- Healthcare Services

- Transformational Skincare Market

Transformational Skincare Market Size, Share, and Growth Forecast, 2026 - 2033

Transformational Skincare Market by Product Type (Face Creams, Serums, Sunscreen, Face Masks), End-User (Female, Male, Kids), Distribution Channel (Online, Offline), and Regional Analysis for 2026-2033

Transformational Skincare Market Share and Trends Analysis

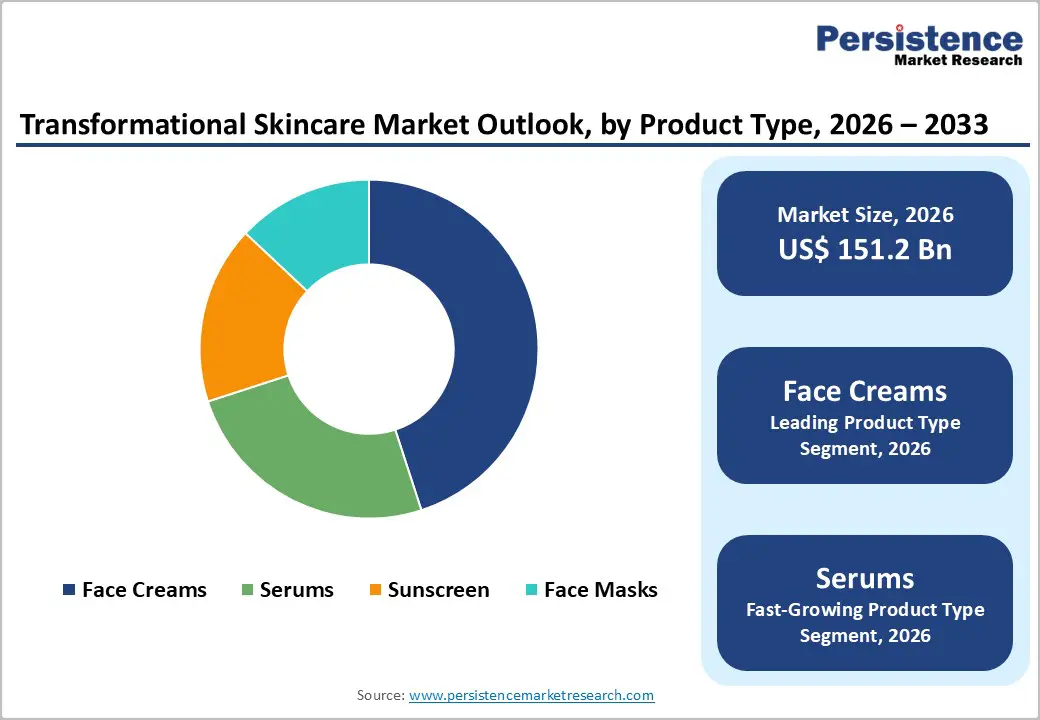

The global transformational skincare market size is likely to be valued at US$ 151.2 billion in 2026, and is projected to reach US$ 300.0 billion by 2033, growing at a CAGR of 7.5% during the forecast period 2026−2033.

Growth is being supported by the rising demand for biotechnology-based formulations that are delivering clinically validated outcomes. Consumers are increasingly adopting advanced ingredients such as exosomes, bioactive peptides, and microbiome-supporting complexes that are targeting long-term skin regeneration rather than short-term cosmetic enhancement. Brands are investing in research collaborations and dermatological testing to strengthen scientific credibility. At the same time, artificial intelligence is integrating with personalized skincare diagnostics to generate data-driven product recommendations. This technological convergence is enabling companies to tailor formulations based on individual skin profiles, thereby increasing product efficacy and customer retention. Environmental awareness is also influencing purchasing behavior across major markets. Consumers are seeking clean formulations with transparent ingredient disclosure and responsibly sourced raw materials. Regulatory bodies are tightening labeling standards, which is reinforcing demand for safety and traceability. Sustainable packaging initiatives and biodegradable components are becoming competitive differentiators. Korean beauty innovation, commonly referred to as K-beauty, is also shaping global product development strategies by emphasizing multi-step routines and skin barrier health. Companies are therefore repositioning portfolios toward multifunctional products that are strengthening skin resilience while maintaining aesthetic appeal.

Key Industry Highlights

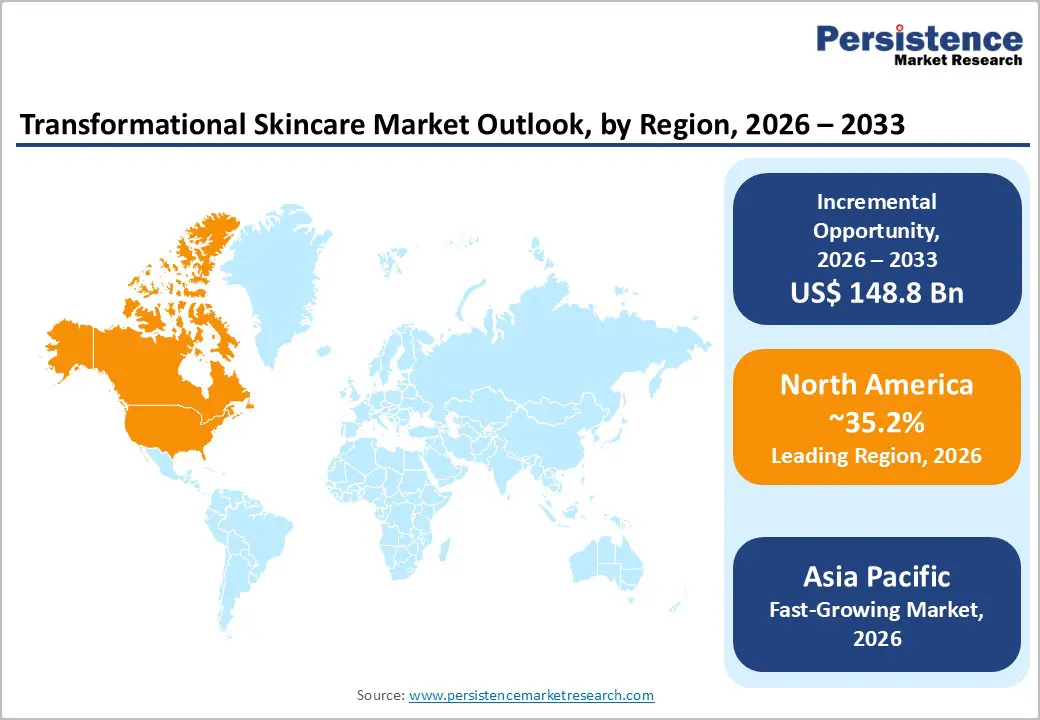

- Dominant Region: North America is expected to command about 35.2% of the market share in 2026, supported by sophisticated consumer awareness and established brand infrastructure.

- Fastest-growing Regional Market: The Asia Pacific market is poised to be the fastest-growing through 2033, owing to the expansive consumer bases and manufacturing efficiency advantages.

- Leading & Fastest-growing Product Type: Face creams are set to dominate with approximately 42.1% revenue share in 2026, while serums are likely to be the fastest-growing segment during the 2026-2033 forecast period.

- Leading & Fastest-growing Application: Female consumers are expected to capture around 35% revenue share in 2026, whereas male consumers are slated to grow the fastest between 2026 and 2033.

- December 2025: IMMACULATE was launched as a transparent, science-backed skincare brand addressing consumer confusion with straightforward, research-driven formulations emphasizing self-care, efficacy, and sustainability.

| Report Attribute | Details |

|---|---|

|

Transformational Skincare Market Size (2026E) |

US$ 151.2 Bn |

|

Market Value Forecast (2033F) |

US$ 300.0 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

12.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Biotechnology Revolution and Clinical Efficacy Demand

Biotechnology innovation is accelerating structural advancement within the transformational skincare market by enabling cellular-level intervention rather than superficial enhancement. Laboratory-developed peptides, recombinant growth factors (RGFs), and precision fermentation–derived compounds are increasingly targeting defined biological pathways associated with collagen synthesis, inflammation control, and barrier repair. These active ingredients are interacting directly with skin cell receptors and signaling mechanisms, thereby supporting measurable physiological improvement. Consumers are prioritizing formulations that demonstrate clinical substantiation and mechanistic clarity. Brands that are communicating the molecular function of bioengineered actives are strengthening credibility and differentiation.

The edible beauty infusion segment is simultaneously reflecting evolving consumer priorities toward systemic wellness. Collagen supplementation and probiotic formulations are gaining traction as individuals are linking gut health and nutrient bioavailability to visible skin outcomes. These ingestible solutions are supporting microbiome balance and structural protein regeneration, which are contributing to longer-term vitality. Consumers are moving away from short-duration aesthetic fixes and are embracing integrated routines that combine topical application with ingestible support. Brands that are aligning nutraceutical formats with surface treatments are creating holistic beauty-from-within frameworks. Educational initiatives explaining absorption pathways and biological impact are enhancing trust among informed buyers. Companies operating at the intersection of biotechnology, nutrition science, and personalized diagnostics are positioning themselves to capture sustained demand as efficacy and transparency continue to guide purchasing decisions.

Limited Shelf Life and Product Degradation Challenges

Transformational skincare products that contain bioactive ingredients, natural extracts, and peptide complexes are facing significant stability constraints that are limiting scalability. Growth factors, enzymes, and live probiotics are maintaining relatively short shelf lives and are degrading when exposed to oxygen, ultraviolet light, or temperature fluctuation. These sensitivities are requiring controlled storage environments and specialized barrier packaging. Companies are implementing cold-chain logistics and multi-layer airless containers to protect formulation integrity. Such requirements are increasing production costs and complicating global distribution networks. When active compounds lose potency during transit or storage, product efficacy declines and brand credibility weakens. Smaller manufacturers are encountering greater pressure because they often lack access to advanced stabilization infrastructure and capital-intensive preservation technologies.

Retail channels are also managing tighter inventory cycles due to reduced product durability. Accelerated stock rotation is increasing operational complexity and raising wastage risk. At the same time, regulatory authorities are applying inconsistent stability testing standards across jurisdictions, which is creating compliance uncertainty for international launches. To mitigate these structural risks, leading companies are investing in microencapsulation systems and inert atmosphere packaging techniques that are extending ingredient viability. Many firms are establishing internal stability benchmarks that exceed minimum regulatory thresholds. Vertical supply chain integration is enabling tighter temperature monitoring from formulation through final delivery. By strengthening preservation science and communicating quality assurance protocols clearly, manufacturers can convert formulation fragility into a differentiated value proposition that supports premium positioning and long-term consumer trust.

Sustainable and Clean Beauty Innovation

Sustainable skincare formulations are attracting rising consumer demand as environmental awareness is influencing purchasing decisions across global markets. Consumers are actively seeking natural, organic, and chemical-free products that align with responsible sourcing practices. Many buyers are evaluating brands based on measurable environmental stewardship rather than marketing claims alone. Upcycled ingredients are converting agricultural by-products into high-value cosmetic actives, thereby reducing raw material waste. Biodegradable and recyclable packaging systems are lowering plastic dependency and supporting waste reduction targets. Circular economy principles are guiding product development from ingredient sourcing through end-of-life disposal. Regulatory frameworks such as the European Union Corporate Sustainability Reporting Directive (EU CSRD) are requiring companies to disclose environmental performance data, which is increasing transparency and operational accountability throughout supply chains.

Strategic companies are strengthening premium positioning by combining clinical validation with sustainability commitments. Certifications such as United States Department of Agriculture Organic (USDA Organic), COSMOS Standard, and Leaping Bunny Cruelty-Free are verifying product claims and reinforcing consumer trust. These third-party endorsements are supporting pricing power and brand differentiation. Biotechnology applications are enabling the conversion of renewable biomass and waste streams into high-performance active ingredients. Firms are maintaining rigorous dermatological testing while advancing environmentally responsible manufacturing processes. This dual focus on efficacy and ecological integrity is creating durable competitive advantages. Leading brands are integrating sustainability metrics into product development frameworks and implementing end-to-end traceability systems. Transparent sourcing and measurable impact reporting are strengthening loyalty among environmentally conscious consumers while aligning long-term profitability with responsible growth objectives.

Category-wise Analysis

Product Type Insights

Face creams are anticipated to account for approximately 42.1% of the transformational skincare market revenue share in 2026, leading this category. Their dominance is reflecting strong consumer demand for multifunctional formulations that deliver hydration, barrier reinforcement, and active ingredient absorption within a single application. Ingredients such as ceramides, hyaluronic acid, and peptide complexes are supporting moisture retention and structural repair at the epidermal level. Increasing preference for cruelty-free and plant-based products is encouraging brands to combine botanical extracts with biotechnology-derived actives to meet both performance and ethical expectations. Continuous advancements in texture engineering are further strengthening this segment. Gel-cream hybrids, lightweight emulsions, and sun protection factor (SPF)–integrated variants are expanding daily usage scenarios and increasing product versatility. As consumers are prioritizing convenience alongside efficacy, face creams are maintaining a stable leadership position within premium and mass-market categories.

Serums are expected to be the fastest-growing product segment between 2026 and 2033, supported by the rising adoption of high-concentration and targeted formulations. Consumers are embracing streamlined skincare routines that emphasize fewer yet more potent products, a trend commonly referred to as skinimalism. Encapsulated retinol systems are enabling controlled release and reduced irritation, while growth factor serums are positioning themselves as non-invasive alternatives to aesthetic procedures. Microbiome-supporting solutions are addressing inflammation and barrier balance, which is increasing therapeutic appeal. Premium-tier expansion is particularly strong, as buyers are investing in clinically validated ingredients such as exosomes, polynucleotides (PDRN), and advanced peptide complexes. Demonstrated clinical efficacy and measurable skin improvement are supporting elevated price points. As scientific transparency and personalization are increasing in importance, serums are expected to capture a growing share of value-driven consumers seeking evidence-based outcomes.

End-User Insights

Female consumers are projected to represent the leading application segment, holding roughly 35% of the transformational skincare market share in 2026. Women are demonstrating a higher propensity for product experimentation and sustained investment in premium anti-aging and corrective formulations. Established brands such as Estée Lauder Companies Inc. and Lancôme, a brand under L’Oréal S.A., are maintaining strong positions through clinically validated product lines and science-backed ingredient claims. The broader self-care movement is reinforcing skincare as a structured wellness routine rather than a purely cosmetic practice. Multi-step regimens inspired by Korean beauty approaches are normalizing layered product usage and expanding average basket size. Female consumers are also driving demand within natural and organic categories, where transparency, ethical sourcing, and environmentally responsible packaging are influencing purchasing decisions. This segment is therefore continuing to anchor revenue stability while shaping innovation priorities.

Male consumers are expected to represent the fastest-growing application segment between 2026 and 2033. Evolving grooming norms, targeted advertising strategies, and broader social acceptance of male skincare are accelerating adoption. Men exhibit distinct physiological characteristics, including higher sebum production and thicker dermal layers, which require formulations focused on oil regulation, pore refinement, and post-shave barrier recovery. Rising disposable income among urban male populations, particularly in Asia Pacific and North America, is supporting premium product uptake. Brands that are positioning men’s skincare as performance-driven and solution-oriented are achieving stronger resonance. Simplified routines emphasizing functional benefits and measurable outcomes are aligning with male preferences for efficiency. As awareness and accessibility improve, this segment is expected to expand at a faster pace than the overall market.

Distribution Channel Insights

Offline stores are projected to command an estimated 68% of total market revenues in 2026, reflecting their continued dominance in product distribution. Physical retail environments are providing consumers with the ability to evaluate texture, fragrance, packaging quality, and ingredient labeling before purchase. This tactile assessment remains critical for premium skincare products where sensory validation influences buying decisions. Traditional retail formats are reinforcing consumer trust through established shopping habits and immediate product availability. Brick-and-mortar outlets are also supporting brand education through in-store consultations and demonstrations. Increasingly, retailers are integrating omnichannel fulfillment strategies such as buy online pick up in store (BOPIS), which are combining digital convenience with physical verification. These hybrid models are maintaining margin control through optimized inventory management while addressing diverse consumer purchasing preferences.

Online stores are expected to represent the fastest-growing distribution channel between 2026 and 2033. E-commerce platforms are expanding reach by offering broader product assortments and streamlined purchasing processes. Consumers are comparing formulations, reviewing ingredient disclosures, and accessing peer feedback without geographic limitations. Digital channels are delivering continuous availability and personalized recommendations powered by data analytics systems. Targeted advertising and influencer collaborations are strengthening brand visibility and accelerating customer acquisition. Direct-to-consumer (D2C) models are enabling subscription programs and automated replenishment cycles, which are increasing repeat purchase frequency. As logistics infrastructure and digital payment adoption continue improving, online distribution is likely to capture a larger proportion of incremental market growth by 2033.

Regional Insights

North America Transformational Skincare Market Trends

North America is poised to dominate with about 35.2% of the transformational skincare market value in 2026, powered by widespread consumer awareness and a well-established brand ecosystem. The United States is driving regional leadership due to mature purchasing behavior and strong adoption of premium and clinically validated formulations. Consumers are actively seeking measurable anti-aging and corrective outcomes, and they are allocating higher discretionary spending toward science-backed products. Established research and development (R&D) capabilities are accelerating innovation cycles and supporting rapid formulation refinement. Compared with more restrictive regulatory jurisdictions, commercialization timelines are relatively streamlined, which is enabling quicker product launches. Brands operating in this region are prioritizing targeted treatments for hyperpigmentation, collagen depletion, and barrier repair, aligning portfolios with both corrective and preventive care demand.

The United States Food and Drug Administration (FDA) is providing defined regulatory pathways for over-the-counter active ingredients, which is facilitating market entry for advanced retinoids and pharmaceutical-grade actives. Multinational corporations such as The Estée Lauder Companies Inc., L’Oréal S.A., and Johnson & Johnson are maintaining significant regional presence, while independent brands are expanding through agile product innovation. Direct-to-consumer digital platforms are enabling emerging players to scale efficiently and strengthen brand-community engagement. Investment capital is concentrating on artificial intelligence–enabled personalization tools, clean beauty certifications, and biotechnology collaborations focused on next-generation bioactive compounds. An integrated omnichannel framework that connects prestige retailers, dermatology partnerships, and e-commerce platforms can maximize consumer access and improving conversion performance across multiple touchpoints.

Europe Transformational Skincare Market Trends

Europe is set to retain its position as a mature market for transformational skincare products and services, supported by harmonized regulatory standards and strong sustainability leadership. EU cosmetics legislation is enforcing comprehensive ingredient safety and labeling requirements, which are strengthening consumer trust. Germany, the United Kingdom, France, and Spain are generating the majority of regional revenue through diversified product portfolios and established retail networks. Consumers across the region are prioritizing clean beauty formulations and clinically validated dermo-cosmetic products that demonstrate measurable efficacy. Brands are aligning research, sourcing, and packaging strategies with strict regulatory frameworks and environmental accountability expectations. The region is setting global benchmarks for ingredient transparency and ecological responsibility. The U.K. is advancing microbiome-focused innovation and clean formulation trends. Germany is leveraging its pharmaceutical heritage to emphasize clinical performance, while France is sustaining prestige leadership through heritage-driven luxury skincare lines.

The EU CSRD is accelerating the development of upcycled and responsibly sourced ingredients by requiring greater environmental disclosure. Biotechnology applications are converting agricultural by-products into high-performance cosmetic actives, thereby reducing resource waste. Investment is prioritizing circular economy models, biodegradable packaging materials, and carbon-neutral supply chain initiatives. Companies are pursuing B Corporation (B-Corp) certification to validate social and environmental governance standards. Market leaders are transforming regulatory stringency into competitive advantage by strengthening compliance systems and documenting measurable sustainability outcomes. Through transparent reporting and responsible production practices, European brands are reinforcing premium positioning while aligning long-term profitability with environmental stewardship objectives.

Asia Pacific Transformational Skincare Market Trends

Asia Pacific is likely to be the fastest-growing market for transformational skincare through 2033, owing to large consumer populations, accelerating urbanization, and cost-efficient manufacturing ecosystems. China, Japan, South Korea, and India are driving regional expansion through rising disposable incomes and increasing adoption of premium skincare products. Middle-class growth is strengthening demand for clinically validated and multifunctional formulations. Cultural emphasis on long-term skin health and youthful appearance is encouraging structured skincare routines. Brands are adapting formulations to regional humidity levels, ultraviolet exposure intensity, and diverse skin tone requirements. Strong production infrastructure is enabling both domestic consumption and export competitiveness. South Korea is maintaining global innovation leadership through K-beauty methodologies, which are emphasizing multi-step regimens and ingredient experimentation. Actives such as snail mucin, fermented botanical extracts, and centella asiatica are reinforcing holistic wellness positioning within the skincare category.

Digital commerce is playing a decisive role in regional growth. Companies such as AMOREPACIFIC Corporation subsidiaries, Cosrx Inc., and APR Co., Ltd., known for Medicube, are leveraging TikTok Shop and other social commerce platforms to accelerate consumer acquisition. In China, advanced e-commerce ecosystems including Tmall and Douyin are enabling rapid brand scaling and targeted marketing precision. Consumers are demonstrating strong appetite for premium international brands alongside innovative domestic labels. Japan is prioritizing pharmaceutical-grade formulations and advanced ultraviolet protection technologies, while India is witnessing accelerated demand growth driven by urban expansion and social media engagement. Southeast Asian markets such as Indonesia, Thailand, and Vietnam are presenting significant untapped potential. Investment across the region is concentrating on digital infrastructure, influencer-led marketing networks, and climate-adaptive localized product development to sustain high growth momentum through the forecast period.

Competitive Landscape

The global transformational skincare market structure is moderately consolidated, with L’Oréal S.A., The Estée Lauder Companies Inc., Unilever PLC, Procter & Gamble Co., and AMOREPACIFIC Corporation collectively accounting for approximately 45–50% of total market share. These established players are leveraging scale advantages in research and development, global distribution, and regulatory compliance to sustain competitive positioning. However, market consolidation dynamics are evolving as independent brands are gaining traction through direct-to-consumer channels and data-driven digital marketing strategies. Smaller companies are targeting highly specific consumer needs with focused product portfolios and science-backed positioning rather than competing on mass-market volume. Digital-native brands are cultivating loyal communities by emphasizing ingredient transparency, clinical validation, and personalized skincare regimens.

Competitive differentiation is increasingly emerging from speed of innovation and content-led engagement strategies. Independent firms are launching products rapidly in response to social media trends and consumer feedback loops, which is shortening development cycles. Targeted content ecosystems are strengthening customer lifetime value by reinforcing education and brand credibility. As digitally engaged communities are scaling, multinational corporations are responding by accelerating acquisition activity aimed at high-growth niche brands with proven unit economics and scalable digital infrastructure. This acquisition-driven expansion strategy is enabling larger firms to integrate agility and innovation into broader portfolios while preserving operational scale efficiencies.

Key Industry Developments

- In September 2025, Galderma launched Cetaphil's new Skin Activator Hydrating & Firming line, creating a new skincare segment targeting "dermatoporosis" aging skin that appears thinning, fragile, and loose due to dormant surface cells. The proprietary formula uses microdosed mandelic acid (AHA) and encapsulated centella asiatica (CICA) to activate cell turnover and restore moisture barriers.

- In September 2025, Bansk Group, a New York-based consumer brands investment firm, acquired a majority stake in affordable, science-backed skincare brand Byoma from Yellow Wood Partners. Byoma focuses on barrier-strengthening products for transformational results and has become a top-five skincare brand at major retailers, now joining Bansk's portfolio alongside Amika, Eva NYC, and Ethique.

- In February 2025, SmartSKN launched SmartSKN PRO, the first AI-powered platform enabling skincare professionals to offer dermoscopic-grade skin analysis via the Muilli AI Dermascope and real-time, hyper-personalized formulations from 25,000+ options using plant metabolites such as green tea, licorice, and Centella asiatica with liposome delivery for optimal absorption.

Companies Covered in Transformational Skincare Market

- L'Oréal S.A.

- Estée Lauder Companies Inc.

- Unilever PLC

- Procter & Gamble Co.

- Shiseido Company Limited

- AMOREPACIFIC Corporation

- Johnson & Johnson

- Kao Corporation

- Beiersdorf AG

- Coty Inc.

- Avon Products Inc.

- The Ordinary (DECIEM)

- Drunk Elephant

- Cosrx

- Medicube

Frequently Asked Questions

The global transformational skincare market is projected to reach US$ 151.2 billion in 2026.

The market is driven by biotechnology innovations, clean beauty demand, and male grooming adoption fuel sustained premiumization and personalization trends.

The market is poised to witness a CAGR of 7.5% from 2026 to 2033.

Key market opportunities include Asia Pacific expansion, sustainability innovations, and clinical aesthetics convergence.

L'Oréal S.A., Estée Lauder Companies Inc., Unilever PLC, Procter & Gamble Co., and AMOREPACIFIC Corporation are some of the key players in the market.