- Beauty & Personal Care

- Skin Protectant Products Market

Skin Protectant Products Market Size, Share, and Growth Forecast, 2026 - 2033

Skin Protectant Products Market by Product Type (Ointments, Creams, Gels, Sprays, Lotions), Ingredients (Natural Ingredients, Synthetic Ingredients), End-User (Individual Care, Cosmetic Clinics), Application (Daily Skin Care, Medical Use, Outdoor Activities, Workplace Protection, Sports & Fitness), and Regional Analysis for 2026 - 2033

Skin Protectant Products Market Share and Trends Analysis

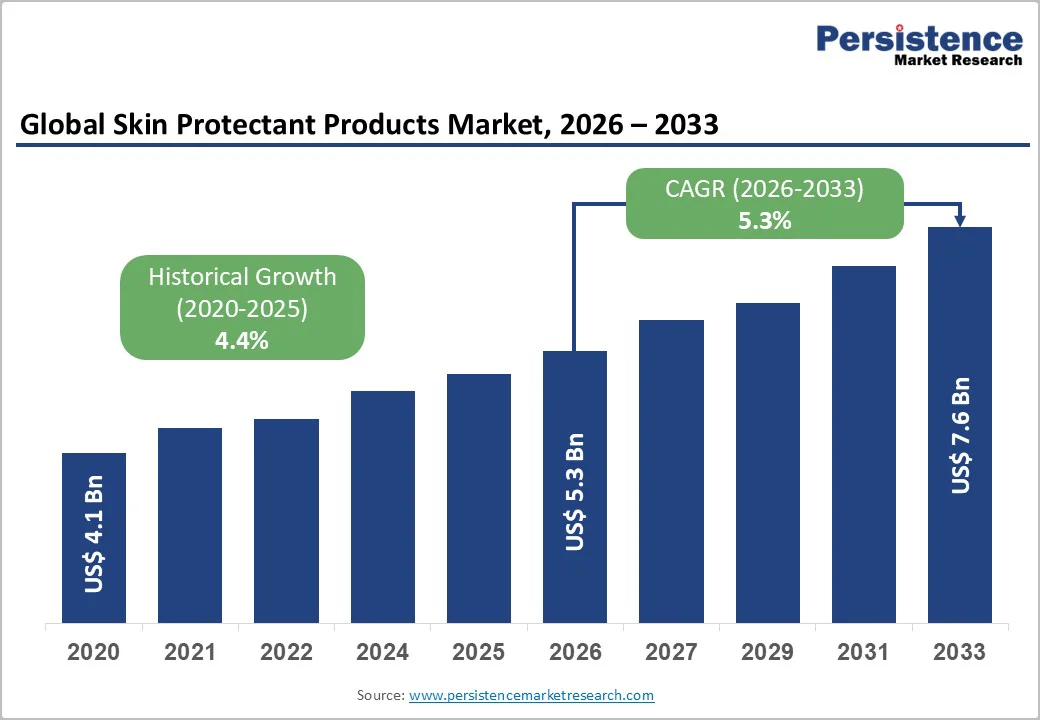

The global skin protectant products market size is likely to be valued at US$5.3 billion in 2026 and is estimated to reach US$7.6 billion by 2033, growing at a CAGR of 5.3% during the forecast period 2026−2033. Heightened awareness regarding dermatological health, coupled with the rising prevalence of skin-related conditions, has catalyzed demand growth across diverse applications. Sunscreen products have transcended their traditional recreational use to become essential components in personal care routines, clinical dermatology practices, and occupational safety protocols for outdoor workers.

This diversification of use cases reflects a fundamental shift in how consumers and healthcare providers perceive photoprotection as a critical health priority rather than a seasonal convenience. Product innovation has also accelerated significantly, with manufacturers developing increasingly sophisticated formulations that combine natural botanical extracts such as zinc oxide and titanium dioxide with advanced synthetic protective agents, improving cosmetic elegance and enhancing stability profiles.

Key Industry Highlights

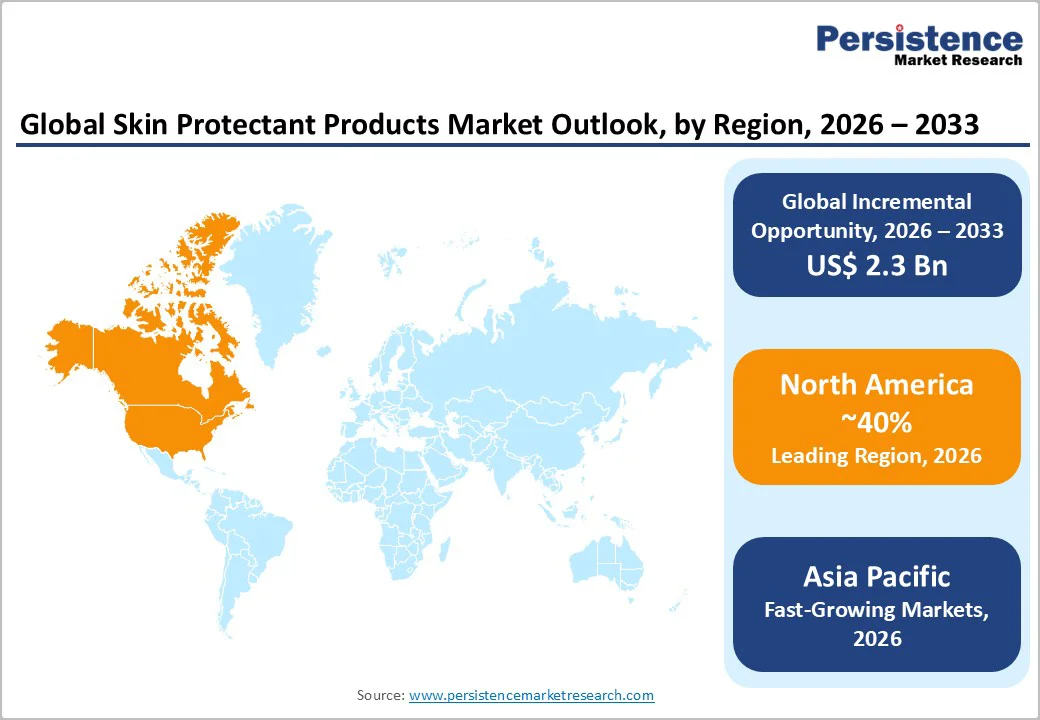

- Dominant Region: North America is projected to lead in 2026 with around 40% share, driven by strong healthcare infrastructure and high consumer spending.

- Fastest-growing Market: Asia-Pacific is expected to be the fastest-growing market through 2033, owing to rising incomes, rapid urbanization, and increased skin health awareness.

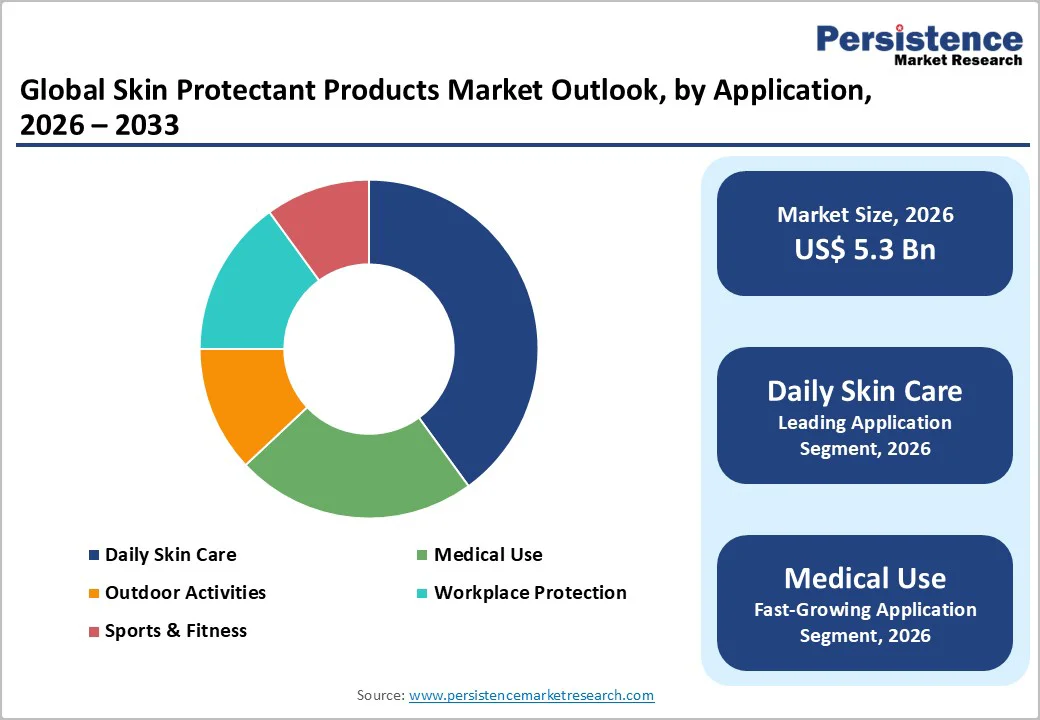

- Leading Application: Daily skin care is likely to dominate with a 42% revenue share in 2026, backed by routine skin protection needs and broad consumer adoption across age groups and lifestyles.

- Fastest-growing Application: Medical applications are poised to register the highest 2026-2033 CAGR, driven by the extensive use of skin protection solutions in hospitals to treat chronic wounds.

| Key Insights | Details |

|---|---|

|

Skin Protectant Products Market Size (2026E) |

US$5.3 Bn |

|

Market Value Forecast (2033F) |

US$7.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.3% |

|

Historical Market Growth (CAGR 2020 to 2024) |

4.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growing Prevalence of Skin Conditions

The surge in dermatological issues has significantly boosted demand for barrier repair products, as both consumers and healthcare professionals emphasize rapid skin barrier restoration, sustained moisture retention, and defense against irritants. Urban pollution, harsh skincare regimens, and environmental stressors such as extreme temperatures or humidity fluctuations exacerbate conditions, including dryness, dermatitis, and minor abrasions, necessitating regular application of protective topicals. A substantial consumer base now prioritizes preventive skincare strategies over reactive interventions, fostering consistent use across pediatric, adult, and geriatric demographics.

Clinical evidence further supports this trajectory, with the World Health Organization (WHO) reporting that nearly 900 million people worldwide suffer from skin diseases at any given time, underscoring an urgent need for affordable topical interventions. Elevated diagnostic frequencies in primary care settings drive product adoption, while clinicians routinely recommend barrier creams to manage both chronic disorders and acute episodes, thereby cultivating institutional trust. Such endorsements have amplified procurement through diverse channels, including retail pharmacies, hospital dispensaries, and e-commerce platforms, ensuring sustained volume growth.

Regulatory Hurdles and Compliance Costs

Regulatory challenges and compliance expenses represent significant barriers to market expansion, requiring manufacturers to synchronize product formulations, labeling requirements, and ingredient specifications with dynamic regulatory frameworks across global jurisdictions. Evolving over-the-counter (OTC) monograph guidelines, rigorous quality assurance standards, and comprehensive safety validation protocols heighten operational demands, prolonging development timelines through mandatory documentation, stability testing, and risk evaluation processes. These factors constrain the speed of new product launches and hinder innovation velocity in a competitive landscape where superior formulation efficacy determines differentiation and market positioning.

Financial strains compound these issues throughout the product lifecycle, as compulsory audits, facility certifications, and reformulation initiatives inflate fixed costs and erode profit margins. Smaller enterprises face higher entry thresholds, with resource constraints diverting scarce capital toward regulatory compliance rather than growth initiatives. At the same time, established corporations grapple with enterprise-wide overhead from quality management systems. Companies that proactively integrate regulatory intelligence into early-stage R&D pipelines and leverage shared compliance platforms can mitigate these pressures, preserving flexibility to broaden stock-keeping unit (SKU) assortments and adapt swiftly to shifting consumer preferences amid tightening oversight.

Emergence of Natural and Organic Formulations

Natural and organic barrier repair formulations emerge as a premium growth avenue, fueled by consumer transitions toward full ingredient disclosure, clean-label skincare regimens, and wellness-integrated personal care products. Escalating sensitivities to synthetic compounds, coupled with expanding knowledge of potential irritants, are driving a preference for plant-based protective agents that dermatologists endorse as safer alternatives for daily use. Brands featuring unadulterated botanical foundations, reduced additive profiles, and sustainably sourced materials achieve accelerated shelf placement in upscale personal care channels, enhancing pricing premiums and fostering enduring customer allegiance.

These products gain further momentum as retailers curate clean beauty collections and dermatological experts champion milder formulations to support sustained skin barrier maintenance across diverse patient profiles. Alignment with sustainability principles, cruelty-free certifications, and ethical production practices particularly appeals to affluent, health-oriented demographics seeking holistic solutions. Enterprises innovating through nutrient-dense oils, herbal extracts, and biologically derived emollients can establish clear competitive edges in saturated markets, effectively attracting discerning buyers who prioritize superior, experiential skincare outcomes over commoditized options.

Category-wise Analysis

Product Type Insights

Ointments are expected to occupy the leadership position, capturing around 30% of the skin protectant products market revenue share in 2026, attributable to their dense occlusive consistency that delivers exceptional moisture occlusion for managing severe dermatological issues such as eczema and burns. Healthcare practitioners consistently recommend ointments for precise therapeutic intervention, securing robust uptake within clinical environments and prescription channels. This entrenched preference underscores the reliability of ointments in addressing acute barrier disruptions, where sustained hydration is essential for recovery and symptom control.

Creams are likely to register the most rapid growth from 2026 to 2033, driven by their versatility and widespread consumer affinity for lightweight, non-greasy formulations that integrate seamlessly into everyday routines. The incorporation of botanical and plant-derived components further elevates their appeal across personal care applications, particularly for sensitive skin profiles that require gentle yet effective protection. This dual appeal positions creams to bridge mass-market accessibility with premium differentiation, enabling brands to target diverse demographics while capitalizing on evolving preferences for multifunctional, consumer-friendly topicals.

Ingredients Insights

Synthetics are poised to command market dominance, securing roughly 60% revenue share in 2026, as ingredients such as dimethicone and zinc oxide deliver robust barrier defense that excels in medical and clinical contexts. Healthcare providers prioritize these components for their established skin compatibility, uniform performance, and dependable outcomes, fueling extensive integration into prescription and OTC formulations. This professional endorsement cements the foundational role of synthetics in therapeutic applications where consistent efficacy outweighs aesthetic considerations.

Natural ingredients are expected to grow the fastest through 2033, driven by consumer enthusiasm for clean, sustainable formulations that incorporate plant extracts and botanicals. Personal care enthusiasts favor these gentle, eco-conscious alternatives that harmonize with wellness-oriented routines and ethical procurement standards. This surge positions brands that blend natural profiles with clinical-grade performance to span mass-market volumes and premium niches, capitalizing on heightened demand for multifunctional topicals that prioritize environmental stewardship and dermal compatibility.

Application Insights

Daily skin care is set to dominate in 2026, projected to hold roughly 40% revenue share, fueled by essential countermeasures against everyday irritants and commitment to holistic dermal wellness. Broad adoption across diverse age cohorts and lifestyle profiles generates reliable volumes, cementing this category as a cornerstone within personal hygiene ecosystems. Its enduring strength stems from universal accessibility and alignment with preventive health paradigms that prioritize sustained barrier integrity for long-term vitality.

Medical use is slated to demonstrate the strongest growth during 2026-2033, driven by hospital deployments for chronic wound management and targeted dermatological interventions. Demographic aging, alongside escalating comorbidities, heightens the need for proven clinical compositions that deliver therapeutic precision. Deepening embedding within standardized healthcare workflows positions this segment for outsized gains, empowering brands to scale professional-grade portfolios that meet rigorous efficacy standards while addressing intensifying global burdens from complex skin pathologies.

Regional Insights

North America Skin Protectant Products Market Trends

North America is projected to dominate, with an estimated 40% share of the skin protectant products market in 2026. The region’s leadership is anchored in a well-established healthcare infrastructure combined with high consumer expenditure on personal care and preventive skincare. Strong penetration of pharmacies, dermatology clinics, and online retail platforms ensures widespread accessibility of both OTC and prescription-grade formulations. The presence of leading multinational skincare and pharmaceutical companies in the U.S. and Canada drives innovation, regulatory compliance, and product availability, reinforcing market stability and sustained growth.

A key factor behind North America’s dominance is the integration of advanced dermatological practices with consumer-focused education on skin barrier protection and chronic condition management. The region benefits from high awareness of product efficacy, safety, and scientific validation, encouraging adoption across age groups and medical-use segments. Rising prevalence of lifestyle-related skin concerns and environmental stressors further intensifies demand for clinically backed barrier solutions. Coupled with regulatory support for novel formulations, the North American market remains both robust and innovation-driven, sustaining its competitive advantage.

Europe Skin Protectant Products Market Trends

Europe is a pivotal market for skin protectant products, underpinned by advanced healthcare systems and heightened consumer awareness of dermal wellness. Robust penetration spans daily maintenance, sensitive-skin solutions, and therapeutic applications, bolstered by stringent regulatory standards that ensure formulation safety and performance. Trust in dermatologically validated, evidence-supported compositions sustains steady uptake through retail outlets and professional dispensaries alike.

Market momentum is expected to accelerate due to regional stakeholders' affinity for transparent labeling, hypoallergenic profiles, and plant-derived alternatives that resonate with health-centric preferences. Sophisticated pharmacy infrastructures, boutique specialists, and proliferating digital marketplaces amplify product reach and user convenience. Escalating interest in dermocosmetics, demographic maturation, and proactive skincare adoption establish Europe as a dependable, premium-value arena, primed for enduring expansion across upscale and accessible offerings tailored to discerning regional dynamics.

Asia Pacific Skin Protectant Products Market Trends

Asia Pacific is well-positioned to become the fastest-growing regional market for skin protectant products from 2026 to 2033, driven by rising disposable incomes, accelerated urbanization, and heightened awareness of dermal wellness. China, India, and Japan have been experiencing surging requirements for preventive and therapeutic skincare interventions. Proliferating e-commerce channels alongside modernized retail infrastructures broaden the availability of routine and specialized protectants, cultivating persistent consumer integration.

Regional dynamics gain additional thrust from pronounced preferences for natural and herbal compositions that emphasize clean, sustainable, and botanical constituents. Intensified recognition of pollution-induced dermal challenges, coupled with the expansion of the middle class, magnifies overall uptake. Healthcare infrastructure enhancements and proliferating dermatology expertise expedite therapeutic deployment, positioning Asia Pacific as a dynamic growth engine that accommodates volume-driven mass offerings and aspirational premium variants attuned to evolving socioeconomic trajectories.

Competitive Landscape

The global skin protectant products market exhibits moderate concentration, with leading enterprises commanding approximately 35% of total revenue through established brand equity, expansive distribution networks, and sophisticated research and development operations. These dominant players sustain superiority across therapeutic and consumer applications by prioritizing breakthrough innovations, clinically substantiated compositions, and worldwide market penetration. Their strategic emphasis on evidence-driven advancements fortifies barriers to entry and ensures resilient positioning amid intensifying competition.

A diverse array of regional and local producers fosters fragmentation, with mid-tier and smaller operators carving niches via specialized offerings, botanical or herbal profiles, and adaptations to localized preferences. Such agility enables targeted fulfillment of distinct consumer requirements, nurturing pockets of specialized expansion within broader ecosystems. Alliances between scale leaders and nimble innovators can further amplify opportunities while mitigating risks from regulatory flux and shifting demographics.

Key Industry Developments

- In October 2025, Australia recalled 18 sunscreens after tests found many failed to meet their claimed SPF levels, including Ultra Violette’s Lean Screen, which was advertised as SPF 50+ but tested at SPF 4.

- In August 2025, Alkem Laboratories launched Olesoft Trucera Moisturizing Lotion, a science-driven formulation aimed at restoring skin hydration, strengthening the barrier, and soothing flare-ups. The product adopts an “inside-out” approach to skin care, combining advanced technology with targeted efficacy to address daily skin concerns.

- In July 2025, Kao Corporation launched new Sensai, Kanebo, and Curél products featuring womb-inspired protective ingredients and synergistic components for deep cleansing and moisturization, supporting global expansion and strengthened market presence.

Companies Covered in Skin Protectant Products Market

- ConvaTec

- 3M

- Johnson & Johnson

- Medline Industries

- Pfizer

- Unilever

- Smith & Nephew

- Essity

- Coloplast

- DermaRite Industries

- Pharmaceutical Specialties

- Salts Healthcare

Frequently Asked Questions

The global skin protectant products market is projected to reach US$ 5.3 billion in 2026.

Rising awareness of skin health, demand for preventive and therapeutic care, and preference for natural and clinically tested formulations are driving the market.

The market is poised to witness a CAGR of 5.3% from 2026 to 2033.

Key market opportunities include growing demand for natural and organic formulations, advanced dermocosmetic solutions, and increasing skin health awareness in emerging economies.

Some of the key market players include ConvaTec, 3M, Johnson & Johnson, Medline Industries, Pfizer, and Unilever.