- Agrochemicals

- Seed Coating Material Market

Seed Coating Material Market Size, Share, and Growth Forecast, 2025 - 2032

Seed Coating Material Market by Ingredient (Polymers, Additives, Binders), Function (Seed Protection, Seed Enhancement), Process (Film Coating, Encrusting, Pelleting), and Regional Analysis for 2025 - 2032

Seed Coating Material Market Size and Trends Analysis

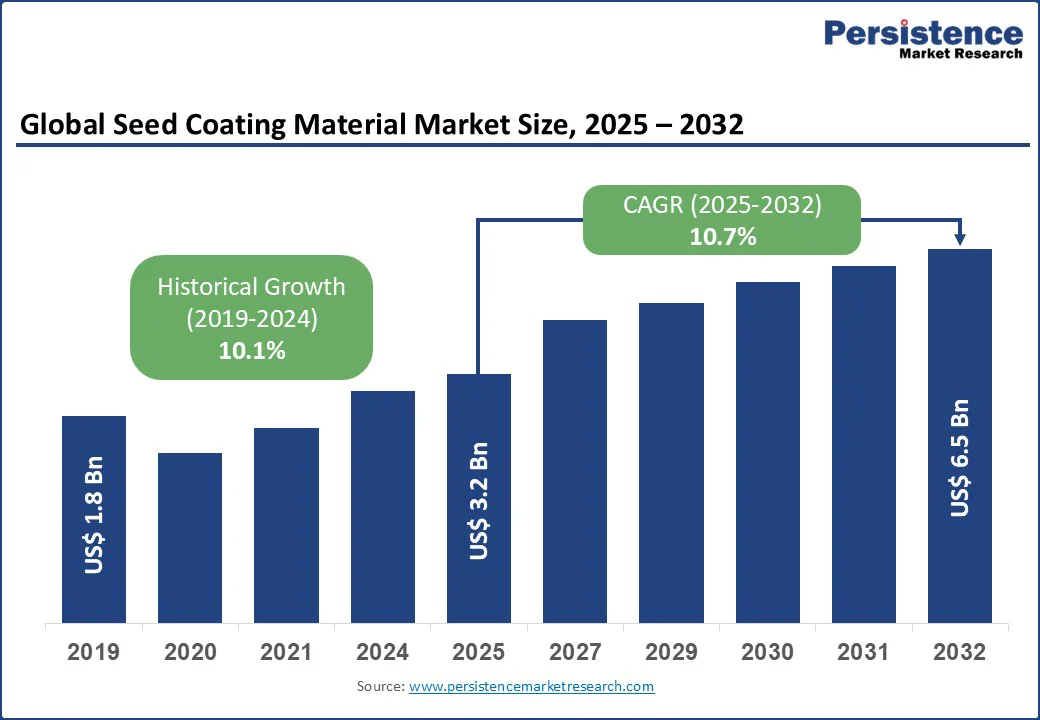

The global seed coating material market size is likely to be valued at US$ 3.2 Bn in 2025 and is expected to reach US$ 6.5 Bn by 2032, growing at a CAGR of 10.7% during the forecast period from 2025 to 2032.

Key Industry Highlights:

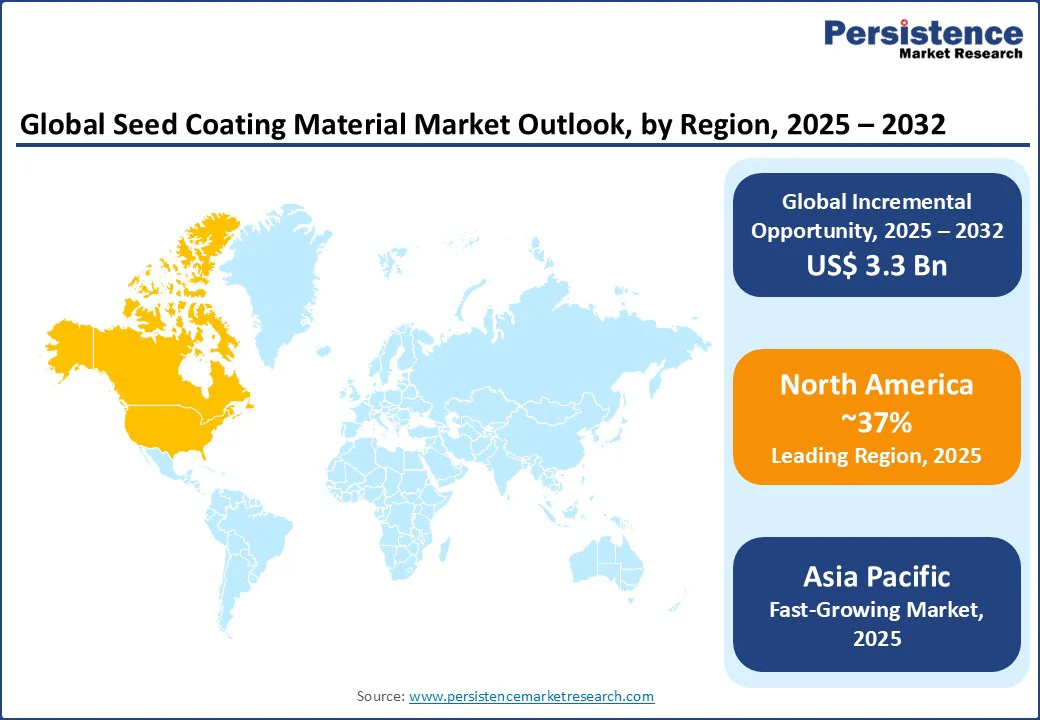

- Leading Region: North America, holding a 37% market share in 2025, driven by advanced agricultural practices, high adoption of seed treatment technologies, and strong demand for high-yield crops in the U.S.

- Fastest-growing Region: Asia Pacific is emerging as the fastest-growing market, fueled by rapid agricultural modernization, increasing government investments in farming infrastructure, and growing demand for coated seeds in countries such as China and India.

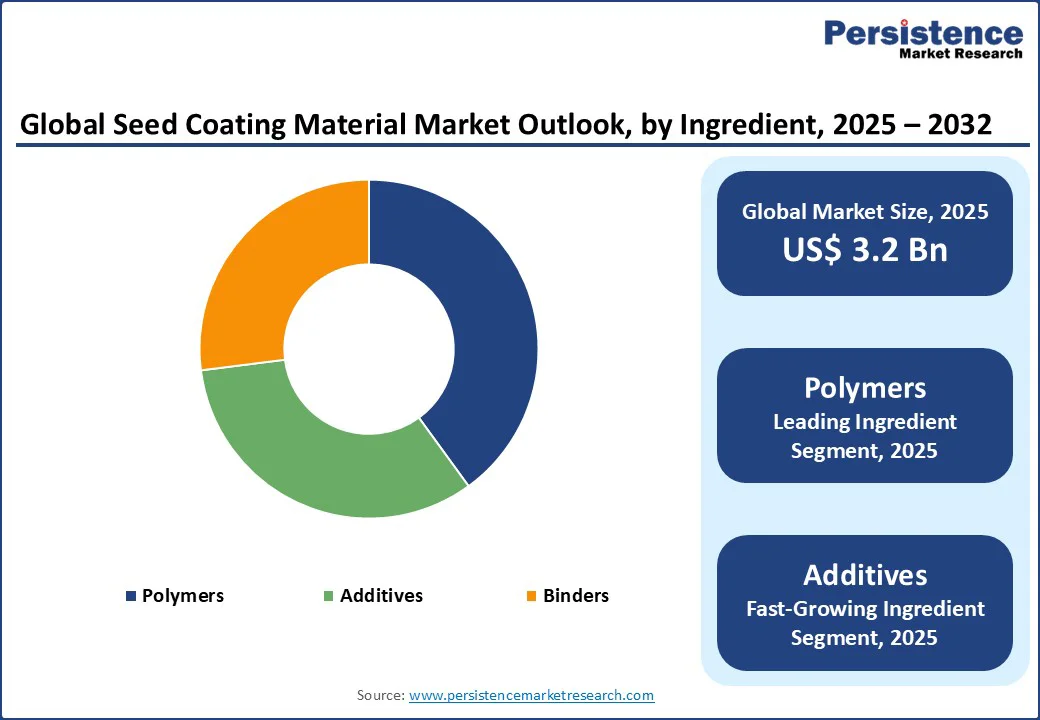

- Dominant Ingredient: Polymers, commanding nearly 40% market share, due to their versatility, cost-effectiveness, and widespread use in enhancing seed performance.

- Leading Function: Seed Protection, accounting for over 62% of market revenue, driven by the need to safeguard seeds from pests, diseases, and environmental stressors.

| Key Insights | Details |

|---|---|

| Seed Coating Material Market Size (2025E) | US$ 3.2 Bn |

| Market Value Forecast (2032F) | US$ 6.5 Bn |

| Projected Growth (CAGR 2025 to 2032) | 10.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 10.1% |

The seed coating material market has witnessed significant growth, driven by the increasing need for enhanced agricultural productivity, rising adoption of precision farming techniques, and advancements in seed treatment technologies.

The demand for high-quality seeds with improved germination rates, disease resistance, and yield potential has significantly boosted market expansion, particularly in agriculture-intensive regions.

Market Dynamics

Driver - Rising Demand for High-yield and Disease-resistant Seeds

The increasing global demand for high-yield and disease-resistant seeds is a primary driver of the seed coating material market. With the global population continuing to expand, there is mounting pressure on the agricultural sector to produce more food using limited arable land.

Farmers are increasingly adopting advanced seed technologies to ensure better crop productivity and resilience. Seed coating plays a vital role in enhancing the performance of high-yield and disease-resistant varieties by providing them with protective layers of polymers, nutrients, and bioactive compounds. These coatings improve seed germination, uniformity in crop establishment, and protection against soil-borne pathogens and pests.

Seed coatings allow precise delivery of fungicides, insecticides, and biological agents, reducing the need for external agrochemical applications and supporting sustainable farming practices. The demand for such advanced solutions is especially strong in regions facing challenges such as climate change, declining soil fertility, and frequent pest infestations.

For instance, in India and China, where food demand is surging and farmers face significant yield losses due to pests and diseases, the adoption of coated hybrid rice and maize seeds has grown rapidly, helping improve productivity and crop resilience. Consequently, the preference for coated seeds is expected to grow steadily, making this driver a major contributor to the global expansion of the seed coating material market.

Restraint - High Costs of Production and Development

The high costs associated with developing and producing seed coating materials pose a significant restraint on market growth. Modern seed coatings often integrate multiple components, including polymers, colorants, micronutrients, and biological agents such as microbes or biostimulants.

Developing these multifunctional formulations requires extensive research, rigorous field trials, and compliance with strict regulatory frameworks, particularly in regions such as the European Union, where environmental and safety standards are stringent.

These activities increase the overall cost of bringing innovative seed coating solutions to market. Additionally, production involves specialized machinery and technologies to ensure uniform application, precision layering, and compatibility with diverse seed types such as cereals, oilseeds, pulses, and vegetables.

Smaller seed producers or companies in emerging markets may find it difficult to invest in such advanced solutions, which limits widespread adoption. For instance, the cost of developing bio-based, microplastic-free seed coatings can be significantly higher than conventional polymer coatings, creating affordability issues for farmers in price-sensitive regions. As a result, while demand is strong, cost barriers continue to challenge both manufacturers and end users, restraining market expansion.

Opportunity - Advancements in biodegradable and smart coating technologies

A significant opportunity shaping the seed coating material market lies in the advancements in biodegradable and smart coating technologies. With growing concerns about environmental sustainability and stringent regulations on microplastics, companies are shifting toward eco-friendly formulations that degrade naturally without leaving harmful residues in the soil.

Biodegradable coatings made from bio-based polymers, starch, and cellulose derivatives not only meet regulatory demands but also appeal to farmers and consumers who are increasingly prioritizing sustainable agriculture practices.

The emergence of smart coating technologies is creating new growth avenues. These advanced coatings are designed to respond to specific soil or environmental conditions, releasing nutrients, growth stimulants, or protective agents at the right time to maximize seed performance. For instance, smart polymers can regulate water absorption and germination based on moisture availability, helping farmers mitigate risks from drought or irregular rainfall.

Such innovations enhance crop productivity, reduce reliance on chemical inputs, and align with precision farming trends. As governments and international bodies push for sustainable food production, the adoption of biodegradable and smart seed coatings is expected to accelerate, offering a strong growth opportunity for market players globally.

Category-wise Analysis

Ingredient Insights

Polymers dominate the seed coating material market, expected to account for approximately 40% of the share in 2025. Their dominance stems from their versatility, cost-effectiveness, and ability to enhance seed performance by improving adhesion, durability, and controlled release of active ingredients.

Polymer-based coatings, offered by companies such as BASF SE and Clariant AG, ensure uniform seed coverage, reduce dust-off, and protect seeds from environmental stressors, making them a preferred choice for large-scale farming and precision agriculture. Their compatibility with mechanized planting systems further drives adoption in commercial agriculture.

The additives segment is the fastest-growing, driven by the increasing demand for bioactive ingredients, such as fungicides, insecticides, and micronutrients, that enhance seed protection and growth.

Additives improve seed resilience against pests and diseases, with products such as Syngenta’s seed treatment additives reporting a 25% reduction in early-stage crop losses. The growing focus on sustainable agriculture and the integration of bio-based additives, such as plant growth promoters, is accelerating adoption, particularly in North America and the Asia Pacific.

Function Insights

Seed protection leads the seed coating material market, holding a 62% share in 2025. The segment’s dominance is driven by the critical need to safeguard seeds from pests, diseases, and environmental stressors, such as drought and extreme temperatures.

Protective coatings, incorporating fungicides and insecticides, ensure higher germination rates and reduce crop losses, making them essential for high-value crops such as corn and soybeans. Companies such as Bayer CropScience and Incotec Group offer advanced protective coatings that improve seed survival.

The seed enhancement segment is the fastest-growing, fueled by the rising demand for coatings that improve germination, nutrient uptake, and crop yield. Enhancers, such as growth promoters and micronutrients, are increasingly used in precision farming to optimize seed performance.

The adoption of smart coatings, which release nutrients based on environmental triggers, is driving rapid growth in this segment, particularly in regions with advanced agricultural systems such as North America and Europe.

Process Insights

Film coating dominates the seed coating material market, accounting for approximately 53% share in 2025. Its dominance is driven by its cost-effectiveness, ease of application, and ability to provide uniform coverage with minimal material usage.

Film coating, offered by companies such as Germains Seed Technology and Precision Laboratories, enhances seed handling, reduces dust-off, and improves planting efficiency, making it ideal for large-scale agriculture and mechanized planting systems.

The pelleting is the fastest-growing segment driven by its ability to standardize seed size and shape, improving planting accuracy and uniformity. Pelleting is particularly popular for small-seeded crops, such as vegetables and flowers, where precise planting is critical. The increasing adoption of precision agriculture in the Asia Pacific and Europe, coupled with advancements in pelleting technologies, is accelerating growth in this segment.

Regional Insights

North America Seed Coating Material Market Trends

North America is expected to hold around 37% of the global seed coating material market share in 2025, making it the dominant region. This leadership is largely attributed to the region’s advanced agricultural practices, extensive use of mechanized farming systems, and the high adoption of seed treatment technologies.

The United States, in particular, plays a central role, with large-scale cultivation of crops such as corn, soybeans, wheat, and canola, which are increasingly supplied as treated or coated seeds. According to the USDA, U.S. corn acreage alone accounts for over 90 million acres annually, where coated hybrid seeds help improve germination, protect against pests, and boost yield potential.

The strong focus on high-yield and disease-resistant crop varieties has fueled the adoption of multifunctional coatings that combine polymers, micronutrients, and bio-protectants. Companies such as BASF, Bayer, and Syngenta have significant market presence in the region, continuously investing in R&D to introduce eco-friendly and precision-based coating solutions.

Additionally, the rising trend of sustainable agriculture and compliance with EPA regulations are encouraging the adoption of biodegradable and low-toxicity coatings, further strengthening North America’s dominance in the seed coating material market.

Europe Seed Coating Material Market Trends

Europe is emerging as a significant player in the seed coating material market, supported by strong agricultural frameworks and collaborative research initiatives. Leading countries, including Germany, France, and the Netherlands, are driving market growth through extensive investments in sustainable agriculture and seed treatment technologies.

The European Union’s Farm to Fork Strategy, aiming to reduce pesticide use, is fueling demand for eco-friendly seed coatings, such as biodegradable polymers and bio-based additives. Companies such as Syngenta AG and Clariant AG are at the forefront of developing innovative coatings that comply with stringent EU regulations.

The region’s focus on high-value crops, such as cereals and vegetables, and the adoption of precision farming techniques are driving demand for advanced seed coating materials. The Netherlands, a hub for seed technology, is driven by demand for pelleted seeds. Europe’s emphasis on sustainability and regulatory compliance ensures steady market growth, positioning the region as a key player in the seed coating material market.

Asia Pacific Seed Coating Material Market Trends

Asia Pacific is emerging as the fastest-growing market for seed coating materials, driven by a combination of rapid agricultural modernization, expanding government support, and rising demand for high-quality seeds.

Countries such as China, India, and Southeast Asian nations are witnessing a significant transformation in their farming practices, with an increasing shift from traditional methods to mechanized and precision agriculture techniques. This modernization has accelerated the adoption of coated seeds, which offer better germination rates, uniform crop establishment, and protection against pests and diseases.

Government initiatives and investments play a crucial role in supporting this growth. In India, for example, programs promoting high-yielding seed varieties, integrated pest management, and sustainable farming technologies have encouraged farmers to adopt coated seeds. Similarly, China’s focus on improving crop productivity and food security has led to large-scale use of hybrid and treated seeds for major crops such as rice, maize, and wheat.

The rising awareness of eco-friendly and biodegradable seed coatings has also boosted market growth, as farmers seek sustainable solutions that reduce environmental impact. Overall, these factors collectively position the Asia-Pacific region as the fastest-growing market, with strong potential for continued expansion throughout the forecast period.

Competitive Landscape

The global Seed Coating Material Market is characterized by intense competition, regional strengths, and a mix of global and niche players. In developed regions such as North America and Europe, large firms such as BASF SE, Bayer CropScience AG, and Syngenta AG dominate through scale, advanced R&D capabilities, and established partnerships with agricultural agencies.

In the Asia Pacific, rapid agricultural developments and increasing demand for coated seeds are attracting significant investments from both international players, such as Croda International plc and Clariant AG, and regional vendors. Companies are focusing on product innovation, eco-friendly coatings, and strategic alliances to gain a competitive edge.

The development of biodegradable and smart coating technologies has emerged as a key differentiator, enabling faster adoption in agriculture-intensive regions. Strategic collaborations, acquisitions, and digital-first approaches for supply chain and marketing are further intensifying the competitive landscape.

The industry exhibits a dual nature, consolidated at the top by global giants while remaining fragmented across numerous regional and niche players catering to local preferences and cost-sensitive segments.

Key Developments:

- In October 2024, Incotec Group launched Disco Blue L-1523, a microplastic-free film coating for sunflower seeds at the Euroseeds Congress, offering enhanced dust control and seed flow, aligned with EU sustainability goals.

- In November 2023, BASF SE launched Flo Rite Pro 02, an advanced seed coating polymer enhancing seed flow and planting precision.

Companies Covered in Seed Coating Material Market

- BASF SE

- Bayer CropScience AG

- Syngenta AG

- Croda International plc

- Clariant AG

- Incotec Group

- Germains Seed Technology

- Sensient Technologies Corporation

- Precision Laboratories LLC

- BrettYoung Seeds Ltd.

- Chromatech Incorporated

- Centor Oceania

- Others

Frequently Asked Questions

The global seed coating material market is projected to reach US$ 3.2 Bn in 2025.

The increasing demand for high-yield and disease-resistant seeds is a key driver.

The seed coating material market is poised to witness a CAGR of 10.7% from 2025 to 2032.

Advancements in biodegradable and smart coating technologies are a key opportunity.

BASF SE, Bayer CropScience AG, Syngenta AG, Croda International plc, and Clariant AG are key players.