- Food Packaging

- Snack Food Packaging Market

Snack Food Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Snack Food Packaging Market By Material (Plastic, Glass, Others), Packaging Type (Flexible Packaging, Pouches & Bags, Others), Snack Type, and Regional Analysis for 2026 - 2033

Snack Food Packaging Market Size and Trends Analysis

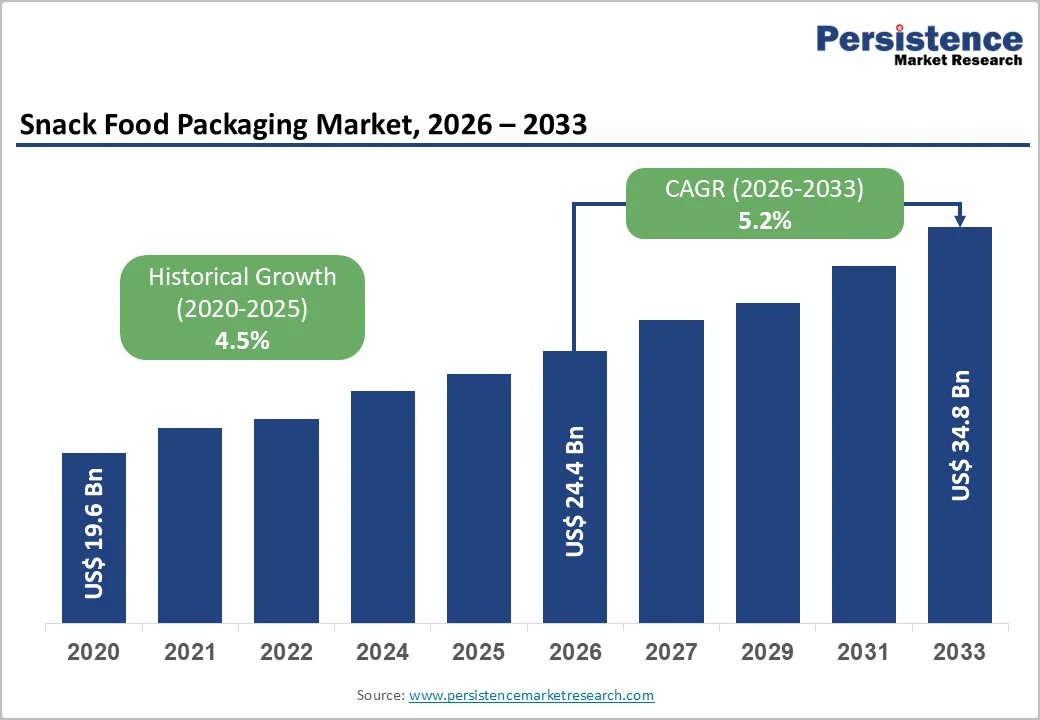

The global snack food packaging market is projected to reach US$24.4 billion in 2026 and US$34.8 billion by 2033, growing at a CAGR of 5.2% between 2026 and 2033, driven by consistent growth in global snack consumption and rising preference for convenient, on-the-go food formats.

Rising urbanization, expansion of e-commerce grocery channels, and strong demand for portion-controlled packaging continue to drive packaging volumes and value. Flexible packaging formats dominate due to their cost efficiency, lightweight logistics, and compatibility with high-speed production lines. Sustainability-driven innovation in recyclable mono-materials, paper-based solutions, and low-carbon barrier technologies is also reshaping investment priorities across the value chain.

Key Industry Highlights

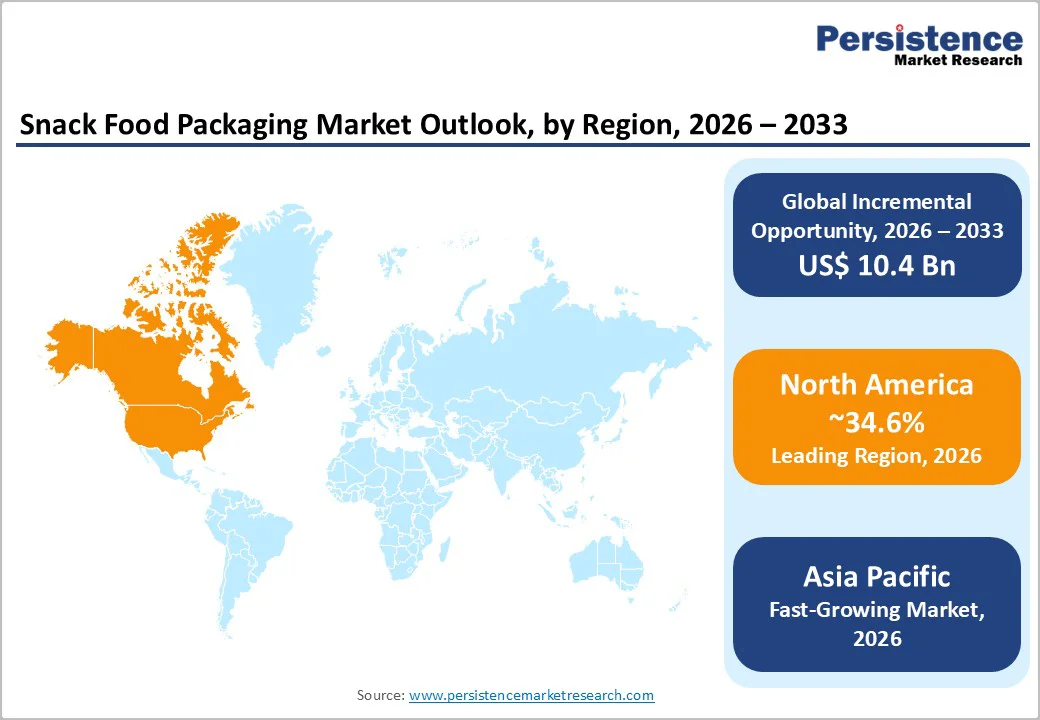

- Leading Region: North America is anticipated to lead the market with an estimated 34.6% share, supported by high per-capita snack consumption, advanced retail infrastructure, and early adoption of recyclable mono-material and resealable flexible packaging formats.

- Fastest-Growing Region: Asia Pacific is likely to be the fastest-growing region, driven by rising disposable incomes, rapid urbanization, and strong growth in flexible pouch adoption across China, India, and Southeast Asia, collectively contributing over 30% of incremental market growth during the forecast period.

- Investment Plans: Capital investments are increasingly directed toward recyclable flexible packaging, automation, and localized manufacturing, with a significant share of new spending focused on mono-material films, downgauging technologies, and capacity expansion in Asia Pacific to support high-volume snack production.

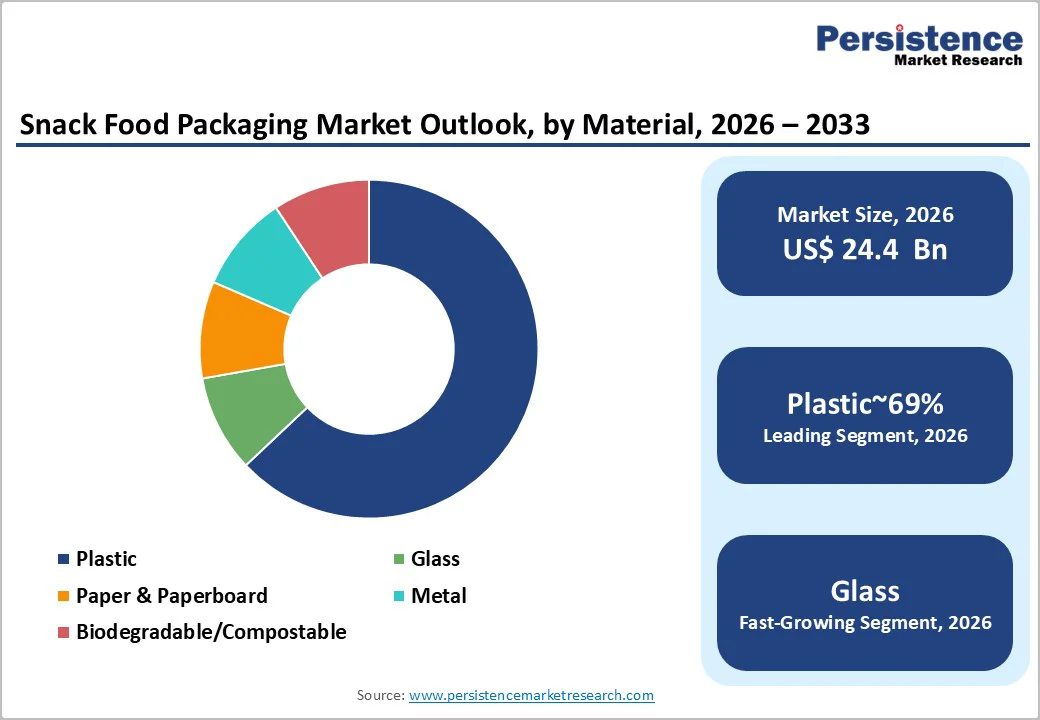

- Dominant Material: Plastic materials are expected to be dominant, accounting for approximately 69% of the total snack food packaging demand, due to their superior barrier properties, lightweight nature, and compatibility with high-speed packaging lines.

- Leading Packaging Type: Flexible packaging is estimated to be the leading packaging type, representing around 75% of the total market share, driven by cost efficiency, logistical advantages, and a strong demand for resealable, on-the-go snack formats across global retail channels

| Key Insights | Details |

|---|---|

| Snack Food Packaging Market Size (2026E) | US$24.4 Bn |

| Market Value Forecast (2033F) | US$34.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising On-the-Go Consumption and Portion Control

Global shifts in consumer lifestyles, particularly urbanization and longer working hours, have significantly increased demand for single-serve and portion-controlled snack formats. These packaging formats are designed to preserve freshness and crispness while supporting convenience-led consumption. Smaller pack sizes typically command higher packaging spend per unit compared to bulk formats, improving value realization for packaging suppliers. Flexible pouches and resealable bags are widely used in these applications, often incorporating advanced barrier films that can extend product shelf life by 6 to 12 months. This structural shift toward smaller packs strengthens per-unit packaging value even amid raw material price volatility.

Sustainability Regulation and Corporate Commitments

Environmental regulations and corporate sustainability commitments are accelerating innovation in snack food packaging materials. Policy instruments such as extended producer responsibility frameworks, recyclable packaging targets, and plastic levies are encouraging brands and converters to transition away from complex laminates toward recyclable or fiber-based alternatives. In response, packaging suppliers are investing in mono-polymer films and paper-dominant pouches that retain barrier performance while improving recyclability. Collaborative development programs between snack brands and packaging suppliers have demonstrated measurable reductions in carbon and water footprints compared to conventional materials. These regulatory and commercial pressures are increasing capital expenditure and R&D intensity, favoring suppliers with validated sustainability credentials.

Flexible Packaging Economics and Supply-Chain Efficiency

Flexible packaging offers material efficiency advantages by using less substrate and significantly reducing transport weight compared to rigid formats. These characteristics translate into lower freight costs, improved pallet efficiency, and reduced warehousing requirements. As snack brands increasingly rely on e-commerce and vending channels, lightweight and dimensionally efficient packaging formats deliver clear margin advantages. Flexible packaging also enables faster design changes and shorter production runs, supporting high SKU proliferation in competitive snack categories. The strong growth trajectory of flexible packaging, combined with premium pricing for advanced barrier films, underpins the sustained expansion of the market.

Barrier Analysis - Recycling Infrastructure and Value-Chain Fragmentation

Despite growing demand for sustainable packaging, inconsistent recycling infrastructure remains a key structural constraint. Many regions lack the industrial sorting and processing capability required to manage multi-layer or specialty packaging materials. In markets with underdeveloped recycling systems, brands often face higher costs to implement take-back programs or alternative collection mechanisms. During transition phases, switching to recycle-ready packaging can increase packaging supply costs by approximately 3-10%, placing pressure on margins unless offset by pricing strategies or operational efficiencies. This fragmentation slows the pace of material substitution despite strong regulatory and consumer momentum.

Volatility in Polymer Feedstock and Conversion Costs

Fluctuations in polymer feedstock prices and energy costs continue to create margin volatility for packaging converters. Although hedging strategies are commonly employed, they do not fully eliminate exposure to price swings. During periods of elevated material costs, snack brands may delay packaging upgrades or select lower-cost substrates that compromise recyclability goals. Historically, raw material price movements of 15-25% have translated into a 2-6% impact on brand-level packaging cost of goods, influencing promotional activity and pack-size strategies. This cyclical cost exposure can delay sustainability-related capital investments.

Opportunity Analysis - Recyclable Mono-Material and Paper-Based Pouches

The transition toward recyclable mono-material films and high-fiber paper pouches represents a major growth opportunity across the packaging ecosystem. If these solutions capture even 10-15% of current laminated pouch volumes by 2033, the resulting retrofit and conversion demand would represent a substantial revenue opportunity for converters, material suppliers, and recycling partners. Pilot programs have demonstrated that brands are willing to pay a premium for packaging solutions with verified recyclability. Successful commercialization models provide clear pathways for scale, particularly in markets with established recycling streams.

Premiumization and Advanced Barrier Technologies

Premium snack categories require enhanced oxygen and moisture protection to maintain product quality, particularly for high-fat, gourmet, or nutritionally fortified products. Advanced metallized films, high-barrier polymers, and active packaging solutions enable these premium offerings while supporting longer shelf life. Premium snack variants often sustain packaging spend levels that are 15-30% higher than those of mainstream products. Packaging suppliers that combine advanced barrier performance with lower environmental impact are well-positioned to capture disproportionate value in this growing segment.

Category-wise Analysis

Material Insights

Plastic is expected to be the dominant material type, accounting for 69% of revenue, primarily due to its lightweight nature, superior barrier performance, and seamless compatibility with high-speed form-fill-seal (FFS) equipment. Flexible plastic films, particularly those based on polyethylene (PE) and polypropylene (PP), account for the majority of snack packaging volumes globally. These materials offer strong resistance to moisture, oxygen, and grease, which is critical for preserving the freshness, texture, and shelf life of high-volume savory snacks such as chips, extruded snacks, and crackers.

Ongoing capital investments continue to favor mono-polymer plastic structures as manufacturers seek to balance performance requirements with recyclability goals. Flexible plastic packaging also provides unmatched logistical efficiency, reducing transportation costs through lower weight and optimized pallet utilization. Features such as resealability, transparent windows, and high-quality graphics further enhance consumer appeal and support premium positioning. These advantages reinforce plastic’s leadership position, particularly in mass-market and high-turnover snack categories distributed through supermarkets, convenience stores, and vending channels.

Glass is likely to be the fastest-growing material segment within premium and niche snack food packaging applications, despite its limited overall market share. Growth is primarily driven by its premium perception, inert properties, and 100% recyclability, which align strongly with sustainability-focused branding and high-end product positioning. Snack categories such as gourmet confectionery, artisanal nuts, dried fruits, and specialty gift packs increasingly adopt glass jars and containers to enhance shelf appeal and reinforce quality credentials.

The growth momentum is concentrated in developed markets such as Europe, Japan, and parts of North America, where consumers are more willing to pay for reusable and premium packaging formats. While higher weight and transportation costs constrain glass, its application in low-volume, high-value snack segments supports above-average CAGR from a low base. As premiumization and sustainability narratives strengthen, glass continues to gain traction in selective snack packaging formats without challenging the dominance of flexible plastics in mass-market applications.

Packaging Type Insights

Flexible packaging is estimated to dominate the market, accounting for approximately 75% of the market share. Its leadership is driven by unmatched versatility, cost efficiency, and adaptability across a wide range of snack formats and distribution channels. Pouches and bags remain the most widely used formats, supporting both single-serve and family-size packs while enabling high-speed manufacturing and efficient storage.

Flexible packaging allows for superior shelf impact through advanced printing and design capabilities, including matte finishes, metallic effects, and transparent elements. These features are particularly valuable in crowded retail environments where brand differentiation is critical. From an operational perspective, flexible formats require less raw material than rigid alternatives and significantly reduce transportation emissions due to lower weight and cube efficiency. These advantages have made flexible packaging the preferred choice for savory snacks, confectionery-adjacent snacks, and baked products across global markets.

Resealable and sustainability-focused pouches are likely to be the fastest-growing sub-segment, expanding at a rate higher than the overall market. Demand is driven by increasing consumer preference for freshness retention, portion control, and reduced food waste, particularly in multi-serve snack formats. Resealable closures such as zippers and press-to-close systems are becoming standard across premium and mid-range snack offerings.

Sustainable pouch designs incorporating recyclable mono-material structures or high-fiber content are gaining rapid acceptance. Advances in lamination technologies, barrier coatings, and digital printing are enabling these pouches to achieve performance parity with conventional formats while offering shorter lead times and lower minimum order quantities. These innovations enable faster product launches and make resealable, sustainable pouches especially attractive to regional brands, private-label brands, and premium snack producers seeking differentiation and regulatory compliance.

Regional Insights

North America Snack Food Packaging Market Trends - Convenience-Driven Demand and Mono-Material Transition

North America is projected to lead, accounting for approximately 34.6% of the market share, with the U.S. accounting for the majority of regional demand. High per-capita snack consumption, a deeply penetrated modern retail ecosystem, and strong preference for convenience-driven formats such as resealable pouches and single-serve packs underpin regional leadership. The U.S. snack sector continues to favor flexible packaging for savory snacks, bakery items, and functional snacks, supported by advanced packaging machinery infrastructure and high automation levels.

Investments across the region increasingly focus on recyclable mono-material structures, downgauged films, and advanced barrier coatings. Major snack brand owners have publicly committed to transitioning toward recyclable or reusable packaging formats, accelerating supplier qualification for mono-PE and mono-PP solutions. State-level sustainability initiatives, including extended producer responsibility (EPR) laws in states such as California and Oregon, are influencing material selection and packaging design. Retailer sustainability scorecards and private-label packaging standards are further shaping procurement strategies, reinforcing demand for packaging suppliers that can meet both performance and regulatory requirements.

Europe Snack Food Packaging Market Trends - Regulation-Led Sustainability and Fiber-Based Innovation

Europe is defined by stringent sustainability expectations, harmonized regulatory frameworks, and well-established recycling systems, making it one of the most regulation-driven markets globally. Germany and the U.K. lead the region in both packaging volumes and innovation, supported by strong packaged-snack consumption and advanced waste-collection infrastructure. France and Spain are witnessing faster adoption of fiber-based and paper-dominant snack packaging, particularly in bakery snacks and premium snack bar categories.

Regulatory alignment under the EU Packaging and Packaging Waste Regulation (PPWR) has accelerated the shift toward recyclable and low-complexity material structures. Several European snack producers and retailers have piloted paper-based pouches and reduced-plastic formats to comply with recyclability thresholds and labeling requirements. Retail chains across Western Europe increasingly mandate packaging recyclability and material transparency, influencing supplier selection and accelerating innovation in fiber-based laminates and recyclable flexible formats. As a result, Europe continues to function as a testing ground for next-generation sustainable snack packaging solutions that later scale globally.

Asia Pacific Snack Food Packaging Market Trends - Volume-Driven Growth and Flexible Packaging Scale-Up

Asia Pacific is likely to be the fastest-growing regional market for snack food packaging, driven by large population bases, rising disposable incomes, and the rapid expansion of modern retail and e-commerce channels. China dominates the region in absolute scale, supported by high snack consumption volumes and a well-developed flexible packaging manufacturing base. India is experiencing strong growth in flexible pouch adoption, particularly for affordable single-serve and small pack formats that cater to price-sensitive consumers. Japan remains distinct, emphasizing premium, high-barrier packaging for quality preservation and aesthetic differentiation.

Investment trends across the region favor localized manufacturing expansion, joint ventures, and supply-chain optimization to support high-volume growth and reduce logistics costs. Multinational packaging suppliers have expanded production capacity in Southeast Asia to better serve regional snack manufacturers. Domestic snack brands are also increasingly upgrading packaging quality to align with international standards, driving demand for better barrier films, resealable formats, and improved print quality. These developments position Asia Pacific as both a high-growth consumption market and a critical global manufacturing hub for snack food packaging.

Competitive Landscape

The global snack food packaging market is moderately consolidated at the top, with global converters controlling significant shares of advanced barrier and sustainable packaging solutions. Beneath this tier, a fragmented regional landscape serves local and price-sensitive markets. Competitive advantage increasingly depends on material innovation, recyclability validation, and manufacturing scale.

Recent years have seen increased consolidation, strategic partnerships, and product innovation focused on sustainability and scale efficiency. Large acquisitions have expanded global footprints and R&D capabilities, while collaborations between packaging suppliers and snack brands have accelerated the commercialization of recyclable and paper-based formats.

Leading companies prioritize sustainable material innovation, cost leadership through scale, and geographic expansion via mergers, acquisitions, and partnerships. Integration of advanced barrier performance with verified sustainability credentials remains the primary differentiator.

Key Industry Developments

- In November 2025, Boom Boom Chewing Gum partnered with packaging specialist Koehler to develop sustainable paper-based packaging for gum products, marking an industry shift toward recyclable, fiber-rich solutions in confectionery and snack segments.

- In July 2025, KIND Snacks launched a fully recyclable paper wrapper pilot for its snack bars, initially available at select retail locations, reflecting growing brand momentum toward recyclable packaging in the U.S. snack category.

Companies Covered in Snack Food Packaging Market

- Amcor plc

- Mondi Group

- Berry Global

- Sealed Air Corporation

- Huhtamaki Oyj

- Sonoco Products Company

- Smurfit Westrock

- DS Smith plc

- Crown Holdings

- Ball Corporation

- TC Transcontinental

- Coveris Group

- Constantia Flexibles

- ProAmpac

- Graham Packaging Company

- Winpak Ltd.

- UFlex Ltd.

- Bemis Company (Amcor)

Frequently Asked Questions

The global snack food packaging market is estimated to be valued at US$24.4 billion in 2026.

By 2033, the snack food packaging market is projected to reach US$34.8 billion.

Key trends include the growing adoption of flexible and resealable packaging, rising demand for sustainable and recyclable materials, increased use of mono-material structures, and premium packaging solutions for better shelf appeal and extended shelf life.

Plastic is the leading material segment, projected to account for around 69% of total market share, due to its lightweight nature, strong barrier properties, and compatibility with high-speed form-fill-seal (FFS) packaging lines.

The snack food packaging market is expected to grow at a CAGR of 5.2% between 2026 and 2033, driven by rising snack consumption, on-the-go eating habits, and innovations in flexible packaging.

Major players include Amcor plc, Mondi Group, Berry Global (Amcor), Huhtamaki Oyj, and Sealed Air Corporation.