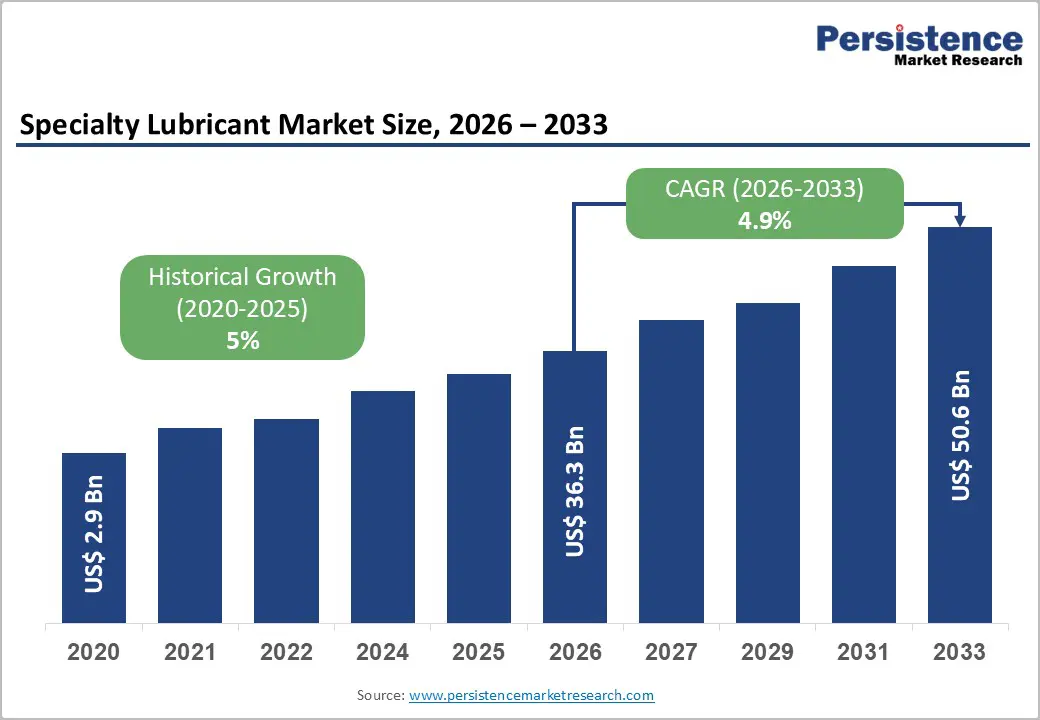

The global specialty lubricant market size is likely to be valued at US$36.3 billion in 2026 and is expected to reach US$50.6 billion by 2033, growing at a CAGR of 4.9% during the forecast period from 2026 to 2033, driven by increasing industrial automation and the rising demand for high-performance lubricants across the automotive and manufacturing sectors.

Market expansion is further supported by the growing requirement for lubricants capable of performing under extreme operating conditions, including ultra-high temperatures and highly corrosive environments, conditions that are becoming more prevalent in advanced aerospace and heavy manufacturing applications. Regulatory emphasis on sustainable and environmentally friendly formulations is also accelerating market development, with Asia Pacific emerging as the leading regional market.

Key Industry Highlights:

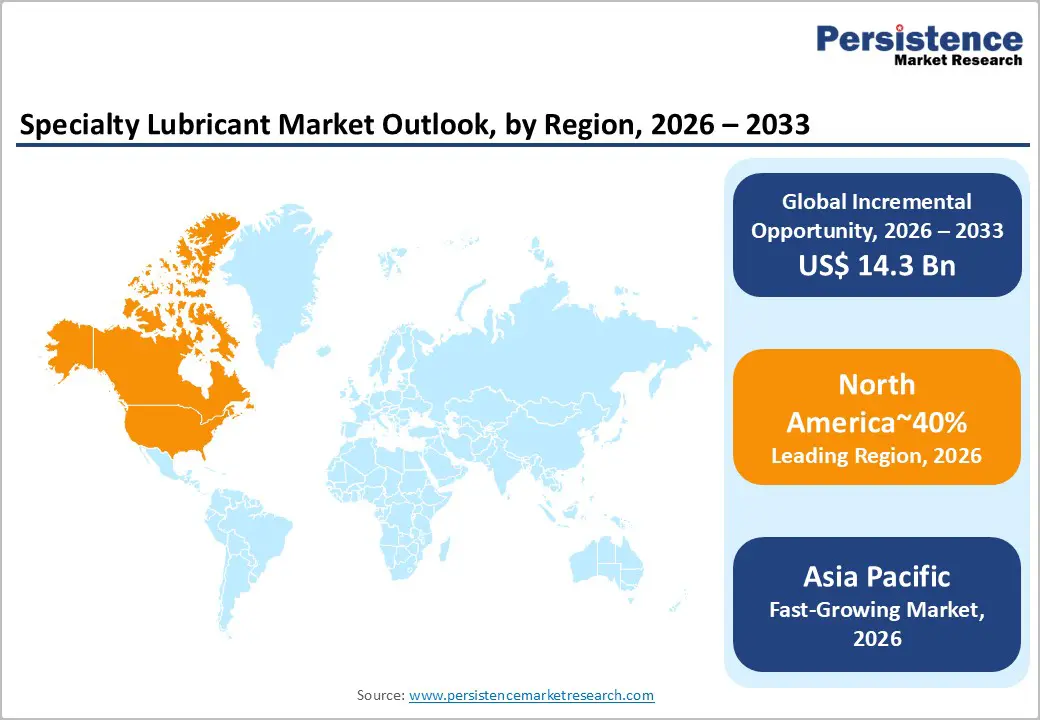

- Leading Region: North America, with approximately 40% share, supported by advanced automotive, aerospace, and industrial sectors, strong R&D capabilities, and established lubricant manufacturing infrastructure.

- Fastest-growing Region: Asia Pacific, fueled by large-scale industrialization, expanding vehicle fleets, and accelerated infrastructure development.

- Leading Base Oil Type: Mineral oils, to account for approximately 46% share, benefiting from cost-effectiveness, established supply chains, and broad compatibility with traditional additive packages.

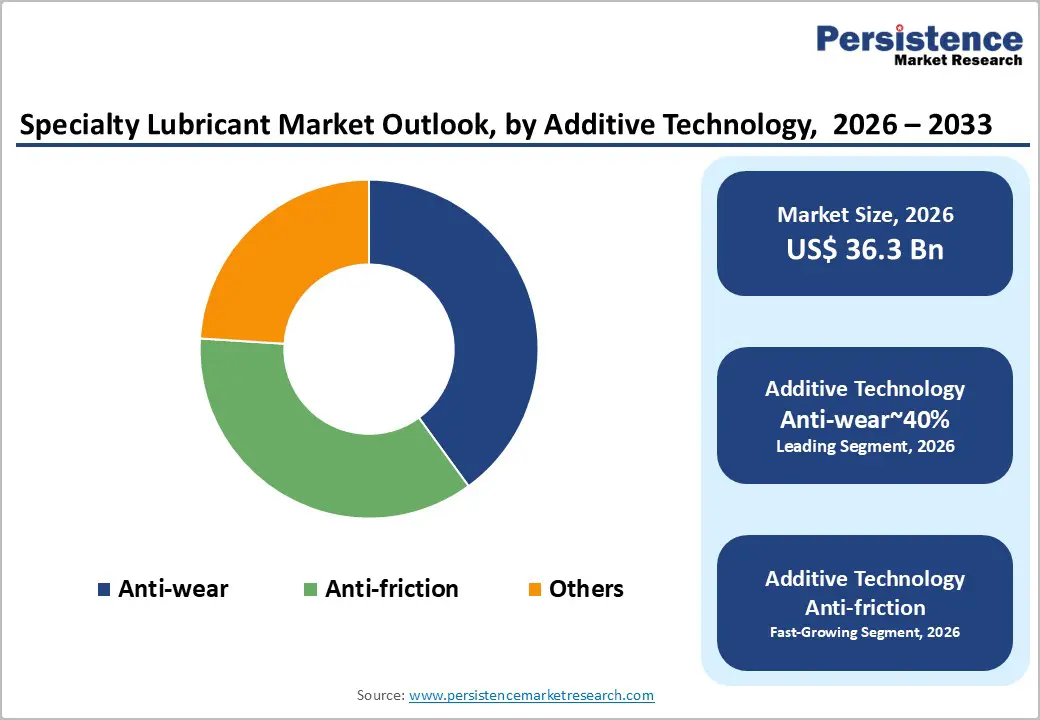

- Leading Additive Technology: Anti-wear additives, to hold approximately 40% share, critical for reducing component degradation, friction, and maintenance costs in engines and industrial machinery.

| Key Insights | Details |

|---|---|

| Specialty Lubricant Market Size (2026E) | US$36.3 Bn |

| Market Value Forecast (2033F) | US$50.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Expansion of the Automotive and Electric Vehicle Sector

The expansion of global automotive production and the structural transition toward electrified powertrains are reshaping demand profiles across the specialty fluids value chain. Electrification alters lubrication requirements by shifting thermal loads, operating temperatures, and component architectures away from internal combustion paradigms toward battery systems, electric motors, and power electronics. This transition elevates the relevance of dielectric lubricants and advanced thermal management fluids capable of maintaining insulation performance, material compatibility, and heat dissipation under higher electrical stress. As vehicle platforms evolve, fluid specifications become embedded within OEM design standards, reinforcing upstream demand for application-specific chemistries aligned with new drivetrain architectures.

At the market structure level, regulatory emissions targets and fleet electrification mandates accelerate platform turnover cycles, compressing qualification timelines for new fluid formulations while raising compliance burdens around safety, recyclability, and chemical stewardship. Lower-viscosity synthetic fluids are increasingly specified to reduce energy losses and thermal degradation, shifting cost structures toward higher-performance base stocks and additive packages. These dynamics reallocate margin pools toward formulation expertise and materials science capabilities, while constraining commoditized lubricant segments that lack compatibility with emerging electric drivetrain and battery thermal management requirements.

Increased Industrial Automation and Industry 4.0

The acceleration of industrial automation and Industry 4.0 adoption is structurally increasing reliance on high-precision motion systems across advanced manufacturing value chains. Robotics, automated assembly lines, and digitally orchestrated production cells operate under continuous-duty cycles with tighter tolerances, higher duty frequencies, and elevated thermal and mechanical stress on bearings, gears, and linear guides. These operating conditions shift lubrication requirements toward specialty greases and fluids with superior anti-friction performance, shear stability, and long service life to sustain uptime within just-in-time production environments. As automation density rises, lubrication performance becomes a critical input to equipment availability, throughput stability, and defect rate control.

At the market level, automation-led productivity mandates reallocate cost sensitivity from unit lubricant pricing toward lifecycle reliability and maintenance interval extension. Unplanned stoppages carry disproportionate economic penalties in digitally synchronized factories, embedding lubricant performance within broader operational risk management frameworks. Regulatory regimes governing workplace safety, machine reliability, and chemical stewardship further shape formulation standards and supplier qualification thresholds. These dynamics structurally favor advanced lubricant chemistries engineered for sealed-for-life components and predictive maintenance regimes, while compressing demand for generic industrial oils that lack compatibility with high-speed, high-precision automated manufacturing architectures.

Barrier Analysis – Established Brand Inertia and Risk Aversion

Procurement behavior in safety-critical and mission-critical sectors is structurally shaped by risk minimization imperatives, reinforcing strong path dependence toward incumbent materials and qualified product lines. In aerospace, nuclear, and other high-consequence operating environments, qualification regimes, certification protocols, and long-duration validation cycles embed conventional products within maintenance standards and operational manuals. The cost of requalification, coupled with the liability exposure associated with performance deviations, elevates the switching barrier for newer specialty formulations. This institutionalized conservatism constrains the diffusion of innovation even where alternative products demonstrate superior technical performance under controlled conditions.

At the value-chain level, incumbent advantage is reinforced by long-term service contracts, embedded vendor relationships, and OEM specifications that lock materials into equipment warranties and maintenance schedules. Regulatory oversight and audit requirements further increase documentation and testing burdens for alternative suppliers, elongating adoption timelines and increasing pre-commercialization costs. These dynamics concentrate market access among established brands with extensive certification portfolios and installed-base credibility, structurally slowing penetration of novel specialty solutions. As a result, innovation cycles face delayed revenue realization, and addressable volumes in critical-use segments remain constrained by institutional risk frameworks rather than purely by technical readiness.

Opportunity Analysis – Bio-based Lubricant Expansion

Bio-based lubricants represent an expanding opportunity within industrial fluids markets as sustainability mandates, green procurement frameworks, and lifecycle impact criteria increasingly influence material selection across manufacturing, transport, and infrastructure operations. Policy incentives embedded within agricultural and renewable materials programs structurally lower input cost barriers for bio-oil feedstocks, while public-sector and enterprise procurement policies embed environmental performance thresholds into tendering processes. Superior biodegradability characteristics reposition bio-lubricants within environmentally sensitive applications such as marine operations, forestry equipment, and water-adjacent industrial assets, where leakage risk and environmental compliance materially affect operating licenses and liability exposure. These dynamics shift lubricant demand from purely performance-led criteria toward blended performance–compliance evaluation frameworks.

From a value-chain perspective, expansion of bio-based lubricants redistributes margin pools toward feedstock sourcing, esterification, and formulation capabilities capable of delivering stable performance across variable agricultural inputs. Regulatory scrutiny over land-use practices and supply-chain traceability increases compliance costs and elevates certification requirements, influencing sourcing strategies and supplier qualification. Processing economics remain sensitive to feedstock price volatility and conversion efficiency, shaping cost curves relative to mineral and synthetic alternatives. As green procurement coverage expands, bio-lubricants transition from niche compliance solutions toward structurally embedded inputs within regulated industrial lubrication portfolios.

Booming Renewable Energy Infrastructure

The expansion of offshore renewable energy infrastructure is creating a structurally attractive niche for specialty lubrication solutions engineered for high-load, low-access operating environments. Offshore wind installations impose severe mechanical and environmental stress on drivetrain, gearbox, and bearing systems, elevating the importance of lubricant formulations that sustain viscosity stability, corrosion resistance, and long service intervals under saline exposure and variable thermal loads. As turbine platforms scale in size and power density, lubrication performance becomes integral to asset availability and maintenance planning, embedding specialty lubricants within the reliability architecture of offshore generation assets. This shifts lubricant demand toward application-specific, high-margin formulations aligned with extended maintenance cycles.

At the value-chain level, offshore deployment increases the economic penalty of unplanned service events, reallocating cost sensitivity from upfront lubricant pricing toward lifecycle performance and failure risk mitigation. Regulatory oversight around offshore environmental protection heightens scrutiny on leakage resilience and biodegradability profiles, influencing formulation requirements and supplier qualification. Supply chains must support offshore logistics, long-term storage stability, and predictable replenishment cycles, increasing barriers to entry for commoditized products. These dynamics structurally favor specialty lubricant providers with validated offshore-grade chemistries and the ability to integrate performance assurance into renewable asset maintenance ecosystems.

Category–wise Analysis

Base Oil Type Insights

Mineral base oil is projected to dominate the specialty lubricants market, accounting for approximately 46% share in 2026, underpinned by its entrenched installed base across legacy industrial fleets, heavy equipment, and process industries. Adoption remains anchored by cost efficiency, additive compatibility, and qualification readiness, with operators prioritizing standardization, supply security, and scale economics in high-volume environments such as mining, construction, cement, steel, and marine operations. Ongoing platform evolution, including Group III+ hydrocracked mineral bases, GTL-derived ultra-clean stocks, and re-refined circular base oils, continues to reinforce replacement cycles and utilization intensity. Vendors such as ExxonMobil, Shell, Chevron, and SK Enmove are expanding portfolios with premium mineral-based platforms to lock in OEM approvals, distributor networks, and long-term service contracts. This combination of mature infrastructure, ecosystem lock-in, and predictable demand sustains mineral base oil dominance within structured industrial lubrication workflows.

Synthetic base oil is expected to be the fastest-growing segment, driven by performance gaps in mineral oils across EV thermal management, wind turbine gearboxes, aerospace systems, and high-precision manufacturing. Growth is being catalyzed by metallocene PAOs, advanced synthetic esters, and dielectric e-fluids, which materially improve thermal stability, shear resistance, and energy efficiency. Accelerating adoption is supported by condition-based monitoring, smart fluid diagnostics, and digital maintenance planning, lowering operational friction for first-time industrial adopters. Companies including Castrol (BP), Klüber Lubrication, Fuchs Petrolub, and Dow are scaling synthetic platforms and application-specific product lines to capture early-cycle demand and embed switching costs.

Additive Technology Insights

Anti-wear additives are expected to dominate, accounting for approximately 40% share, underpinned by their entrenched role in protecting high-torque drivetrains, heavy-duty industrial gearboxes, mining equipment, and precision robotics. Adoption remains anchored by wear mitigation, qualification readiness with OEM specifications, and reliability under thin-film lubrication regimes, with operators prioritizing uptime, extended drain intervals, and standardized additive packages across large fleets. Ongoing platform evolution, including ashless anti-wear chemistries, temperature-activated molecular layer deposition systems, and synergistic OFM–AW super-blends, continues to reinforce replacement cycles and utilization intensity. Vendors such as Lubrizol, Afton Chemical, Infineum, and BASF are expanding additive platforms and bundled formulations to lock in OEM approvals, global blending partnerships, and long-term service contracts. This combination of mature infrastructure, ecosystem lock-in, and predictable demand sustains segment dominance in high-load industrial workflows.

Antifriction additives (Friction Modifiers) are expected to be the fastest-growing segment, driven by energy-efficiency mandates, EV range optimization, and performance gaps of legacy lubrication under ultra-low-viscosity regimes. Growth is being catalyzed by advanced organic friction modifiers, soluble molybdenum complexes, polymeric thin-film modifiers, and emerging ionic-liquid systems, which materially improve drag reduction, stick-slip control, and micro-pitting resistance. Accelerating adoption is supported by AI-enabled formulation optimization, co-engineering with low-viscosity synthetic base oils, and condition-based energy monitoring, lowering operational friction for first-time adopters. Companies including Vanderbilt Chemicals, Croda International, Evonik, and Adeka are scaling new friction-modifier platforms to capture early-cycle demand and embed switching costs.

Regional Insights

North America Specialty Lubricant Market Trends

North America is anticipated to remain the leading region, with an expected share of around 40% of global revenue in 2026. This leadership is primarily anchored in the region’s structurally strong industrial base, high technology intensity, and early adoption of high-performance synthetic and semi-synthetic formulations across automotive, industrial, and energy applications. The U.S. is expected to continue setting the demand trajectory through sustained activity in advanced manufacturing, shale oil and gas operations, and data-intensive infrastructure such as hyperscale data centers, all of which require precision, high-stability lubricant solutions. Canada complements this position through mining, energy, and heavy industrial usage, while Mexico increasingly supports the regional ecosystem via automotive and electronics manufacturing supply chains.

Major suppliers such as ExxonMobil, Chevron, Shell (via Pennzoil and Quaker State), FUCHS, and Klüber Lubrication are likely to focus on higher-margin niches, including metalworking fluids, electric vehicle fluids, and thermal management liquids for electronics and data centers. Investment momentum around re-refining, advanced additive systems, and application-specific formulations suggests the region’s growth profile will be driven by value density and performance requirements rather than commoditized demand. Overall, North America is expected to lead not only in scale but also in specification complexity, reinforcing its position as the reference market for premium and specialty lubricant technologies.

Europe Specialty Lubricant Market Trends

Europe represents a stable and steady specialty lubricants market, functioning as a global reference point for high-value formulation, application-specific engineering, and technology transfer. Demand is expected to remain anchored in premiumization rather than volume expansion, with industrial users prioritizing performance longevity, energy efficiency, and application-critical reliability. The region’s position as a “global R&D lab” is reflected in the way advanced formulations are developed, validated with OEMs, and then diffused into other regions. FUCHS and TotalEnergies are increasingly positioning circular and re-refined base oil portfolios as premium industrial solutions rather than cost substitutes, while Klüber Lubrication continues to scale ultra-specialized greases for wind turbines, robotics, and high-load bearings used in European manufacturing clusters.

High-performance mobility platforms from Audi, BMW, and Porsche are accelerating the adoption of dedicated e-fluids and thermal management lubricants, while Airbus and Rolls-Royce continue to drive demand for extreme-condition synthetics in aerospace and turbine applications. Across factories, the shift toward automation and longer maintenance cycles is increasing uptake of long-life specialty greases and condition-optimized fluids, often specified directly by OEMs. As a result, Europe is expected to sustain its influence through formulation leadership and specification-setting power, positioning the region as a steady, high-value market that shapes global specialty lubricant standards rather than competing on scale.

Asia Pacific Specialty Lubricant Market Trends

Asia Pacific functions as the fastest growing region for specialty lubricants, driven by scale-intensive industrialization, expanding mobility fleets, and rapid infrastructure deployment. The region combines volume growth with accelerating product sophistication as OEM standards tighten and end users shift from basic mineral oils toward application-specific synthetics and semi-synthetics. Manufacturing expansion across heavy industry, automotive assembly, electronics, and renewables underpins structurally rising demand for hydraulic fluids, process oils, thermal management fluids, and EV-compatible lubricants. Product strategies increasingly emphasize low-viscosity formulations for efficiency compliance, long-drain fluids for fleet economics, and specialty greases for wind, mining, and automated manufacturing lines.

Market momentum is reinforced by capacity localization, regulatory tightening, and technology diffusion across the regional value chain. Investment in localized lubricant and base oil production reduces import dependence while enabling faster customization for domestic OEM specifications. China and India anchor regional volume growth through manufacturing scale, vehicle parc expansion, and infrastructure programs, while advanced industrial users accelerate adoption of predictive maintenance, fluid analytics, and condition-based lubrication practices. Competitive dynamics are defined by strong regional champions such as Sinopec, PetroChina, IOCL, and HPCL alongside global majors leveraging technology transfer, co-development with OEMs, and premium product differentiation to capture value in high-growth end-use segments.

Competitive Landscape

The global industrial lubricants market is moderately consolidated, led by global energy and specialty majors such as Shell, ExxonMobil, TotalEnergies, Chevron, BP (Castrol), and Fuchs, which collectively shape pricing benchmarks, product standards, and supply reliability through worldwide production and distribution networks. These players matter because their scale, long-standing OEM partnerships, and application engineering capabilities position them as preferred suppliers across manufacturing, mining, energy, and heavy industry. While leadership is concentrated at the top, competitive intensity persists as specialty formulators and regional blenders retain influence in high-margin, application-specific niches.

Competitive positioning is increasingly defined by R&D depth, digital service integration, and lifecycle-oriented service models, with leaders moving beyond product sales toward condition monitoring, predictive maintenance, and “lubrication-as-a-service” offerings. Industry behavior reflects sustained portfolio upgrading, technology-led differentiation, and selective consolidation, while niche specialists continue to defend fragmented segments through deep domain expertise and customized formulations. This dynamic points to steady top-end consolidation alongside durable fragmentation in specialty applications.

Key Industry Highlights:

- In February 2026, FUCHS debuted an immersion cooling fluid for AI data centers. This development addressed the high thermal management demands of high-performance computing and positioned the company at the forefront of a niche technological segment.

- In January 2026, ExxonMobil and BYD partnered on hybrid lubricant technology. This collaboration targeted the specialized requirements of hybrid electric vehicles and ensured engine longevity and efficiency across diverse driving conditions.

- In November 2025, Shell topped the global lubricants market for the 19th consecutive year. This continued leadership enabled Shell to leverage its extensive scale to advance R&D in specialty segments, particularly in the APAC region.

- In October 2025, Shell India unveiled India’s first Shell-branded synthetic gear oil in the Spirax category. The Shell Spirax S4 GX 75W-90 delivered enhanced gearbox protection and smoother gear shifts for passenger cars and light commercial vehicles.

Companies Covered in Specialty Lubricant Market

- ExxonMobil Corporation

- Shell plc

- TotalEnergies SE

- Chevron Corporation

- BP p.l.c. (Castrol)

- FUCHS SE

- Klüber Lubrication (Freudenberg Group)

- Dow Inc. (Molykote)

- BASF SE

- China Petroleum & Chemical Corporation (Sinopec)

- PetroChina Company Limited

- Idemitsu Kosan Co., Ltd.

- ENEOS Corporation

- Petronas (Petroliam Nasional Berhad)

- Valvoline Inc.

- Phillips 66 Company

- Quaker Houghton

Frequently Asked Questions

The global specialty lubricant market is projected to be valued at US$36.3 billion in 2026 and is expected to reach US$50.6 billion by 2033, driven by rising industrial automation, the expansion of electric vehicles, and demand for high-performance fluids in extreme operational conditions.

The transition to electric powertrains creates new demand for dielectric and high-performance thermal management fluids for batteries and motors. This shift, alongside continuous automotive production, requires application-specific lubricants that meet stricter performance and efficiency standards, moving the market away from generic formulations.

The specialty lubricant market is forecast to grow at a CAGR of 4.9% from 2026 to 2033, reflecting steady demand from industrial automation and the evolving needs of advanced automotive and renewable energy sectors.

North America is the leading regional market, accounting for approximately 40% share, supported by its advanced industrial base, strong R&D capabilities, and significant demand from the automotive, aerospace, and energy sectors.

The specialty lubricant market is moderately consolidated, led by global majors such as Shell, ExxonMobil, Chevron, and TotalEnergies, which capitalize on scale and strong OEM partnerships. Niche players such as FUCHS SE, Klüber Lubrication, and Quaker Houghton compete through specialized expertise and high-margin, application-specific formulations.