- Automotive Components & Materials

- Automotive Shock Absorbers Market

Automotive Shock Absorbers Market Size, Trends, Share, and Growth Forecast for 2026 - 2033

Automotive shock absorbers Market by Product Type (Hydraulic, Gas-filled, Adjustable/Electronic, Coilover and Damper), by Design (Twin Tube and Mono Tube), Vehicle Type (Passenger Cars, LCVs, MCVs & HCVs, Two Wheelers and Electric Vehicles), and Sales Channel (OEM, and Aftermarket), and Regional Analysis from 2026 - 2033

Automotive Shock Absorbers Market Size and Trends Analysis

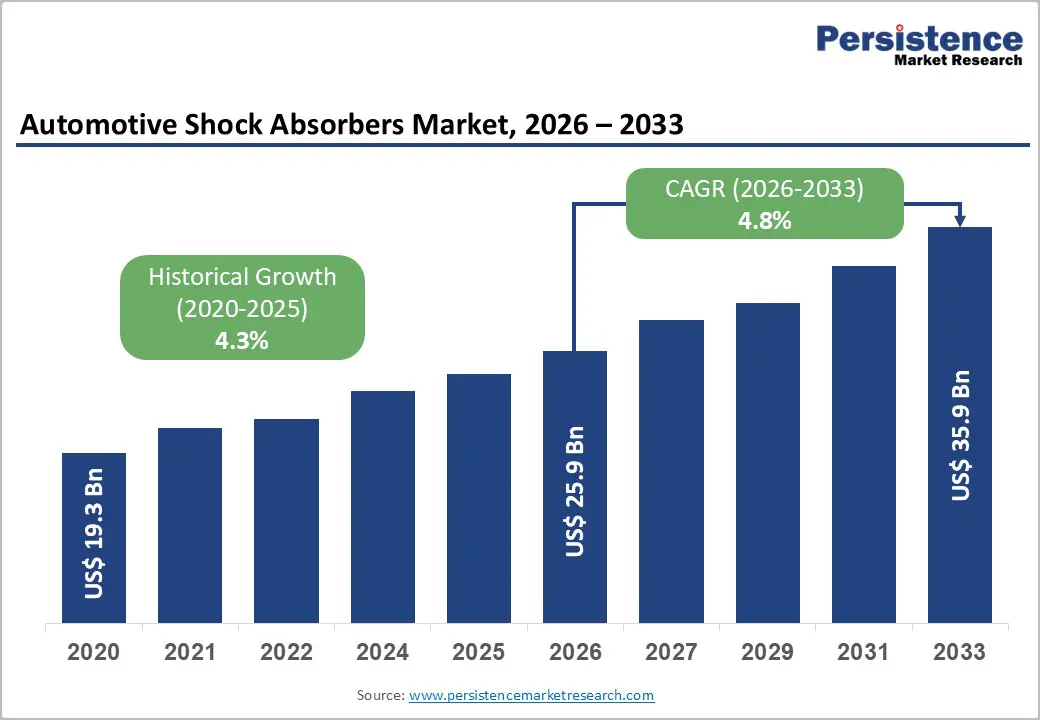

The global automotive shock absorbers market size is likely to be valued at US$ 25.9 billion in 2026 to US$ 35.9 billion by 2033 growing at a CAGR of 4.8% during the forecast period from 2026 to 2033.

Smart suspension systems use sensors and advanced damping algorithms to enhance real-time ride comfort, handling, and stability, driving demand for advanced shock absorber technologies. Integrated electronics enable connectivity with smartphones, allowing features like predictive maintenance, remote diagnostics, and over-the-air software updates for optimized performance.

Key Industry Highlights:

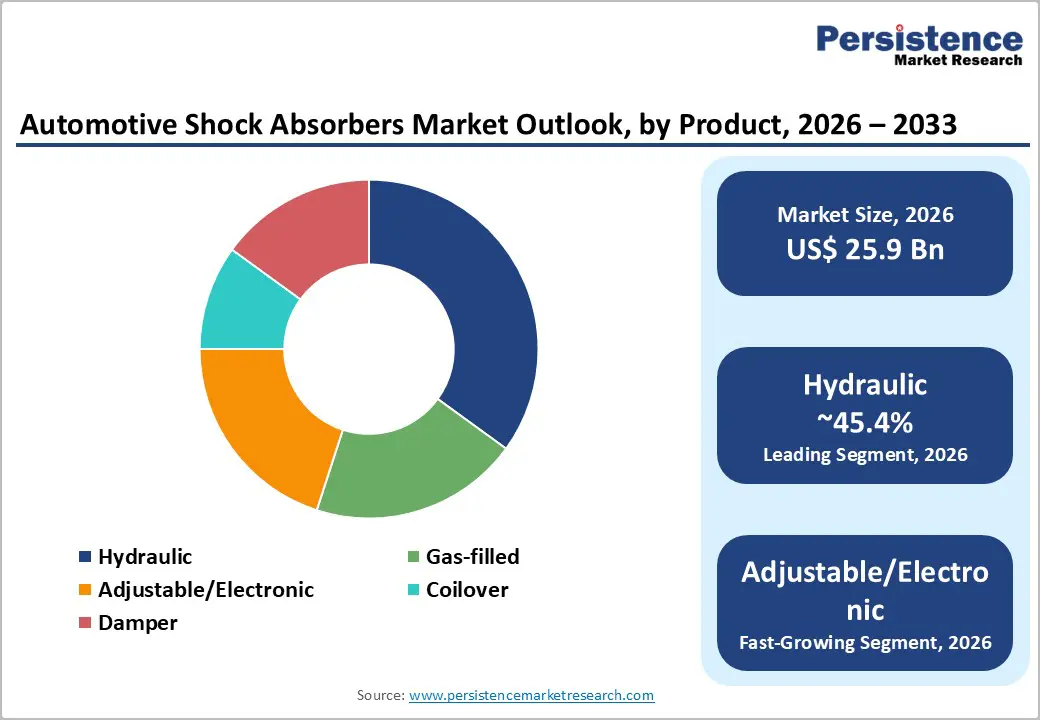

- Leading Product Category: Gas Filled absorbers dominate with 45% market share, while Electronic/Adjustable systems represent fastest-growing segment at 8.5% CAGR, capturing premium positioning and emerging technology adoption across vehicle platforms.

- Design Architecture Dynamics: Monotube designs command 62% market share through superior thermal management and electronic integration capabilities, while Twin-tube architectures expand 5-6% annually, driven by lightweight material applications and specialized platform requirements including electric vehicles and motorcycles.

- Vehicle Application Segmentation: Passenger cars lead with 56.4% share reflecting production scale dominance; electric vehicles emerge as fastest-growing application at 12% CAGR, projecting EV-specific shock absorber market reaching US$ 4.5 billion by 2033 as vehicle electrification accelerates.

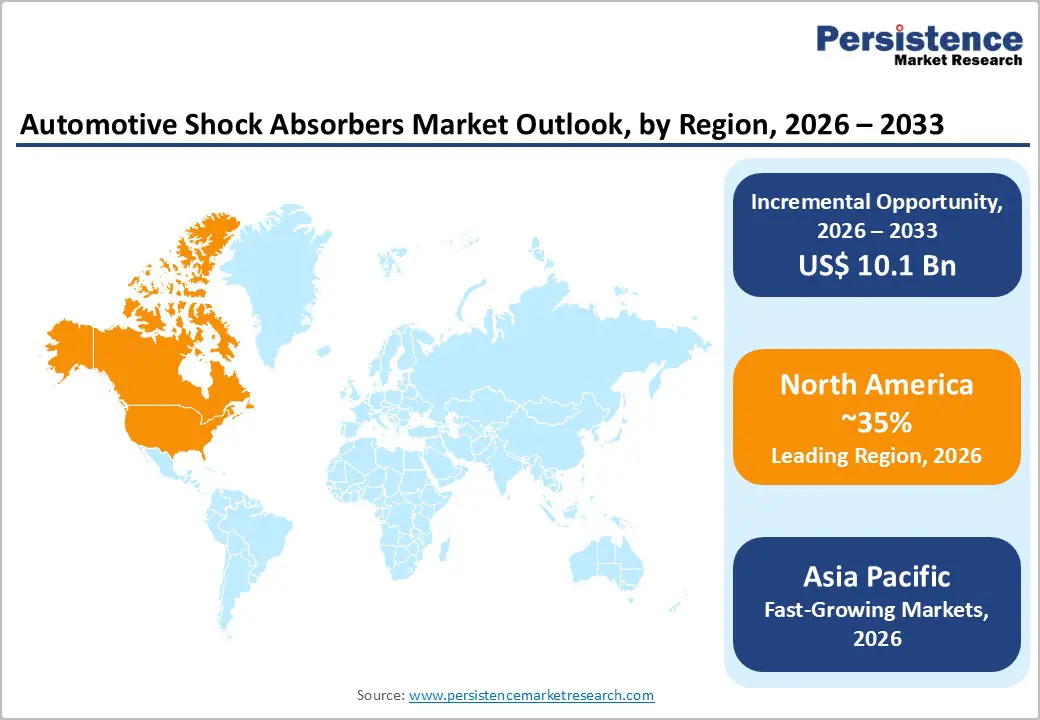

- Geographic Leadership: North America maintains 35% global market share through mature aftermarket and established OEM relationships; Asia-Pacific demonstrates fastest regional growth at 7% CAGR, projected to increase from 25% to 30% global share by 2033, reflecting vehicle production concentration and emerging market expansion.

- Technology Evolution: Electronic damping systems transitioning from premium to mainstream adoption, with market penetration expanding from 35% in developed markets to emerging presence in mid-range platforms; regenerative suspension technology commercialization 2026-2027 creates additional value-capture opportunity in electric vehicle segment.

- Competitive Consolidation: Top 10 suppliers control 60% market share, indicating moderate market concentration with ongoing consolidation pressures on regional manufacturers; investment focus concentrating on Asia-Pacific manufacturing expansion and electronic system capability development supporting OEM relationship differentiation and emerging market supply chain positioning.

| Key Insights | Details |

|---|---|

|

Market Size (2026E) |

US$ 25.9 Bn |

|

Projected Market Value (2033F) |

US$ 35.9 Bn |

|

Forecast Growth Rate (CAGR 2026 to 2033) |

4.8% |

|

Historical Growth Rate (CAGR 2020 to 2025) |

4.2% |

Market Dynamics

Drivers - High Demand for Premium & Luxury Automobiles, and Improved Ride Quality

Increasing population of high-net-worth individuals globally is driving the demand for premium and luxury automobiles. This market trend is attracting international players to invest and expand their presence With strategic activities such as mergers and expansions, the market for automotive shock absorbers is expected to expand further, bringing new products to the market. Customers’ attitudes about comfort and safety in the automotive industry have been evolving. Car suspension is crucial when considering the comfort of the driver and co-passengers. Shock absorbers are referred to as suspension assemblies in cars and offer greater comfort and reliability.

Increasing M&A Activity Between Key Manufacturers

Mergers and acquisition transactions may enable companies to expand their product portfolios by acquiring technologies, intellectual property, or product lines from other firms. This can allow companies to offer a broad range of shock absorber products to meet the diverse needs of customers. These can result in economies of scale, allowing companies to reduce production costs through increased purchasing power, improved operational efficiency, and optimized supply chain management. These cost savings can enhance competitiveness and profitability. Mergers and acquisitions among key market players are allowing them to stay ahead.

- In October 2024, Italian brake manufacturer Brembo announced the acquisition of Swedish suspension specialist Öhlins Racing for $405 million. This strategic move aims to bolster Brembo's position in the automotive market by integrating Öhlins' advanced suspension technologies, including shock absorbers and steering dampers.

Focus on Advancements in Damping Valve Technology

Advanced damping valve technology allows for more precise control over damping forces, resulting in smoother and more comfortable rides for vehicle occupants. This improved ride quality is a significant selling point for consumers, driving demand for vehicles equipped with advanced shock absorbers. A damping valve is fitted at the lower portion of a shock absorber to dampen shocks. Manufacturers of shock absorbers are concentrating on improving the damping effect for luxury vehicles through significant improvements in damping valve technology.

Modern damp valve technology often incorporates adjustable or adaptive features, allowing drivers to customize suspension settings according to their preferences or driving conditions. This customization capability appeals to enthusiasts and performance-oriented drivers, fueling demand for high-performance shock absorbers

Restraint - Fluctuations in Raw Material Prices and Need for Investment-Intensive R&D

Price competition is a significant challenge in the automotive shock absorbers market. Companies often face pressure to offer competitive pricing while maintaining profitability. Fluctuations in raw material costs, currency exchange rates, and intense competition can put downward pressure on shock absorber prices, influencing manufacturers' profit margins.

Rapid pace of technological advancements poses both opportunities and challenges for shock absorber manufacturers. Keeping up with the latest technologies, such as smart shock absorbers, connected systems, and advanced manufacturing processes, requires significant investments in research, development, and production capabilities.

Preferences and buying patterns of people are continually evolving, and companies must stay attuned to these changes. Factors such as increased demand for fuel-efficient shock absorbers, eco-friendly options, and enhanced performance create challenges for manufacturers to adapt their product offerings and meet consumers’ changing expectations.

Opportunity - Growing Demand for Electric and Hybrid Vehicles

The growing demand for better ride quality and comfort, improved safety features, and increased vehicle production rates are the key factors driving the growth of the market. The introduction of advanced technologies such as electronic shock absorbers and adaptive suspension systems is also expected to fuel the growth of the industry in the coming years. In addition, the increasing demand for electric and hybrid vehicles is also expected to create opportunities. EVs and HEVs have unique characteristics compared to traditional internal combustion engine vehicles, such as different weight distribution, lower center of gravity, and quieter operation. Shock absorbers for EVs and HEVs thus need to be specifically designed to accommodate these differences, presenting an opportunity for manufacturers to develop specialized products tailored to the needs of these vehicles.

Category-wise Insights

Passenger Car Record the Maximum Deployment of Shock Absorbers

The passenger car segment dominated the market and is projected to be the faster-growing segment during the forecast period 2026-2033. The growing demand for pickup trucks and vans for commercial use is the main reason propelling the commercial vehicles segment in the worldwide shock absorber market. Additionally, it is anticipated that the increasing demand for commercial vehicles will increase the production of automobile parts and components, such as steering and suspension, high-volume engines, transmissions, and powertrain parts.

Light truck shock absorbers or commercial vehicle shock absorbers are designed to withstand heavier loads and provide durability for vans, pick-up trucks, and light commercial vehicles. These shock absorbers have reinforced sidewalls and tread patterns suitable for commercial applications.

Commercial truck shock absorbers or heavy-duty shock absorbers are specifically designed for large trucks, buses, and other heavy commercial vehicles. They offer high load-carrying capacity, durability, and resistance to wear for long-haul transportation.

Hydraulic Shock Absorbers Segment dominated Shock Absorbers Market

The hydraulic shock absorb segment is projected to dominate the market with approximately USD 14 billion in revenue by 2026. These shock absorbers remain a preferred choice for budget-friendly and mass-market vehicles due to their cost-effective manufacturing and long-standing reliability. Known for their simplicity and proven performance, hydraulic shocks provide effective damping of road vibrations, resulting in a smooth and comfortable ride, an essential feature for consumers prioritizing comfort. Their widespread use and established history in the automotive sector further support their continued demand.

In contrast, gas-filled shock absorbers, typically infused with nitrogen gas, offer superior heat dissipation and enhanced performance under continuous or heavy-duty usage. These characteristics make gas-filled options more appealing to performance-focused drivers seeking improved handling and responsiveness, especially in high-performance or sportier vehicles.

Regional Insights

China to Reach Significant Market Share in Asia Pacific

Asia Pacific is likely to lead the global shock absorber market in 2026. The market in Asia Pacific is projected to record a significant CAGR in the forthcoming years. The market in the region is expanding with increasing automobile sales in China. China has been aggressively promoting the adoption of electric vehicles and new energy vehicles to reduce air pollution, dependence on imported oil, and greenhouse gas emissions. As a result, there is a growing demand for shock absorbers designed for electric and hybrid vehicles, presenting opportunities for manufacturers in the Chinese market to capitalize on this trend.

The market in China is expected to reach US$5.3 Bn by 2033, expanding at a CAGR of 5.4% due to the ever-rising demand for automobiles in the country. Additionally, increasing focus on automotive safety features and implementation of emission norms in the country is further expected to boost market growth.

North America Automotive Shock Absorber Market Trends

The overall demand for shock absorbers is closely tied to the production and sales of vehicles in North America. Factors such as economic conditions, consumer confidence, and new vehicle launches impact the demand for shock absorbers. The North American market has a strong preference for light trucks, SUVs, and crossovers.

The suspension requirements for these vehicles differ from smaller cars, influencing the demand for specific types of shock absorbers designed for larger and heavier vehicles. The popularity of performance and sports cars in North America contributes to the demand for high-performance shock absorbers. Consumers seeking enhanced handling, responsiveness, and a sportier driving experience drive this trend.

Competitive Landscape

Companies invest heavily in research and development to develop advanced shock absorber technologies that offer superior performance, durability, and comfort. Key areas of innovation include adaptive damping systems, lightweight materials, electronic controls, and integration with vehicle dynamics systems.

The market is moderately fragmented, where Tier-I players hold 57% to 58% share of the global market. Gabriel India Limited, Tenneco Inc., ThyssenKrupp AG, KYB Corp., Mando Corporation, and Hitachi Astemo are considered leading players in the market operating with a vast global presence.

Market participants are strategically focusing on the introduction of durable and lightweight materials as well as public and private investments in the automotive, aerospace, and wind turbine sectors to attain higher market shares.

Key Industry Developments:

- In Sept 2024, Tenneco launched a new website, www.monroeridesolutions.com, featuring the company’s full range of electronic and passive suspension technologies chosen by many of the world’s premier light vehicle and commercial truck manufacturers. The Monroe Ride Solutions business is part of Tenneco’s global performance solutions segment

- In January 2024, KYB unveiled a new environment-friendly hydraulic fluid called SustainaLub. This new fluid contributes to carbon neutrality by switching from petroleum derived base oil to naturally derived base oil. It absorbs CO from the atmosphere during the cultivation of the plants used for the base oil raw materials, also reducing CO emissions during transportation.

Companies Covered in Automotive Shock Absorbers Market

- KYB Corporation

- Gabriel India Limited

- Tenneco Inc.

- ThyssenKrupp AG

- Mando Corporation

- Hitachi Astemo, Ltd.

- ITT Inc.

- Duro Shox Pvt Ltd

- ZF Friedrichshafen AG

- Meritor Inc.

- SHOWA Corporation

- Endurance Technologies Ltd.

- Others Key Players

Frequently Asked Questions

The Automotive Shock Absorbers market is estimated to be valued at US$ 25.9 Bn in 2026.

The primary demand for the automotive shock absorbers market is the global expansion of vehicle production and the growing vehicle parc, which increases the need for both OEM installations and aftermarket replacements.

In 2026, the North America region will dominate the market with an exceeding 35% revenue share in the global Automotive Shock Absorbers market.

Among the Vehicle Type, Passenger Cars holds the highest preference, capturing beyond 56.4% of the market revenue share in 2026, surpassing other Vehicle Type.

The key players in Automotive Shock Absorbers are KYB Corporation, Gabriel India Limited, Tenneco Inc. and ThyssenKrupp AG.